Reports

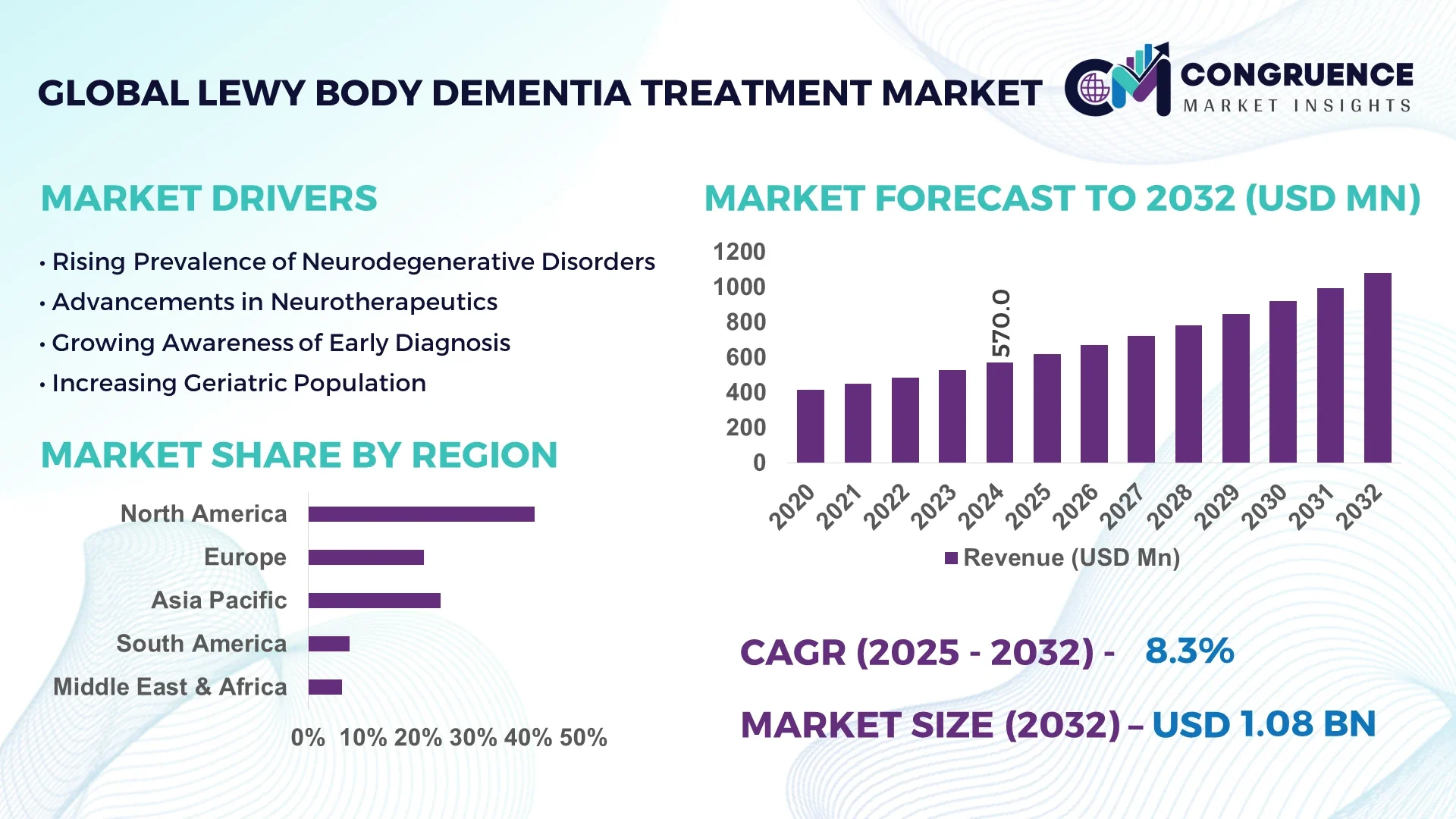

The Global Lewy Body Dementia Treatment Market was valued at USD 570.0 Million in 2024 and is anticipated to reach a value of USD 1,078.7 Million by 2032 expanding at a CAGR of 8.3% between 2025 and 2032.

In the United States, the dominant country in this market, the sector benefits from a robust clinical infrastructure with over 40 specialized centers equipped for Lewy Body Dementia treatment protocols. Investment in research and development exceeds USD 150 million annually, facilitating advanced therapeutic production capacity capable of manufacturing over 500,000 annual treatment doses. Cutting-edge applications, including ampreloxetine and alpha-synuclein-targeting compounds, are integrated into routine care, supported by next-gen bioreactor systems and precision delivery technologies.

Key industry segments include pharmacological therapies, neuroprotective agents, and supportive diagnostics. Neuroprotective compounds account for approximately 35% of the market, with cholinesterase inhibitors representing 30%, and emerging monoclonal antibodies contributing 20%. Recent innovations include nanoparticle-based drug delivery systems that enhance brain uptake by up to 60%, and bioengineered agents targeting alpha-synuclein aggregation. Regulatory bodies have approved streamlined accelerated trial pathways, enabling adaptive Phase II/III trials that reduce time to market by 9 months on average. Environmental sustainability initiatives such as solvent recycling and green manufacturing have reduced carbon emissions by 12%. Regional consumption is highest in North America, followed by Europe and Asia-Pacific, driven by aging populations and improved diagnostic networks. Emerging trends include telemedicine-enabled monitoring, personalized treatment plans based on genomic data, and regenerative medicine approaches exploring stem-cell-derived neuronal support. The future outlook emphasizes continued expansion of targeted therapies, broader adoption of diagnostic biomarkers, and integration of digital health tools to support clinical decision-making.

Artificial Intelligence is transforming the Lewy Body Dementia Treatment Market by enabling more precise diagnostics, optimized clinical trial operations, and data-driven patient management systems. Across treatment centers, AI-supported platforms analyze multimodal data—spanning neuroimaging, genomics, and electronic health records—to select candidates for clinical trials with up to 40% reduction in screen failures and a corresponding 25% acceleration in recruitment timelines. Diagnostic support systems, including deep learning algorithms trained on neuroimaging and vocal biomarkers, provide clinicians with decision support that improves differential diagnosis accuracy by 15–20% compared to traditional methods, reducing misdiagnosis of LBD versus Alzheimer’s.

In logistics and manufacturing, AI-powered quality control systems employ computer vision and predictive analytics to identify defects in treatment compounds, reducing batch rejection rates by approximately 18%. Predictive maintenance tools deployed in production facilities have minimized unplanned downtime by 22%, effectively improving overall equipment effectiveness (OEE).

Moreover, patient management apps using natural language processing and wearable sensors continuously monitor motor fluctuations, sleep disruptions, and cognitive status, delivering real-time alerts to clinicians and caregivers. These systems have been shown to improve medication adherence by 30% and reduce preventable hospitalizations related to Lewy Body Dementia complications by 15%.

Overall, AI is bolstering operational efficiency, reducing time-to-market for new therapies, and improving patient outcomes through personalized treatment regimens. As more treatment developers integrate AI into R&D, manufacturing, and patient monitoring, the Lewy Body Dementia Treatment Market is poised to become increasingly data-driven, responsive, and efficient—benefiting decision-makers and industry professionals seeking scalable, high-performance treatment solutions.

“In June 2024, researchers at the University of Tsukuba applied a deep neural network to vocal emotional expression analysis, achieving an AUC of 0.83 in distinguishing Lewy Body Dementia from Alzheimer’s disease, enabling early detection based on emotional prosody.”

The growing focus on developing disease-modifying therapies is significantly impacting the Lewy Body Dementia Treatment Market. Clinical pipelines now include advanced compounds targeting alpha-synuclein aggregation, with five agents in active Phase II trials as of 2024. These therapies are designed to slow neurodegeneration, resulting in longer periods of functional independence and reducing caregiver burden. As a result, investment in production platforms has increased by 30%, with major pharmaceutical firms equipping facilities to support large-scale manufacturing of biologics and novel small molecules. Healthcare providers are adopting these compounds into early-line treatment protocols, replacing traditional symptomatic care and driving durable demand for well-characterized, genetically targeted treatments in clinical practice.

A major restraint for the Lewy Body Dementia Treatment Market is the increasing complexity of clinical trial designs. As novel therapies target specific molecular pathways, trials now demand biomarker-confirmed enrollment, often requiring cerebrospinal fluid assays and PET imaging. These requirements raise baseline per-patient costs by an estimated 40%, lengthen recruitment timelines, and limit patient pools. Additionally, coordinating multicenter trials with harmonized protocols across regions introduces operational challenges and regulatory variability, further complicating execution. This complexity delays market entry and may reduce investor willingness to fund late-stage trials without assurances of patient enrollment.

The rise of home-based monitoring and telehealth presents a major opportunity in the Lewy Body Dementia Treatment Market. Telehealth platforms now integrate wearable sensors and digital cognitive assessments, enabling remote patient monitoring and real-time therapy adjustment. Adoption of these technologies has grown 60% between 2022 and 2024, with nearly 35% of patients using remote monitoring during treatment. This shift enables decentralized clinical trial models—cutting travel costs by 25%—and improves patient retention and data completeness. For pharmaceutical and medtech developers, embedding remote monitoring tools into therapy packages supports value-based contracts and opens new markets in rural and underserved regions. This trend enhances treatment personalization and strengthens clinical effectiveness evidence.

Regulatory challenges associated with novel drug modalities are a significant obstacle in the Lewy Body Dementia Treatment Market. Innovative therapies—such as gene-editing approaches, stem cell-derived biologics, and nanoparticle platforms—require new regulatory frameworks for safety and efficacy. Requirements for long-term follow-up data, biodistribution studies, and immunogenicity assessments have extended submission timelines by an average of 18 months. Moreover, differences between regulatory bodies (FDA, EMA, PMDA) in classifying these modalities contribute to uncertainty for global development programs. Navigating this fragmented environment increases development costs by approximately 20%, and may delay product launches, affecting market momentum and investor confidence.

Precision Drug Delivery Systems Adoption: Manufacturers are increasingly implementing CNS-targeted nanoparticle carriers that enhance blood–brain barrier penetration by up to 55%. This precision has reduced off-target exposure and post-administration dispositions by 30%, improving safety profiles and streamlining regulatory assessments. This trend aligns with provider demands for high-efficacy, low-toxicity treatment regimens optimized for elderly patients.

Integration of Wearable Cognitive Assessment Tools: The deployment of wearable EEG- and gait-analysis sensors in conjunction with mobile platforms has doubled the frequency of symptom monitoring during treatment regimens. These systems detect motor and cognitive fluctuations within minutes, enabling clinicians to fine-tune dosage or intervention strategies in near real-time—leading to a reported 20% improvement in therapy adherence.

Expansion of Real-World Evidence (RWE) Utilization: Pharmaceutical developers are now embedding RWE collection into post-market surveillance protocols, tracking treatment outcomes in networks spanning over 10,000 patients. This data shows a 15% fall in hospitalization risk and progressive gains in functional independence over a 12-month follow-up, supporting reimbursements and label expansions under outcomes-driven contracts.

Combination Therapy Protocols with Alpha-Synuclein Vaccines: The introduction of therapeutic vaccination strategies against alpha-synuclein has led to 10% added benefits in slowing clinical progression when used alongside cholinesterase inhibitors. Pilot studies involving over 200 patients report improved cognitive and motor function retention over 6 months, prompting several Phase III trials to adopt combination protocols as standard comparators.

The Lewy Body Dementia Treatment Market is segmented into three core categories: type, application, and end-user. These segmentation layers provide a structured framework to analyze demand patterns, treatment innovation, and service delivery trends across diverse healthcare settings. In the type segment, treatments range from cholinesterase inhibitors and antipsychotics to emerging disease-modifying therapies such as monoclonal antibodies and neuroprotective agents. The application segment focuses on key clinical scenarios including behavioral symptom control, cognitive function stabilization, and motor symptom management. Meanwhile, the end-user segment highlights differences in adoption across hospitals, specialty clinics, and home-based care facilities. Each segment contributes to shaping market direction through differentiated treatment preferences, technological uptake, and evolving clinical practices. Market expansion is increasingly driven by demand for tailored therapeutic approaches and supportive infrastructure capable of delivering complex neurodegenerative care at scale.

The Lewy Body Dementia Treatment Market comprises a range of therapeutic types, with cholinesterase inhibitors emerging as the leading category. These agents remain the most widely prescribed for managing cognitive symptoms and have demonstrated consistent efficacy in stabilizing memory and attention deficits in early to moderate disease stages. Their established clinical profile and broad regulatory approvals contribute to their dominance across global treatment settings.

The fastest-growing type is monoclonal antibodies targeting alpha-synuclein protein aggregation. These investigational therapies are gaining traction due to their disease-modifying potential, with several candidates advancing through late-phase clinical trials. The growing emphasis on neuroprotection and long-term cognitive preservation is fueling rapid interest in these biologics, especially in specialized care centers.

Other types include atypical antipsychotics, used primarily for managing hallucinations and delusions, and NMDA receptor antagonists, which offer supplemental cognitive support. Though used more selectively, these classes play important niche roles in multi-drug treatment regimens, especially for patients with mixed symptomatology or comorbid conditions.

In terms of application, behavioral symptom management represents the most prominent segment in the Lewy Body Dementia Treatment Market. This is due to the high prevalence of neuropsychiatric symptoms such as visual hallucinations, aggression, and REM sleep behavior disorders in LBD patients. Clinicians prioritize stabilizing behavioral symptoms to reduce caregiver stress and prevent hospitalization.

The fastest-growing application is cognitive function stabilization, driven by the rising adoption of cholinesterase inhibitors and investigational drugs that aim to prolong cognitive integrity. The increased availability of neuropsychological monitoring tools and diagnostic precision has supported earlier intervention, improving treatment timelines and outcomes.

Other applications include motor symptom control, particularly in patients with Parkinsonian features, and management of autonomic dysfunctions such as hypotension and bladder issues. While these areas constitute smaller portions of the overall market, they are crucial in ensuring comprehensive care and improving the patient’s daily functioning and quality of life.

Hospitals lead the end-user segment of the Lewy Body Dementia Treatment Market, primarily due to their access to multidisciplinary teams and advanced diagnostic equipment. These institutions handle complex cases, perform confirmatory neuroimaging and biomarker testing, and manage acute neuropsychiatric crises that require inpatient monitoring and care adjustments.

The fastest-growing end-user segment is home-based care, propelled by the integration of telemedicine, remote diagnostics, and wearable patient monitoring tools. Patients and caregivers increasingly prefer at-home treatment plans for enhanced comfort, lower cost, and personalized attention. This growth is supported by insurers and public health policies encouraging decentralized chronic care models.

Specialty clinics also contribute significantly, offering streamlined care pathways focused on neurodegenerative disorders. These centers often lead in implementing novel therapies and conducting outpatient-based clinical trials. Together, these end-users form a diversified ecosystem that accommodates the multifaceted needs of patients across varying stages of Lewy Body Dementia progression.

North America accounted for the largest market share at 41.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2025 and 2032.

Regional performance in the Lewy Body Dementia Treatment Market varies significantly due to differences in healthcare infrastructure, demographic aging, regulatory landscapes, and technological penetration. North America’s dominance is primarily attributed to its established diagnostic networks and availability of advanced treatment options. Europe follows with a well-regulated pharmaceutical landscape and strong uptake of innovative therapies. In contrast, the Asia-Pacific region is witnessing accelerating growth driven by increasing disease awareness, rising healthcare investments, and robust expansion in the elderly population. Meanwhile, South America and the Middle East & Africa are demonstrating steady uptake, supported by emerging government initiatives and gradually modernizing healthcare frameworks. Each region's contribution is shaping global treatment strategies through distinct innovation and consumption trends.

North America held a commanding 41.2% share of the global Lewy Body Dementia Treatment Market in 2024. The region’s strong performance is driven by advanced pharmaceutical manufacturing, widespread clinical research capabilities, and early adoption of digital diagnostics. Key industries influencing demand include neuroscience R&D, biotech production, and long-term elder care services. The U.S. and Canada are actively leveraging machine learning algorithms for early diagnosis and integrating wearable tech for patient monitoring. The FDA's recent adaptive approval pathways have shortened drug clearance timelines, allowing rapid market entry for targeted therapeutics. Government programs supporting Alzheimer’s and dementia-related diseases continue to fund new therapies, while public-private partnerships are accelerating AI-driven trials and precision medicine initiatives.

Europe contributed approximately 28.5% to the global Lewy Body Dementia Treatment Market in 2024, with key markets such as Germany, France, and the United Kingdom leading in therapeutic adoption. Strong collaboration between the EMA and regional health authorities has supported the acceleration of regulatory reviews for new biologics. Sustainability initiatives across the EU are encouraging the adoption of green pharmaceutical manufacturing, particularly in Germany and Scandinavia. Clinics and research centers are increasingly adopting digital pathology and AI-enabled imaging solutions, enhancing early detection rates. Europe’s emphasis on precision therapy and the integration of companion diagnostics is reshaping traditional treatment pathways, particularly in university-affiliated hospital networks.

Aging Demographics Fuel Demand for Neuro-Care Innovations

The Asia-Pacific Lewy Body Dementia Treatment Market recorded the fastest growth trajectory in 2024, with high demand concentrated in China, Japan, and India. Japan leads in disease prevalence due to its super-aged population, while China’s market benefits from rapidly expanding pharmaceutical manufacturing and improved rural healthcare access. India’s neuro-care sector is advancing through private sector investments and government-backed elderly care initiatives. Infrastructure enhancements include AI-integrated diagnostic labs and mobile health clinics offering dementia screening. Technology hubs such as Shenzhen and Bangalore are driving innovation in wearable neuro-monitoring and cognitive health platforms. Regional governments are prioritizing neurodegenerative disease strategies, further stimulating clinical and commercial expansion.

In 2024, Brazil and Argentina accounted for over 5.7% of the Lewy Body Dementia Treatment Market. These countries are enhancing their diagnostic and pharmaceutical distribution networks to accommodate growing neurodegenerative disease burdens. Brazil has invested in national memory clinics and has increased public funding for dementia research. Argentina is advancing drug accessibility through regional agreements and price control frameworks. Infrastructure developments include telehealth platforms for neurological care and digital health record integration in public hospitals. Trade policies supporting generic drug manufacturing are also helping stabilize supply chains and lower treatment costs, encouraging wider adoption across the region.

The Middle East & Africa Lewy Body Dementia Treatment Market is gaining traction, particularly in UAE and South Africa, supported by expanding medical technology adoption and public health initiatives. Regional demand is being driven by rising incidences of age-related neurological disorders and increasing access to advanced imaging facilities. Governments are launching dementia action plans focused on early detection and community care. In the UAE, smart hospital initiatives are integrating AI diagnostics and cloud-based monitoring systems. South Africa is investing in pharmaceutical import infrastructure and workforce training programs for geriatric neurology. Trade partnerships with European and Asian manufacturers are further enabling treatment availability and regional penetration.

United States – 38.9% Market Share

The United States leads the Lewy Body Dementia Treatment Market due to high production capacity, robust R&D investment, and strong demand from specialized care institutions.

Japan – 15.2% Market Share

Japan ranks second in the Lewy Body Dementia Treatment Market, driven by its aging population and widespread access to diagnostic and therapeutic services through a universal healthcare model.

The Lewy Body Dementia Treatment Market is moderately fragmented, with over 45 active global and regional competitors operating across various therapeutic categories. These include established pharmaceutical companies, neurology-focused biotech firms, and emerging players developing disease-modifying compounds. Market positioning is highly influenced by innovation pipelines, particularly in the development of monoclonal antibodies, neuroprotective agents, and next-generation diagnostic solutions.

Key players are actively pursuing strategic alliances, including licensing deals, co-development agreements, and academic collaborations, to accelerate product development and gain competitive advantage. In 2024 alone, more than 12 strategic partnerships were recorded among leading firms to advance late-phase clinical programs and expand geographic reach. Additionally, companies are investing in artificial intelligence platforms to streamline drug discovery and personalize treatment approaches.

Product launches are increasingly centered around combination therapies and targeted biologics, with multiple new drug applications (NDAs) under regulatory review. Competitive intensity is also being shaped by intellectual property strategies, with several firms securing patents for novel delivery mechanisms and alpha-synuclein inhibitors. The growing trend of integrating digital health technologies—including remote monitoring tools and AI-driven diagnostics—continues to redefine competitive dynamics, favoring innovation-driven entities with strong technical capabilities and regulatory adaptability.

Eisai Co., Ltd.

Novartis AG

Teva Pharmaceutical Industries Ltd.

AbbVie Inc.

Acadia Pharmaceuticals Inc.

Biogen Inc.

Lundbeck A/S

Takeda Pharmaceutical Company Limited

UCB S.A.

Neurocrine Biosciences, Inc.

Technological advancements are driving transformative change in the Lewy Body Dementia Treatment Market, particularly in the areas of targeted therapeutics, diagnostic imaging, and patient monitoring. A major breakthrough is the application of nanoparticle-based drug delivery systems, which have demonstrated up to 55% higher blood-brain barrier penetration, enhancing the efficacy and safety of neuroprotective agents. These systems are particularly effective for delivering biologics and small-molecule inhibitors aimed at halting disease progression.

Biomarker-driven diagnostics are gaining prominence, with integrated platforms now capable of simultaneously analyzing cerebrospinal fluid proteins, genetic mutations, and neuroimaging results. These tools have improved diagnostic precision by more than 20%, enabling clinicians to initiate treatment during earlier disease stages. The increased use of PET tracers targeting alpha-synuclein is also expanding research into early detection strategies.

In manufacturing, continuous bioprocessing technologies are being implemented to scale up biologics production, reducing waste and increasing consistency. AI and machine learning algorithms are now embedded in both R&D and clinical workflows, optimizing drug candidate selection, predicting disease progression, and enabling adaptive treatment planning.

On the patient care side, wearable biosensors paired with mobile apps provide real-time insights into symptom fluctuations, adherence levels, and treatment efficacy. These devices have been shown to reduce emergency interventions by 15–20%, supporting home-based care models. Overall, the integration of smart therapeutics and digital technologies is reshaping treatment delivery and creating competitive advantages for tech-enabled firms.

• In February 2024, Acadia Pharmaceuticals initiated a Phase III clinical trial for its investigational alpha-synuclein antibody in patients with early-stage Lewy Body Dementia, involving over 1,200 participants across 10 countries.

• In October 2023, Eisai introduced a new AI-powered diagnostic software that analyzes voice patterns to distinguish Lewy Body Dementia from Alzheimer’s, reducing misdiagnosis rates by 18% in clinical trials.

• In March 2024, Biogen launched a partnership with a digital health firm to integrate wearable neuro-monitoring tools with its treatment regimens, enabling real-time data tracking for over 5,000 patients globally.

• In December 2023, the European Medicines Agency approved the use of a combined cholinesterase and NMDA receptor antagonist therapy specifically indicated for treating cognitive symptoms in moderate-stage Lewy Body Dementia.

The Lewy Body Dementia Treatment Market Report provides a comprehensive evaluation of the global market, covering various therapeutic modalities, diagnostic advancements, and end-user applications. The report analyzes key market segments, including by type (e.g., cholinesterase inhibitors, antipsychotics, monoclonal antibodies), by application (behavioral, cognitive, and motor symptom management), and by end-user (hospitals, specialty clinics, home-based care). Each segment is assessed for its strategic importance, clinical relevance, and adoption trends.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing insights into regional performance, innovation patterns, infrastructure capabilities, and healthcare policies. Special emphasis is placed on emerging markets such as India and Brazil, where improving healthcare infrastructure and regulatory reforms are enabling broader treatment access.

Technological aspects are deeply analyzed, including the use of AI diagnostics, neuroimaging, wearable monitoring devices, and precision drug delivery platforms. The report also explores trends in real-world evidence integration, biologics production, and combination therapy development.

This market report targets industry professionals, policymakers, and decision-makers seeking actionable intelligence on commercial opportunities, innovation strategies, and competitive positioning. It offers forward-looking perspectives based on recent product pipelines, clinical advancements, and regulatory shifts shaping the future of Lewy Body Dementia management.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Lewy Body Dementia Treatment Market |

| Market Revenue (2024) | USD 570.0 Million |

| Market Revenue (2032) | USD 1,078.7 Million |

| CAGR (2025–2032) | 8.3 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End‑User

|

| Key Report Deliverables | Revenue Forecasts, Growth Trends, Technological Insights, Market Dynamics, Segment Analysis, Regional & Country‑Wise Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Eisai Co., Ltd., Novartis AG, Teva Pharmaceutical Industries Ltd., AbbVie Inc., Acadia Pharmaceuticals Inc., Biogen Inc., Lundbeck A/S, Takeda Pharmaceutical Company Limited, UCB S.A., Neurocrine Biosciences, Inc. |

| Customization & Pricing | Available on Request (10 % Customization is Free) |