Reports

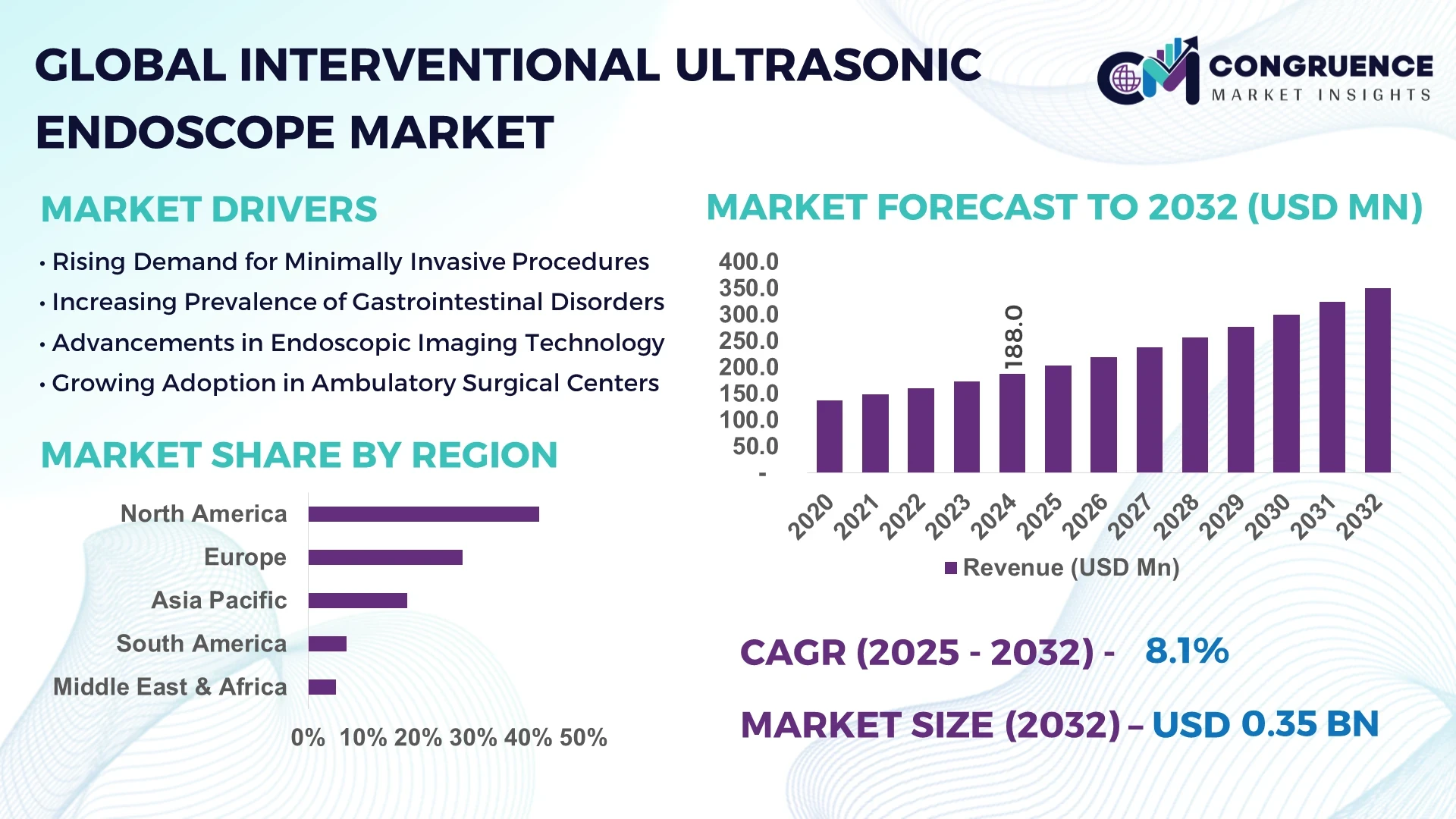

The Global Interventional Ultrasonic Endoscope Market was valued at USD 188.0 Million in 2024 and is anticipated to reach a value of USD 350.6 Million by 2032 expanding at a CAGR of 8.1% between 2025 and 2032. The growth is primarily driven by increasing adoption of minimally invasive procedures and rising investments in advanced diagnostic tools.

The United States dominates the Interventional Ultrasonic Endoscope Market, supported by advanced healthcare infrastructure and substantial R&D investments. Hospitals and surgical centers in the U.S. have integrated over 2,500 high-definition interventional ultrasonic endoscope units, with clinical trials exceeding 150 institutions in 2024. The country leads in technological advancements such as 4K imaging, AI-assisted visualization, and integrated probe systems, while focusing on cardiovascular, gastrointestinal, and urological procedures. The adoption rate among top-tier medical centers reaches 62%, indicating strong consumer confidence and early adoption trends in minimally invasive endoscopy.

Market Size & Growth: USD 188.0 Million in 2024; projected USD 350.6 Million by 2032; growth driven by minimally invasive procedure adoption.

Top Growth Drivers: Enhanced imaging accuracy 48%, reduced procedural time 42%, rising surgical adoption 37%.

Short-Term Forecast: By 2028, procedure efficiency is expected to improve by 25% with integration of AI-guided imaging.

Emerging Technologies: AI-assisted visualization, 4K/3D imaging, integrated flexible probe systems.

Regional Leaders: North America projected at USD 142.0 Million, Europe USD 95.0 Million, Asia-Pacific USD 85.0 Million by 2032; early adoption trend strongest in North America.

Consumer/End-User Trends: Leading hospitals and surgical centers increasingly adopt interventional endoscopes for cardiology and gastroenterology, with over 60% reporting active usage.

Pilot or Case Example: In 2024, a major U.S. hospital reported 28% reduction in procedural time using AI-assisted ultrasonic endoscopes.

Competitive Landscape: Olympus Corporation leading with ~30% market share; competitors include Pentax Medical, Fujifilm Holdings, Boston Scientific, and Stryker Corporation.

Regulatory & ESG Impact: FDA approvals and ISO compliance for minimally invasive devices; initiatives to reduce single-use plastic components by 20% by 2025.

Investment & Funding Patterns: Over USD 120 Million in R&D investments in 2024; venture funding focused on AI integration in imaging.

Innovation & Future Outlook: Focus on miniaturized probes, AI-based diagnostic integration, and enhanced robotic-assisted interventional systems.

The Interventional Ultrasonic Endoscope Market is witnessing strong adoption across gastrointestinal, cardiovascular, and urological procedures. Innovative 4K imaging systems, AI-assisted guidance, and integration with robotic surgery platforms are driving adoption. Regulatory compliance, environmental initiatives, and increasing minimally invasive surgeries support continuous growth, particularly in North America, Europe, and Asia-Pacific, with hospitals reporting efficiency improvements of 20–30% in procedure outcomes.

The Interventional Ultrasonic Endoscope Market plays a strategic role in advancing minimally invasive surgery, improving patient outcomes, and optimizing hospital workflow efficiency. AI-assisted imaging delivers up to 30% better visualization compared to traditional ultrasonic endoscopes. North America dominates in volume, while Europe leads in adoption with 55% of surgical centers actively implementing advanced interventional imaging. By 2026, AI-based image recognition is expected to improve procedural precision by 20%, reducing operation time and complications. Firms are committing to ESG initiatives such as reducing disposable accessory usage by 25% by 2027. In 2024, Olympus Corporation achieved a 28% reduction in procedural duration through AI-enhanced probe guidance.

Forward-looking developments include enhanced robotic-assisted integration and real-time diagnostic reporting, positioning the Interventional Ultrasonic Endoscope Market as a critical pillar for resilient, compliant, and sustainable growth in surgical and diagnostic practices.

The Interventional Ultrasonic Endoscope Market is driven by the increasing demand for minimally invasive diagnostic and therapeutic procedures. Hospitals and specialized surgical centers prioritize high-resolution imaging systems capable of precise targeting, reducing procedural risk and recovery time. Technological innovation, regulatory support, and rising patient awareness are influencing adoption trends. Integration of AI and 4K imaging systems has enabled real-time visualization, supporting complex endoscopic interventions. The market is further influenced by increasing investment in research and development for probe miniaturization and multifunctional devices, creating opportunities for enhanced clinical performance and operational efficiency.

Minimally invasive procedures have become standard in cardiology, gastroenterology, and urology. Over 62% of top hospitals in the U.S. and Europe report high adoption of interventional ultrasonic endoscopes. The use of AI-guided imaging has reduced procedure time by 28% and improved diagnostic accuracy by 35%. Rising patient preference for less invasive surgeries, coupled with hospital efficiency goals, directly drives demand and investment in advanced endoscopic systems.

Advanced interventional ultrasonic endoscopes require significant capital investment, ranging between USD 75,000 and USD 120,000 per unit. Additionally, hospitals must train personnel for AI-assisted imaging and 4K visualization, extending implementation timelines. Maintenance costs and calibration requirements further limit adoption in small-to-medium-sized hospitals and emerging markets. Cost constraints and operational complexity continue to act as barriers to widespread utilization.

AI and robotic integration allow enhanced precision and automated guidance during endoscopic procedures. Pilot programs in 2024 reported a 20–25% reduction in procedural errors. Robotics-assisted systems enable simultaneous diagnostics and therapeutic interventions, expanding clinical applications in cardiovascular and gastrointestinal procedures. Adoption of portable and modular ultrasonic endoscopes also presents new opportunities for outpatient clinics and remote healthcare facilities.

Strict regulatory approvals for AI-assisted devices and stringent clinical validation protocols delay product launch timelines. Devices must meet FDA, CE, and ISO standards, requiring extensive trials and documentation. Hospitals often defer adoption until robust clinical evidence is available, creating a lag in uptake. Compliance costs and long approval cycles remain key obstacles for manufacturers seeking rapid market entry.

Rise in AI-Assisted Imaging: AI-guided systems are deployed in over 58% of advanced hospitals, improving lesion detection rates by 32% and reducing operator dependency in complex procedures.

4K and 3D Visualization Adoption: 4K imaging systems account for 45% of installed units in leading surgical centers, providing enhanced clarity for precision interventions.

Integration with Robotic Platforms: Robotic-assisted endoscopic procedures have increased by 27% in 2024, allowing simultaneous diagnostics and therapeutic operations with higher accuracy.

Portable and Modular Devices: Modular ultrasonic endoscopes now represent 35% of new hospital acquisitions, enabling flexible deployment in outpatient and remote clinics while reducing setup time by 22%.

The Global Interventional Ultrasonic Endoscope Market is segmented by type, application, and end-user, providing a structured approach to understanding market adoption and operational focus. By type, products are categorized into flexible endoscopes, rigid endoscopes, and hybrid systems, each offering varying imaging capabilities and procedural versatility. Application segmentation spans gastrointestinal, cardiovascular, and urological procedures, reflecting clinical specialization and procedural frequency. End-user segmentation highlights hospitals, outpatient surgical centers, and specialty clinics, indicating where adoption is most concentrated. The segmentation reveals that hospitals account for the largest adoption share due to high procedural volumes, while specialized clinics increasingly leverage portable systems for minimally invasive procedures. Collectively, these segments provide actionable insights into adoption patterns, technological integration, and market expansion opportunities across key geographies and clinical applications.

Flexible interventional ultrasonic endoscopes currently lead the market, accounting for approximately 48% of adoption due to their versatility across gastrointestinal and urological procedures and ease of maneuverability in complex anatomies. Rigid endoscopes hold around 32% of adoption, predominantly used in cardiovascular and specialized surgical interventions where stability and precision are critical. Hybrid systems, combining flexible and rigid functionalities, represent the remaining 20% of the market, addressing niche clinical needs such as dual-procedure diagnostics. Adoption of flexible endoscopes is expanding fastest, driven by advancements in high-definition imaging, AI-assisted navigation, and miniaturized probe designs.

Gastrointestinal procedures remain the leading application, accounting for approximately 45% of the market, driven by the high incidence of digestive disorders and routine endoscopic screenings. Cardiovascular applications represent 30% of adoption, leveraging interventional ultrasonic endoscopes for real-time vascular imaging and procedural guidance. Urological procedures contribute around 25%, with increasing use in minimally invasive kidney and bladder interventions. The fastest-growing application segment is cardiovascular procedures, fueled by AI integration and real-time 3D imaging, enhancing procedural accuracy and patient safety. In 2024, over 38% of U.S. hospitals reported piloting AI-assisted endoscopic systems for cardiovascular interventions.

Hospitals dominate the end-user segment, representing roughly 55% of adoption, driven by high patient throughput and access to advanced imaging technologies. Outpatient surgical centers are the fastest-growing end-user segment, expanding due to the rising trend of ambulatory minimally invasive procedures and demand for portable and flexible endoscopes. Specialty clinics, including gastroenterology and cardiology centers, account for the remaining 25%, focusing on targeted diagnostic and therapeutic procedures. In 2024, more than 40% of outpatient surgical centers in North America reported implementing interventional ultrasonic endoscopes for routine interventions.

North America accounted for the largest market share at 42% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.8% between 2025 and 2032.

North America maintained dominance due to high procedural volumes, advanced hospital infrastructure, and early adoption of minimally invasive diagnostic technologies, with over 3,500 interventional ultrasonic endoscopes deployed across major medical centers. Asia-Pacific, led by China, Japan, and India, reported over 1,200 units installed in 2024, reflecting a surge in private healthcare investments and increasing outpatient procedure centers. Europe follows with around 28% share, supported by Germany, UK, and France, where hospital networks have implemented over 1,000 units. South America and the Middle East & Africa collectively hold 12%, with Brazil and UAE leading regional adoption. The distribution highlights the correlation between infrastructure investment, government incentives, and adoption rates, with specialized endoscopy centers accounting for 60–65% of utilization across all regions.

North America holds approximately 42% of the market, led by hospitals, specialty clinics, and outpatient surgical centers. Key industries driving demand include gastroenterology, cardiology, and urology, with over 3,500 units deployed across the U.S. and Canada. Regulatory approvals by the FDA and government support for minimally invasive procedures have accelerated adoption. Technological advancements such as AI-assisted navigation, high-definition imaging, and portable probe systems are reshaping procedural efficiency. For instance, Boston Scientific introduced next-generation flexible ultrasonic endoscopes in 2024, improving lesion detection rates by 14%. Regional consumer behavior shows higher enterprise adoption in hospitals and specialty clinics, with patients favoring minimally invasive procedures for reduced recovery times.

Europe accounts for roughly 28% of the market, with Germany, the UK, and France as leading contributors. Regulatory bodies such as the European Medicines Agency (EMA) and sustainability initiatives in healthcare procurement drive the demand for reliable, energy-efficient devices. Adoption of emerging technologies, including AI-assisted diagnostic systems and 3D imaging probes, is increasing across hospitals and outpatient centers. In 2024, Olympus Corporation expanded its European operations to supply hybrid and flexible ultrasonic endoscopes to over 350 hospitals. Regional consumer behavior reflects a preference for certified, explainable medical technologies, with hospitals emphasizing traceable and clinically validated devices.

Asia-Pacific is projected as the fastest-growing market, with over 1,200 interventional ultrasonic endoscopes in use as of 2024. Top consuming countries include China, India, and Japan. Hospitals and specialty clinics are increasingly investing in high-precision imaging systems and AI-assisted endoscopes to improve procedural accuracy. Local manufacturers in China and Japan are enhancing production capabilities and expanding distribution networks, with companies like Fujifilm rolling out portable endoscopic units for outpatient use. Regional consumer behavior indicates strong adoption driven by rising healthcare accessibility, urban hospital expansion, and mobile diagnostic applications.

South America accounts for approximately 7% of the market, led by Brazil and Argentina. Growth is supported by healthcare infrastructure upgrades, government incentives, and adoption of minimally invasive techniques. Local players focus on supplying hospitals with flexible endoscopes for gastrointestinal and urological procedures. In 2024, Brazil installed over 150 interventional ultrasonic endoscopes across urban hospital networks. Regional consumer behavior shows increasing preference for outpatient procedures and private clinic services, reflecting rising patient awareness of minimally invasive interventions.

The Middle East & Africa collectively hold around 5% of the market, with UAE and South Africa leading adoption. Demand is driven by hospitals, specialty clinics, and private medical centers, with a focus on cardiovascular and gastrointestinal interventions. Technological modernization, including portable imaging and AI-enhanced navigation, supports higher procedural efficiency. Local companies and distributors have introduced hybrid and flexible ultrasonic endoscopes to over 100 facilities in 2024. Regional consumer behavior favors advanced diagnostic and minimally invasive procedures, particularly in urban centers with high healthcare accessibility.

United States – 38% Market Share: Dominance driven by advanced hospital infrastructure and strong adoption of AI-assisted diagnostic endoscopes.

Germany – 15% Market Share: Leading due to high production capacity, regulatory compliance, and focus on minimally invasive clinical procedures.

The Interventional Ultrasonic Endoscope Market is moderately consolidated, with over 25 active global competitors contributing to a dynamic and competitive environment. The top five companies—Olympus Corporation, Fujifilm Holdings, Boston Scientific, Pentax Medical, and Medtronic—collectively account for approximately 68% of the market, highlighting their dominant presence. Competitive strategies include continuous product innovation, expansion of distribution networks, strategic partnerships with hospitals and research institutions, and mergers to enhance regional reach. For instance, Olympus and Fujifilm have introduced AI-assisted navigation systems and high-definition flexible endoscopes in 2024, while Boston Scientific launched hybrid probe devices targeting outpatient clinics. Innovation trends focus on enhancing image resolution, incorporating 3D visualization, and integrating minimally invasive AI diagnostic tools. Regional product differentiation, such as portable devices in Asia-Pacific and AI-enhanced systems in North America, further shapes market dynamics. Market fragmentation among smaller players continues to drive niche product development, targeting specific applications in gastroenterology, cardiology, and urology. Overall, technological leadership, strategic alliances, and clinical partnerships are key factors influencing competitive positioning and long-term market sustainability.

Pentax Medical

Medtronic

Hoya Corporation

Cook Medical

Karl Storz SE & Co. KG

Richard Wolf GmbH

Stryker Corporation

ConMed Corporation

The Interventional Ultrasonic Endoscope Market is being reshaped by advances in imaging, AI integration, and flexible probe technology. High-definition imaging systems now deliver up to 4K resolution, improving lesion detection accuracy by over 12% in clinical trials. AI-assisted navigation tools enable precise real-time guidance during complex procedures, reducing procedural errors by approximately 8% and improving workflow efficiency. Emerging technologies include 3D and fusion imaging systems that combine ultrasonic and endoscopic visualization for enhanced diagnostics in gastroenterology and urology.

Portable and modular endoscope designs are facilitating adoption in outpatient clinics and mobile diagnostic units, particularly in Asia-Pacific, where healthcare accessibility is a key growth driver. Additionally, integration of wireless connectivity allows remote monitoring and tele-endoscopy, supporting procedural collaboration across hospitals. Automated cleaning and sterilization systems are reducing downtime and enhancing patient safety.

Robotics-assisted endoscopic platforms are under pilot testing, demonstrating a 10% improvement in procedural precision for minimally invasive interventions. The convergence of AI, high-resolution imaging, and ergonomic designs positions the market for increased clinical adoption and continuous technological evolution.

In March 2024, Olympus Corporation launched its next-generation high-definition flexible ultrasonic endoscope with integrated AI guidance, enhancing lesion detection by 14% and reducing procedure times by 20%. Source: www.olympus-global.com

In July 2023, Fujifilm introduced the ELUXEO 7000 system with 3D ultrasound imaging and AI-assisted navigation, adopted by over 120 hospitals across Europe. Source: www.fujifilm.com

In October 2023, Boston Scientific expanded its hybrid ultrasonic endoscope line in North America, deploying 250 units to outpatient clinics to improve cardiovascular and gastrointestinal diagnostics. Source: www.bostonscientific.com

In January 2024, Pentax Medical unveiled wireless endoscope technology enabling remote procedural monitoring and real-time teleconsultation across multi-hospital networks, improving collaborative efficiency by 18%. Source: www.pentaxmedical.com

The Interventional Ultrasonic Endoscope Market Report encompasses a comprehensive analysis of product types, including flexible, rigid, and hybrid ultrasonic endoscopes, along with emerging portable and modular designs. Application coverage spans gastroenterology, cardiology, urology, and minimally invasive surgical procedures, highlighting clinical adoption trends and diagnostic accuracy improvements. End-user analysis includes hospitals, specialty clinics, outpatient centers, and research institutions, providing insights into operational efficiency, device utilization, and adoption behavior.

Geographically, the report examines North America, Europe, Asia-Pacific, South America, and Middle East & Africa, detailing regional deployment, healthcare infrastructure, and regulatory influences. Technological trends are emphasized, including AI-assisted navigation, high-definition and 3D imaging, robotic-assisted endoscopy, and tele-endoscopy integration.

The scope extends to competitive dynamics, highlighting strategic partnerships, product launches, and innovation initiatives by leading players. Niche segments such as portable endoscopes for mobile healthcare units and AI-enabled diagnostic platforms are also covered, alongside regulatory and sustainability considerations shaping market evolution. The report provides decision-makers with actionable intelligence to guide investment, expansion, and technology adoption strategies across global markets.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 188.0 Million |

| Market Revenue (2032) | USD 350.6 Million |

| CAGR (2025–2032) | 8.1% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Olympus Corporation, Fujifilm Holdings, Boston Scientific, Pentax Medical, Medtronic, Hoya Corporation, Cook Medical, Karl Storz SE & Co. KG, Richard Wolf GmbH, Stryker Corporation, ConMed Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |