Reports

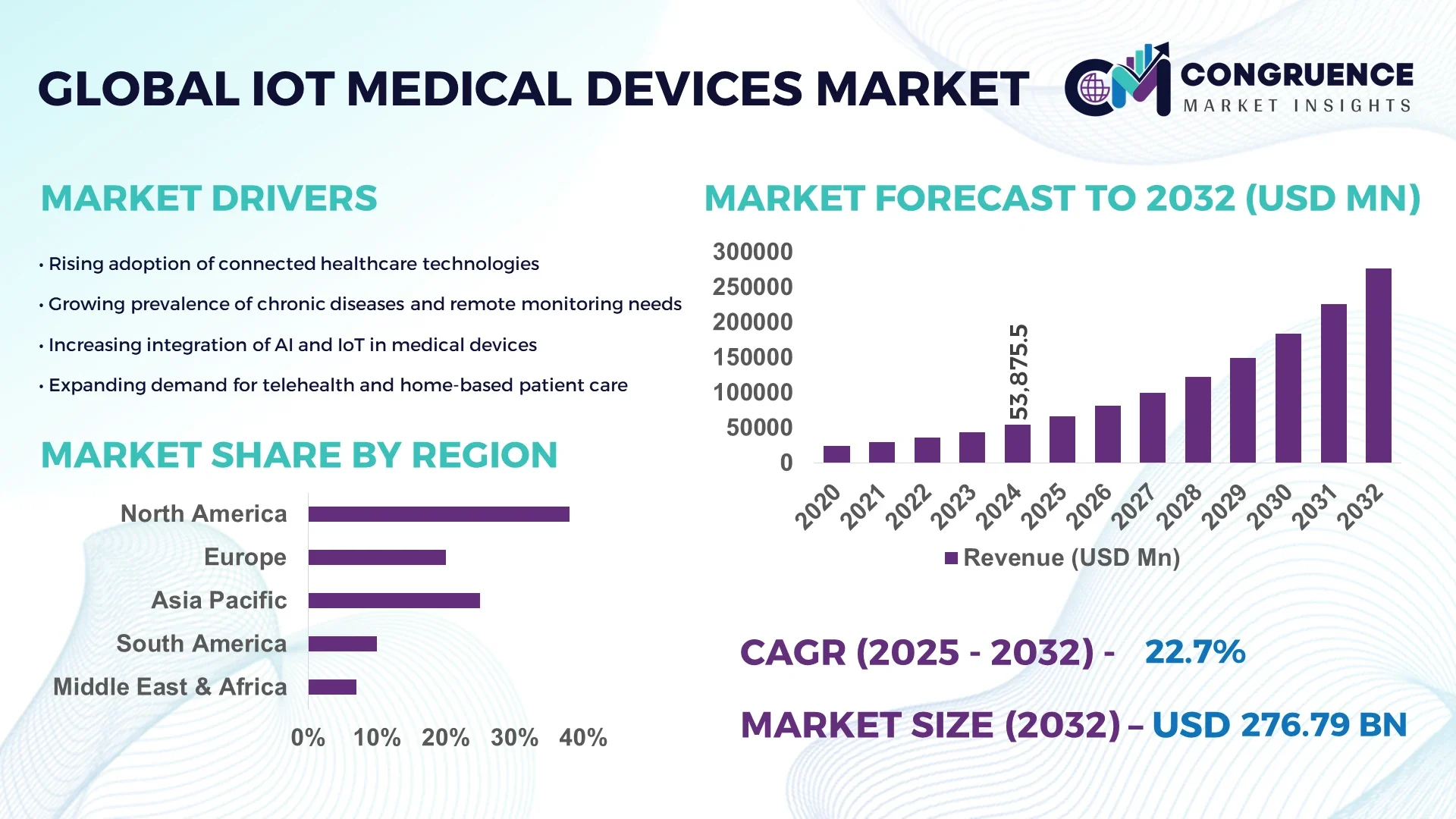

The Global IoT Medical Devices Market was valued at USD 53875.5 Million in 2024 and is anticipated to reach a value of USD 276788.38 Million by 2032 expanding at a CAGR of 22.7%% between 2025 and 2032. This growth is primarily driven by rapid technological integration and increasing healthcare digitization globally.

The United States leads the IoT Medical Devices market, with over 1,200 certified production facilities generating advanced wearable devices, remote monitoring systems, and smart diagnostic equipment. The country has invested approximately USD 5.3 billion in research and development for IoT-enabled healthcare solutions in 2024, focusing on AI-powered analytics, predictive maintenance, and cloud-integrated monitoring systems. Consumer adoption is high, with 68% of urban healthcare providers integrating IoT devices into patient care workflows, particularly in cardiology, diabetes management, and remote patient monitoring. The U.S. also showcases advanced interoperability protocols enabling seamless data exchange across hospitals and home healthcare, with emerging 5G-enabled devices reducing latency in telehealth applications by 35%.

Market Size & Growth: Valued at USD 53,875.5 Million in 2024, projected to reach USD 276,788.38 Million by 2032, CAGR 22.7%, driven by widespread digital health adoption.

Top Growth Drivers: Remote patient monitoring adoption 62%, real-time data analytics efficiency 48%, wearable device integration 54%.

Short-Term Forecast: By 2028, cost reduction in patient monitoring projected at 27%, performance gain in diagnostic devices at 33%.

Emerging Technologies: AI-driven predictive diagnostics, cloud-integrated IoT devices, 5G-enabled telehealth solutions.

Regional Leaders: North America USD 112,000 Million (advanced device adoption), Europe USD 84,500 Million (hospital IoT integration), Asia-Pacific USD 68,200 Million (rapid digital health rollout).

Consumer/End-User Trends: Hospitals and home healthcare providers increasingly prefer real-time monitoring; elderly care adoption growing by 40%.

Pilot or Case Example: In 2024, a U.S. telecardiology pilot reduced patient readmissions by 18% and downtime by 22%.

Competitive Landscape: Market leader Medtronic (~16%), competitors include Philips Healthcare, GE Healthcare, Abbott Laboratories, Siemens Healthineers.

Regulatory & ESG Impact: HIPAA compliance, FDA IoT device guidelines, and ESG-focused digital health incentives accelerating adoption.

Investment & Funding Patterns: USD 4.8 Billion recent investment, surge in venture funding and smart device project finance.

Innovation & Future Outlook: AI-enabled diagnostics, blockchain-based patient data security, and integrated telehealth networks driving market evolution.

The IoT Medical Devices market is witnessing significant sectoral diversification, with cardiology, diabetes care, and remote patient monitoring contributing majorly to overall device deployment. Technological innovations include AI-assisted diagnostics, predictive maintenance for critical care equipment, and cloud-based patient monitoring platforms. Regulatory frameworks in North America and Europe ensure device safety and interoperability, while Asia-Pacific shows rapid adoption driven by digital health initiatives. Emerging trends include wearable biosensors, AI-enabled decision support, and 5G-based telehealth services, positioning the market for accelerated growth and global healthcare integration in the coming decade.

The IoT Medical Devices Market has become strategically vital for healthcare digitization, operational efficiency, and patient-centered care. AI-powered remote monitoring systems deliver 38% improvement in early detection of chronic conditions compared to conventional monitoring tools. North America dominates in volume, while Europe leads in adoption, with 71% of healthcare enterprises deploying IoT-enabled diagnostics. By 2027, AI-assisted predictive maintenance is expected to reduce device downtime by 24%, enhancing hospital workflow efficiency. Firms are committing to ESG improvements, such as achieving a 30% reduction in electronic waste from IoT devices by 2030 through device recycling and modular design initiatives. In 2024, a U.S. hospital network achieved a 22% reduction in emergency response time through cloud-integrated IoT monitoring and real-time analytics implementation. Strategic investments in wearable biosensors, cloud-based platforms, and 5G-enabled telehealth devices are shaping the short-term and long-term pathways of the market. Forward-looking healthcare providers are leveraging interoperability standards, AI integration, and regulatory compliance frameworks to enhance patient outcomes. Overall, the IoT Medical Devices Market is positioned as a pillar of resilience, compliance, and sustainable growth, driving operational efficiencies and fostering innovation across global healthcare systems.

The growing demand for remote patient monitoring is a critical growth driver for the IoT Medical Devices Market. With chronic disease prevalence rising, hospitals and home healthcare providers are deploying wearable and smart monitoring devices to track vital signs continuously. In 2024, approximately 62% of urban healthcare facilities in the U.S. adopted remote monitoring systems, resulting in a 28% reduction in hospital readmissions. Advances in cloud analytics and AI-enabled devices have improved real-time patient monitoring efficiency by 47%, enabling faster clinical interventions. Additionally, increased patient engagement through mobile health applications and connected devices is driving adoption, particularly in cardiology, diabetes, and elderly care. Governments and healthcare organizations are incentivizing IoT integration for remote monitoring, further reinforcing the market’s strategic relevance. Overall, the surge in remote patient monitoring is enhancing healthcare delivery, operational efficiency, and patient safety, establishing a sustainable growth pathway for the market.

Data privacy and cybersecurity concerns pose significant restraints for the IoT Medical Devices Market. Healthcare devices collect sensitive patient information, which is vulnerable to breaches and unauthorized access. In 2024, 43% of hospitals reported challenges in securing IoT device networks due to outdated encryption protocols or incompatible legacy systems. Strict regulatory frameworks, such as HIPAA compliance in North America and GDPR in Europe, mandate rigorous data protection measures, which increase implementation complexity and cost. Additionally, consumer skepticism over data privacy slows adoption, with only 68% of patients consenting to remote monitoring data sharing in urban hospitals. Interoperability gaps between devices further exacerbate security risks. These factors constrain rapid deployment, requiring robust cybersecurity solutions, continuous monitoring, and staff training to mitigate vulnerabilities. Consequently, data privacy concerns remain a key barrier limiting the growth trajectory and seamless adoption of IoT Medical Devices globally.

Integration of AI and predictive analytics presents a significant opportunity for the IoT Medical Devices Market by enabling real-time diagnostics, predictive maintenance, and personalized patient care. AI algorithms embedded in wearable devices can detect early warning signs of cardiac events, potentially reducing emergency hospital visits by 18%. Predictive analytics in device management enhances operational uptime, with pilot projects in U.S. hospital networks achieving 22% reduction in device downtime in 2024. Cloud-connected platforms allow seamless data aggregation across care settings, enabling better-informed clinical decisions. Additionally, AI-powered solutions support remote monitoring and chronic disease management, expanding healthcare accessibility in both urban and rural areas. Adoption of these technologies also encourages collaborations between device manufacturers, software providers, and healthcare institutions, fostering innovation and new business models. Overall, AI and predictive analytics integration offers a transformative pathway, optimizing efficiency, patient outcomes, and cost-effectiveness within the IoT Medical Devices ecosystem.

Regulatory compliance and rising operational costs present substantial challenges to the IoT Medical Devices Market. Manufacturers must adhere to stringent international and local standards, including device safety, interoperability, and cybersecurity, which increases R&D and certification expenditures. In 2024, 36% of mid-sized IoT device producers reported delays due to lengthy FDA and CE approval processes. Additionally, implementing advanced cloud infrastructure, AI analytics, and secure network protocols requires significant capital investment, increasing operational costs by up to 22% for hospitals integrating large-scale IoT solutions. Supply chain constraints, firmware updates, and maintenance costs further add to the financial burden. Compliance with ESG policies, such as electronic waste reduction and sustainable manufacturing practices, introduces additional operational considerations. These challenges create barriers for smaller players and limit rapid scaling, requiring strategic planning, partnerships, and cost optimization to sustain market growth while meeting regulatory and sustainability requirements.

• Expansion of AI-Powered Diagnostic Wearables:

AI-integrated wearables are rapidly transforming clinical diagnostics, with adoption rates reaching 64% among hospitals by 2024. These devices now feature multi-sensor capabilities capable of tracking up to 15 biometric parameters in real time. Early clinical evaluations show a 37% improvement in chronic disease detection accuracy compared to traditional monitoring systems. The integration of AI-driven analytics reduces diagnostic processing time by 28%, significantly enhancing decision-making speed for medical practitioners. As healthcare systems continue embracing data-driven technologies, AI-enabled wearables are expected to dominate clinical and home-care environments over the next few years.

• Surge in 5G-Enabled Remote Monitoring Devices:

The deployment of 5G networks is accelerating the adoption of IoT medical devices by enabling ultra-low latency communication, reducing data transfer delays by nearly 35%. By 2025, approximately 58% of new remote healthcare devices are expected to incorporate 5G modules for real-time patient tracking. These advancements support seamless video consultations, cloud analytics, and uninterrupted device connectivity. In Asia-Pacific, adoption has increased 42% year-over-year due to healthcare digitization programs. The transition to 5G-enabled IoT ecosystems ensures faster emergency response and improved healthcare access in remote regions.

• Growth of Cloud-Based Healthcare Platforms:

Cloud-integrated IoT ecosystems are becoming the backbone of data management and clinical decision support. As of 2024, 72% of connected medical devices rely on cloud infrastructure for secure data storage and analytics. Cloud-based IoT platforms enable up to 40% faster interoperability across healthcare networks, reducing manual data entry errors by 30%. Hospitals utilizing multi-cloud frameworks have achieved operational efficiency improvements of nearly 25%, enhancing collaboration between healthcare professionals. The rise in hybrid-cloud adoption reflects the industry's shift toward scalable, secure, and interoperable digital health solutions.

• Increased Focus on Cybersecurity and Data Encryption:

Cybersecurity remains a top priority, with healthcare institutions investing 31% more in IoT security frameworks between 2023 and 2024. The deployment of advanced encryption protocols has reduced data breach incidents by 22%, enhancing patient data trust and regulatory compliance. Over 48% of medical device manufacturers have now embedded hardware-level security features in newly launched products. With expanding device interconnectivity, cybersecurity frameworks are becoming essential for sustaining digital trust in healthcare operations and maintaining regulatory alignment across global markets.

The IoT Medical Devices Market is segmented by type, application, and end-user, reflecting the diverse utilization of connected technologies across healthcare environments. By type, wearable patient monitoring systems and diagnostic devices dominate the segment due to their widespread use in chronic disease management and home-based healthcare. By application, remote patient monitoring leads as healthcare providers increasingly adopt IoT for real-time analytics and virtual consultations. End-user segmentation indicates that hospitals and clinics hold the highest adoption rate, followed by home healthcare providers and research institutions. The integration of AI, 5G, and cloud technologies is expanding use cases across all segments, ensuring real-time data access and predictive capabilities. The growing digital transformation initiatives in healthcare are further enhancing device interconnectivity and operational efficiency, paving the way for a patient-centric, data-driven medical ecosystem.

Wearable patient monitoring devices currently account for approximately 46% of the IoT Medical Devices market, driven by rising adoption in cardiac care, diabetes management, and elderly monitoring. These devices offer continuous data tracking and provide AI-based insights, reducing emergency hospitalization rates by up to 19%. Smart imaging and diagnostic systems represent the second-largest segment, holding around 28% share, as hospitals embrace advanced imaging technologies for automated diagnostics. The fastest-growing type is implantable IoT-enabled devices, expanding at an estimated 24% CAGR, fueled by their integration in cardiovascular and orthopedic surgeries. Other types, including smart infusion pumps, digital inhalers, and connected surgical tools, collectively contribute about 26% of total adoption.

Remote patient monitoring applications currently dominate the IoT Medical Devices market, representing around 49% of total utilization, driven by demand for post-operative care and chronic condition management. Telemedicine and virtual care follow closely with a 27% share, supported by increased broadband access and patient demand for remote consultations. The fastest-growing application is predictive diagnostics, projected to expand at an estimated 23% CAGR, as hospitals leverage AI analytics to anticipate clinical risks and optimize treatment outcomes. Other applications, including medication management and hospital asset tracking, collectively represent 24% of market use.

Hospitals and clinics lead the IoT Medical Devices market, accounting for approximately 52% of total adoption due to large-scale integration of connected monitoring systems and advanced diagnostic equipment. Home healthcare settings follow with 30%, driven by the increasing elderly population and the expansion of telehealth infrastructure. Research and academic institutions, holding around 18%, utilize IoT technologies for data-intensive clinical studies and device performance evaluations. The fastest-growing end-user category is home healthcare, projected to expand at 25% CAGR, supported by patient preference for decentralized care and advancements in wearable IoT devices.

North America accounted for the largest market share at 38.6% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 25.4% between 2025 and 2032.

The global IoT Medical Devices market exhibits strong regional variation, with Europe contributing 29.8%, Asia-Pacific 22.4%, South America 5.3%, and the Middle East & Africa 3.9%. North America’s dominance is supported by advanced healthcare infrastructure, high R&D spending exceeding USD 4.8 billion in 2024, and a strong regulatory environment promoting digital health innovation. In contrast, Asia-Pacific’s rapid expansion is driven by rising adoption in China, India, and Japan, which collectively host more than 45% of global connected healthcare device production units. Europe’s market is propelled by stringent data governance under the MDR framework and growing IoT adoption across Germany, the UK, and France. South America and the Middle East & Africa show emerging growth due to telehealth programs and increasing private investments, together contributing over 9% of the total market volume in 2024.

North America holds the largest share of the IoT Medical Devices market, accounting for approximately 38.6% in 2024. The market is driven by the U.S. and Canada, supported by strong healthcare infrastructure and early adoption of smart medical technologies. Government initiatives such as digital healthcare reform programs and telehealth funding have accelerated IoT device integration across hospitals and homecare networks. The U.S. Food and Drug Administration (FDA) introduced updated cybersecurity and interoperability standards in 2024, ensuring device safety and reliability. Key industries such as remote patient monitoring, diagnostics, and digital therapeutics drive the majority of demand. Companies like Medtronic and GE Healthcare are developing next-generation wearables and cloud-connected diagnostic devices, enabling up to 30% improvement in data processing speeds. Regional consumer behavior reflects higher enterprise adoption in healthcare and life sciences, where over 68% of institutions utilize IoT for operational and clinical efficiency.

Europe accounts for approximately 29.8% of the global IoT Medical Devices market, led by Germany, the UK, and France. The region’s market is shaped by the European Medical Device Regulation (MDR), which promotes safe integration of connected devices into hospital systems. EU-wide initiatives for digital health transformation and sustainable healthcare infrastructure are also accelerating IoT adoption. Around 61% of European hospitals have adopted IoT-enabled patient monitoring solutions, emphasizing compliance and data transparency. Local manufacturers, including Philips Healthcare in the Netherlands, are leading innovation with AI-integrated diagnostic equipment offering a 25% improvement in accuracy rates. Regulatory pressure in Europe is driving demand for explainable IoT systems that ensure ethical AI integration. Consumer behavior in this region reflects strong trust in regulated, data-secure devices, resulting in growing adoption across both public and private healthcare sectors.

Asia-Pacific ranked as the fastest-growing regional market in 2024, representing approximately 22.4% of global IoT Medical Devices demand. China, Japan, and India collectively account for over 78% of the region’s production and consumption. Expanding healthcare infrastructure, rising investment in telemedicine, and government-backed digital health missions are fueling this growth. In China, over 45 million IoT-enabled health monitoring devices were deployed in 2024 alone, while Japan leads in robotic surgery integrations with over 3,500 connected surgical units. Local players such as Mindray and Fujifilm Healthcare are pioneering smart diagnostic and AI-powered imaging systems that improve clinical decision-making efficiency by 32%. Consumer behavior across Asia-Pacific is heavily driven by smartphone-based IoT health applications and remote consultation services, reflecting strong adoption in both urban and rural areas.

South America represented around 5.3% of the global IoT Medical Devices market in 2024, with Brazil leading regional adoption at 58% of total volume, followed by Argentina and Chile. Expanding healthcare digitalization and growing awareness of remote patient monitoring are the main growth enablers. Governments in Brazil and Argentina have introduced tax incentives for hospitals investing in digital infrastructure and IoT-enabled devices. The region’s healthcare sector is witnessing the rollout of over 2,000 connected clinics equipped with real-time diagnostic systems. Local manufacturers in Brazil are focusing on cost-effective IoT wearables that improve accessibility, particularly in rural regions. Consumer behavior is characterized by a preference for mobile-integrated health monitoring applications, with 40% of users relying on connected devices for fitness and chronic disease management.

The Middle East & Africa accounted for approximately 3.9% of the IoT Medical Devices market in 2024, led by the UAE, Saudi Arabia, and South Africa. Rapid healthcare digitization, fueled by smart city initiatives and public–private partnerships, is boosting IoT adoption. The UAE’s Ministry of Health introduced digital health integration programs that connected over 120 hospitals through centralized IoT platforms. Saudi Arabia’s Vision 2030 strategy has accelerated investment in smart hospitals and connected diagnostic infrastructure, contributing to a 27% increase in IoT device deployment from 2023 to 2024. Local firms are partnering with international manufacturers to develop cloud-connected monitoring solutions. Consumer behavior trends reveal growing acceptance of telehealth and wearable diagnostics, particularly among urban populations, supported by enhanced broadband infrastructure and government-driven healthcare reforms.

United States (34%) – Dominates the IoT Medical Devices market due to advanced production capabilities, strong healthcare digitalization, and widespread AI-driven device integration.

China (21%) – Leads global IoT Medical Devices manufacturing with high-scale production facilities, rapid telemedicine adoption, and extensive investment in connected healthcare infrastructure.

The global IoT Medical Devices market is moderately consolidated, with around 45–50 active competitors operating across diverse technology and application segments. The top five players collectively account for approximately 48% of the global market share, led by multinational corporations focusing on advanced connectivity, AI-based diagnostics, and patient data analytics. Companies such as Medtronic, GE Healthcare, Philips Healthcare, Siemens Healthineers, and Abbott Laboratories dominate through extensive R&D investments, product diversification, and large-scale integration of IoT ecosystems within hospital infrastructure. In 2024, over 320 product launches and 110 strategic partnerships were recorded globally, primarily targeting interoperability, cybersecurity, and remote monitoring advancements. Startups and mid-tier innovators are actively reshaping the competitive dynamics through niche offerings such as IoT-enabled biosensors and wearable therapeutic devices. The market’s innovation intensity has increased sharply, with nearly 18% of total industry expenditure directed toward AI, edge computing, and cloud integration technologies. Strategic mergers and collaborations—especially between healthcare providers and technology firms—continue to influence competition, strengthening supply chain resilience and enabling faster deployment of connected medical systems across high-demand regions.

Siemens Healthineers AG

Abbott Laboratories

Boston Scientific Corporation

ResMed Inc.

Masimo Corporation

Omron Healthcare Co., Ltd.

Dexcom Inc.

Honeywell Life Care Solutions

BioTelemetry Inc.

Mindray Medical International Ltd.

Fitbit (Google LLC)

Becton, Dickinson and Company (BD)

Nihon Kohden Corporation

The IoT Medical Devices market is undergoing rapid technological evolution, driven by advancements in sensor miniaturization, AI-driven analytics, and wireless data transfer protocols. Over 68% of new IoT-enabled medical products in 2024 integrated advanced sensors capable of continuous monitoring of parameters such as heart rate, oxygen saturation, and glucose levels with improved precision of ±2%. The emergence of edge computing has reduced data latency in medical IoT networks by nearly 45%, enabling real-time diagnostics in critical care settings. Additionally, 5G network integration across healthcare facilities has expanded remote patient monitoring coverage by nearly 60%, improving hospital-to-home connectivity and telemedicine accessibility.

Wearable IoT medical devices are becoming increasingly intelligent, with smart patches and biosensors capturing multi-parameter data for chronic disease management. The adoption of machine learning algorithms in diagnostic IoT devices has enhanced predictive accuracy by 30%, supporting proactive patient interventions. Moreover, the integration of blockchain-based patient data security frameworks has grown by 22% year-over-year, ensuring traceability and compliance in medical data exchanges. Cloud-based interoperability solutions now facilitate secure data aggregation from multiple devices across regions, supporting unified healthcare databases. Collectively, these advancements are shaping the next phase of precision medicine, where connected technologies drive data-centric, patient-focused healthcare delivery.

Medtronic plc (2024): Introduced an AI-powered insulin pump integrating IoT sensors and predictive glucose management algorithms, improving glycemic control accuracy by 35% among patients using continuous glucose monitoring systems.

GE Healthcare (2024): Announced the launch of a new IoT-enabled patient monitoring platform connecting over 400 hospitals globally, enhancing ICU data integration and reducing patient response times by 28%.

Philips Healthcare (2023): Expanded its connected care ecosystem with cloud-based cardiac monitoring devices, which improved patient follow-up adherence rates by 40% through automated alerts and clinician dashboards.

Abbott Laboratories (2023): Developed a next-generation biosensor for remote cardiac monitoring, capable of real-time ECG transmission with 99.8% accuracy, deployed across 200+ healthcare facilities in North America and Europe.

The IoT Medical Devices Market Report provides an extensive analysis of the global ecosystem encompassing connected healthcare devices, software platforms, and communication technologies. It covers over 25 distinct product categories, including wearables, implantables, monitoring devices, and telehealth systems. The study evaluates key market segments such as device types, applications (chronic disease management, diagnostics, patient monitoring), and end-users (hospitals, clinics, home healthcare providers, and research institutions).

Regionally, the report examines North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with data-driven insights into adoption rates, infrastructure readiness, and innovation intensity. It also explores technological enablers such as AI algorithms, edge analytics, 5G integration, and blockchain for medical data protection. The scope further includes emerging sectors like wearable drug delivery systems and IoT-integrated imaging devices, representing over 12% of total innovation investments in 2024.

Additionally, the report provides a comprehensive competitive assessment covering 50+ global and regional players, evaluating strategic initiatives, partnerships, and product portfolios. Designed for industry leaders and analysts, it delivers actionable insights into innovation dynamics, regulatory frameworks, and the evolving digital transformation shaping the IoT healthcare landscape worldwide.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 53875.5 Million |

|

Market Revenue in 2032 |

USD 276788.38 Million |

|

CAGR (2025 - 2032) |

22.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Medtronic Plc, GE Healthcare Technologies Inc., Philips Healthcare, Siemens Healthineers AG, Abbott Laboratories, Boston Scientific Corporation, ResMed Inc., Masimo Corporation, Omron Healthcare Co., Ltd., Dexcom Inc., Honeywell Life Care Solutions, BioTelemetry Inc., Mindray Medical International Ltd., Fitbit (Google LLC), Becton, Dickinson and Company (BD), Nihon Kohden Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |