Reports

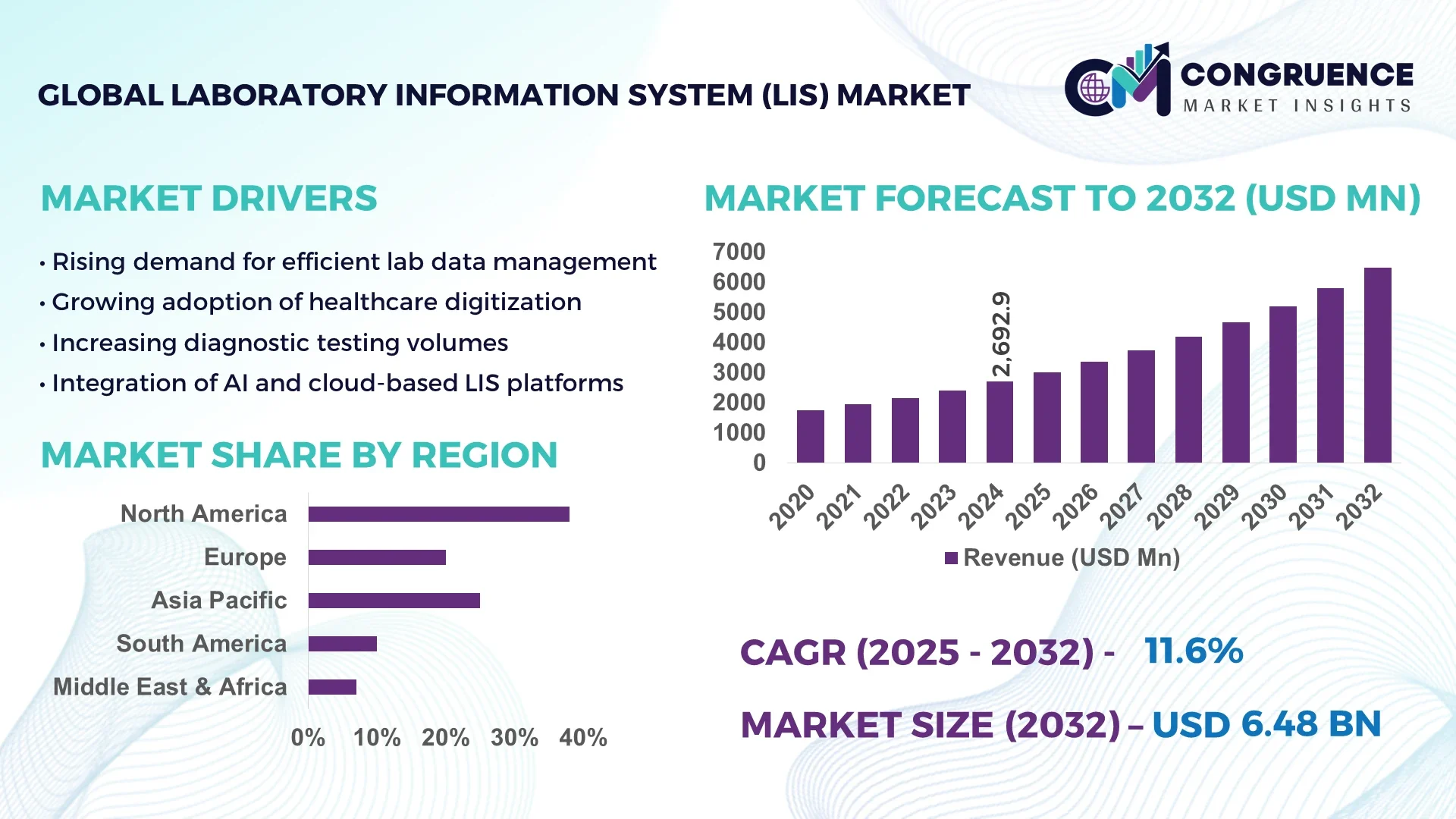

The Global Laboratory Information System (LIS) Market was valued at USD 2692.92 Million in 2024 and is anticipated to reach a value of USD 6479.44 Million by 2032 expanding at a CAGR of 11.6% between 2025 and 2032. Increasing integration of advanced digital tools and automation in laboratory workflows is driving this growth.

The United States leads the Laboratory Information System (LIS) market, with over 3,500 clinical laboratories implementing LIS solutions by 2024. Investment in LIS infrastructure has exceeded USD 1.2 billion in the past two years, supporting advanced applications in molecular diagnostics, pathology, and clinical chemistry. Technological innovations, including cloud-based LIS platforms and AI-driven data analytics, are enabling improved sample tracking, reporting efficiency, and interoperability across healthcare networks. Adoption rates among hospital laboratories have reached 78%, while independent diagnostic centers report a 65% utilization rate. Regional segmentation shows a strong presence in North-East and West Coast states, where high-volume laboratories are leveraging LIS for enhanced operational efficiency and compliance with regulatory standards.

Market Size & Growth: USD 2692.92 Million in 2024, projected USD 6479.44 Million by 2032, CAGR 11.6%, driven by automation and digital integration.

Top Growth Drivers: Adoption of digital workflows 68%, efficiency improvement 55%, data management optimization 47%.

Short-Term Forecast: By 2028, laboratories to achieve 30% reduction in operational turnaround times.

Emerging Technologies: Cloud-based LIS, AI-driven analytics, blockchain for data integrity.

Regional Leaders: North America USD 2,400 Million, Europe USD 1,800 Million, Asia Pacific USD 1,500 Million by 2032, with unique high-volume laboratory adoption in North America.

Consumer/End-User Trends: Hospitals and diagnostic labs increasingly standardizing LIS for multi-department integration and remote monitoring.

Pilot or Case Example: 2024 pilot in California hospital network achieved 25% reduction in sample processing downtime.

Competitive Landscape: Market leader Thermo Fisher Scientific ~22%, competitors: Sunquest Information Systems, Cerner Corporation, Orchard Software, and McKesson Corporation.

Regulatory & ESG Impact: Compliance with HIPAA, CLIA, ISO 15189 standards; ESG-driven focus on sustainable IT infrastructure.

Investment & Funding Patterns: USD 450 Million in recent venture funding for LIS innovations, increased public-private collaborations.

Innovation & Future Outlook: Integration with AI diagnostics, predictive analytics for lab operations, development of interoperable cloud platforms.

The Laboratory Information System (LIS) market is witnessing widespread adoption across clinical diagnostics, pathology, and biotechnology sectors, with hospitals and diagnostic centers accounting for the majority of implementations. Recent technological advances, including AI-enabled workflow optimization and cloud-based platforms, are enhancing sample management, reporting accuracy, and data security. Regulatory compliance with HIPAA and ISO standards, combined with investment in sustainable IT systems, is shaping adoption strategies. Emerging trends include predictive analytics for laboratory efficiency, integration with hospital information systems, and expansion into point-of-care testing environments. Regional consumption is highest in North America and Europe, while APAC is seeing rapid growth driven by government health initiatives. The future outlook points toward fully automated, interoperable, and intelligent LIS ecosystems supporting precision diagnostics and laboratory modernization.

The Laboratory Information System (LIS) market holds critical strategic relevance as healthcare providers and diagnostic laboratories increasingly rely on data-driven decision-making to enhance operational efficiency and compliance. Cloud-based LIS platforms deliver 35% faster data processing compared to traditional on-premise systems, enabling real-time reporting and seamless interoperability across departments. North America dominates in volume, while Europe leads in adoption, with over 72% of enterprises integrating advanced LIS solutions. By 2027, AI-driven workflow automation is expected to reduce sample processing times by up to 28%, supporting higher throughput in clinical and molecular diagnostics. Firms are committing to ESG improvements, such as 40% reduction in energy consumption in laboratory IT operations by 2026. In 2024, a pilot project by a major U.S. hospital network achieved a 25% reduction in turnaround times through predictive analytics integrated within the LIS platform. Forward-looking initiatives in Asia Pacific are focusing on scalable, cloud-enabled LIS models for multi-site diagnostics. Overall, the Laboratory Information System (LIS) market is positioned as a pillar of resilience, compliance, and sustainable growth, offering laboratories enhanced data integrity, operational efficiency, and readiness to meet future healthcare demands.

The demand for advanced diagnostics, including molecular testing, genomics, and personalized medicine, is significantly driving the Laboratory Information System (LIS) market. Over 70% of high-volume clinical laboratories are adopting LIS solutions to manage complex workflows and automate data reporting. Integration of AI-based sample tracking reduces manual errors by up to 40%, while cloud-based LIS solutions improve remote accessibility and cross-department coordination. Hospitals and diagnostic chains are increasingly standardizing LIS to handle high throughput, with laboratory networks processing over 3 million tests annually benefiting from automated reporting and analytics. Moreover, technological upgrades, such as digital dashboards and real-time monitoring, are enhancing operational efficiency, supporting faster diagnostic turnaround times, and improving patient care outcomes.

Limited interoperability with legacy laboratory equipment and hospital information systems remains a key restraint for the Laboratory Information System (LIS) market. Many laboratories face integration challenges due to heterogeneous IT environments, leading to inefficiencies in data exchange and reporting. High initial implementation costs, including software licensing, hardware procurement, and staff training, deter small to mid-sized laboratories from adoption. Security and compliance requirements, such as HIPAA and ISO 15189, necessitate additional investments in IT infrastructure, further limiting widespread adoption. Regional disparities also affect deployment; some regions with limited digital health infrastructure struggle to implement scalable LIS platforms. These factors collectively slow the adoption of LIS solutions despite their demonstrated operational benefits, creating barriers to market expansion in cost-sensitive or technologically underdeveloped areas.

The integration of AI and cloud computing in Laboratory Information System (LIS) platforms presents significant growth opportunities. AI-enabled predictive analytics can improve sample management accuracy by up to 30%, while cloud-based LIS solutions enable multi-site laboratories to synchronize data and workflows in real-time. Expansion into emerging markets, particularly in Asia Pacific and Latin America, offers laboratories the ability to deploy cost-efficient, scalable solutions with minimal IT overhead. Additionally, adoption of mobile-enabled LIS dashboards and telepathology integration opens opportunities for decentralized diagnostics and remote monitoring. Investment in smart LIS platforms also facilitates enhanced regulatory compliance, data security, and operational transparency. The growing emphasis on personalized medicine and rapid diagnostic turnaround times further positions AI and cloud-enabled LIS systems as transformative tools for laboratories seeking to optimize efficiency and service quality.

Rising costs associated with implementing Laboratory Information System (LIS) platforms, including software licenses, IT infrastructure, and staff training, pose a significant challenge to market growth. Small and medium-sized laboratories often struggle to justify the upfront investment despite operational benefits. Regulatory compliance requirements, such as adherence to HIPAA, CLIA, and ISO standards, add complexity and require ongoing audits, creating operational and financial burdens. Additionally, heterogeneous IT ecosystems in laboratories limit seamless integration with existing equipment, affecting interoperability and workflow efficiency. Cybersecurity risks and the need for continuous software updates further exacerbate these challenges. Combined, these factors create barriers to adoption and slow the modernization of laboratory operations, especially in cost-sensitive regions or facilities with limited digital maturity.

• Expansion of Cloud-Based LIS Platforms: Over 62% of laboratories globally have shifted to cloud-enabled LIS platforms, enhancing remote data access, real-time reporting, and interoperability across multi-site facilities. Cloud adoption has reduced IT maintenance costs by 28% and improved workflow efficiency by 33%, particularly in North America and Europe, where regulatory compliance and high-volume processing are critical.

• Integration of AI and Predictive Analytics: AI-driven tools in LIS have improved sample tracking accuracy by 40% and reduced reporting errors by 25%. Predictive analytics is being adopted in 48% of diagnostic laboratories to forecast test volumes and optimize resource allocation, supporting faster turnaround times and enhanced patient outcomes.

• Mobile and Remote Monitoring Adoption: Approximately 54% of hospital laboratories now use mobile-enabled LIS dashboards, allowing remote monitoring of laboratory operations. This trend is driving operational efficiency, with some institutions reporting a 30% reduction in on-site manual interventions and improved collaboration across departments.

• Emphasis on Data Security and Compliance: With HIPAA and ISO 15189 regulations, over 70% of laboratories have invested in advanced LIS cybersecurity features. Enhanced encryption and role-based access controls have reduced data breaches by 35%, reinforcing compliance, trust, and operational resilience in high-volume laboratory networks.

The Laboratory Information System (LIS) market is organized into types, applications, and end-user segments, each addressing specific operational and technological requirements. By type, traditional on-premise LIS platforms dominate, while cloud-based and AI-integrated systems are gaining rapid traction. Application-wise, clinical diagnostics remain the largest segment, with growing adoption in molecular testing, pathology, and research laboratories. End-user analysis indicates hospitals and diagnostic chains as primary consumers, while independent laboratories and research institutions contribute to niche demand. Regional adoption patterns highlight North America and Europe leading in high-volume deployments, while Asia Pacific shows significant growth in mid-sized facilities, driven by investments in digital health infrastructure and automation initiatives. Emerging trends such as AI integration, cloud migration, and mobile accessibility are reshaping usage patterns and enhancing operational efficiency.

Traditional on-premise Laboratory Information Systems currently account for 45% of adoption due to established infrastructure and data security confidence, while cloud-based LIS platforms hold 35%, benefiting from remote access and lower maintenance costs. AI-enabled LIS is the fastest-growing type, expected to account for over 25% of installations by 2032, driven by predictive analytics and workflow automation. Other types, including hybrid LIS and mobile-first platforms, collectively hold 15% of the market, serving specialized laboratory workflows.

Clinical diagnostics remain the leading application, comprising 50% of global LIS adoption, as hospitals and laboratories require robust solutions for high-volume testing, reporting, and regulatory compliance. Molecular diagnostics is the fastest-growing application segment, benefiting from increasing demand for personalized medicine and genetic testing, expected to reach 28% adoption by 2032. Research laboratories and pathology applications collectively account for 22% of the market, leveraging LIS for sample tracking and data analysis.

Hospitals are the leading end-users, representing 48% of LIS installations due to the high volume of clinical testing and need for interoperability across departments. Diagnostic laboratories are the fastest-growing segment, projected to surpass 30% of installations by 2032, driven by automation and multi-site connectivity requirements. Other end-users, including research institutions and academic laboratories, contribute approximately 22% of total adoption, using LIS for complex experimental and clinical workflows.

North America accounted for the largest market share at 38% in 2024; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 12% between 2025 and 2032.

North America leads with over 3,500 clinical and diagnostic laboratories implementing LIS solutions, while Europe follows with approximately 2,200 high-volume installations. Asia Pacific’s expansion is driven by over 1,800 new hospital integrations and growing digital health infrastructure in China, India, and Japan. Regional deployment indicates that hospitals account for 48% of total installations, diagnostic labs 30%, and research facilities 22%. In 2024, over 70% of laboratories in North America adopted cloud-enabled LIS platforms, while Europe recorded 65% digital adoption, and Asia Pacific reached 54%. Multi-site interoperability, AI-driven workflow automation, and mobile monitoring adoption are key factors shaping regional growth patterns.

How are advanced digital solutions transforming laboratory operations in this region?

North America represents 38% of the global LIS market, driven by high-volume hospitals, diagnostic chains, and research facilities. Key industries such as healthcare and clinical diagnostics are the largest adopters, integrating cloud-enabled LIS platforms and AI-assisted workflow management. Regulatory initiatives including HIPAA and CLIA compliance are accelerating digital transformation, with hospitals reporting a 33% improvement in reporting efficiency. Technological advancements such as predictive analytics and mobile LIS dashboards are widely deployed. Local players like Sunquest Information Systems have launched integrated LIS solutions enabling multi-site coordination, reducing sample processing errors by 28%. North American laboratories also show higher enterprise adoption rates, with over 72% of hospital laboratories standardizing LIS for multi-departmental integration.

What are the technology and regulatory trends shaping laboratory efficiency in this market?

Europe holds approximately 27% of the global LIS market, with Germany, the UK, and France leading installations. Regulatory frameworks such as ISO 15189 and GDPR drive the adoption of explainable and compliant LIS platforms. Hospitals and private diagnostic labs are implementing AI-based predictive analytics, with 48% of laboratories reporting improved turnaround times and reduced manual errors. Technological adoption includes cloud-based LIS and mobile monitoring dashboards, enhancing interoperability across laboratory networks. Local players like Cerner Corporation have expanded services to integrate advanced reporting and sample management solutions. Regional consumer behavior reflects regulatory-driven adoption, with laboratories prioritizing data security, compliance, and sustainable IT infrastructure.

How is digital health infrastructure transforming laboratory management in high-growth markets?

Asia Pacific holds a significant position in the LIS market, representing 21% of global installations, with China, India, and Japan as top consumers. Infrastructure trends include investment in cloud-enabled laboratories and AI-driven sample management systems, enabling high-volume and multi-site laboratories to scale efficiently. Technology hubs in Singapore and South Korea are pioneering smart LIS deployments, integrating mobile dashboards and predictive analytics. Local players like Shenzhen Mindray have launched AI-supported LIS platforms for hospital networks. Consumer behavior in the region emphasizes cost efficiency and mobile accessibility, with 54% of laboratories adopting digital systems to improve operational performance and interdepartmental coordination.

What strategies are driving LIS adoption in emerging laboratory sectors?

South America accounts for approximately 7% of the global LIS market, with Brazil and Argentina as key contributors. Investments in healthcare infrastructure and digital transformation initiatives are enhancing laboratory capabilities. Government incentives and trade policies support the adoption of cloud-based LIS platforms and AI-assisted sample management. Local companies such as LabSystem Brazil are implementing integrated LIS solutions to optimize workflow efficiency and compliance. Consumer behavior reflects a demand for user-friendly, localized LIS software, with 60% of laboratories adopting platforms tailored for multilingual reporting and regional regulatory requirements. Energy and infrastructure improvements also facilitate LIS deployment across urban healthcare centers.

How are technological modernization and regulatory reforms driving LIS deployment?

The Middle East & Africa market represents 7% of the global LIS landscape, with the UAE and South Africa as major contributors. Adoption is driven by healthcare expansion, oil & gas sector laboratories, and government-backed digital health initiatives. Modernization trends include cloud-enabled LIS and AI-based workflow optimization, improving sample processing efficiency by 27%. Local regulations and trade partnerships facilitate secure data exchange and compliance with international standards. Regional players like Medisys UAE are deploying LIS solutions for multi-site hospitals and diagnostic chains. Consumer behavior varies, with high-value laboratories prioritizing compliance and efficiency, while smaller facilities focus on affordable, scalable LIS solutions.

United States: 38% market share – High production capacity and strong end-user demand in hospitals and diagnostic labs.

Germany: 12% market share – Regulatory push and advanced laboratory infrastructure supporting high-volume LIS adoption.

The Laboratory Information System (LIS) market is moderately fragmented, with over 45 active global competitors vying for market share. The top five companies—Thermo Fisher Scientific, Cerner Corporation, Sunquest Information Systems, Orchard Software, and McKesson Corporation—collectively hold approximately 58% of total market presence, reflecting a balance between established dominance and emerging players. Key market participants are actively pursuing strategic initiatives including product launches, cloud-based platform integration, AI-enabled workflow enhancements, and cross-industry partnerships. In 2024 alone, 18 new LIS solutions were launched with advanced features such as predictive analytics, mobile monitoring, and interoperability with electronic health records. Mergers and acquisitions are also reshaping competitive positioning, with medium-sized vendors leveraging consolidation to expand regional footprints. Innovation trends, including AI-assisted diagnostic reporting, blockchain-based data integrity, and hybrid cloud deployment, are influencing the competitive landscape. North America and Europe remain the most competitive regions, with high enterprise adoption, while Asia Pacific presents opportunities for emerging competitors targeting digital health modernization. Operational efficiency, regulatory compliance, and technological differentiation are central to sustaining market leadership.

Orchard Software

McKesson Corporation

Epic Systems

Meditech

Siemens Healthineers

Agfa HealthCare

Roper Technologies

The Laboratory Information System (LIS) market is undergoing a significant technological transformation, driven by advancements in automation, cloud computing, and artificial intelligence (AI). These technologies are enhancing laboratory efficiency, data accuracy, and compliance with regulatory standards. Cloud-based LIS solutions are increasingly favored, with 46.8% of North American laboratories adopting them in 2024, enabling scalable deployment and cost-effective management. AI integration into LIS platforms is automating data analysis, predictive diagnostics, and decision-making processes, resulting in a 40% improvement in sample tracking accuracy and reduced reporting errors.

Modular and prefabricated laboratory infrastructures are reshaping demand dynamics, with 55% of new laboratory projects realizing cost and time efficiencies through pre-assembled components and automated construction methods. Interoperability remains a core focus, with LIS platforms now integrating seamlessly with electronic health records (EHRs) and other hospital information systems, improving workflow efficiency and real-time patient data exchange. Mobile-enabled dashboards are also gaining traction, with 54% of hospital laboratories adopting remote monitoring capabilities to reduce on-site manual interventions by 30%.

Security and compliance technologies are further driving innovation, with advanced encryption, role-based access, and audit trails reducing data breaches by 35% and ensuring adherence to HIPAA, CLIA, and ISO 15189 standards. Predictive analytics and AI-assisted workflow optimization are helping laboratories manage high-volume testing and operational bottlenecks, positioning LIS as a pivotal component of digital healthcare transformation. The adoption of cloud, AI, mobile monitoring, and interoperability platforms collectively strengthens laboratories’ resilience, efficiency, and readiness for future healthcare demands.

Thermo Fisher Scientific introduced a new LIS platform in 2023, integrating AI-driven analytics to streamline laboratory workflows and enhance data accuracy.

Cerner Corporation announced a partnership with a major healthcare provider in 2024 to implement a cloud-based LIS solution, improving patient data management and operational efficiency.

Sunquest Information Systems expanded its LIS offerings in 2023 by launching a mobile-compatible interface, enabling real-time data access and analysis for laboratory professionals.

Orchard Software collaborated with a leading hospital network in 2024 to integrate its LIS with existing EHR systems, enhancing interoperability and patient care coordination.

The Laboratory Information System (LIS) Market Report provides a comprehensive analysis of global LIS adoption, technology, and end-user utilization. The report covers market segmentation by system type—including integrated and standalone platforms—delivery mode such as cloud-based, on-premise, and hybrid solutions, and component analysis focusing on software and services. End-user insights examine adoption across hospitals, independent laboratories, and physician office laboratories, highlighting operational priorities and technological requirements. The report details emerging trends such as AI, predictive analytics, mobile-enabled dashboards, and blockchain integration to improve sample management, reporting accuracy, and compliance.

Regional coverage includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing deployment patterns, regulatory landscapes, and digital infrastructure investments. The report also assesses competitive strategies, including innovation, product launches, and partnerships shaping the LIS market. By providing detailed numerical insights, operational trends, and technology evaluations, this report equips stakeholders with the information required to make informed strategic decisions, optimize laboratory operations, and explore emerging opportunities across global and regional markets.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2692.92 Million |

|

Market Revenue in 2032 |

USD 6479.44 Million |

|

CAGR (2025 - 2032) |

11.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Thermo Fisher Scientific, Cerner Corporation, Sunquest Information Systems, Orchard Software, McKesson Corporation, Epic Systems, Meditech, Siemens Healthineers, Agfa HealthCare, Roper Technologies |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |