Reports

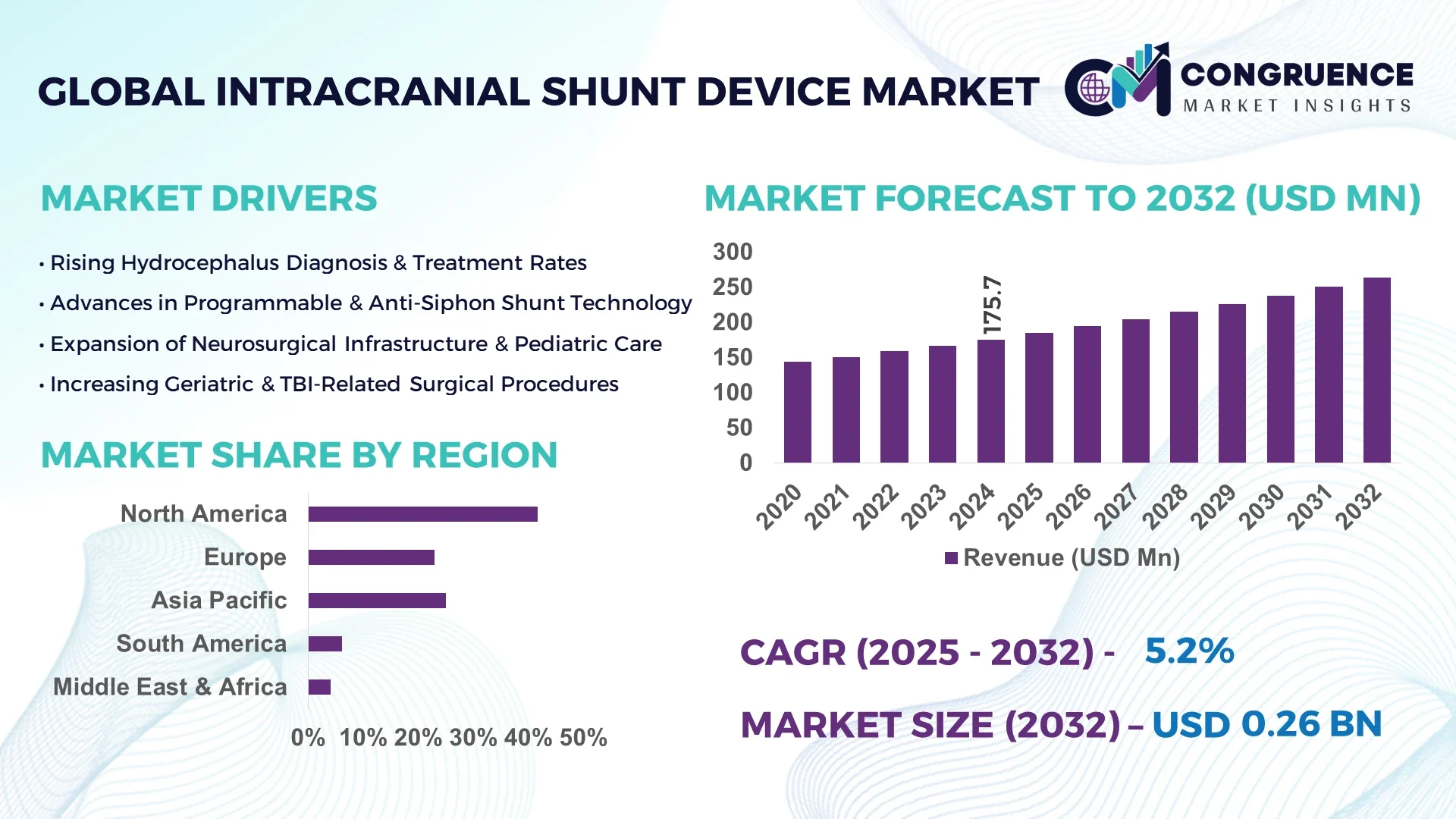

The Global Intracranial Shunt Device Market was valued at USD 175.68 Million in 2024 and is anticipated to reach a value of USD 263.547 Million by 2032 expanding at a CAGR of 5.2% between 2025 and 2032.

The United States leads global production of intracranial shunt devices, supported by extensive investment in neurosurgical research, robust manufacturing infrastructure, and early adoption of technologically advanced shunt systems across tertiary healthcare institutions.

The intracranial shunt device market is gaining momentum due to the increasing prevalence of hydrocephalus and other neurological conditions that necessitate cerebrospinal fluid (CSF) diversion. Key sectors contributing to the growth include pediatric neurosurgery, adult neurology, and trauma care units, with each segment showing rising demand for adjustable and programmable valve systems. Advancements such as anti-siphon mechanisms, antibiotic-impregnated catheters, and MRI-compatible materials are improving clinical outcomes and reducing post-surgical complications. Regulatory policies favoring Class III medical devices in developed regions are expediting product approvals, particularly in Europe and North America. Economically, the expansion of healthcare insurance and increasing government expenditure on neurological care in Asia-Pacific is fostering market development. Regionally, emerging economies are witnessing a surge in neurosurgical procedure volumes due to better diagnostic imaging and specialist availability. The future outlook is positive, with innovations in smart shunt systems and biofeedback-integrated monitoring likely to reshape the long-term market landscape.

Artificial Intelligence is significantly reshaping the Intracranial Shunt Device Market by enabling intelligent diagnostics, predictive analytics, and real-time surgical support. AI-driven imaging platforms are now being integrated into preoperative assessments to improve the detection of CSF abnormalities and streamline treatment planning. These platforms facilitate precision in catheter placement, reducing complications and improving surgical efficiency. Additionally, AI is transforming post-operative monitoring by enhancing shunt function surveillance through smart telemetry systems that track intracranial pressure fluctuations and transmit real-time alerts to clinicians.

Another critical development includes AI-based simulations that aid in designing more efficient valve mechanisms, improving fluid drainage control tailored to patient-specific physiological profiles. The use of machine learning algorithms in hospital data systems has also allowed for risk stratification and outcome prediction in patients undergoing shunt implantation. Moreover, robotic-assisted systems powered by AI are supporting neurosurgeons with greater accuracy in shunt placement, especially in complex anatomical scenarios. These systems are further integrated with electronic health records (EHRs), enabling seamless data exchange and post-surgical analytics. As hospitals prioritize operational performance and patient safety, the role of AI in automating device calibration, identifying early signs of shunt malfunction, and reducing readmission rates is proving invaluable. The AI-driven evolution within the Intracranial Shunt Device Market is not only enhancing procedural outcomes but also streamlining the entire treatment continuum for neurosurgical teams globally.

“In 2024, a U.S.-based medtech firm deployed an AI-powered remote monitoring system for intracranial shunt devices that reduced device malfunction response time by 42% across pilot hospital sites, enhancing patient safety and minimizing emergency interventions.”

The Intracranial Shunt Device Market is undergoing rapid transformation, driven by rising incidences of hydrocephalus, improvements in neurosurgical technologies, and growing healthcare awareness across both developed and developing nations. The increasing utilization of programmable shunt systems, which allow non-invasive pressure adjustments, is accelerating product adoption, especially in pediatric and geriatric patients. Additionally, evolving regulatory frameworks are streamlining device approvals, especially in Europe and North America, encouraging innovation and expanding the competitive landscape. Meanwhile, a shift toward minimally invasive neurosurgical procedures is increasing the demand for advanced shunt systems equipped with enhanced safety and feedback features. Industry consolidation, product portfolio diversification, and partnerships with AI and IoT developers are further shaping the competitive dynamics of the global intracranial shunt device ecosystem. Furthermore, expanding reimbursement coverage in emerging markets is strengthening the infrastructure for neuro-care, increasing market penetration for advanced shunting solutions.

A key driver for the growth of the Intracranial Shunt Device Market is the rising prevalence of hydrocephalus and other conditions requiring cerebrospinal fluid management. An estimated 1 in every 500 children is affected by hydrocephalus, creating continuous demand for effective long-term treatment solutions. The aging global population has also led to an increase in cases of normal pressure hydrocephalus (NPH), which is often misdiagnosed as Alzheimer's or Parkinson's disease. This demographic trend contributes significantly to the demand for shunt systems in elderly patients. Simultaneously, trauma-related brain injuries and post-surgical complications in neuro-oncology patients are driving the need for customizable and durable shunt systems. Healthcare providers are increasingly opting for programmable valve systems that reduce revision surgeries and improve patient outcomes, enhancing demand across hospital and specialized neuro-care centers.

Despite advancements in design and materials, the Intracranial Shunt Device Market continues to face significant restraints due to high rates of device malfunction and post-surgical complications. Shunt malfunction—often resulting from obstruction, infection, or disconnection—remains a leading cause for reoperation, with failure rates reported as high as 40% within the first year after implantation. This leads to increased healthcare costs, prolonged hospitalization, and heightened surgical risks, particularly in pediatric cases. Additionally, shunt infections can cause serious complications and are often difficult to detect early, thereby increasing the burden on both patients and providers. Concerns around these recurring issues have led to cautious adoption in some healthcare systems and continue to impact clinician confidence, especially in under-resourced medical settings.

One of the most promising opportunities in the Intracranial Shunt Device Market lies in the integration of smart technologies, including sensor-based telemetry and AI-powered remote monitoring systems. These innovations are enabling real-time tracking of intracranial pressure (ICP) and shunt performance, allowing early detection of malfunction and reducing the need for emergency revision surgeries. Telehealth-compatible shunt monitoring devices are emerging as critical tools, especially in remote or underserved areas where access to neurosurgical care is limited. Moreover, advancements in biocompatible materials and antimicrobial coatings are reducing infection rates and improving implant longevity. As healthcare systems globally prioritize predictive diagnostics and personalized treatment, the convergence of digital health platforms with intracranial shunt technology presents untapped potential for long-term growth and clinical efficiency.

A major challenge confronting the Intracranial Shunt Device Market is the lack of adequate neurosurgical infrastructure in low- and middle-income countries. Limited availability of trained neurosurgeons, inadequate diagnostic facilities, and low awareness of hydrocephalus symptoms contribute to delayed diagnosis and under-treatment. In many regions, especially in parts of Sub-Saharan Africa and Southeast Asia, public hospitals struggle to maintain consistent supplies of advanced medical devices, including programmable shunts. Furthermore, cost-sensitive markets are constrained by limited reimbursement mechanisms, forcing patients to opt for less sophisticated or reused devices, which increases complication rates. These systemic issues create barriers to market entry and expansion, particularly for manufacturers aiming to scale their advanced product lines into high-need, underserved populations.

• Surge in Adoption of Programmable Valves: Programmable shunt valves are gaining traction due to their non-invasive adjustability and reduced need for revision surgeries. In 2024, over 60% of new shunt implants in tertiary care hospitals across developed markets used programmable valve systems. Their ability to adapt CSF drainage pressure post-implantation allows for patient-specific treatment, significantly improving outcomes. Pediatric and geriatric neurosurgical units are particularly adopting these systems to minimize risk and avoid frequent surgical interventions.

• Integration of Telemetry and Sensor-Based Monitoring: Real-time intracranial pressure monitoring is transforming post-operative care. Modern shunt systems equipped with embedded pressure sensors and wireless telemetry recorded a 38% reduction in undetected malfunctions in comparative studies across major neuro-centers. These devices transmit alerts to clinicians, enhancing early intervention and patient safety. The integration of IoT platforms with shunt technology is a pivotal trend enhancing long-term monitoring and facilitating outpatient care models.

• Miniaturization of Shunt Components for Pediatric Use: The market is witnessing increased demand for miniaturized shunt systems tailored for infants and young children. Manufacturers are developing ultra-compact, flexible catheters that accommodate pediatric cranial structures. In 2024, new device launches focused on reducing component size while improving flow regulation precision. Hospitals are increasingly selecting these systems to reduce surgical complexity and improve compatibility with growing anatomical changes.

• Expansion in Emerging Healthcare Markets: Healthcare infrastructure development in regions like Southeast Asia, Latin America, and Eastern Europe is increasing access to neurosurgical interventions. In 2024, neurosurgical procedure volumes rose by 26% in Tier-2 cities of India and Brazil due to rising awareness and better insurance coverage. This growth is fueling demand for cost-effective yet advanced shunt systems, with companies launching economy-tier programmable valves that retain core features but remain affordable for public health institutions.

The Intracranial Shunt Device Market is segmented into types, applications, and end-users, each offering unique insights into the evolving market structure. By type, the market encompasses fixed/standard pressure valves, programmable valves, and anti-siphon devices, with programmable systems leading due to their clinical versatility. Applications span hydrocephalus, traumatic brain injury, and brain tumors, with hydrocephalus dominating overall usage volumes. In terms of end-users, hospitals account for the majority of procedures, supported by neurosurgical expertise and equipment, while ambulatory surgical centers are seeing increased adoption driven by shorter procedure times and lower costs. This segmentation structure enables stakeholders to assess demand patterns, identify target markets, and align their strategies with evolving clinical practices and technology demands.

Programmable valves lead the product type segment in the Intracranial Shunt Device Market due to their customizable pressure settings, reducing the need for revision surgeries. In 2024, they accounted for a majority of new installations across advanced healthcare centers. Their popularity is driven by the ability to adapt drainage parameters without requiring surgical access, particularly beneficial in pediatric and geriatric care settings. The fastest-growing segment is anti-siphon devices, which have seen increased integration into existing shunt systems to prevent over-drainage during posture changes. These are being widely adopted in regions with high incidences of shunt complications. Fixed or standard pressure valves still retain relevance in cost-sensitive and resource-constrained markets due to their affordability and simplicity. Manufacturers are also offering hybrid models combining standard pressure valves with anti-siphon features, serving niche requirements in developing markets. Innovation within the type segment is centered on minimizing complications and improving patient-tailored treatment pathways.

Hydrocephalus remains the leading application within the Intracranial Shunt Device Market, with the majority of implants globally conducted to treat congenital and acquired forms of the condition. Its dominance is supported by the steady volume of procedures across pediatric and elderly populations. The fastest-growing application is traumatic brain injury (TBI), particularly in countries with rising road accident rates and an aging demographic susceptible to falls. In 2024, TBI-related shunt installations grew significantly in regions such as Southeast Asia and Central Europe. Brain tumors represent another important application segment, especially in post-tumor resection cases where CSF flow is compromised. There is also growing attention on normal pressure hydrocephalus (NPH), often misdiagnosed but increasingly being recognized due to advanced imaging and diagnostic protocols. Each application area presents unique clinical demands, which are pushing manufacturers to develop specialized and highly adaptable device solutions.

Hospitals are the dominant end-user in the Intracranial Shunt Device Market, accounting for the largest share of implant procedures globally. Their leadership stems from access to neurosurgical specialists, advanced imaging equipment, and comprehensive postoperative care facilities. The fastest-growing end-user segment is ambulatory surgical centers (ASCs), particularly in urban regions of the U.S., Japan, and Germany, where demand for efficient, cost-effective neurosurgical interventions is rising. ASCs are benefiting from advancements in minimally invasive procedures and shorter recovery timelines, making them an attractive choice for select patient demographics. Specialty clinics are also gaining relevance, especially in pediatric-focused practices that manage long-term shunt therapy and routine valve adjustments. Additionally, academic and research institutions are contributing to the market by participating in clinical trials and product evaluations, which often shape purchasing decisions in public healthcare systems. These diversified end-user dynamics offer opportunities for tailored product development and targeted marketing strategies.

North America accounted for the largest market share at 41.7% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2025 and 2032.

The North American dominance is driven by advanced neurosurgical infrastructure, a high volume of hydrocephalus cases, and significant adoption of programmable and sensor-enabled shunt systems. Meanwhile, the Asia-Pacific region is undergoing rapid healthcare modernization, increased access to diagnostic imaging, and government-backed investment in pediatric and geriatric neurology services. Rising demand from developing countries such as China and India is accelerating the installation of cost-efficient, technologically advanced intracranial shunt devices. Globally, the demand is also fueled by increased awareness about normal pressure hydrocephalus in aging populations and a consistent rise in road accident-induced traumatic brain injuries. In addition, product innovations—such as antimicrobial shunt coatings and AI-powered pressure monitoring systems—are contributing to rapid clinical adoption in both high-income and emerging markets. These regional trends underscore a shifting landscape in the Intracranial Shunt Device Market, with opportunities for expansion and diversification becoming increasingly evident.

Expanding Neurosurgical Adoption Driven by Digital Shunt Monitoring Systems

North America held approximately 41.7% of the global intracranial shunt device market in 2024, underpinned by robust neurosurgical activity across urban hospitals and academic medical centers. Demand is largely driven by the U.S. healthcare sector, where programmable valves and smart shunt systems dominate new installations. The region’s high prevalence of congenital hydrocephalus, coupled with early diagnosis and well-equipped NICUs, supports the continuous adoption of advanced devices. Regulatory support through streamlined Class III medical device pathways has enabled quicker product rollouts, particularly for AI-enhanced and telemetry-integrated shunt systems. Government initiatives like increased funding for pediatric neurology and neurotrauma care have further strengthened this growth. Technological trends such as wireless intracranial pressure sensors and EHR-integrated monitoring platforms are improving clinical workflows and patient outcomes, solidifying North America’s position as a key hub for innovation and procedural volume in the Intracranial Shunt Device Market.

Modernized Valve Technologies Elevating Neurological Patient Outcomes

Europe commanded 29.4% of the global market share for intracranial shunt devices in 2024, led by countries like Germany, the UK, and France. These markets are characterized by sophisticated healthcare systems and a proactive regulatory framework. The European Medicines Agency (EMA) and respective national health authorities continue to support the approval of innovative neurosurgical devices, promoting market competitiveness and safety. Additionally, the region’s focus on sustainable healthcare has spurred the development of bio-compatible and MRI-safe materials in shunt components. Technological upgrades such as adjustable flow-control valves and digitally monitored shunt systems are being rapidly adopted in both adult and pediatric neurosurgical departments. Germany, in particular, has become a leading adopter of smart shunt devices due to its extensive neurology infrastructure and aging population. The transition toward value-based healthcare is also encouraging hospitals across Europe to invest in high-reliability, long-life shunt solutions.

Growing Surgical Volumes Boosting Regional Medical Device Innovation

Asia-Pacific ranks as the fastest-growing region in the Intracranial Shunt Device Market and held 18.6% of the global market volume in 2024. China, India, and Japan are the primary contributors to this growth, supported by a surge in hydrocephalus diagnosis rates and expanding access to neurosurgical services. China’s government-driven healthcare reforms and large-scale hospital expansions have catalyzed demand for programmable shunt systems. India has seen a sharp increase in pediatric neurosurgery cases due to improved awareness and screening programs, while Japan remains at the forefront of adopting miniaturized and MRI-compatible shunt technologies. Local manufacturers are investing in R&D to produce cost-effective, high-performance devices for the regional market. Additionally, medical device parks and innovation hubs in South Korea and Singapore are actively fostering the development of AI-integrated shunt systems and pressure-sensing valves. Infrastructure upgrades, medical tourism, and partnerships with global firms are strengthening Asia-Pacific’s position as a critical growth engine in this market.

Shifting Clinical Practices Supported by Public Health Investment

In 2024, South America accounted for 6.3% of the global intracranial shunt device market, with Brazil and Argentina emerging as dominant players. Brazil leads in terms of neurosurgical procedures and device installations due to its expansive public health network and growing base of specialized neurological hospitals. Government initiatives aimed at improving pediatric healthcare are driving increased deployment of programmable shunt valves across urban centers. Argentina is seeing rising adoption of smart valve technologies and minimally invasive surgical techniques within its private healthcare institutions. While infrastructure disparities persist in rural areas, public-private partnerships are working to improve access to advanced medical devices. Regional manufacturing incentives and relaxed trade policies are also encouraging international players to expand operations and supply chains locally. These developments reflect a region in transition, adapting to technological innovations while addressing systemic challenges in healthcare delivery.

Modern Healthcare Investments Catalyzing Market Access and Innovation

The Middle East & Africa region accounted for 4.0% of the global intracranial shunt device market in 2024. Key contributors include the UAE, Saudi Arabia, and South Africa, where investments in specialty hospitals and neuro-care infrastructure are accelerating adoption. The UAE, in particular, has prioritized technological modernization in its national health strategy, leading to the integration of AI-based pressure monitoring and electronic calibration systems in top-tier hospitals. South Africa is investing in public neurosurgery capacity, improving patient access to hydrocephalus treatments across underserved populations. Medical device regulatory harmonization efforts across Gulf Cooperation Council (GCC) countries have simplified entry for international manufacturers. Additionally, partnerships with European and Asian firms are introducing locally optimized, cost-efficient solutions tailored for regional epidemiology. Despite uneven healthcare access across the continent, strategic health funding and capacity-building initiatives are gradually boosting the region’s footprint in the global Intracranial Shunt Device Market.

United States – 38.5% market share

High production capacity and rapid adoption of AI-integrated programmable shunt systems position the U.S. as a global leader in the intracranial shunt device market.

Germany – 15.2% market share

Strong end-user demand, advanced healthcare infrastructure, and a high volume of neurosurgical procedures drive Germany’s leadership in the intracranial shunt device market.

The Intracranial Shunt Device market is moderately consolidated, with approximately 25–30 active global and regional manufacturers competing across various product segments. Key players differentiate themselves through proprietary valve designs, AI-enabled telemetry integration, and durability of shunt components. Innovation remains the central competitive strategy, with companies launching programmable valves that offer non-invasive adjustability and smart pressure monitoring features. The increasing demand for miniaturized and pediatric-specific shunt systems has encouraged product development tailored to niche clinical needs.

Strategic collaborations between medical device firms and neurology-focused research institutes are accelerating product innovation cycles. Several companies have entered strategic partnerships with software developers and IoT firms to integrate AI-based monitoring into their product offerings. Additionally, market participants are leveraging regulatory clearances from FDA and CE marking to strengthen their positioning in North America and Europe. Mergers and acquisitions have also intensified, with companies acquiring smaller firms offering specialized valve or sensor technologies to expand their portfolios. Competitive pricing, durability enhancements, and post-surgical support offerings are also influencing purchasing decisions in cost-sensitive markets. The race to deliver highly reliable, patient-specific, and technologically integrated shunt systems continues to shape the evolving competitive landscape.

Medtronic plc

B. Braun Melsungen AG

Integra LifeSciences Corporation

Spiegelberg GmbH & Co. KG

Sophysa SA

Moller Medical GmbH

Natus Medical Incorporated

Christoph Miethke GmbH & Co. KG

Dispomedica GmbH

Anuncia Medical Inc.

Technological advancements in the Intracranial Shunt Device Market are reshaping clinical standards, focusing on precision, real-time monitoring, and enhanced biocompatibility. Programmable valve technology continues to dominate, allowing clinicians to adjust cerebrospinal fluid (CSF) drainage without surgical intervention. These systems are now integrated with magnetic control features and memory-resistant settings to prevent unintentional pressure changes during MRI scans.

The integration of sensor-based telemetry systems is one of the most transformative developments. These technologies enable continuous monitoring of intracranial pressure, transmitting data wirelessly to clinicians through mobile or desktop interfaces. In 2024, over 30% of newly deployed shunt systems in urban medical centers included some form of digital feedback mechanism. Innovations in sensor miniaturization have made it feasible to embed pressure sensors within the valve or catheter, offering real-time diagnostics and predictive malfunction alerts.

Materials science is also evolving rapidly. Antimicrobial and silver-ion coatings are now standard in high-end models to reduce infection risks post-surgery. Manufacturers are investing in shape-memory alloys and flexible polymers to improve device flexibility and lifespan, especially for pediatric use cases. Additionally, AI-assisted design and simulation tools are enabling the rapid development of customized shunt configurations based on patient-specific anatomical and physiological data, supporting precision medicine approaches.

• In February 2023, Medtronic launched the M-Flow programmable valve system in select European markets, offering precision-controlled CSF drainage with magnetic adjustability and integrated anti-siphon mechanisms for adult hydrocephalus patients.

• In July 2023, Sophysa introduced a next-generation digital pressure monitoring shunt system that wirelessly syncs with neurosurgical platforms, enabling real-time valve performance analytics and pressure trend visualization.

• In January 2024, Integra LifeSciences announced the expansion of its programmable shunt production facility in New Jersey, boosting output capacity by 35% to meet rising demand from North American pediatric hospitals.

• In May 2024, Christoph Miethke GmbH & Co. KG unveiled a sensor-integrated gravitational valve with built-in memory functionality, designed to minimize overdrainage in upright positions while retaining programmable flow settings.

The Intracranial Shunt Device Market Report provides a comprehensive examination of the global landscape, covering key product types, technological innovations, and evolving end-user dynamics. It encompasses programmable valves, fixed pressure valves, and anti-siphon devices, analyzing their clinical advantages, procedural volumes, and innovation trajectories. The report evaluates application areas such as hydrocephalus, traumatic brain injuries, brain tumors, and post-surgical CSF management, offering segmented insights that help stakeholders understand usage patterns across demographics and medical conditions.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed commentary on top-performing countries, regional demand shifts, healthcare infrastructure capacity, and investment trends. It also highlights emerging markets where neurosurgical accessibility is expanding through public-private collaborations.

On the technology front, the report explores advancements in telemetry systems, AI integration, smart valve configurations, and biomaterial innovation. It discusses how digital health, tele-neurosurgery, and real-time monitoring are becoming central to product differentiation. Moreover, the report covers competitive benchmarking, recent product launches, and strategic developments, offering critical data for manufacturers, investors, healthcare providers, and policy planners seeking strategic entry or expansion. It provides actionable intelligence across operational, regulatory, and innovation-driven vectors shaping this high-impact medical device market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 175.68 Million |

|

Market Revenue in 2032 |

USD 263.547 Million |

|

CAGR (2025 - 2032) |

5.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Medtronic plc, B. Braun Melsungen AG, Integra LifeSciences Corporation, Spiegelberg GmbH & Co. KG, Sophysa SA, Moller Medical GmbH, Natus Medical Incorporated, Christoph Miethke GmbH & Co. KG, Dispomedica GmbH, Anuncia Medical Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |