Reports

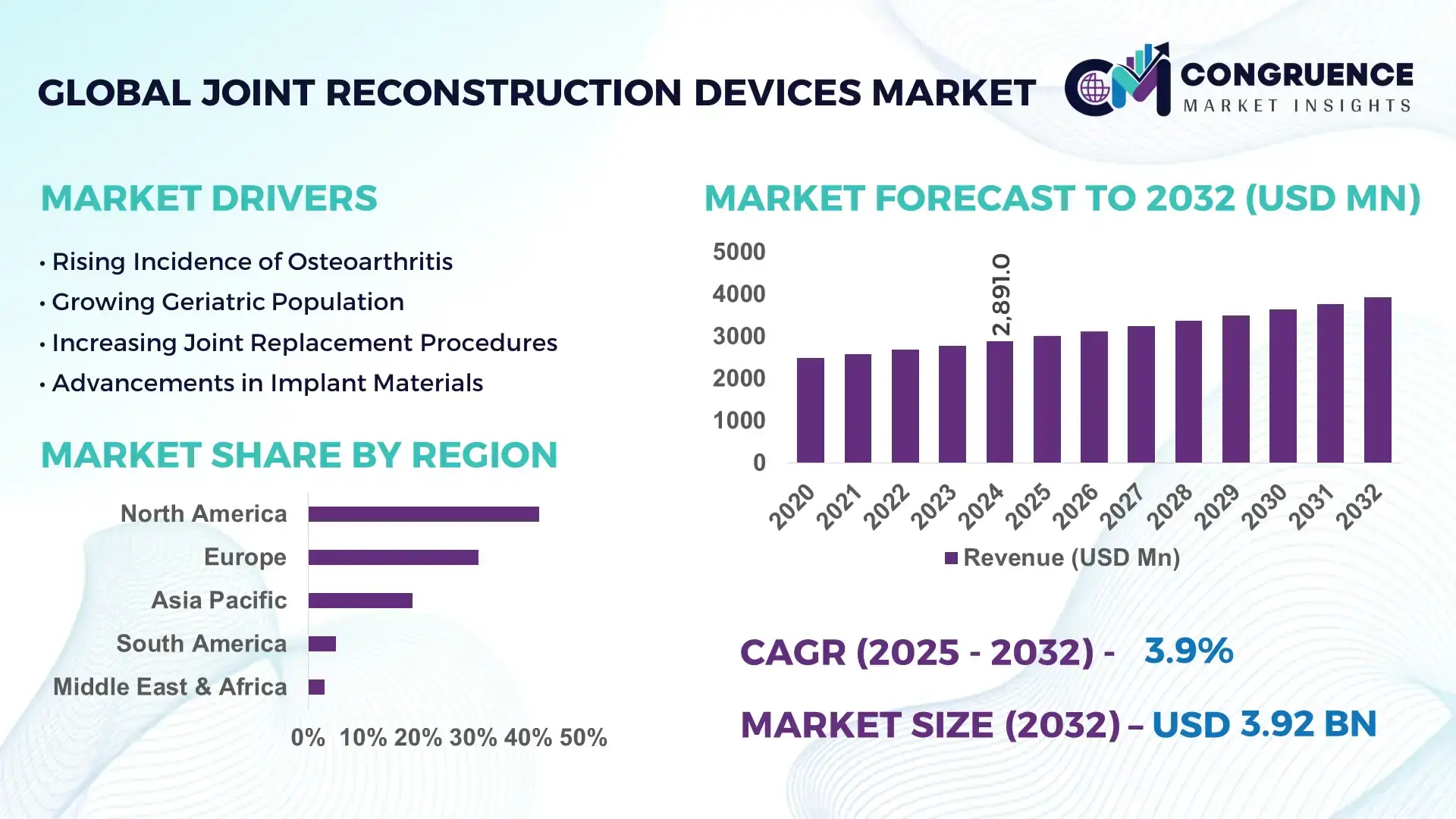

The Global Joint Reconstruction Devices Market was valued at USD 2,891.0 Million in 2024 and is anticipated to reach a value of USD 3,920.2 Million by 2032, expanding at a CAGR of 3.88% between 2025 and 2032, according to an analysis by Congruence Market Insights. Steady procedural volume growth supported by aging populations, rising osteoarthritis incidence, and continuous implant material innovation is sustaining long-term market expansion.

The United States dominates the global Joint Reconstruction Devices Market in terms of industrial depth and technological leadership. The country hosts over 6,000 orthopedic-focused hospitals and ambulatory surgical centers, with more than 1.2 million joint replacement procedures performed annually. Domestic manufacturers operate high-capacity production facilities capable of delivering millions of knee, hip, and shoulder implants per year, supported by annual orthopedic R&D investments exceeding USD 2.5 billion. Advanced applications include robotic-assisted joint replacement systems deployed in over 35% of large hospitals, while additive manufacturing is increasingly used for patient-specific implants. Adoption of ceramic-on-polyethylene and titanium porous coatings has expanded significantly, improving implant longevity and osseointegration outcomes.

Market Size & Growth: Valued at USD 2,891.0 Million in 2024, projected to reach USD 3,920.2 Million by 2032, growing at a CAGR of 3.88%, driven by rising elective orthopedic procedures and implant durability improvements.

Top Growth Drivers: Aging population impact (42%), increase in sports-related injuries (28%), and adoption of minimally invasive joint replacement techniques (21%).

Short-Term Forecast: By 2028, robotic-assisted joint reconstruction is expected to improve surgical precision metrics by approximately 30%.

Emerging Technologies: Robotic-assisted surgery platforms, 3D-printed patient-specific implants, and advanced bearing surface materials.

Regional Leaders: North America (USD 1,520 Million by 2032) with robotic adoption growth; Europe (USD 1,120 Million by 2032) driven by public healthcare upgrades; Asia Pacific (USD 980 Million by 2032) supported by procedure volume expansion.

Consumer/End-User Trends: Hospitals account for nearly 68% of implant usage, while ambulatory surgical centers show the fastest adoption growth.

Pilot or Case Example: In 2023, a robotic knee replacement program in Japan achieved a 22% reduction in post-operative recovery time.

Competitive Landscape: Market leader holds approximately 18% share, followed by Zimmer Biomet, DePuy Synthes, Smith+Nephew, and Stryker.

Regulatory & ESG Impact: Increased compliance with implant traceability regulations and material recyclability initiatives.

Investment & Funding Patterns: Over USD 1.1 Billion invested globally in orthopedic implant innovation during the last three years.

Innovation & Future Outlook: Integration of AI-driven surgical planning and smart implants is reshaping long-term clinical outcomes.

The Joint Reconstruction Devices Market spans knee, hip, shoulder, and extremity implants, with knee reconstruction contributing roughly 46% of procedural demand. Recent innovations in porous titanium structures and sensor-enabled implants are enhancing post-surgical monitoring. Regulatory focus on implant safety, combined with rising outpatient procedure volumes in Asia Pacific, is reshaping consumption patterns, while personalized orthopedic solutions define future growth pathways.

The Joint Reconstruction Devices Market holds significant strategic relevance within global healthcare systems as it directly addresses mobility restoration, workforce productivity, and long-term quality-of-life outcomes. From a strategic standpoint, hospitals and device manufacturers are increasingly aligning investments with measurable surgical efficiency gains and lifecycle implant performance. For example, robotic-assisted joint reconstruction delivers nearly 25% improvement in implant alignment accuracy compared to conventional manual techniques, directly reducing revision surgery risks.

From a regional benchmark perspective, North America dominates in procedure volume, while Europe leads in technology adoption with nearly 48% of orthopedic centers utilizing digital preoperative planning tools. In Asia Pacific, expanding healthcare infrastructure is accelerating adoption, particularly in urban hospital networks.

Short-term projections indicate that by 2027, AI-enabled surgical planning systems are expected to reduce average operating room time by approximately 18%, improving hospital throughput and cost efficiency. Compliance and ESG considerations are also shaping strategic decisions, with firms committing to 30% recyclable implant packaging and 20% waste reduction targets by 2030.

A micro-scenario highlights that in 2024, a South Korean hospital network achieved a 19% reduction in post-operative complications through the deployment of smart sensor-enabled knee implants. Looking ahead, the Joint Reconstruction Devices Market is positioned as a pillar of resilience, regulatory compliance, and sustainable growth, integrating precision medicine principles with scalable surgical technologies.

The Joint Reconstruction Devices Market dynamics are shaped by demographic shifts, procedural innovation, and healthcare infrastructure evolution. Rising life expectancy has increased demand for durable implants capable of supporting active lifestyles beyond age 65. Technological integration—such as robotics, navigation systems, and advanced biomaterials—continues to redefine surgical standards. At the same time, payer emphasis on outcome-based reimbursement models is influencing device selection and procedural efficiency. Emerging markets are contributing incremental procedure volumes, while developed regions focus on revision surgeries and high-performance implants. Supply chain localization and regulatory harmonization are further influencing manufacturing strategies and product lifecycle management across the Joint Reconstruction Devices Market.

The global population aged 65 and above is expanding rapidly, directly increasing the incidence of degenerative joint conditions. Clinical data indicate that more than 35% of individuals over 60 exhibit radiographic signs of osteoarthritis, driving sustained demand for joint replacement procedures. Knee and hip reconstructions represent the majority of these interventions, with procedure volumes increasing annually in hospital and outpatient settings. Improved implant longevity—now exceeding 20 years in many cases—has also increased physician confidence in recommending surgery earlier in disease progression. Together, these factors significantly amplify procedural throughput and device utilization rates.

Joint reconstruction procedures remain capital-intensive, with implant systems, robotic platforms, and post-operative care contributing to elevated costs. In several regions, total procedure expenses can exceed USD 15,000 per case, limiting access in cost-sensitive healthcare systems. Reimbursement variability further complicates adoption, particularly for premium implants and advanced surgical technologies. Budget constraints in public healthcare systems have slowed equipment upgrades, while price sensitivity among patients continues to restrain broader penetration of next-generation joint reconstruction solutions.

Personalized joint reconstruction solutions represent a high-impact opportunity. Advances in imaging and additive manufacturing now enable patient-specific implants that improve anatomical fit and joint kinematics. Clinical observations show that customized implants can reduce intraoperative adjustment time by up to 30% and improve post-operative comfort scores. Expanding adoption in revision surgeries and complex deformity cases is opening new revenue streams, particularly in high-volume orthopedic centers seeking differentiation through precision medicine approaches.

Regulatory approval for joint reconstruction devices involves rigorous biomechanical testing, clinical validation, and post-market surveillance. Approval timelines can extend beyond 24 months, delaying product launches and increasing development costs. Variations in regulatory frameworks across regions further complicate global commercialization strategies. Compliance requirements for traceability, sterilization validation, and material safety add operational burdens, particularly for smaller manufacturers attempting to scale internationally.

Expansion of Robotic-Assisted Joint Replacement: Robotic systems are now used in approximately 32% of knee replacement procedures, improving implant positioning accuracy by over 25% and reducing intraoperative variability.

Growth in Outpatient Joint Reconstruction: Same-day discharge procedures have increased by 41% over the past four years, driven by minimally invasive techniques and enhanced recovery protocols.

Advancements in Implant Materials: Adoption of ceramic-on-polyethylene bearings has risen by 38%, significantly reducing wear rates and extending implant service life.

Integration of Smart and Sensor-Enabled Implants: Early deployment of sensor-equipped knee implants has demonstrated 15–20% improvement in post-surgical rehabilitation monitoring efficiency, enabling data-driven follow-up care and outcome optimization.

The Joint Reconstruction Devices Market segmentation reflects differentiated demand patterns across product types, clinical applications, and end-user categories. From a product perspective, knee, hip, shoulder, and extremity reconstruction systems dominate usage, shaped by demographic aging and mobility-related disorders. Application-wise, primary joint replacement procedures account for the largest procedural volumes, while revision surgeries and trauma-related reconstructions are gaining prominence due to implant longevity considerations. End-user adoption is concentrated in hospitals, but ambulatory surgical centers and specialized orthopedic clinics are increasingly influential as minimally invasive techniques reduce inpatient dependency. Segmentation trends indicate that technological sophistication, procedural efficiency, and patient recovery outcomes are key determinants influencing purchasing and adoption decisions across all segments.

The Joint Reconstruction Devices Market by type is led by knee reconstruction devices, which account for approximately 46% of total adoption. This leadership is supported by the high prevalence of knee osteoarthritis, particularly among populations aged over 60, and the procedural standardization of total knee arthroplasty across healthcare systems. Hip reconstruction devices follow closely with about 34% adoption, benefiting from strong clinical outcomes and long implant lifespans. The fastest-growing type is shoulder reconstruction devices, expanding at an estimated CAGR of 5.2%, driven by increasing sports injuries, improved anatomical implant designs, and broader surgical training adoption. Extremity reconstruction devices (including ankle, elbow, and wrist systems) play a niche but growing role, collectively contributing around 20% of overall device utilization, particularly in trauma and deformity correction cases.

By application, primary joint replacement procedures represent the leading segment with nearly 62% of total procedural adoption, reflecting their routine use in managing degenerative joint diseases. These procedures benefit from standardized surgical pathways and predictable clinical outcomes. Revision joint reconstruction accounts for roughly 24%, driven by aging implant cohorts and rising expectations for long-term mobility. The fastest-growing application segment is revision joint surgery, expanding at an estimated CAGR of 5.6%, supported by increased implant lifespan monitoring and higher survivorship among younger recipients requiring secondary interventions. Other applications, including trauma-related and partial joint reconstructions, collectively contribute around 14% of demand. Consumer and institutional adoption trends indicate that over 42% of hospitals in the United States are piloting digital preoperative planning tools for joint reconstruction, while nearly 36% of orthopedic patients report preference for minimally invasive joint replacement options due to faster recovery timelines.

From an end-user perspective, hospitals dominate the Joint Reconstruction Devices Market, accounting for approximately 68% of total device utilization. This dominance reflects their ability to manage complex cases, maintain advanced surgical infrastructure, and support post-operative rehabilitation. Ambulatory surgical centers (ASCs) are the fastest-growing end-user segment, expanding at a CAGR of 6.1%, driven by cost efficiencies, shorter patient stays, and increasing payer acceptance of outpatient joint replacement. Specialty orthopedic clinics and rehabilitation centers collectively represent about 24% of end-user adoption, particularly for follow-up procedures and partial joint interventions. Industry adoption metrics indicate that nearly 40% of ASCs globally now perform at least one form of joint reconstruction procedure, while over 55% of orthopedic surgeons report increased reliance on digital navigation or robotic assistance in high-volume centers.

North America accounted for the largest market share at 42% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.6% between 2025 and 2032.

Region-wise performance in the Joint Reconstruction Devices Market highlights strong contrasts in maturity, infrastructure, and procedural volumes. North America leads due to high surgical penetration, advanced reimbursement frameworks, and early adoption of robotic-assisted joint reconstruction. Europe follows with a well-established public healthcare base and standardized orthopedic protocols across major economies. Asia-Pacific is emerging as a high-growth region, supported by rapid hospital infrastructure expansion, increasing procedure volumes, and improving affordability. South America and the Middle East & Africa collectively represent a smaller but steadily expanding portion of global demand, driven by improving access to orthopedic care, gradual policy support, and rising awareness of mobility-restoring surgical solutions. Across regions, differences in patient demographics, outpatient adoption rates, and technology penetration continue to shape localized market trajectories.

North America accounts for approximately 42% of global Joint Reconstruction Devices Market demand, supported by high procedural volumes and strong clinical capacity. The region performs over 1.3 million joint replacement surgeries annually, primarily across knee and hip procedures. Demand is driven by hospitals, orthopedic specialty centers, and a rapidly expanding ambulatory surgical center network. Regulatory support through streamlined implant approvals and reimbursement alignment has strengthened adoption of next-generation implants. Technological advancements include widespread use of robotic-assisted surgery, now integrated into nearly 35% of large orthopedic hospitals, and digital preoperative planning tools. Local manufacturers and device leaders are expanding smart implant portfolios and investing in porous titanium and sensor-enabled designs. Consumer behavior reflects a preference for minimally invasive procedures, with over 48% of patients favoring outpatient joint replacement when clinically eligible.

Europe represents around 31% of the global Joint Reconstruction Devices Market, with Germany, the UK, and France accounting for the majority of regional procedures. Public healthcare systems drive consistent demand, performing more than 900,000 joint replacements annually across the region. Regulatory frameworks emphasize implant safety, traceability, and lifecycle assessment, accelerating demand for durable and explainable implant technologies. Sustainability initiatives are influencing procurement, with hospitals prioritizing reusable instrumentation and recyclable packaging. Adoption of navigation-assisted and robotic joint reconstruction has reached approximately 29% of tertiary hospitals. Regional manufacturers are focusing on low-wear bearing surfaces and cementless fixation systems. Consumer behavior varies, with European patients demonstrating higher acceptance of standardized implant models aligned with national reimbursement guidelines.

Asia-Pacific ranks third by market size but leads global growth momentum, contributing nearly 19% of total demand in 2024. China, Japan, and India are the top consuming countries, together performing over 1.1 million joint replacement procedures annually. Infrastructure expansion, particularly the addition of multi-specialty hospitals, is accelerating device adoption. Regional manufacturing hubs are scaling production of cost-efficient implants, while innovation clusters in Japan and South Korea focus on robotics and biomaterials. Digital surgical planning adoption has crossed 22% in urban hospitals, supporting precision outcomes. Consumer behavior reflects rising awareness, with increasing preference for mobility-restoring surgeries among patients aged 55–70, particularly in metropolitan areas.

South America accounts for approximately 5% of the global Joint Reconstruction Devices Market, led by Brazil and Argentina. The region performs an estimated 180,000 joint reconstruction procedures annually, primarily in urban centers. Public-private healthcare partnerships are improving access to orthopedic surgeries, while import-friendly trade policies are easing device availability. Infrastructure upgrades in tertiary hospitals are enabling adoption of modern implant systems. Regional distributors and manufacturers are expanding surgeon training programs to improve procedural outcomes. Consumer behavior shows increasing demand for joint replacement among working-age populations, driven by occupational injuries and lifestyle-related joint degeneration.

The Middle East & Africa region contributes roughly 3% of global market demand, with the UAE and South Africa as leading countries. High-end private hospitals in the Gulf region are driving adoption of advanced joint reconstruction technologies, including robotic systems and customized implants. Government-backed healthcare modernization programs are expanding orthopedic capacity, particularly in urban hubs. Trade partnerships are improving device availability across Africa. Consumer behavior is bifurcated, with premium care demand concentrated in private facilities, while public systems gradually expand access to essential joint reconstruction procedures.

United States – 38% Market Share: Strong production capacity, high procedure volumes, and advanced surgical technology adoption support leadership in the Joint Reconstruction Devices Market.

Germany – 9% Market Share: High orthopedic procedure density, robust public healthcare funding, and standardized implant regulations drive sustained demand in the Joint Reconstruction Devices Market.

The competitive environment in the Joint Reconstruction Devices Market is moderately consolidated yet intensely innovative, with dozens of active competitors ranging from global medical device conglomerates to specialized orthopedic innovators. The market features strategic positioning by key players leveraging product launches, technology upgrades, partnerships, and capacity expansions to secure procedural adoption across global healthcare systems. The top 5 companies collectively represent an estimated ~65%–70% combined share of total global joint reconstruction device deployment, reflecting concentrated leadership but with competitive pressure from emerging firms and niche innovators.

Key players are engaged in rapid technological advancement trends, including robotic-assisted surgical platforms, 3D-printed patient-specific implants, sensor-enabled smart devices, and digital preoperative planning ecosystems. Strategic initiatives in the past 18-24 months include multiple FDA clearances of advanced robotic systems, expanded global manufacturing footprints, and industry partnerships aimed at integrating artificial intelligence and augmented reality into surgical workflows. Competitive dynamics are further shaped by mergers and acquisitions; for example, leading orthopedic firms continue to pursue portfolio expansion through bolt-ons and targeted acquisitions to broaden joint reconstruction offerings and address unmet clinical needs.

The market’s nature reflects both high innovation intensity and capital commitment, as firms allocate significant resources to R&D, regulatory compliance, and commercial footprint enhancements. Regional competition varies, with North American and European players typically leading in technology adoption, while Asia-Pacific competitors are expanding through manufacturing scale and cost competitiveness. Overall, the competitive landscape prioritizes clinical performance, surgical precision, and integrated procedural solutions as differentiators in this evolving medical devices sector.

DePuy Synthes

Medtronic

Aesculap Inc.

CONMED Corporation

DJO LLC

NuVasive, Inc.

Wright Medical Group N.V.

The Joint Reconstruction Devices Market is being reshaped by a wave of current and emerging technologies that are enhancing clinical precision, patient outcomes, and operational efficiencies. A major technological trend is the uptake of robotic-assisted surgical systems designed to support surgeons in knee, hip, and shoulder replacements with sub-millimeter accuracy, reducing variability in implant alignment and improving functional outcomes. Recent iterations of these platforms include advanced workflow software, image integration, and haptic-feedback mechanisms. Digital surgical planning tools, integrating patient imaging with cloud-based analytics, allow customized preoperative procedures that align implant selection with anatomical nuances, significantly improving fit and stability.

Additive manufacturing (3D printing) is another pivotal innovation, enabling patient-specific implants tailored to unique anatomical structures, and prototypes are increasingly used for complex cases to reduce intraoperative adjustments. Metal additive techniques also allow creation of lattice structures that promote bone in-growth and reduce implant weight while preserving structural strength. Smart implants embedded with sensors provide real-time postoperative monitoring, enabling data-driven rehabilitation strategies and early detection of complications.

Emerging technologies such as augmented reality (AR) and mixed reality (MR) platforms support surgeons in real-time visualization of critical anatomy during joint reconstruction, potentially reducing operative times and enhancing precision. Integration of machine learning algorithms into surgical robotics and imaging systems is improving automation of landmark identification, implant sizing, and trajectory planning.

The market also sees innovation in biomaterials, with high-cross-linked polyethylene, ceramic composites, and novel coatings enhancing wear resistance and long-term durability. These technological advances are supported by adjacent digital health solutions, including postoperative telemonitoring and AI-augmented rehabilitation tools, driving a shift toward comprehensive, data-enriched joint care ecosystems. Together, these technologies are not only transforming surgical practice but also redefining patient expectations for recovery timelines and functional outcomes in joint reconstruction procedures.

At the AAOS 2025 Annual Meeting, Smith+Nephew showcased advanced orthopaedic reconstruction technologies including the expanded CORI Surgical System (robotics and pre-op planning), CATALYSTEM Primary Hip System, and the FDA-cleared AETOS Stemless Shoulder option, underlining ongoing clinical and digital innovation. Source: www.smith-nephew.com

In Q2 2024, Stryker unveiled the Mako Total Knee 2.0 robotic platform upgrade, featuring improved software and surgeon interface enhancements aimed at optimizing total knee replacement precision and procedural efficiency.

In Q2 2024, Smith+Nephew launched its AETOS Shoulder System with full U.S. market availability, designed for total shoulder arthroplasty with integrated 3D planning software to support surgical precision.

In February 2024, AddUp and Anatomic Implants announced collaboration on a 510(k) submission for the world’s first 3D-printed toe joint replacement solution, highlighting advancements in additive-manufactured orthopedic implants.

The Joint Reconstruction Devices Market Report offers a comprehensive analytical framework covering the full breadth of this medical device segment. It encompasses segmentation by product type, including knee, hip, shoulder, and extremity reconstruction systems, each differentiated by surgical technique, implant materials, and technological integration. The report examines clinical applications, such as primary joint replacement, revision surgeries, minimally invasive procedures, and trauma-related reconstructions, highlighting procedural volumes and evolving clinical pathways across healthcare settings.

Geographically, the scope includes regional assessments across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, detailing unique adoption trends, infrastructure maturity, regulatory landscapes, and end-user preferences. End-user analysis spans hospitals, ambulatory surgical centers, specialty orthopedic clinics, and outpatient procedural hubs, reflecting divergent operational models and consumer behavior in joint reconstruction adoption.

Technological focus areas within the report include robotic surgical systems, digital preoperative planning tools, additive manufacturing technologies, smart implant innovations, and advanced biomaterials that enhance implant performance and patient outcomes. The report also identifies innovation clusters and regional technology hubs, as well as emerging trends such as AI-augmented surgical assistance, sensor-enabled postoperative monitoring, and augmented reality surgical guidance.

Industry focus areas address competitive dynamics, strategic initiatives, regulatory influences, and evolving reimbursement models affecting device deployment and market growth strategies. By integrating quantitative segmentation parameters with qualitative insights, the report serves as a decision-oriented resource for professionals, investors, and enterprise leaders seeking to understand opportunities, challenges, and future trajectories within the joint reconstruction devices landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 2,891.0 Million |

| Market Revenue (2032) | USD 3,920.2 Million |

| CAGR (2025–2032) | 3.88% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Zimmer Biomet Holdings, Inc., Stryker Corporation, Smith+Nephew plc, DePuy Synthes, Medtronic, Aesculap Inc., CONMED Corporation, DJO LLC, NuVasive, Inc., Wright Medical Group N.V. |

| Customization & Pricing | Available on Request (10% Customization Free) |