Reports

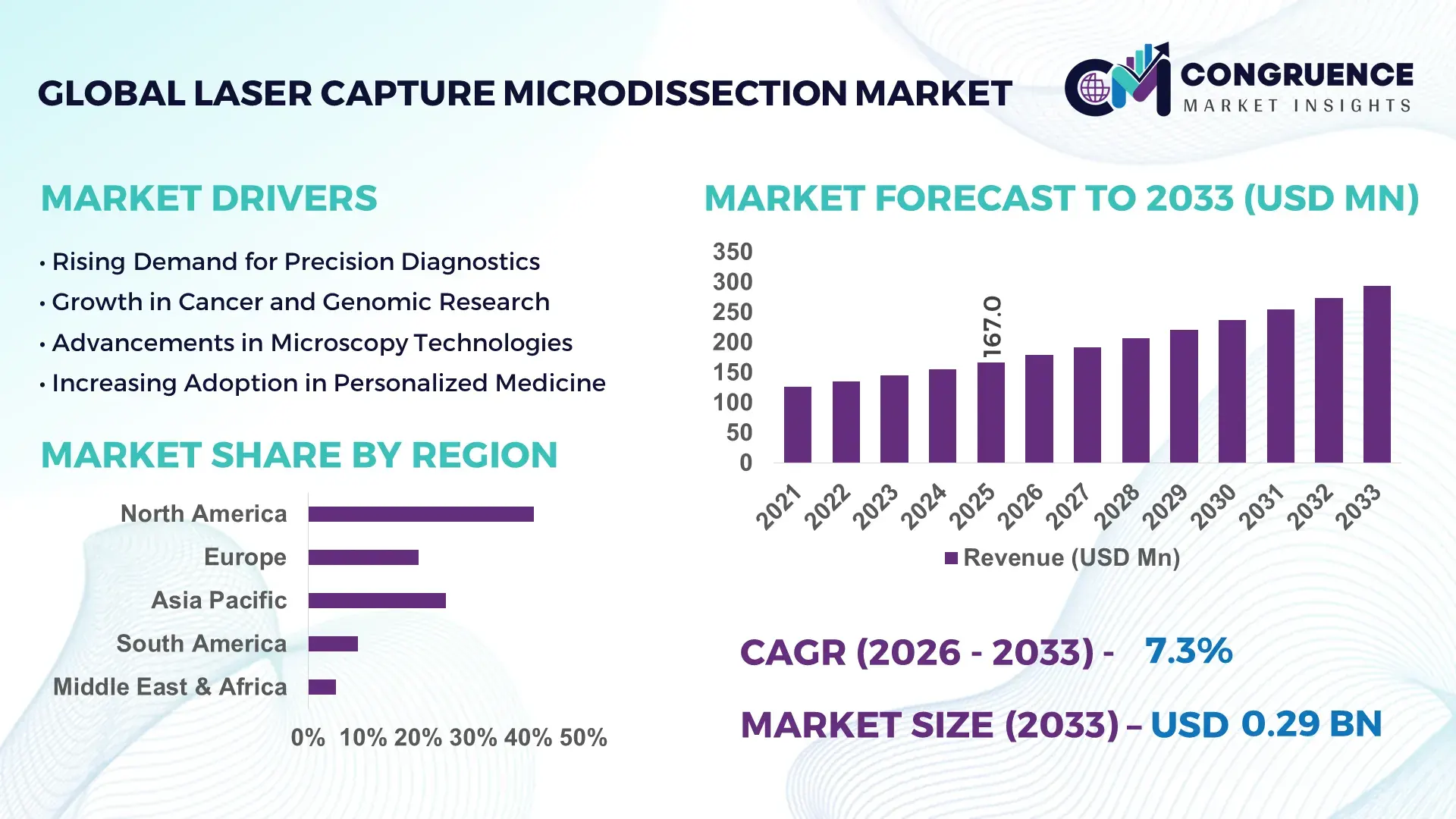

The Global Laser Capture Microdissection Market was valued at USD 167 Million in 2025 and is anticipated to reach a value of USD 293.43 Million by 2033 expanding at a CAGR of 7.3% between 2026 and 2033. The growth is driven by the increasing adoption of high-precision tissue analysis tools in advanced molecular diagnostics and translational research workflows.

The United States maintains a highly developed ecosystem for laser capture microdissection technologies, supported by extensive biomedical infrastructure and continuous innovation in life sciences instrumentation. More than 45% of pathology and genomics laboratories across the country utilize LCM systems for applications such as cancer tissue profiling and RNA/DNA extraction. Annual public and private investments in life sciences exceed USD 50 billion, significantly boosting advanced microscopy and microdissection adoption. Additionally, over 60% of clinical research programs in oncology incorporate LCM-based sample isolation for biomarker discovery and precision therapy development. The presence of more than 1,500 biotech companies and rapid advancements in AI-integrated imaging systems further enhance the technological landscape and application depth of LCM across research and clinical domains.

Market Size & Growth: Valued at USD 167 Million in 2025 and projected to reach USD 293.43 Million by 2033, growing at a CAGR of 7.3%, driven by rising precision medicine demand.

Top Growth Drivers: Precision oncology adoption increased by 38%, genomic research demand rose by 42%, and laboratory automation efficiency improved by 29%.

Short-Term Forecast: By 2028, sample processing efficiency is expected to increase by 35% along with a 22% reduction in operational costs.

Emerging Technologies: AI-powered image recognition, automated laser microdissection systems, and high-throughput digital pathology platforms.

Regional Leaders: North America projected to reach USD 120 Million by 2033 with strong clinical integration; Europe at USD 85 Million with robust research funding; Asia-Pacific at USD 70 Million driven by expanding biotech infrastructure.

Consumer/End-User Trends: High adoption among academic institutes, pharmaceutical companies, and diagnostic laboratories focusing on cell-specific molecular analysis.

Pilot or Case Example: In 2024, a clinical pilot project demonstrated a 40% improvement in biomarker detection accuracy using automated LCM systems.

Competitive Landscape: Leading player holds approximately 28% market share, followed by Leica Microsystems, Thermo Fisher Scientific, Zeiss, and Danaher Corporation.

Regulatory & ESG Impact: Increasing regulatory focus on precision diagnostics and favorable funding policies are accelerating technology adoption.

Investment & Funding Patterns: Over USD 600 Million invested globally in life science instrumentation with rising venture capital in automation technologies.

Innovation & Future Outlook: Growth driven by single-cell analysis integration, next-generation sequencing compatibility, and miniaturized LCM devices.

Laser capture microdissection technology continues to gain traction across key sectors including oncology, neuroscience, and infectious disease research, with oncology accounting for over 40% of application demand due to its critical role in tumor microenvironment analysis. Advanced systems incorporating UV and infrared laser technologies are enhancing precision and minimizing sample contamination. Regulatory support for personalized medicine and genomic diagnostics is further accelerating adoption in developed markets. Asia-Pacific is emerging as a high-growth region due to increased healthcare expenditure and expansion of biotechnology clusters, while Europe benefits from strong academic-industry collaborations. Emerging trends such as integration with multi-omics platforms, cloud-based data analytics, and automated sample processing are expected to reshape the competitive landscape and drive long-term market expansion.

The Laser Capture Microdissection Market holds strong strategic relevance in precision diagnostics, molecular pathology, and next-generation sequencing workflows, enabling highly accurate isolation of specific cell populations from complex tissue samples. This capability is increasingly critical in oncology, where targeted biomarker discovery and tumor heterogeneity analysis are driving demand for advanced microdissection systems. Automated laser capture microdissection platforms deliver up to 45% improvement in sample purity compared to manual microdissection techniques, significantly enhancing downstream genomic and proteomic analysis accuracy.

North America dominates in volume due to extensive laboratory infrastructure and research funding, while Asia-Pacific leads in adoption with over 35% of newly established biotechnology laboratories integrating LCM systems into their workflows. The strategic integration of artificial intelligence and digital pathology is transforming operational efficiency, with AI-assisted image recognition improving tissue selection accuracy by over 30%. By 2028, AI-integrated microdissection platforms are expected to reduce sample processing time by 25% while increasing throughput by more than 40%.

From a compliance and ESG perspective, firms are committing to laboratory sustainability improvements, including a 20% reduction in consumable waste and energy-efficient instrumentation by 2030. In 2024, a leading biotechnology firm in Germany achieved a 32% increase in workflow efficiency through automated LCM integration combined with digital imaging systems. As research and clinical diagnostics continue to evolve toward precision-based approaches, the Laser Capture Microdissection Market is emerging as a critical enabler of high-accuracy, compliant, and scalable laboratory operations, positioning it as a pillar of resilience, regulatory alignment, and sustainable growth.

The rising focus on precision oncology is a major driver of the Laser Capture Microdissection Market, as it enables accurate isolation of tumor cells for detailed molecular analysis. Over 60% of cancer research studies now require cell-specific sampling techniques to understand tumor heterogeneity and identify actionable biomarkers. Laser capture microdissection allows researchers to isolate pure populations of malignant cells, improving diagnostic accuracy by nearly 35% compared to bulk tissue analysis. Additionally, the increasing adoption of next-generation sequencing technologies has created a strong need for high-quality sample preparation, further boosting LCM utilization. Government initiatives supporting cancer research and the expansion of personalized medicine programs are also contributing to increased demand, with clinical laboratories increasingly integrating LCM systems into their diagnostic workflows.

High capital investment and operational complexity remain key restraints in the Laser Capture Microdissection Market, limiting widespread adoption, particularly in small and mid-sized laboratories. Advanced LCM systems require significant upfront investment, often exceeding standard laboratory equipment budgets, along with ongoing costs for maintenance and consumables. Additionally, the operation of these systems demands skilled personnel trained in microscopy, laser handling, and molecular biology techniques. Studies indicate that over 40% of smaller research facilities face challenges in adopting LCM due to technical expertise gaps and budget constraints. Furthermore, integration with existing laboratory information systems and workflows can be complex, requiring additional time and resources. These factors collectively slow down adoption rates, especially in developing regions with limited access to advanced laboratory infrastructure.

The rapid expansion of single-cell analysis presents significant growth opportunities for the Laser Capture Microdissection Market, as it requires highly precise and contamination-free cell isolation techniques. Single-cell genomics and transcriptomics are gaining traction, with research studies increasing by over 50% in the past five years. LCM technology enables the isolation of individual cells from heterogeneous tissue environments, making it a critical tool for advanced biological research. The integration of LCM with next-generation sequencing and spatial biology platforms is further enhancing its value proposition. Additionally, increasing investments in biotechnology startups and research institutions are creating new avenues for technology deployment. Emerging applications in immunology and regenerative medicine are also expected to drive demand, positioning LCM as a key enabler of future scientific breakthroughs.

Standardization and sample variability pose significant challenges to the Laser Capture Microdissection Market, impacting reproducibility and consistency in research outcomes. Variations in tissue preparation, staining techniques, and operator handling can lead to inconsistencies in sample quality, affecting downstream analysis. Studies show that up to 25% of LCM-based experiments face reproducibility issues due to differences in protocol execution. Additionally, the lack of universally accepted guidelines for LCM procedures creates difficulties in cross-laboratory comparisons and large-scale studies. This challenge is further compounded by the complexity of biological samples, which can vary significantly in composition and structure. Addressing these issues requires the development of standardized protocols, advanced automation, and improved training programs, which are essential for ensuring reliable and scalable use of LCM technologies across diverse applications.

Automation-Driven Workflow Efficiency Increasing by Over 40%: The integration of automated laser capture microdissection systems is significantly transforming laboratory workflows, with over 65% of advanced research labs adopting automation to reduce manual intervention. Automated systems have demonstrated up to 40% improvement in sample processing efficiency and nearly 30% reduction in human error. Laboratories using robotic-assisted microdissection platforms report a 25% increase in throughput, particularly in high-volume genomic studies, making automation a critical trend shaping operational scalability and precision.

AI-Integrated Imaging Enhancing Tissue Selection Accuracy by 30%: Artificial intelligence and machine learning algorithms are increasingly embedded in LCM platforms to enable real-time tissue recognition and selection. More than 50% of newly installed systems now include AI-powered imaging capabilities, improving tissue targeting accuracy by approximately 30% compared to conventional microscopy methods. These advancements are particularly impactful in oncology research, where precise tumor cell identification improves biomarker detection rates by over 35%, supporting the growing demand for precision diagnostics.

Expansion of Single-Cell Analysis Applications Growing by 50%: The adoption of LCM in single-cell genomics and spatial transcriptomics has increased by more than 50% over the past five years, driven by the need for high-resolution molecular data. Approximately 45% of life sciences research projects now incorporate single-cell analysis workflows, with LCM playing a vital role in isolating individual cells from heterogeneous tissues. This trend is accelerating innovation in personalized medicine and advanced therapeutic research, with laboratories reporting up to 28% improvement in experimental reproducibility.

Rising Adoption in Emerging Markets Increasing by 35%: Asia-Pacific and Latin America are witnessing rapid expansion in LCM adoption, with over 35% growth in installations across biotechnology and clinical laboratories. Government-backed healthcare initiatives and increasing investments in research infrastructure have contributed to a 30% rise in advanced laboratory setups in these regions. Additionally, local manufacturing and distribution networks have improved accessibility, reducing equipment acquisition time by nearly 20%, thereby accelerating market penetration and regional competitiveness.

The Laser Capture Microdissection Market is segmented based on type, application, and end-user, each contributing uniquely to overall industry expansion. By type, systems are broadly categorized into infrared (IR) and ultraviolet (UV) laser-based microdissection platforms, with UV systems gaining traction due to higher precision capabilities. In terms of application, molecular biology and oncology research dominate due to increasing demand for tumor-specific cell analysis and biomarker discovery, accounting for a significant portion of system utilization. End-user segmentation highlights academic and research institutions as primary contributors, followed by pharmaceutical and biotechnology companies that leverage LCM for drug discovery and genomic analysis. Diagnostic laboratories are also emerging as key adopters, supported by the growing demand for personalized medicine. The segmentation reflects a strong alignment between technological innovation and application-specific requirements, enabling targeted growth across multiple industry verticals.

Laser Capture Microdissection systems are primarily segmented into ultraviolet (UV) laser microdissection and infrared (IR) laser capture microdissection technologies. UV laser-based systems currently account for approximately 58% of total adoption due to their superior precision in isolating specific cell populations without contamination. These systems are widely preferred in advanced genomic and proteomic research, where high-resolution tissue dissection is critical. In contrast, IR-based systems hold around 32% share and are valued for their ability to gently capture cells using thermoplastic films, making them suitable for delicate tissue samples. However, adoption in hybrid laser systems combining both UV and IR technologies is rising rapidly, expected to grow at a CAGR of 8.1% due to their versatility and enhanced functionality. Other niche technologies, including laser pressure catapulting systems, collectively contribute nearly 10% of the market, serving specialized research applications.

The Laser Capture Microdissection Market is segmented into applications such as oncology research, neuroscience, molecular biology, and infectious disease studies. Oncology research dominates with approximately 44% share due to the critical need for precise tumor cell isolation and biomarker identification. Molecular biology applications account for nearly 28%, focusing on gene expression analysis and DNA sequencing. However, neuroscience applications are emerging as the fastest-growing segment, with an estimated CAGR of 8.5%, driven by increasing studies on neurodegenerative diseases and brain tissue analysis. Infectious disease research and immunology collectively contribute around 20% of total usage, supporting advancements in pathogen identification and immune response studies.

End-user segmentation in the Laser Capture Microdissection Market includes academic and research institutions, pharmaceutical and biotechnology companies, and diagnostic laboratories. Academic and research institutions lead with approximately 48% share, driven by extensive use in genomics, proteomics, and translational research. Pharmaceutical and biotechnology companies account for around 34%, leveraging LCM for drug discovery, biomarker validation, and precision medicine development. Diagnostic laboratories are the fastest-growing segment, with a projected CAGR of 7.9%, supported by the increasing integration of LCM in clinical diagnostics and personalized treatment planning. Other end-users, including contract research organizations and forensic laboratories, collectively contribute nearly 18% of the market, utilizing LCM for specialized analytical applications.

Region North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.6% between 2026 and 2033.

North America’s dominance is supported by over 65% penetration of advanced laboratory technologies and the presence of more than 1,200 active genomics research facilities. Europe follows with approximately 29% share, driven by strong academic collaborations and government-backed research funding programs exceeding USD 15 billion annually. Asia-Pacific holds around 22% share, with China, Japan, and India collectively contributing over 70% of regional demand due to expanding biotechnology infrastructure and increasing healthcare investments. South America accounts for nearly 5% of the global market, supported by growing clinical research activities, particularly in Brazil and Argentina. The Middle East & Africa region contributes approximately 3%, with increasing adoption of advanced diagnostic technologies and rising investments in healthcare modernization across the UAE and South Africa.

North America holds approximately 41% of the Laser Capture Microdissection Market share, supported by strong demand from oncology research, molecular diagnostics, and pharmaceutical R&D sectors. Over 70% of biotechnology firms in the region have integrated high-precision microdissection systems into their workflows. Government initiatives, including annual research funding exceeding USD 50 billion, continue to drive innovation and adoption. Regulatory frameworks promoting precision medicine and genomic diagnostics further support market expansion. Technological advancements such as AI-integrated imaging and automated microdissection platforms have improved laboratory efficiency by over 35%. A notable example includes Thermo Fisher Scientific expanding its advanced LCM product portfolio with enhanced imaging capabilities, improving sample accuracy across research facilities. Consumer behavior reflects high enterprise adoption, particularly in healthcare and life sciences, with over 60% of large-scale laboratories prioritizing automation and digital integration.

Europe accounts for approximately 29% of the Laser Capture Microdissection Market, with key markets including Germany, the UK, and France contributing over 65% of regional demand. Regulatory bodies focusing on clinical accuracy and data transparency have increased the adoption of advanced diagnostic tools. Sustainability initiatives targeting a 20% reduction in laboratory waste by 2030 are influencing procurement decisions. More than 55% of research institutions in Europe have adopted digital pathology and automated LCM systems to improve workflow efficiency. Technological advancements in UV laser systems and integration with sequencing platforms are gaining traction. A leading regional player, Leica Microsystems, continues to innovate with high-precision LCM solutions, enhancing adoption across academic and clinical laboratories. Consumer behavior in Europe reflects a strong preference for compliant, high-quality, and environmentally sustainable laboratory technologies.

Asia-Pacific ranks as the fastest-growing region in the Laser Capture Microdissection Market, contributing approximately 22% of global demand. China, Japan, and India collectively account for over 70% of regional consumption, driven by rapid expansion of biotechnology and pharmaceutical sectors. More than 40% of new laboratory setups in the region are equipped with advanced microdissection systems, reflecting increasing investment in research infrastructure. Governments are investing heavily in healthcare modernization, with China alone allocating over USD 10 billion annually toward biotechnology development. Technological trends include integration with AI-driven diagnostics and cloud-based data analysis platforms. A regional example includes Olympus Corporation advancing imaging-integrated LCM solutions, improving tissue analysis efficiency by over 30%. Consumer behavior is characterized by growing adoption among mid-sized laboratories and increasing demand for cost-effective yet high-performance systems.

South America accounts for approximately 5% of the Laser Capture Microdissection Market, with Brazil and Argentina contributing over 65% of regional demand. The region is witnessing gradual improvements in research infrastructure, particularly in clinical diagnostics and academic research institutions. Government incentives aimed at strengthening healthcare systems and increasing research output are supporting adoption of advanced laboratory technologies. More than 35% of research laboratories in Brazil have upgraded to digital and automated systems, including LCM platforms. Trade policies promoting import of advanced scientific equipment are further enhancing market accessibility. A regional example includes increased adoption of precision diagnostic tools in Brazilian oncology centers, improving diagnostic accuracy by nearly 25%. Consumer behavior reflects growing interest in cost-efficient solutions and gradual transition toward automation in laboratory processes.

The Middle East & Africa region contributes approximately 3% to the Laser Capture Microdissection Market, with key growth countries including the UAE and South Africa. Demand is primarily driven by healthcare modernization initiatives and increasing investments in clinical research infrastructure. Over 30% of newly established laboratories in the UAE are equipped with advanced diagnostic technologies, including LCM systems. Government partnerships and international collaborations are supporting technology transfer and adoption. Technological modernization includes integration of digital pathology and AI-assisted diagnostics, improving laboratory efficiency by nearly 20%. A regional example includes healthcare institutions in the UAE adopting advanced imaging-integrated LCM systems to enhance cancer diagnostics. Consumer behavior shows increasing demand for high-quality diagnostic solutions, particularly in urban healthcare centers, with gradual expansion into research institutions.

United States – 38% share: Laser Capture Microdissection Market growth driven by strong biotechnology infrastructure and high adoption in precision oncology research.

Germany – 16% share: Laser Capture Microdissection Market supported by advanced research facilities and strong regulatory focus on high-precision diagnostics.

The Laser Capture Microdissection Market is characterized by a moderately consolidated competitive landscape, with the top five companies accounting for approximately 62% of the total market share. Over 25 active global and regional players compete across product innovation, technological integration, and strategic partnerships. Leading companies are focusing on developing automated and AI-integrated LCM systems, which have demonstrated up to 35% improvement in operational efficiency and accuracy. Strategic initiatives such as mergers, acquisitions, and collaborations with research institutions are increasing, with over 15 notable partnerships recorded in the past three years. Product innovation remains a key competitive factor, with more than 40% of companies investing in next-generation imaging and microdissection technologies. Additionally, companies are expanding their global footprint through distribution agreements and localized manufacturing to improve accessibility. The market also shows increasing competition from emerging players offering cost-effective solutions, particularly in Asia-Pacific. Continuous advancements in single-cell analysis and integration with genomic technologies are further intensifying competition, making innovation and strategic positioning critical for long-term success.

Thermo Fisher Scientific

Leica Microsystems

Carl Zeiss AG

Danaher Corporation

Olympus Corporation

Arcturus Bioscience

MMI CellCut

Molecular Machines & Industries

Fluidigm Corporation

Eppendorf AG

Technological advancements in the Laser Capture Microdissection Market are centered on improving precision, automation, and integration with advanced molecular analysis platforms. Modern LCM systems increasingly incorporate ultraviolet (UV) and infrared (IR) laser technologies, enabling cell isolation accuracy levels exceeding 95% while minimizing contamination risks. UV laser systems are widely used for high-resolution tissue cutting, while IR-based systems provide gentle capture mechanisms suitable for fragile samples, with over 60% of laboratories utilizing hybrid systems to balance precision and sample integrity.

Automation is a key technological driver, with more than 65% of newly installed LCM systems featuring automated stage control, image recognition, and laser targeting capabilities. These systems reduce manual intervention by nearly 30% and improve reproducibility across experiments. Integration with digital pathology platforms has enabled high-throughput workflows, allowing laboratories to process up to 40% more samples daily compared to conventional methods. AI-powered imaging algorithms are further enhancing tissue identification, improving selection accuracy by over 30% in complex biological samples.

Another major innovation is the integration of LCM with next-generation sequencing (NGS) and single-cell analysis platforms. Approximately 50% of genomic research laboratories now use LCM in conjunction with NGS to enable precise extraction of DNA and RNA from targeted cells. Additionally, advancements in spatial transcriptomics and proteomics are expanding LCM applications, with over 35% of research projects incorporating multi-omics approaches. Miniaturization and portability of LCM systems are also emerging trends, with compact devices reducing laboratory space requirements by nearly 20%. Cloud-based data management and real-time analytics integration are improving data accessibility and collaboration across research teams. These technological developments are collectively transforming LCM into a highly efficient, scalable, and indispensable tool for precision medicine, advanced diagnostics, and cutting-edge life sciences research.

• In January 2025, Carl Zeiss AG expanded its microscopy portfolio with enhanced laser microdissection capabilities integrated into its Axio Observer platform, improving tissue isolation precision and workflow efficiency for advanced pathology applications. Source: www.zeiss.com

• In September 2024, Leica Microsystems introduced an upgraded version of its LMD7 laser microdissection system, featuring improved UV laser control and automated sample collection, enabling up to 25% higher throughput in molecular research laboratories. Source: www.leica-microsystems.com

• In March 2025, Thermo Fisher Scientific strengthened its precision medicine portfolio by integrating advanced imaging software with microdissection workflows, enhancing biomarker discovery accuracy by over 30% in oncology research applications. Source: www.thermofisher.com

• In June 2024, Olympus Corporation advanced its microscopy solutions by enhancing imaging-guided microdissection compatibility, enabling improved cellular visualization and increasing sample targeting efficiency by approximately 20% in life sciences laboratories. Source: www.olympus-global.com

The Laser Capture Microdissection Market Report provides a comprehensive analysis of the global industry, covering a wide range of segments, technologies, applications, and regional dynamics. The report evaluates key product types, including ultraviolet (UV) laser systems, infrared (IR) capture systems, and hybrid technologies, which collectively account for over 90% of market utilization across research and clinical laboratories. It also examines emerging innovations such as AI-integrated imaging systems, automated microdissection platforms, and multi-omics integration tools that are increasingly shaping the competitive landscape.

From an application perspective, the report covers critical areas such as oncology, molecular biology, neuroscience, and infectious disease research, with oncology representing more than 40% of total demand due to its reliance on precise cell isolation for tumor analysis. The scope further includes detailed insights into end-user segments, including academic and research institutions, pharmaceutical and biotechnology companies, and diagnostic laboratories, which together contribute over 80% of total system adoption globally.

Geographically, the report analyzes key regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with regional contributions ranging from approximately 3% to over 40% depending on infrastructure and research intensity. The study also highlights niche and emerging segments such as single-cell genomics and spatial transcriptomics, which are experiencing adoption increases of over 35% in advanced research settings. Additionally, the report outlines regulatory frameworks, technological advancements, and evolving industry standards influencing market development. This structured analysis enables stakeholders to identify growth opportunities, assess competitive positioning, and make informed strategic decisions across the Laser Capture Microdissection Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

7.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Thermo Fisher Scientific, Leica Microsystems, Carl Zeiss AG, Danaher Corporation, Olympus Corporation, Arcturus Bioscience, MMI CellCut, Molecular Machines & Industries, Fluidigm Corporation, Eppendorf AG |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |