Reports

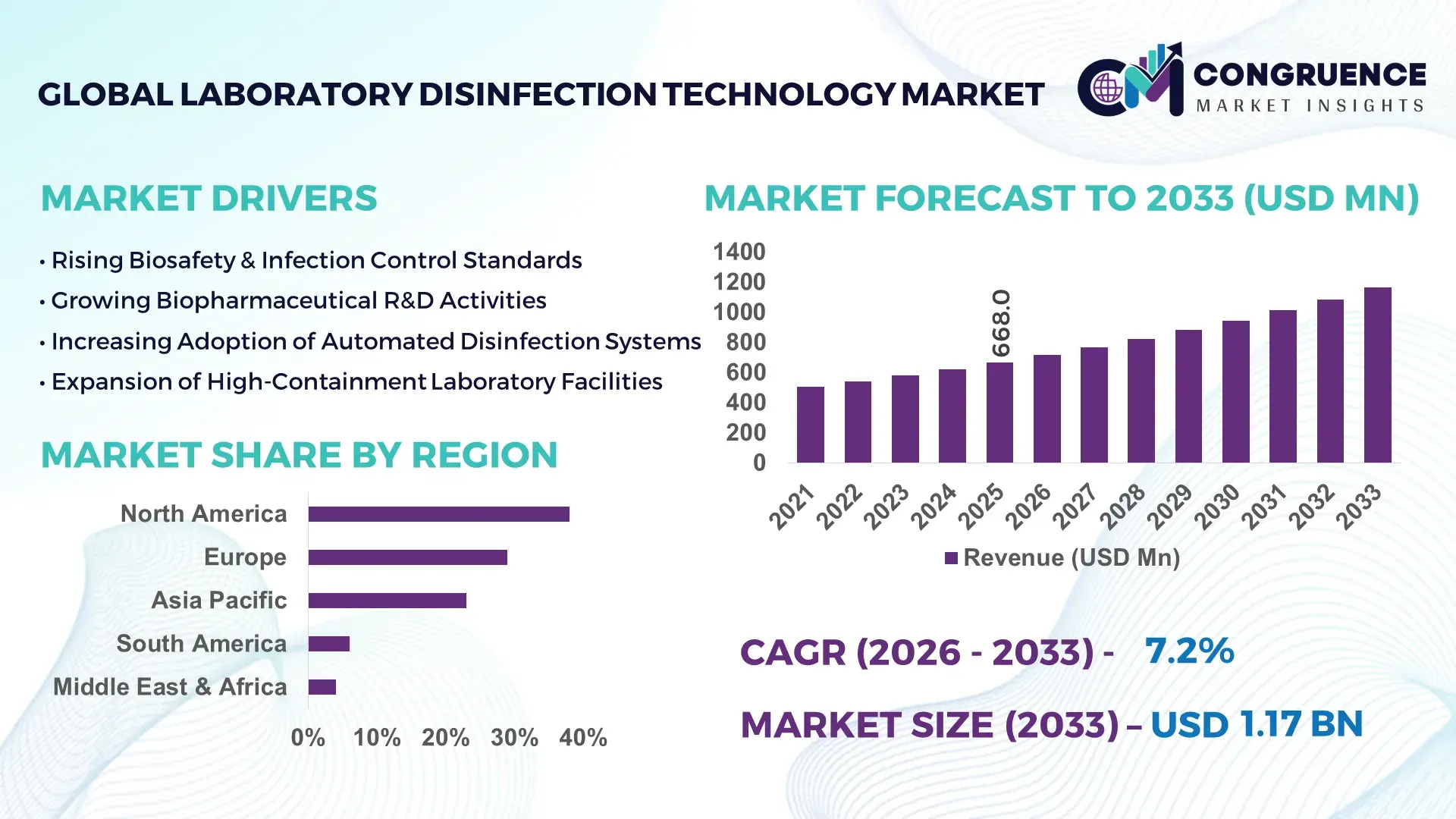

The Global Laboratory Disinfection Technology Market was valued at USD 668.0 Million in 2025 and is anticipated to reach a value of USD 1,165.0 Million by 2033 expanding at a CAGR of 7.2% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market is expanding steadily due to rising biosafety standards, increasing laboratory automation, and stricter contamination control protocols across pharmaceutical, clinical diagnostics, and research laboratories.

The United States represents the most advanced national ecosystem within the Laboratory Disinfection Technology Market, supported by over 12,000 clinical laboratories and more than 1,500 biopharmaceutical manufacturing facilities operating under stringent biosafety frameworks. The country invests over USD 50 billion annually in biomedical research, with more than 70% of large research laboratories adopting automated UV-C and hydrogen peroxide vapor (HPV) disinfection systems. Approximately 65% of high-containment BSL-3 laboratories in the U.S. have integrated IoT-enabled environmental monitoring and disinfection validation systems, while pharmaceutical cleanroom facilities report over 40% deployment of robotic or touchless surface disinfection technologies.

Market Size & Growth: USD 668.0 Million (2025) projected to reach USD 1,165.0 Million (2033) at 7.2% CAGR, driven by increasing biosafety compliance requirements and automation in laboratory infrastructure.

Top Growth Drivers: 72% adoption of automated disinfection protocols in pharma labs; 48% efficiency improvement via UV-C systems; 35% reduction in contamination incidents using HPV technologies.

Short-Term Forecast: By 2028, automated laboratory disinfection systems are expected to reduce manual sanitation costs by 28% and improve operational uptime by 22%.

Emerging Technologies: AI-enabled contamination detection, autonomous UV-C robots, and IoT-based disinfection cycle validation platforms are reshaping laboratory hygiene standards.

Regional Leaders: North America projected at USD 410 Million by 2033 with strong regulatory adoption; Europe at USD 325 Million driven by GMP upgrades; Asia-Pacific at USD 295 Million supported by biotech expansion.

Consumer/End-User Trends: Pharmaceutical manufacturers account for nearly 46% usage, followed by clinical diagnostics labs at 32% and academic research institutions at 18%, with rising automation preference.

Pilot or Case Example: In 2024, a U.S. biopharma facility implemented autonomous UV-C systems achieving 38% contamination reduction and 30% faster room turnover.

Competitive Landscape: Market leader Ecolab holds approximately 18% share, followed by STERIS, Getinge, 3M, and Advanced Sterilization Products.

Regulatory & ESG Impact: Enhanced GMP revisions and biosafety standards mandate 99.9% microbial reduction benchmarks; 42% of labs are adopting low-chemical disinfection to meet ESG targets.

Investment & Funding Patterns: Over USD 850 Million invested globally in laboratory automation and sterilization infrastructure upgrades between 2023–2025, with increased venture activity in robotics-based systems.

Innovation & Future Outlook: Integration of AI analytics with real-time pathogen detection and automated validation reporting is expected to redefine contamination control standards globally.

Pharmaceutical manufacturing contributes approximately 46% of total demand, followed by diagnostics at 32% and academic research at 18%. Innovations such as AI-driven UV validation systems and eco-friendly hydrogen peroxide formulations are reshaping product development. Regulatory tightening in North America and Europe accelerates technology upgrades, while Asia-Pacific laboratories show 40% higher equipment procurement growth. Sustainable disinfection and robotics integration remain central to long-term strategic expansion.

The Laboratory Disinfection Technology Market holds strategic importance within global pharmaceutical manufacturing, clinical diagnostics, biotechnology research, and public health infrastructure. As laboratory automation expands and biosafety levels intensify, contamination control has transitioned from a procedural requirement to a core operational KPI. AI-enabled UV-C disinfection systems deliver 35% faster sterilization cycles compared to traditional manual chemical wipe-down standards, while hydrogen peroxide vapor systems demonstrate 30% higher microbial eradication efficiency than conventional liquid disinfectants.

North America dominates in volume due to its dense network of research laboratories and biopharmaceutical facilities, while Europe leads in advanced adoption, with nearly 68% of regulated laboratories integrating automated validation and digital compliance documentation platforms. By 2028, AI-driven environmental monitoring integrated with robotic disinfection is expected to improve contamination detection accuracy by 40% and reduce manual audit preparation time by 25%.

From a compliance and ESG perspective, firms are committing to 50% reductions in hazardous chemical disinfectant usage by 2030, replacing them with low-residue UV and vapor-based systems. In 2024, a leading U.S.-based pharmaceutical manufacturer achieved a 33% reduction in cleanroom downtime through autonomous disinfection scheduling and IoT-based microbial load monitoring.

Looking ahead, the Laboratory Disinfection Technology Market will serve as a foundational pillar of resilience, regulatory alignment, and sustainable laboratory operations, ensuring operational continuity, audit readiness, and advanced biosafety performance across critical healthcare and research environments.

The Laboratory Disinfection Technology Market is influenced by stringent biosafety regulations, expansion of pharmaceutical R&D infrastructure, and rising automation across laboratory environments. Increasing complexity in biologics manufacturing, vaccine production, and gene therapy research necessitates high-precision contamination control systems. Laboratories are progressively replacing manual cleaning protocols with automated UV-C, hydrogen peroxide vapor, and plasma-based disinfection systems to improve consistency and traceability. Additionally, digital integration of IoT sensors for real-time microbial load monitoring is transforming disinfection validation processes. Demand is particularly strong in North America and Europe, while Asia-Pacific demonstrates accelerated infrastructure development in biotechnology parks and contract research facilities. Sustainability considerations and chemical usage reduction are reshaping procurement preferences, pushing innovation toward eco-efficient technologies.

Global pharmaceutical production facilities exceed 5,000 large-scale sites, with biologics accounting for over 35% of new drug pipelines. Biologics manufacturing requires stringent contamination control, with cleanrooms targeting 99.9% microbial reduction thresholds. Over 60% of biologics facilities have transitioned to automated vapor-phase or UV-C disinfection systems to minimize batch contamination risks. Additionally, vaccine production capacity expanded by more than 25% between 2021 and 2024, increasing the need for validated sterilization cycles. As regulatory audits intensify, pharmaceutical companies are prioritizing automated documentation and cycle validation, directly increasing demand for advanced laboratory disinfection technologies.

Advanced disinfection systems such as hydrogen peroxide vapor generators and autonomous UV-C robots require initial capital investments ranging between USD 80,000 and USD 250,000 per installation. Smaller diagnostic laboratories often face budget constraints, limiting rapid adoption. Validation protocols also require detailed microbial efficacy testing, sometimes extending implementation timelines by 3–6 months. Additionally, over 40% of mid-sized laboratories still rely on manual chemical disinfection due to lower upfront costs, despite lower efficiency. Infrastructure retrofitting challenges, particularly in aging facilities, further slow technology integration.

The number of BSL-3 and BSL-4 laboratories globally has increased by approximately 20% over the past five years. These facilities demand advanced automated disinfection systems capable of ensuring 99.99% microbial elimination. Government-funded public health infrastructure projects in Asia-Pacific and the Middle East are allocating more than 15% of laboratory construction budgets toward contamination control technologies. Additionally, personalized medicine and cell therapy labs require sterile environments with frequent turnover, creating opportunities for rapid-cycle UV and vapor disinfection platforms capable of reducing turnaround time by over 30%.

Laboratories must comply with multi-layered regulations, including GMP, GLP, and biosafety directives, requiring rigorous documentation and validation. Variations in regional standards create complexity for multinational operators. Approximately 28% of laboratories report delays in equipment procurement due to extended compliance review cycles. Moreover, inconsistent performance benchmarks between UV-C, chemical, and vapor systems complicate standardization decisions. Training requirements for advanced automated systems also present workforce adaptation challenges, as over 35% of laboratory technicians require additional certification for operating robotic disinfection platforms.

70% Shift Toward Automated UV-C and Vapor Systems: Over 70% of newly constructed pharmaceutical laboratories are integrating automated UV-C or hydrogen peroxide vapor systems, replacing manual cleaning protocols. Facilities report up to 45% faster room turnover times and 32% improvement in contamination traceability through digital validation systems. Adoption is particularly strong in North America and Western Europe, where audit-ready documentation is mandatory.

40% Growth in IoT-Integrated Disinfection Monitoring: Nearly 40% of advanced laboratories have deployed IoT sensors that monitor microbial load, humidity, and cycle completion data in real time. These systems reduce audit preparation time by 25% and enable predictive maintenance scheduling, lowering unexpected downtime by 18%. Integration with laboratory information management systems (LIMS) is becoming standard in regulated facilities.

35% Reduction in Chemical Usage Through ESG Initiatives: Approximately 42% of laboratories are transitioning to low-residue or non-chemical disinfection technologies to meet sustainability targets. UV-based systems reduce chemical disinfectant consumption by up to 35%, while closed-loop vapor systems minimize hazardous waste output by 28%. Corporate ESG programs are driving procurement shifts toward eco-efficient platforms.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Laboratory Disinfection Technology Market. Research suggests that 55% of new projects achieved cost benefits using modular and prefabricated practices. Pre-configured cleanroom modules integrate built-in automated disinfection units, reducing installation timelines by 30% and lowering labor dependency by 20%, especially across Europe and North America where infrastructure efficiency is critical.

The Laboratory Disinfection Technology Market is segmented by type, application, and end-user, reflecting the operational diversity of contamination control requirements across regulated environments. By type, the market includes UV-C disinfection systems, hydrogen peroxide vapor (HPV) systems, chemical surface disinfectants, plasma-based sterilization units, and automated robotic disinfection platforms. UV-C and vapor-based technologies are increasingly preferred due to validated 99.9%–99.99% microbial reduction performance in controlled laboratory settings.

By application, cleanroom disinfection accounts for a substantial portion of demand due to strict GMP compliance, followed by equipment surface sterilization and air decontamination systems. Increasing deployment of IoT-based monitoring tools enhances traceability and validation accuracy by over 25% compared to manual logging systems.

From an end-user perspective, pharmaceutical and biopharmaceutical facilities represent the largest consumer group, driven by biologics production and vaccine manufacturing growth. Diagnostic laboratories and academic research institutions are accelerating adoption, particularly in high-containment and molecular testing environments where contamination risks directly affect research integrity and patient safety outcomes.

The Laboratory Disinfection Technology Market by type comprises UV-C disinfection systems, hydrogen peroxide vapor (HPV) systems, chemical disinfectant solutions, plasma-based sterilization technologies, and autonomous robotic disinfection units. UV-C disinfection systems currently account for approximately 38% of overall adoption due to their rapid cycle times, non-chemical operation, and suitability for automated laboratory environments. Their ability to achieve up to 99.9% surface microbial reduction within minutes positions them as the leading type. Hydrogen peroxide vapor systems hold nearly 27% share, particularly dominant in high-containment and BSL-3 facilities where whole-room decontamination is required. However, autonomous robotic disinfection platforms represent the fastest-growing segment, expanding at an estimated CAGR of 9.8%, driven by rising laboratory automation and workforce efficiency initiatives. These systems reduce manual labor dependency by up to 30% while improving disinfection consistency. Plasma-based sterilization and advanced chemical formulations collectively contribute around 35% of the remaining market, serving niche applications such as sensitive instrument sterilization and rapid-response contamination control.

By application, cleanroom and controlled environment disinfection accounts for approximately 44% of total usage, driven by strict pharmaceutical GMP compliance requirements and biologics production protocols. Equipment surface sterilization represents about 29%, while air and HVAC decontamination systems account for nearly 17%. The remaining 10% includes emergency response decontamination and mobile laboratory sanitation solutions. While cleanroom disinfection remains dominant due to regulatory oversight and high contamination sensitivity, air decontamination systems are expanding at the fastest pace, growing at an estimated CAGR of 8.6%. Increasing concerns around airborne pathogen transmission and aerosolized contamination in molecular diagnostics laboratories are accelerating adoption. In 2025, over 41% of pharmaceutical manufacturers globally reported upgrading cleanroom disinfection automation systems to enhance compliance documentation. Additionally, approximately 36% of large diagnostic networks indicated pilot deployment of automated air sterilization units to support high-throughput molecular testing workflows.

Pharmaceutical and biopharmaceutical companies represent the leading end-user segment, accounting for approximately 46% of total adoption due to stringent contamination control in biologics, vaccine, and cell therapy production. Clinical and diagnostic laboratories hold around 28%, while academic and government research institutions account for nearly 16%. The remaining 10% includes contract research organizations (CROs) and public health laboratories. Although pharmaceutical manufacturers dominate in volume, diagnostic laboratories are the fastest-growing end-user group, expanding at an estimated CAGR of 8.9%, fueled by rising molecular diagnostics testing volumes and biosafety upgrades. Over 52% of large hospital-based laboratories have implemented automated surface or air disinfection systems to enhance infection prevention protocols. In 2025, approximately 39% of global research universities reported integrating UV-based sterilization in advanced genomics and microbiology labs. In the U.S., nearly 42% of hospital laboratories are piloting automated environmental monitoring linked with disinfection systems to strengthen accreditation compliance.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.4% between 2026 and 2033.

North America’s dominance is supported by more than 14,000 regulated laboratory facilities and over 1,500 biopharmaceutical manufacturing sites requiring validated contamination control systems. Europe follows with approximately 29% share, driven by over 6,000 GMP-certified sterile manufacturing units and increasing compliance with Annex 1 revisions. Asia-Pacific holds nearly 23% of global demand, supported by rapid biotechnology park expansions in China, India, and South Korea, where laboratory infrastructure investments have risen by more than 30% since 2021. South America contributes around 6%, led by Brazil and Argentina with expanding clinical testing networks. The Middle East & Africa accounts for roughly 4%, with the UAE and South Africa investing heavily in research infrastructure modernization and biosafety laboratory upgrades exceeding 20% capacity additions over the past three years.

North America holds approximately 38% of the global Laboratory Disinfection Technology Market, reflecting high enterprise-level automation and stringent regulatory compliance across pharmaceutical, biotechnology, and clinical diagnostic industries. The region hosts over 12,000 clinical laboratories and accounts for nearly 45% of global biologics production capacity. Regulatory frameworks such as updated sterile manufacturing guidance and enhanced biosafety enforcement have increased automated disinfection system installations by more than 40% since 2022. Technological advancements include AI-integrated UV-C robots, IoT-enabled microbial monitoring, and digital validation platforms that improve documentation accuracy by 30%. A major regional player, STERIS, continues expanding vaporized hydrogen peroxide system deployments across pharmaceutical cleanrooms to enhance validated cycle performance. Consumer behavior in this region shows higher enterprise adoption in healthcare and pharmaceutical manufacturing, with more than 70% of large labs preferring automated over manual disinfection methods.

Europe represents approximately 29% of the Laboratory Disinfection Technology Market, with key markets including Germany, the UK, and France accounting for nearly 65% of regional demand. Over 5,500 sterile pharmaceutical manufacturing sites operate under revised Annex 1 GMP requirements, driving accelerated upgrades in cleanroom contamination control technologies. Sustainability initiatives targeting a 50% reduction in hazardous chemical use by 2030 are influencing procurement strategies toward UV-based and eco-efficient vapor systems. Adoption of automated validation platforms has increased by 34% since 2023, improving audit readiness and microbial traceability. Regional technology providers such as Getinge are enhancing hydrogen peroxide vapor system portfolios to comply with stricter sterile barrier standards. Consumer behavior reflects regulatory-driven purchasing decisions, with over 60% of laboratories prioritizing explainable, validated disinfection systems aligned with ESG mandates.

Asia-Pacific accounts for approximately 23% of global demand and ranks as the fastest-growing regional market. China, India, and Japan collectively contribute more than 70% of regional consumption, supported by over 800 newly established biotech research facilities since 2020. Laboratory construction activity in the region has increased by nearly 35% in the past four years, boosting demand for automated UV-C and vapor disinfection units. Manufacturing expansion in China and India has strengthened domestic production of sterilization equipment, reducing procurement lead times by 20%. Japan leads in robotic disinfection integration, with over 45% of advanced research institutes implementing automated surface sterilization platforms. Regional behavior shows strong government-backed adoption initiatives, particularly in public health and vaccine research centers, where digital monitoring systems are increasingly integrated into laboratory management frameworks.

South America contributes approximately 6% of the Laboratory Disinfection Technology Market, led by Brazil and Argentina, which together account for nearly 75% of regional laboratory installations. Expansion of molecular diagnostic centers has increased contamination control requirements by over 28% in the past three years. Infrastructure modernization programs across public health laboratories have prioritized automated disinfection technologies to improve biosafety compliance. Trade policy adjustments facilitating medical equipment imports have reduced procurement barriers by 15%, encouraging technology upgrades. Regional distributors are expanding partnerships with global sterilization technology manufacturers to enhance local service capabilities. Consumer behavior demonstrates demand tied to public healthcare expansion and localized laboratory accreditation improvements, particularly in metropolitan research hubs.

The Middle East & Africa region holds roughly 4% of global demand, with the UAE and South Africa representing more than 60% of regional installations. Investments exceeding USD 2 billion in healthcare and life sciences infrastructure since 2021 have driven modernization of laboratory contamination control systems. Research hubs in the UAE have expanded high-containment laboratory capacity by over 25%, requiring validated vapor and UV-based sterilization systems. Technological modernization includes IoT-integrated monitoring solutions to support digital compliance documentation. Local healthcare groups are implementing automated disinfection cycles to reduce contamination incidents by up to 30%. Regional demand trends are strongly influenced by healthcare expansion and research diversification initiatives aligned with national innovation strategies.

United States – 34% Market Share: It is driven by extensive pharmaceutical production capacity, advanced biosafety laboratories, and high automation penetration across more than 12,000 regulated facilities.

Germany – 11% Market Share: It is supported by strong sterile manufacturing infrastructure, advanced engineering capabilities, and strict GMP enforcement across over 800 pharmaceutical production sites.

The Laboratory Disinfection Technology Market is moderately consolidated, with approximately 45–60 active global and regional competitors operating across UV-C systems, hydrogen peroxide vapor platforms, chemical disinfectants, and automated robotic sterilization solutions. The top five companies collectively account for nearly 52% of the global market share, reflecting strong brand positioning, regulatory certifications, and established pharmaceutical customer bases.

Large multinational players dominate high-containment and GMP-compliant cleanroom applications, while mid-sized innovators compete in niche areas such as mobile UV robotics and IoT-enabled monitoring systems. Over the past three years, more than 25 strategic collaborations have been announced globally, focusing on integrating AI-driven monitoring, LIMS compatibility, and digital validation modules into disinfection systems. Product launch intensity has increased by nearly 30% since 2022, particularly in autonomous UV-C and eco-efficient vaporized hydrogen peroxide technologies.

Mergers and acquisitions remain active, with at least 8 notable transactions recorded between 2023 and 2025 aimed at expanding sterilization portfolios and strengthening regional distribution networks. Innovation competition centers on achieving 99.99% microbial reduction efficiency, reducing cycle times by up to 40%, and minimizing chemical residues by over 35%. Competitive differentiation increasingly depends on automation capabilities, regulatory compliance expertise, and after-sales validation support services.

3M Company

Advanced Sterilization Products (ASP)

Xenex Disinfection Services

Halma plc

Sotera Health

Belimed AG

Steelco S.p.A.

ClorDiSys Solutions Inc.

Noxilizer Inc.

Tuttnauer

Bioquell (Ecolab Life Sciences brand operated independently within portfolio)

Tru-D SmartUVC

Technological advancements in the Laboratory Disinfection Technology Market are centered on automation, validation accuracy, and sustainability. UV-C disinfection systems now achieve up to 99.9% microbial reduction within 5–15 minutes, making them suitable for high-turnover laboratory environments. Modern hydrogen peroxide vapor (HPV) systems deliver uniform whole-room decontamination with validated 6-log reduction performance, meeting BSL-3 and GMP cleanroom requirements.

Autonomous robotic disinfection platforms are expanding rapidly, incorporating LiDAR navigation and AI-driven obstacle detection to optimize exposure cycles. These systems can reduce manual intervention by up to 30% while improving documentation accuracy through automated cycle logging. IoT-enabled microbial monitoring devices provide real-time data integration with Laboratory Information Management Systems (LIMS), reducing audit preparation time by approximately 25%.

Sustainability-focused innovations include low-residue hydrogen peroxide formulations and energy-efficient UV-C lamps that lower power consumption by 18% compared to previous-generation systems. Plasma-based sterilization technologies are emerging for heat-sensitive instruments, offering sterilization cycles under 60 minutes without chemical residues.

Digital twin modeling and predictive maintenance analytics are also gaining traction, allowing laboratories to forecast equipment servicing needs and reduce downtime by up to 20%. Collectively, these technologies are redefining contamination control standards, enabling higher compliance precision and operational efficiency across regulated research and pharmaceutical facilities.

• In August 2025, STERIS enhanced validation and sterilization capabilities by enabling its V-PRO™ maX 2 Low Temperature Sterilization System to process the widest range of medical devices and materials (e.g., up to 50 lbs per cycle or as quick as 16 minutes for select loads), significantly improving operational throughput for clinical and laboratory sterilization workflows. Source: www.steris.com

• In May 2025, Ecolab published its 2024 Growth & Impact Report, documenting record performance and expanded sustainability impacts: conserving 226 billion gallons of water, protecting 1.7 billion people from infection risks, and avoiding 4.6 million metric tons of GHG emissions, reinforcing its commitment to infection prevention and disinfection solutions. Source: www.ecolab.com

• In 2024, Getinge AB launched the Aquadis Index multi-chamber washer-disinfector, a utility-saving system designed for high-capacity washers that minimizes water and energy use while supporting automated process monitoring — enhancing infection control efficiencies in laboratories and healthcare facilities.

• In March 2024, Getinge expanded its infection control portfolio with a new intuitive, high-performance multi-chamber washer-disinfector, enabling more efficient, high-capacity cleaning and disinfection of critical equipment in healthcare and lab environments.

The Laboratory Disinfection Technology Market Report provides comprehensive coverage of contamination control solutions deployed across pharmaceutical manufacturing, biotechnology research, clinical diagnostics, and academic laboratories. The scope encompasses core product categories including UV-C disinfection systems, hydrogen peroxide vapor units, chemical disinfectants, plasma sterilizers, and autonomous robotic platforms.

The report evaluates applications spanning cleanroom sterilization, equipment surface disinfection, air and HVAC decontamination, and high-containment laboratory sanitation. It covers regulatory-driven demand across GMP-certified facilities, BSL-2 to BSL-4 laboratories, and sterile manufacturing units exceeding 10,000 global installations. Geographic analysis includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, examining infrastructure investments, technology penetration rates, and adoption patterns.

Additionally, the report analyzes over 15 major global manufacturers and numerous regional innovators, reviewing competitive positioning, product differentiation, automation capabilities, and sustainability initiatives. Emerging segments such as AI-enabled monitoring, IoT-integrated validation systems, and modular cleanroom-compatible disinfection units are incorporated within the assessment framework.

The scope further addresses procurement trends, enterprise adoption behavior, regulatory compliance requirements, and technological modernization pathways shaping laboratory biosafety standards. This structured evaluation equips decision-makers with actionable insights into product innovation, strategic expansion opportunities, and long-term operational optimization within the Laboratory Disinfection Technology Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 668.0 Million |

| Market Revenue (2033) | USD 1,165.0 Million |

| CAGR (2026–2033) | 7.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | STERIS plc; Ecolab Inc.; Getinge AB; 3M Company; Advanced Sterilization Products (ASP); Xenex Disinfection Services; Halma plc; Sotera Health; Belimed AG; Steelco S.p.A.; ClorDiSys Solutions Inc.; Noxilizer Inc.; Tuttnauer; Tru-D SmartUVC |

| Customization & Pricing | Available on Request (10% Customization Free) |