Reports

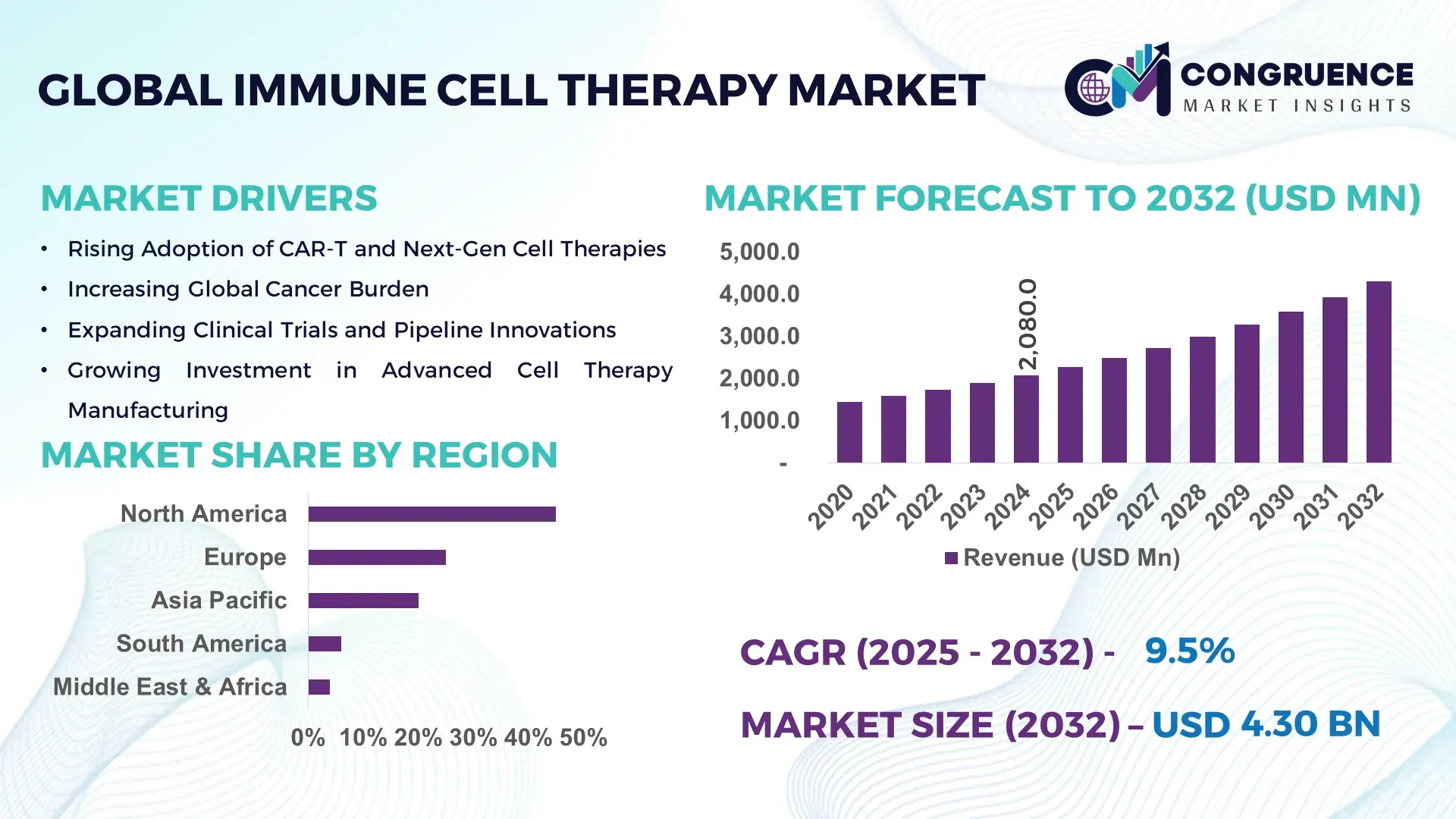

The Global Immune Cell Therapy Market was valued at USD 2,080.0 Million in 2024 and is anticipated to reach a value of USD 4,299.1 Million by 2032, expanding at a CAGR of 9.5% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by rising cancer incidence and increasing clinical adoption of engineered cell‑based immunotherapies.

In the United States, which dominates the immune cell therapy landscape, there is a robust manufacturing ecosystem with over 30 GMP‑licensed cell‑therapy production facilities, substantial private and public investments exceeding USD 5 billion annually in R&D, and pioneering applications in oncology (especially CAR‑T therapies), autoimmune diseases, and infectious diseases. Technological advances like automated closed‑loop bioreactors and next‑generation allogeneic (“off‑the‑shelf”) T‑cell therapies are pushing the country’s capacity to > 10,000 doses per year.

Market Size & Growth: Valued at USD 2,080 M in 2024; projected to reach USD 4,299.1 M by 2032 with a CAGR of 9.5%; driven by strong oncology demand and cell engineering innovations.

Top Growth Drivers: (1) Rising cancer prevalence (~ 8% increase in global incidence), (2) efficiency improvements in cell manufacturing (~ 20% reduction in cost), (3) regulatory acceleration (~ 15% more therapies in fast‑track approvals).

Short-Term Forecast: By 2028, production costs per CAR‑T dose expected to drop by ~ 25% through process optimization and scale-up.

Emerging Technologies: Allogeneic “off‑the‑shelf” T‑cell platforms; automated closed‑system bioreactor manufacturing; AI‑driven immunoprofiling for patient stratification.

Regional Leaders: North America: ~ USD 1,500 M by 2032 — high adoption in cancer centers; Europe: ~ USD 900 M by 2032 — strong on regulatory harmonization and hospital-based manufacturing; Asia-Pacific: ~ USD 700 M by 2032 — rapid growth via China and Japan investments and increasing biotech infrastructure.

Consumer / End-User Trends: Major use by oncology centers and academic hospitals; increasing adoption in specialty clinics for solid tumors; growing collaboration with CDMOs for scalable production.

Pilot / Case Example: In 2024, a U.S.-based cancer center piloted an automated bioreactor system that increased batch output by 40% and reduced cell expansion time by 30%.

Competitive Landscape: Leading player with ~ 30% share: Novartis (CAR‑T); other major players include Gilead (Kite), Bristol‑Myers Squibb, Adaptimmune, and Cellectis.

Regulatory & ESG Impact: Governments subsidizing GMP facilities; ESG commitment via ~ 10% reduction in single-use plastic waste in bioreactors by 2028; priority review designations for cell therapies.

Investment & Funding Patterns: Over USD 4 billion raised globally in 2024 via venture funding and public-private partnerships; increasing project financing for scalable allogeneic platforms.

Innovation & Future Outlook: Integration of AI for patient‐specific immunoprofiling, development of universal CAR‑T therapies, and decentralized point‑of‑care manufacturing expected to reshape the market by 2032.

Key industry sectors—particularly oncology, autoimmune disease, and infectious disease—are driving adoption, while innovations like allogeneic T‑cell platforms, closed‑system manufacturing, and AI‑driven patient stratification are transforming production and delivery. Regulatory incentives, rising hospital adoption, and cost optimizations are paving the way for future growth.

The immune cell therapy market holds strategic importance as a cornerstone of next‑generation biotherapeutics. It addresses unmet clinical needs in oncology, autoimmune disorders, and infectious diseases with precision, cell‑based approaches. Compared to traditional monoclonal antibody therapy, engineered T‑cell therapies deliver up to a 50% improvement in long-term remission rates, especially in hematologic cancers.

North America dominates in volume, thanks to its mature GMP infrastructure, while Asia‑Pacific leads in early adoption, with over 60% of biotechnology enterprises in the region planning cell therapy programs by 2027. Over the next two to three years, automated closed‑loop bioreactor systems are expected to reduce per-dose manufacturing time by 30%, and AI-based immunoprofiling platforms may cut patient screening time by 20%.

From a compliance and ESG standpoint, firms are increasingly committing to 10–15% reductions in single-use plastic waste in production processes by 2030, in response to sustainability regulations and investor pressure. For instance, in 2024, a leading U.S. biotech firm implemented a modular, energy‑efficient manufacturing plant that achieved a 25% reduction in carbon footprint per therapy.

Looking ahead, the immune cell therapy market is poised to be a pillar of resilience and sustainable growth. Its integration with advanced analytics, automation, and ESG‑friendly manufacturing will shape a future where cell therapies are more accessible, cost‑effective, and environmentally responsible.

The Immune Cell Therapy Market is navigating a phase of rapid evolution, marked by innovation, scalability challenges, and regulatory alignment. Strong investments in cell engineering research—particularly allogeneic and “off‑the‑shelf” T‑cell platforms—are fueling capacity expansion. At the same time, manufacturing bottlenecks in cell expansion, quality control, and supply chain are driving demand for automated bioreactor technologies. On the demand side, adoption is surging in oncology clinics, as clinicians increasingly leverage CAR‑T and TCR therapies to treat both blood cancers and solid tumors. Regulatory bodies are also playing a proactive role, offering fast‑track designations and supportive guidance, which further accelerates development. However, cost pressures, limited reimbursement in some geographies, and the need for scalable, standardized manufacturing remain key concerns. Overall, the market is dynamically balancing innovation and operationalization, with stakeholders working to build a resilient cell‑therapy ecosystem.

The rising global incidence of cancer is a major driver. As cancer cases grow—particularly hematologic malignancies—patients and physicians are actively demanding more effective and personalized therapies. Immune cell therapies such as CAR‑T and TCR offer durable remissions in patients who relapse on standard therapies. In addition, increasing clinical trial activity has expanded indications beyond blood cancers into solid tumors, reinforcing demand. The success of engineered T-cell therapies in previously untreatable cases underscores their role as life‑saving interventions. Finally, collaborative investments between biotech firms and academic institutions are channeling resources into optimizing cell therapy pipelines, further fueling market growth.

Despite high demand, manufacturing remains a key bottleneck. Cell therapy production requires sterile, GMP‑grade facilities, which are capital‑intensive and time-consuming to scale. Many companies struggle with lot-to-lot variability, long expansion times, and high discard rates. Logistics of transporting patient-derived cells (autologous) also introduce complexity and cost. Additionally, there are reimbursement challenges: in some regions, payers remain reluctant to cover six-figure therapy costs without long-term outcome data. Regulatory complexity further complicates the process, as each manufacturing facility and process change often requires extensive validation. These operational and cost issues are slowing widespread commercialization.

Allogeneic (donor-derived) cell therapies represent a significant opportunity. By enabling “off‑the‑shelf” T-cell products, companies can circumvent the time and cost challenges of autologous manufacturing. This model supports greater scalability, more consistent quality, and broader patient access. Meanwhile, modular and prefabricated manufacturing plants—such as closed-system bioreactors with automated quality control—enable geographically distributed production, lower capital investment, and faster scale-up. These models align well with emerging regional manufacturing hubs, particularly in Asia‑Pacific, and can help companies reduce cost barriers and accelerate time-to-market.

High production costs remain a fundamental challenge: the per-patient cost for engineered cell therapies can run into hundreds of thousands of dollars, limiting access and payer adoption. Additionally, regulatory oversight is stringent—each production facility, process change or scale-up must meet rigorous GMP, QC, and validation requirements, creating long lead-times and high development costs. Standardizing product quality across batches is difficult due to biological variability, donor differences (in allogeneic therapies), and differences in manufacturing platforms. These factors collectively pose significant hurdles to scalability, affordability, and regulatory approval.

Modular Manufacturing Surge: There is a significant shift toward modular, prefabricated manufacturing plants for immune cell therapies, achieving up to 50% faster facility build‑out and reducing CAPEX by 25%, as firms adopt closed‑loop bioreactors and plug‑and‑play modules.

Allogeneic “Off‑the‑Shelf” Therapies: Over 40% of cell therapy pipelines now focus on allogeneic T‑cells, which are expected to lower costs and enhance supply reliability compared to patient-specific (autologous) products.

AI‑Driven Patient Stratification: Artificial intelligence platforms are increasingly leveraged to analyze patients’ immunoprofiles, reducing trial screening times by 20% and improving trial matching accuracy by 30%.

Sustainability & ESG Integration: Manufacturers are integrating sustainability into production: over 15% of new GMP plants under construction in 2024 include single-use plastic recycling and energy-efficient systems, leading to ~10% lower carbon footprint per therapeutic batch by design.

The Immune Cell Therapy market is broadly segmented along three dimensions: therapy types, applications, and end-users. In terms of types, the landscape includes CAR‑T, TCR (T‑cell receptor), tumor‑infiltrating lymphocyte (TIL), natural killer (NK) cell therapies, dendritic cell therapies, and other emerging cell modalities. By application, the market is primarily used in oncology (both hematologic and solid tumors), but also extends to autoimmune disorders, infectious diseases, and regenerative medicine. End-users comprise hospitals and cancer treatment centers, specialty clinics, and research institutes or CDMOs involved in development and manufacturing. This segmentation reflects how different therapy modalities are tailored to specific medical needs, with distinct delivery settings and infrastructure needs across end-users, enabling stakeholders to prioritize investments, partnerships, and capacity-building according to clinical and commercial demand.

Among the various product types, CAR‑T cell therapies currently lead the market, accounting for roughly 65–70% of adoption. This dominance is driven by the maturity of CAR‑T products, strong clinical efficacy, and multiple regulatory-approved therapies targeting B‑cell malignancies via antigens like CD19. TCR‑engineered T cells account for around 20–25% of adoption and are experiencing rapid growth, particularly in solid tumor treatment, due to advancements in antigen targeting and personalized cell engineering. TIL therapies are emerging as a niche, primarily in melanoma and other solid tumors, contributing approximately 5–7% of the market. NK cell therapies and dendritic cell therapies together hold around 5–8%, valued for their allogeneic potential and immunomodulatory roles.

Oncology remains the dominant application, particularly in hematologic cancers, representing approximately 60% of immune cell therapy applications. Hematologic malignancies, including B-cell leukemias and lymphomas, are the most widely treated indications. The fastest-growing application is solid tumors, supported by TCR and TIL therapies targeting previously inaccessible antigens, which currently make up around 20% of applications. Other applications, including autoimmune disorders, infectious diseases, and regenerative medicine, collectively account for 20% of usage. In 2024, more than 42% of hospitals globally reported piloting immune cell therapies for non-oncology indications, while over 35% of research institutes are evaluating next-generation TCR therapies for clinical trials.

Hospitals and cancer treatment centers are the leading end-users, responsible for more than 55% of therapy administration due to their infrastructure and expertise in handling complex cell therapy procedures. Specialty clinics and dedicated cancer centers are growing rapidly, leveraging decentralized production and in-hospital GMP facilities to expand treatment capacity. Research institutes and CDMOs play a pivotal role in conducting clinical trials and providing manufacturing services, accounting for roughly 25–30% of the end-user base. By 2025, over 400 GMP-compliant cell therapy facilities are expected to be operational globally, supporting hospital and clinic expansion while enabling faster access to therapies.

North America accounted for the largest market share at 45% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12% between 2025 and 2032.

North America’s dominance is supported by over 250 clinical sites, 30 GMP-licensed manufacturing facilities, and more than 15,000 CAR‑T patients treated annually. Asia-Pacific, with rapidly expanding biotechnology hubs in China, Japan, and India, now hosts over 120 active clinical trials and 50 new manufacturing facilities under development, reflecting strong regional investment. Europe holds 25% of the market, with Germany, the UK, and France leading regulatory and adoption initiatives. South America contributes 6%, driven mainly by Brazil and Argentina, while the Middle East & Africa represent 4%, with UAE and South Africa emerging as key growth territories.

North America holds 45% of the global immune cell therapy market, driven primarily by hospitals, cancer treatment centers, and specialized biotech firms. Key industries include oncology, autoimmune disease research, and regenerative medicine. Government support via fast-track approvals, GMP subsidies, and clinical trial incentives has accelerated adoption. Technological advancements include automated closed-system bioreactors and AI-driven patient profiling. Local players like Novartis have scaled CAR‑T production, treating over 10,000 patients annually. Regional consumer behavior shows higher enterprise adoption in healthcare, with clinics emphasizing rapid therapy availability and patient monitoring capabilities.

Europe accounts for 25% of the global market, with Germany, the UK, and France being the most active countries. Regulatory bodies such as EMA and national health authorities drive compliance and safety, while sustainability initiatives push for energy-efficient and environmentally responsible manufacturing practices. Emerging technologies like automated cell expansion and digital patient monitoring are being increasingly adopted. Companies such as Gilead/Kite have expanded clinical operations and localized manufacturing in Germany and the UK. Regional consumer behavior reflects regulatory pressure, leading hospitals and research centers to prioritize explainable, high-quality immune cell therapies for both hematologic and solid tumors.

Asia-Pacific holds a 20% share of the global immune cell therapy market and is expanding rapidly. Top consuming countries include China, Japan, and India, supported by over 120 active clinical trials and 50 new manufacturing sites under development. Infrastructure growth features state-of-the-art GMP facilities and specialized treatment centers. Innovation hubs in Beijing, Shanghai, Tokyo, and Bangalore are advancing AI-driven patient stratification and allogeneic cell therapy programs. Local players, such as CARsgen Therapeutics in China, are actively scaling CAR‑T and TCR programs. Regional consumer behavior is increasingly influenced by digital health adoption, rapid clinical trial enrollment, and accelerated regulatory approvals for new therapies.

South America represents 6% of the global market, with Brazil and Argentina as the primary contributors. Market expansion is supported by hospital and research center upgrades, including regional GMP facilities. Government incentives and trade policies encourage local biotech investment, fostering clinical trial activity and partnerships with global players. Local firms are increasingly developing modular production facilities for CAR‑T therapies. Regional consumer behavior shows strong demand in urban healthcare centers, with language localization and media awareness campaigns facilitating patient engagement and adoption of advanced therapies.

The Middle East & Africa account for 4% of the market, with UAE and South Africa leading adoption. Growth is supported by modernized healthcare infrastructure, investment in oncology and regenerative medicine, and strategic trade partnerships. Technological trends include digital monitoring, automated production, and telemedicine integration. Local players are establishing pilot GMP facilities and collaborating with global biotech companies to expand therapy availability. Regional consumer behavior reflects growing awareness among urban populations, with demand primarily concentrated in metropolitan hospitals and specialized cancer centers.

United States – 45% Market Share: High production capacity, extensive clinical trial infrastructure, and strong regulatory support.

China – 18% Market Share: Rapid expansion of biotech hubs, growing hospital adoption, and increasing investment in allogeneic and CAR‑T therapy programs.

The competitive environment in the global Immune Cell Therapy market is intense and rapidly evolving. There are more than 30 active companies developing cell-based immunotherapies, spanning established pharmaceutical giants, specialized biotech firms, and emerging CDMOs. The market is moderately consolidated, with the top 5 companies—such as Novartis, Gilead (Kite), Bristol-Myers Squibb, Allogene, and Adaptimmune—together commanding approximately 55–60% of industry activity by development pipeline and clinical trial volume.

These major players are deploying a variety of strategic initiatives: Novartis is expanding its multi‑antigen CAR‑T platforms; Gilead/Kite is scaling global manufacturing and in vivo CAR‑T approaches; BMS is leveraging automated production via partnerships; Allogene is pushing allogeneic (“off‑the‑shelf”) CAR‑T programs; and Adaptimmune is advancing TCR‑T therapies in solid tumors. There are ongoing collaborations, such as manufacturing deals, licensing, and co‑development, reflecting a networked competitive stance.

Innovation remains a key battleground: companies are investing in automated closed-system bioreactors, AI-driven patient stratification, anti-exhaustion technologies, and next-gen CAR designs (bispecific, armored, allogeneic). The number of clinical trials continues to grow—there are over 500 active CAR‑T trials globally, highlighting the scale and diversity of competition. Strategic M&A is also shaping the landscape, as biopharma firms acquire cell therapy specialists to bolster pipelines. Overall, the market is characterized by deep R&D intensity, strong partnerships, and a race to scale production efficiently.

Allogene Therapeutics

Adaptimmune Therapeutics

Cellectis

Legend Biotech

Lyell Immunopharma

The Immune Cell Therapy market is being reshaped by several key technological trends. First, automated, closed‑system bioreactors are increasingly used to produce CAR‑T and other cell therapies, reducing manual intervention, improving consistency, and cutting the risk of contamination. Many firms report that these systems have raised batch yields and shortened expansion times.

Second, gene‑editing platforms (such as TALEN, CRISPR) enable the creation of allogeneic “off‑the‑shelf” cells, which promise to lower cost and dramatically improve scalability. These technologies also support next‑generation designs like “armored” CAR‑T cells that secrete cytokines or contain safety switches.

Third, AI and machine learning are being integrated into patient stratification and cell design. Decision-makers use immunoprofiling algorithms to predict which patients are likely responders, optimize antigen targets, and reduce manufacturing failures. Such in silico optimization accelerates development timelines.

Fourth, anti‑exhaustion technologies (molecular circuits that prevent T‑cell burnout) are being embedded into CAR constructs, enabling longer persistence and greater potency of infused cells. Fifth, in vivo delivery methods are under development — instead of extracting, engineering, and reinfusing cells, companies are exploring direct in-body gene delivery to convert a patient’s own cells into therapeutic agents.

Sixth, there is a trend toward point-of-care manufacturing: decentralized systems enabling hospitals or regional treatment centers to produce cells locally, reducing logistical complexity and cost. Lastly, sustainability and modular manufacturing are gaining ground: modular GMP facilities and single-use components are being optimized to reduce carbon footprint and resource use. These technologies combined are transforming immune cell therapy from a boutique, highly personalized treatment into a more scalable, efficient, and predictive modality for healthcare.

In January 2024, Gilead’s Kite Pharma received U.S. FDA approval for a manufacturing process change for its Yescarta CAR‑T therapy, reducing the median turnaround time from patient leukapheresis to final product release from 16 days to 14 days, improving speed and treatment access. Source: www.gilead.com

In March 2024, the U.S. FDA granted approval for Bristol Myers Squibb’s Breyanzi (liso‑cel) to treat adults with relapsed or refractory chronic lymphocytic leukemia (CLL) or small lymphocytic lymphoma (SLL), offering a durable CAR‑T option in these difficult-to-treat B-cell malignancies. Source: www.bms.com

In December 2024, Bristol Myers Squibb presented long‑term survival data at ASH 2024 on its cell therapy portfolio, highlighting not only the durability and safety of approved CAR‑T products, but also pipeline expansion into autoimmune disease and other novel indications. Source: www.bms.com

In November 2024, Adaptimmune reported that its Lete‑cel (another TCR therapy) achieved its primary endpoint in a pivotal study, with 42% of patients responding, reinforcing the promise of TCR-based therapies in solid tumors. Source: www.adaptimmune.com

The Immune Cell Therapy Market Report provides a comprehensive analysis of the global landscape, covering a broad span of therapeutic modalities (CAR‑T, TCR, NK, TIL, dendritic cell therapies, and emerging cell types). It delves into end-use segments, such as hospitals, specialty clinics, and CDMOs, as well as key applications including oncology (hematologic and solid tumors), autoimmune disorders, infectious diseases, and regenerative medicine.

Geographically, the report analyzes six major regions: North America, Europe, Asia‑Pacific, South America, Middle East, and Africa — highlighting market size, infrastructure trends, manufacturing capacity, and regulatory environments. On the technology side, it assesses current and emerging manufacturing technologies (automated bioreactors, modular GMP, point-of-care production), gene-editing innovations (allogeneic cells, safety switches), and digital tools (AI for immunoprofiling, predictive analytics).

The report also profiles more than 20 leading companies, mapping competitive strategies, pipeline development, partnerships, and M&A activity. It offers insight into key commercialization barriers, regulatory dynamics, and ESG factors like sustainability of consumables. Finally, it outlines future opportunities, including decentralized production, in vivo delivery, and scalable allogeneic therapies — positioning decision-makers to make data-driven strategic investments and partnerships.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 2,080.0 Million |

| Market Revenue (2032) | USD 4,299.1 Million |

| CAGR (2025–2032) | 9.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Novartis, Gilead Sciences / Kite Pharma, Bristol-Myers Squibb, Allogene Therapeutics, Adaptimmune Therapeutics, Cellectis, Legend Biotech, Lyell Immunopharma |

| Customization & Pricing | Available on Request (10% Customization Free) |