Reports

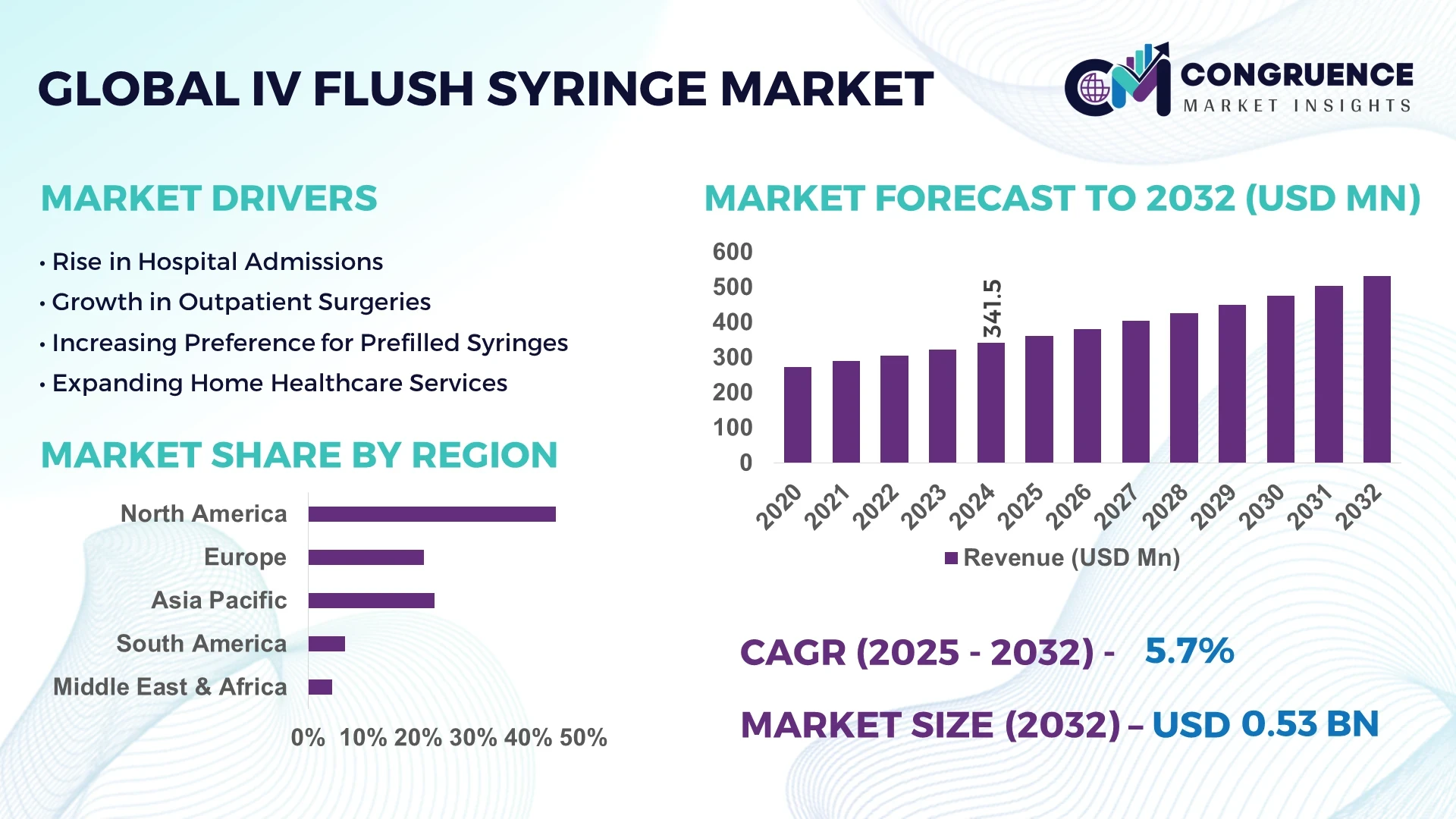

The Global IV Flush Syringe Market was valued at USD 341.5 Million in 2024 and is anticipated to reach a value of USD 532.1 Million by 2032, expanding at a CAGR of 5.7% between 2025 and 2032.

The increasing use of intravenous (IV) devices in healthcare settings for the administration of fluids and medications is a key factor driving market growth. Moreover, innovations in the production of IV flush syringes, such as pre-filled syringes and easy-to-use designs, are expected to enhance market adoption across various regions.

The United States currently dominates the IV flush syringe market, driven by its advanced healthcare infrastructure, high healthcare spending, and the growing demand for IV catheters and related medical products. With numerous hospitals, surgical centers, and outpatient facilities, the U.S. is a key market for IV flush syringes, as these devices are used extensively to ensure catheter patency and prevent thrombus formation in both inpatient and outpatient care settings.

Furthermore, advancements in healthcare technologies are also contributing to the growth of the IV flush syringe market, as hospitals and clinics increasingly adopt devices that improve patient safety and procedural efficiency. The global demand for these products is further supported by rising incidences of chronic diseases such as diabetes, cardiovascular conditions, and cancer, which require frequent IV access.

Artificial Intelligence (AI) is increasingly making its way into the IV flush syringe market, transforming both the manufacturing processes and the use of these syringes in healthcare. AI-based technologies are being utilized to enhance the design, accuracy, and safety of syringes used for flushing IV catheters. By integrating AI into the production of medical devices, manufacturers are improving quality control, ensuring that each syringe meets strict medical standards and reducing the risk of defects. AI-powered systems are also being used to monitor IV therapy and improve the accuracy of catheter flushes, ensuring that patients receive the right amount of saline or medication through precise dosing.

One of the most notable advancements is the application of AI in smart syringe systems that automatically adjust the volume of fluid used in an IV flush, based on real-time patient data and medical needs. These AI-enabled syringes reduce the risk of human error, improve patient outcomes, and streamline hospital workflows. Additionally, the use of AI helps manufacturers track and predict demand for these devices more accurately, enabling more efficient inventory management and distribution.

AI is also playing a role in the research and development (R&D) of more advanced IV flush syringes. Through predictive analytics, AI tools assist in identifying trends and developing new syringe models that better meet the evolving needs of patients and healthcare providers. This includes improving syringe ergonomics, user-friendliness, and compatibility with existing medical equipment. These innovations are expected to further shape the future of the IV flush syringe market, making healthcare procedures safer, more efficient, and more cost-effective.

“In 2024, a leading medical device company introduced a smart IV flush syringe system that utilizes AI to monitor and adjust fluid flow based on real-time patient vitals, ensuring optimal catheter flushing. This system has significantly reduced the occurrence of catheter blockages and enhanced patient safety in critical care units.”

The demand for enhanced safety features in medical devices, including IV flush syringes, is a key driver in the market. As patient safety becomes a top priority in healthcare settings, the adoption of syringes equipped with features such as air bubble prevention, precise fluid delivery, and easy-to-use mechanisms has increased. This trend is particularly prominent in hospitals, surgical centers, and home healthcare settings, where IV flush syringes play a critical role in preventing complications such as thrombosis or catheter-related infections.

The rising costs of raw materials and stringent regulatory requirements for medical devices are significant restraints to market growth. Manufacturers are under increasing pressure to meet the high standards set by regulatory bodies such as the FDA and EMA. This has resulted in higher production costs, which can make it challenging for smaller manufacturers to compete and for new products to enter the market. Additionally, the need for constant updates and testing of syringes to comply with evolving safety regulations adds another layer of complexity to market dynamics.

The growing trend of home healthcare is creating new opportunities for the IV flush syringe market. With an increasing number of patients receiving IV treatments at home, there is a rising demand for easy-to-use and safe medical devices, including IV flush syringes. As more people opt for home care to manage chronic conditions, manufacturers are focusing on developing syringes that are not only effective but also simple for non-medical professionals to use. This expansion into home healthcare is expected to drive the demand for IV flush syringes in the coming years.

One of the key challenges facing the IV flush syringe market is the complexity of the global supply chain. Disruptions caused by factors such as natural disasters, pandemics, or geopolitical tensions can affect the availability of raw materials and the timely delivery of finished products. Manufacturers may also face difficulties in meeting fluctuating demand levels, particularly during periods of heightened healthcare needs, which can lead to delays and shortages. Addressing these supply chain challenges is crucial for ensuring consistent market growth and meeting the needs of healthcare providers.

Rising Demand for Automated Syringe Systems: The demand for automated IV flush syringe systems is on the rise as hospitals and clinics seek to improve efficiency and reduce human error. These systems allow for the automatic administration of IV flushes, based on real-time patient data, which enhances safety and optimizes workflow.

Shift Towards Prefilled Syringes: Prefilled IV flush syringes are gaining popularity due to their ease of use and ability to reduce contamination risks. Healthcare providers are increasingly adopting prefilled syringes to streamline procedures and reduce the need for manual preparation, particularly in emergency or critical care situations.

Focus on Sustainability: As environmental concerns continue to grow, there is an increasing emphasis on producing IV flush syringes using sustainable materials. Manufacturers are exploring biodegradable and recyclable options, in response to global initiatives to reduce plastic waste and the environmental impact of medical devices.

Growth in Demand for Single-Use Devices: The preference for single-use IV flush syringes is increasing, driven by the need to minimize the risk of infection transmission. Hospitals and clinics are increasingly favoring disposable syringes for their convenience, cost-effectiveness, and ability to reduce cross-contamination in sterile environments.

The IV flush syringe market can be broadly segmented by type, application, and end-user. Each of these segments presents unique growth opportunities driven by technological advancements, consumer needs, and healthcare trends. By type, the market is divided into saline syringes, heparin syringes, and others. Applications range from preventing catheter blockages to intravenous drug administration. End-users primarily include hospitals, clinics, ambulatory surgical centers, and home healthcare settings. Understanding the dynamics within each segment is essential for market participants to tailor their strategies and capitalize on the evolving demands of the healthcare industry.

The IV flush syringe market is segmented into saline, heparin, and other types. Among these, saline flush syringes dominate the market due to their widespread use in maintaining the patency of intravenous lines and preventing blockages. They are particularly popular in healthcare settings where IV catheters are in constant use, such as hospitals and clinics. Saline syringes are preferred because they are simple, cost-effective, and pose fewer risks of complications compared to other alternatives.

Heparin syringes are the fastest-growing segment in this market. Heparin, an anticoagulant, is used for more specialized medical treatments, such as preventing blood clots in patients with a high risk of thrombosis. With increasing cases of cardiovascular diseases and patients requiring prolonged intravenous therapy, the demand for heparin flush syringes is expected to grow. These syringes ensure the proper functioning of IV lines in patients with specific medical needs, making them indispensable in critical care environments.

Other types, such as those used in pediatric and neonatal care, are smaller segments but continue to see growth, driven by the rising demand for specialized healthcare products tailored to vulnerable patient populations.

In terms of application, the two primary categories are catheter blockage prevention and intravenous drug administration. Among these, catheter blockage prevention is the leading application, as IV flush syringes are widely used to clear and maintain the patency of IV catheters, ensuring that they function optimally and prevent complications like thrombus formation. The need for maintaining an open IV line is critical in hospitals, surgical centers, and other healthcare facilities, making catheter blockage prevention a key driver for the market.

Intravenous drug administration is another key application, particularly for patients who require regular IV infusions of medications or fluids. This application segment is also growing as healthcare providers increasingly adopt standardized IV flush protocols to reduce the risk of complications during IV treatments. With a growing focus on improving patient safety and treatment outcomes, IV flush syringes are becoming integral to the process of drug delivery and fluid management.

As hospitals and clinics continue to prioritize patient safety and efficiency in IV procedures, the demand for IV flush syringes in both of these applications will remain strong, with catheter blockage prevention being the dominant driver.

The primary end-users of IV flush syringes are hospitals, ambulatory surgical centers, clinics, and home healthcare settings. Hospitals are the largest end-user segment, accounting for the highest demand for IV flush syringes due to the high number of inpatient admissions, surgeries, and emergency procedures. Hospitals also make use of a wide range of IV catheter devices, which require regular flushing to maintain their functionality.

Ambulatory surgical centers (ASCs) are the fastest-growing end-user segment, primarily driven by the increasing number of outpatient surgeries and minimally invasive procedures. As these centers offer a wide array of treatments, the need for IV flush syringes is growing, particularly in cases where short-term intravenous access is required.

Clinics also represent a significant portion of the market, particularly for chronic care and dialysis patients who require regular IV flush procedures. As the demand for clinic-based treatments rises, so does the need for IV flush syringes in these settings.

Finally, home healthcare is an emerging and fast-growing segment, driven by the increasing trend of patients receiving IV treatments at home. As more patients manage chronic conditions at home, the demand for IV flush syringes in the home healthcare sector is expected to rise, making it a key area of focus for manufacturers in the coming years.

North America accounted for the largest market share at 45% in 2024; however, the Asia-Pacific region is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

The dominance of North America is driven by advanced healthcare infrastructure, an aging population, and high demand for medical devices. On the other hand, the Asia-Pacific region is set to experience rapid growth due to increased healthcare spending, particularly in countries like China and India, and a rising population of chronic disease patients.

North America holds the largest market share for IV flush syringes, valued at USD 150 million in 2024. The United States is the primary driver in the region, with a well-established healthcare system and significant demand for medical devices, especially due to a high incidence of chronic diseases and the aging population. The focus on infection control, safety, and efficiency in healthcare procedures continues to fuel the demand for advanced IV flush syringes. The U.S. government’s efforts to improve healthcare standards and reduce healthcare-associated infections also contribute to the growth of this market.

Europe’s IV flush syringe market was valued at USD 85 million in 2024, with major contributors including the United Kingdom, Germany, and France. These countries lead due to their advanced healthcare systems and strong regulatory frameworks. The market is driven by increasing awareness about patient safety and the prevention of healthcare-associated infections. Furthermore, the growing trend of adopting disposable, prefilled, and single-use IV flush syringes in hospitals, clinics, and outpatient surgical centers is spurring demand across the region. The increasing focus on reducing healthcare costs without compromising patient care further supports market growth.

The Asia-Pacific region is witnessing rapid growth in the IV flush syringe market, valued at USD 50 million in 2024. This region is anticipated to experience the fastest growth due to healthcare improvements, expanding healthcare infrastructure, and rising investments in medical devices. China and India, with large populations and rising incidences of chronic diseases, are significant contributors to the market expansion. Furthermore, government initiatives aimed at improving healthcare access and quality are driving the demand for medical devices such as IV flush syringes. The increasing prevalence of conditions such as cardiovascular diseases and diabetes is also boosting market growth in this region.

South America, valued at USD 18 million in 2024, is showing steady growth in the IV flush syringe market, driven by healthcare improvements in Brazil and Argentina. The demand is fueled by the rising number of patients with chronic conditions like diabetes, cardiovascular diseases, and cancer. As hospitals and outpatient surgical centers continue to grow, there is an increasing need for IV flush syringes to manage intravenous treatments effectively. The South American market is also benefiting from greater government investment in healthcare infrastructure and technology, aiming to improve medical device accessibility and overall healthcare standards.

The Middle East & Africa (MEA) region holds a market value of USD 12 million in 2024, with steady growth expected over the coming years. Saudi Arabia, the UAE, and South Africa are the primary contributors to this market expansion, driven by increased healthcare investments, improving medical facilities, and a rise in medical tourism. As healthcare access improves, demand for medical devices such as IV flush syringes grows. Additionally, the rise in chronic diseases and government efforts to address health concerns are pushing the demand for advanced medical products across the MEA region.

United States – Market value: USD 150 million in 2024. The U.S. is the largest market for IV flush syringes due to its robust healthcare system, the prevalence of chronic diseases, and a strong focus on patient safety.

China – Market value: USD 75 million in 2024. China is seeing significant growth due to improving healthcare infrastructure, rising rates of chronic diseases, and increasing government healthcare spending.

The global IV flush syringe market is characterized by a competitive landscape with several key players vying for market share. Major companies such as BD (Becton, Dickinson and Company), B. Braun Melsungen AG, Cardinal Health, Medline Industries, LP, and Nipro Corporation dominate the market. These companies have established strong distribution networks, extensive product portfolios, and significant brand recognition, enabling them to maintain a competitive edge. Additionally, emerging players like Medefil, Inc., Polymedicure, and Aquabiliti are gaining traction by offering innovative products and targeting niche markets. The market is witnessing a trend towards consolidation, with leading players acquiring smaller companies to enhance their product offerings and expand their market presence. Strategic partnerships, mergers, and acquisitions are common strategies employed to strengthen market position and drive growth. Furthermore, companies are focusing on research and development to introduce new technologies and improve product quality, thereby meeting the evolving needs of healthcare providers and patients.

BD (Becton, Dickinson and Company)

B. Braun Melsungen AG

Cardinal Health

Medline Industries, LP

Nipro Corporation

Medefil, Inc.

Polymedicure

Aquabiliti

SteriCare Solutions

The IV flush syringe market is experiencing significant technological advancements aimed at enhancing patient safety, improving usability, and ensuring environmental sustainability. Manufacturers are increasingly incorporating safety features such as needleless connectors and tamper-evident caps to prevent needlestick injuries and contamination. Additionally, the development of prefilled syringes with precise dosages reduces the risk of medication errors and ensures consistent administration. The use of biocompatible materials, such as medical-grade plastics and glass, is prevalent to minimize adverse reactions and maintain the integrity of the flush solution. Furthermore, there is a growing emphasis on eco-friendly manufacturing processes and recyclable packaging to align with global sustainability goals. Automation in production lines is also being adopted to enhance efficiency and reduce human error. These technological innovations are driving the evolution of the IV flush syringe market, catering to the increasing demand for safer, more efficient, and environmentally conscious medical devices.

In June 2024, BD (Becton, Dickinson and Company) announced the launch of a new line of prefilled saline IV flush syringes designed with enhanced safety features, including tamper-evident caps and needleless connectors, to reduce the risk of contamination and needlestick injuries.

In August 2024, Medline Industries, LP expanded its manufacturing facility in the United States to increase production capacity for IV flush syringes, aiming to meet the growing demand in North America and improve supply chain efficiency.

In October 2024, B. Braun Melsungen AG introduced a new line of eco-friendly IV flush syringes made from recyclable materials, aligning with global sustainability initiatives and responding to increasing regulatory pressures for environmentally responsible products.

In December 2024, Nipro Corporation received regulatory approval for its new line of heparin IV flush syringes, which feature improved stability and longer shelf life, addressing concerns related to product recalls and enhancing patient safety.

The IV flush syringe market report provides a comprehensive analysis of the industry, encompassing various product types, end-users, and regional markets. It delves into the market dynamics, including drivers, restraints, opportunities, and threats, offering insights into the factors influencing market growth. The report also examines the competitive landscape, profiling key players and their strategies to maintain market leadership. Technological advancements and innovations in product design and manufacturing processes are highlighted, showcasing the industry's efforts to enhance safety, efficiency, and sustainability. Furthermore, the report assesses regulatory frameworks and guidelines impacting the market, providing a clear understanding of compliance requirements. Market forecasts and trends are presented, offering stakeholders valuable information to make informed decisions. Overall, the report serves as a vital resource for industry participants, investors, and policymakers seeking to navigate the evolving IV flush syringe market.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global IV Flush Syringe Market |

| Market Revenue (2024) | USD 341.5 Million |

| Market Revenue (2032) | USD 532.1 Million |

| CAGR (2025–2032) | 5.7% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type:

By Application:

By End-User:

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape, Technological Advancements, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | BD (Becton, Dickinson and Company), B. Braun Melsungen AG, Cardinal Health, Medline Industries, LP, Nipro Corporation, Medefil, Inc., Polymedicure, Aquabiliti, SteriCare Solutions |

| Customization & Pricing | Available on Request (10% Customization is Free) |