Reports

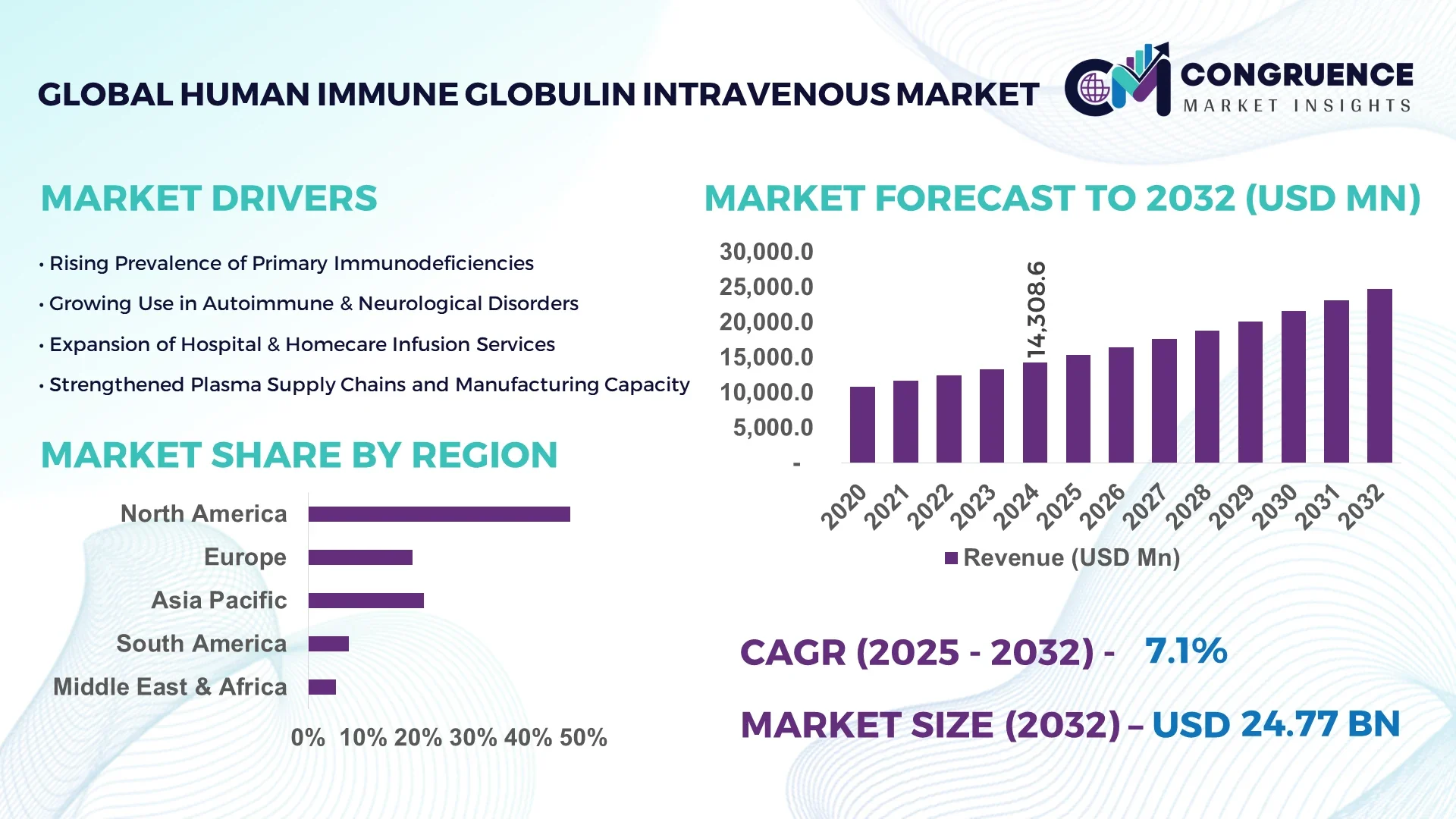

The Global Human Immune Globulin Intravenous Market was valued at USD 14,308.56 Million in 2024 and is anticipated to reach a value of USD 24,769.18 Million by 2032 expanding at a CAGR of 7.1% between 2025 and 2032.

The United States leads in the Human Immune Globulin Intravenous market with substantial biomanufacturing capabilities, robust investment in biopharmaceutical infrastructure, and advanced clinical applications for immunodeficiency and autoimmune conditions. The country continues to scale up production facilities and invest in cold-chain logistics technologies for efficient plasma-derived therapies.

The Human Immune Globulin Intravenous market has experienced substantial evolution driven by growing demand for immunoglobulin therapy in primary immunodeficiency diseases, chronic inflammatory demyelinating polyneuropathy, and Kawasaki disease. Healthcare systems globally are increasing the use of IVIG in off-label indications, including neurological and hematological disorders, further diversifying clinical use. Technological advancements in fractionation processes and recombinant alternatives have improved purity and safety, reducing infection risks. Countries like Germany, China, and Japan are boosting regional demand due to aging populations and rising autoimmune disease prevalence. Regulatory bodies such as the FDA and EMA have implemented stringent quality and safety guidelines for plasma sourcing and manufacturing, pushing companies to innovate in compliance. Environmental concerns related to plasma collection and disposal are spurring the adoption of greener processing methods. Additionally, the expansion of public health programs in developing economies is increasing access to immunoglobulin therapies, shaping long-term market growth.

Artificial Intelligence (AI) is reshaping the Human Immune Globulin Intravenous Market by introducing advanced data analytics, predictive modeling, and process automation into production and distribution pipelines. AI algorithms are optimizing plasma donor selection by analyzing genetic markers and health profiles to enhance the efficiency and yield of plasma collection. Machine learning models are now used in immunoglobulin batch tracking to ensure traceability, improving compliance with regulatory frameworks. AI-driven imaging and diagnostics are assisting clinicians in identifying eligible IVIG candidates faster and with greater precision, shortening treatment initiation timelines.

In manufacturing environments, AI-enabled process controls monitor temperature, pH, and flow rates during fractionation in real time, reducing contamination risks and operational waste. Pharmaceutical firms are employing AI tools for demand forecasting to align plasma procurement with shifting patient needs, especially in seasonal immune therapy cycles. Furthermore, AI chatbots and virtual assistants are being integrated into patient care to track IVIG infusion schedules and monitor side effects, enhancing post-treatment engagement. In logistics, route optimization tools using AI minimize delays in cold-chain delivery, ensuring that immunoglobulin therapies maintain efficacy upon arrival. As a result, the Human Immune Globulin Intravenous Market is benefiting from greater cost-efficiency, reduced human error, and improved scalability in both developed and emerging regions.

“In 2024, a major U.S.-based biopharmaceutical firm deployed an AI-powered digital twin platform across its IVIG production line, which resulted in a 15% increase in plasma protein yield and a 12% reduction in energy consumption within six months of implementation.”

The Human Immune Globulin Intravenous Market is shaped by evolving therapeutic needs, technological innovations, and increasing healthcare expenditure across both developed and emerging economies. Key dynamics include rising prevalence of primary immunodeficiency disorders, neurological conditions, and autoimmune diseases that require immunoglobulin-based therapies. Clinical demand is further reinforced by the growing acceptance of IVIG treatments for off-label uses. Governments and private healthcare providers are scaling up plasma collection infrastructure to meet increasing demand. Additionally, investments in biopharmaceutical manufacturing and cold-chain logistics are improving distribution capabilities. At the same time, regulatory harmonization and enhanced quality control standards are contributing to a more structured and resilient market ecosystem.

The increasing incidence of immunodeficiencies and chronic neurological diseases is significantly boosting the demand within the Human Immune Globulin Intravenous Market. Conditions like common variable immunodeficiency (CVID), Guillain-Barré syndrome, and chronic inflammatory demyelinating polyneuropathy (CIDP) are becoming more prevalent, especially in aging populations. For example, the incidence of CIDP is estimated at 1.6 to 8.9 per 100,000 people globally. This uptrend in immune-related health issues is compelling hospitals and specialty clinics to stock intravenous immunoglobulin as a frontline therapy. The consistency in clinical outcomes and the broadening spectrum of therapeutic applications are further pushing clinicians to opt for IVIG solutions, directly strengthening market growth.

One of the critical restraints affecting the Human Immune Globulin Intravenous Market is the complex and resource-intensive plasma collection process. Since IVIG is derived from human plasma, the market is highly dependent on donor availability, which is often regionally constrained. Regulatory standards for donor screening, pathogen testing, and plasma fractionation make the supply chain highly sensitive and vulnerable to disruptions. For instance, geopolitical tensions or health crises like pandemics can sharply reduce donor turnout and halt collection efforts. The time-consuming nature of processing—taking up to nine months from collection to product—further aggravates delays, making it challenging for manufacturers to meet real-time demand.

The Human Immune Globulin Intravenous Market is witnessing promising opportunities in emerging economies such as India, Brazil, and Southeast Asian nations. These regions are rapidly upgrading their healthcare infrastructure and implementing national immunization and treatment programs that include IVIG therapies. Governments are allocating greater budgets toward managing autoimmune and rare disorders, while foreign investments in local manufacturing facilities are increasing. In India alone, demand for plasma-derived therapies has grown by more than 30% over the past five years. Public-private partnerships and technology transfers are creating scalable models for cost-effective production and distribution, paving the way for broader market penetration.

Operating in the Human Immune Globulin Intravenous Market requires navigating stringent regulatory frameworks across multiple jurisdictions. Regulatory compliance involves rigorous documentation, pharmacovigilance, quality control audits, and adherence to evolving clinical trial protocols. For instance, manufacturers must ensure traceability of every plasma unit, conduct viral inactivation validation, and maintain sterile packaging and cold storage. These requirements contribute to elevated operational costs and extended time-to-market, particularly for new entrants or smaller biotech firms. Additionally, any deviation or non-compliance can result in product recalls, legal penalties, or facility shutdowns, posing substantial financial and reputational risks in a highly competitive market.

• Expansion of Home-Based IVIG Administration Services: The Human Immune Globulin Intravenous market is witnessing a surge in demand for home-based infusion services, especially across North America and Western Europe. An increasing number of patients with chronic autoimmune and immunodeficiency disorders are opting for at-home treatments due to improved patient convenience, reduced hospital costs, and availability of remote monitoring technologies. By 2024, over 28% of IVIG treatments in the U.S. were administered outside clinical settings, facilitated by mobile nursing services and telemedicine platforms that ensure adherence and monitor adverse effects.

• Integration of Smart Infusion Devices: Smart infusion pumps and digitally monitored delivery systems are becoming increasingly integrated into immunoglobulin administration, reducing dosing errors and enhancing patient safety. Devices now feature real-time alerts, programmable dosage limits, and integrated health record compatibility. The European market, in particular, is seeing rapid adoption of connected infusion technologies, with over 35% of hospital units in Germany reporting use of AI-enabled pump systems to administer IVIG therapies efficiently and safely.

• Strategic Manufacturing Capacity Expansions: Major pharmaceutical firms are scaling up IVIG production facilities through advanced fractionation technologies and regional manufacturing hubs. In 2024, more than six global biopharmaceutical companies announced investments in expanding plasma fractionation capacities across Asia-Pacific, targeting reduced import dependency. These expansions are intended to stabilize supply chains and support growing regional demand, particularly in China and India where immunoglobulin demand is rising significantly.

• Rise in Immunoglobulin Demand for Off-Label Neurological Use: The use of IVIG in treating off-label neurological disorders such as multiple sclerosis and Alzheimer’s-related cognitive decline is expanding. Clinical practices are increasingly recognizing IVIG as an adjunct or alternative where conventional treatments fail. A multicenter evaluation in 2024 indicated an uptick of over 19% in off-label neurological prescriptions across tertiary care hospitals in North America. This trend reflects shifting clinical guidelines and deeper understanding of immunological factors in neurodegenerative disorders.

The Human Immune Globulin Intravenous market is strategically segmented by type, application, and end-user, each category offering critical insights for industry stakeholders. Product type segmentation includes various immunoglobulin concentrations and formulations tailored for distinct clinical conditions. Application segmentation spans therapeutic areas such as immunodeficiency syndromes, autoimmune disorders, and hematological conditions, with newer categories like neurology showing rapid growth. End-user segmentation highlights hospitals, home care providers, specialty clinics, and diagnostic laboratories as key consumers. Among these, hospitals remain dominant due to their infrastructure and clinical expertise, but home infusion services are quickly gaining ground. The segmentation landscape is evolving with technological advancements, increased awareness, and tailored immunotherapy approaches driving differential adoption patterns across regions and facilities.

The Human Immune Globulin Intravenous market includes several types, notably 5% liquid, 10% liquid, lyophilized powders, and specialty formulations enriched for specific antibodies. Among these, the 10% liquid formulation leads in usage due to its enhanced bioavailability and reduced infusion time, making it preferred for both acute and chronic treatment cycles. It is widely adopted in hospital and home care environments for its dosing convenience. Meanwhile, the fastest-growing segment is specialty immunoglobulin products, particularly those developed for specific indications like anti-D immunoglobulin or hyperimmune globulins. Their rise is driven by demand for targeted therapy in conditions such as hepatitis B exposure and certain infections. Lyophilized powders hold relevance in regions lacking robust cold-chain infrastructure, offering stability advantages. Although less prominent in mature markets, the 5% formulation remains relevant in pediatric and sensitive cases due to lower viscosity and reduced infusion reactions.

Applications of Human Immune Globulin Intravenous span across primary immunodeficiency, chronic inflammatory demyelinating polyneuropathy (CIDP), immune thrombocytopenic purpura (ITP), Kawasaki disease, and off-label neurological uses. Primary immunodeficiency remains the leading application segment, supported by consistent diagnosis rates and lifelong treatment requirements. This segment benefits from early detection programs and high clinical awareness. CIDP is emerging as the fastest-growing application due to the increasing prevalence among the elderly population and favorable treatment outcomes. Advancements in neurology have prompted broader IVIG use, particularly in refractory cases. Kawasaki disease maintains a stable demand, especially in pediatric care settings in East Asia. Additionally, the off-label use of IVIG in neurology and infectious disease management is expanding, driven by growing clinical trials and evolving treatment protocols. Hospitals and specialty clinics are witnessing an uptick in such diverse applications, indicating the therapy’s versatility.

Hospitals dominate the Human Immune Globulin Intravenous market end-user segment owing to their capacity to manage complex infusion therapies, monitor adverse reactions, and provide critical care support. Their infrastructural readiness and access to emergency protocols make them the top choice for high-dose or long-duration IVIG treatments. Home healthcare services represent the fastest-growing end-user category, particularly in North America and Western Europe. Improved patient compliance, reduced hospitalization costs, and technological support for remote monitoring are key drivers of this shift. Specialty clinics also contribute significantly by offering niche immunology and neurology services, where IVIG is a core treatment. Diagnostic laboratories, while not direct consumers, support the market through disease detection and immunoglobulin level monitoring, influencing treatment initiation and customization. This diverse end-user structure enhances flexibility in market distribution and improves accessibility for patients across various treatment settings.

North America accounted for the largest market share at 47.6% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2025 and 2032.

North America’s market dominance is driven by advanced healthcare systems, widespread clinical adoption of IVIG therapies, and strong plasma collection infrastructure. Meanwhile, the Asia-Pacific region is experiencing rapid expansion due to rising immunological disease prevalence, large untreated patient populations, and growing investments in healthcare access and biomanufacturing capacity. Regional dynamics are being shaped by policy reforms, digital health integration, and rising awareness of immunoglobulin-based therapies among clinicians and patients.

Widespread Plasma Access and Digital Health Tools Fueling Demand

The Human Immune Globulin Intravenous market in this region held a commanding share of 47.6% in 2024. The expansion is strongly influenced by the United States, which leads in plasma collection volume and treatment availability across immunology and neurology sectors. Demand is bolstered by industries including biotechnology, specialty healthcare, and diagnostics. Regulatory agencies have expedited approval pathways for IVIG treatments, enhancing market fluidity. The FDA’s support for streamlined clinical trials and broader off-label use has widened adoption. Digitally enhanced infusion monitoring systems and AI-powered inventory tools are now widely used in hospitals and clinics, reducing wastage and improving therapeutic precision, driving long-term regional demand.

Harmonized Regulations and Manufacturing Excellence Accelerate Growth

The Human Immune Globulin Intravenous market in this region captured approximately 26.1% of the global share in 2024. Germany, France, and the United Kingdom are the key contributors due to well-developed healthcare frameworks and expanding plasma fractionation capacities. The European Medicines Agency has implemented centralized safety and quality regulations that streamline market entry and post-marketing surveillance. Sustainability initiatives such as green cold-chain logistics and energy-efficient bioprocessing are also gaining traction. The region is leveraging automation and AI-driven manufacturing technologies to increase plasma yield and reduce contamination risks. Demand from public hospitals and specialty immunology clinics is steadily climbing, driving consistent regional performance.

Rapid Healthcare Expansion and Domestic Biotech Innovation Driving Growth

The Human Immune Globulin Intravenous market in this region ranked highest in growth momentum globally in 2024. China, Japan, and India are the top-consuming countries, supported by expanding healthcare insurance coverage and increasing awareness about immunodeficiencies. China is investing in high-capacity fractionation plants, while India has seen over a 35% surge in immunoglobulin imports for hospital usage. Japan’s aging population contributes to strong demand in neurology and autoimmune segments. Regional biotechnology firms are collaborating with global players for technology transfers, improving domestic production. Tech innovation hubs in Singapore and South Korea are promoting AI-integrated plasma analytics and remote IVIG monitoring platforms.

Government-Backed Healthcare Programs Stimulating Market Uptake

The Human Immune Globulin Intravenous market in this region is gradually expanding, with Brazil and Argentina being the major contributors. Brazil alone accounted for more than 62% of the regional demand in 2024. National immunization and chronic disease management programs are creating steady demand for immunoglobulin therapies. Infrastructure modernization efforts across public hospitals, coupled with strategic import agreements, are enabling stable product supply. Governments are offering tax incentives and public-private partnerships to boost biopharmaceutical imports and local distribution. Additionally, increased clinical trials related to neurological disorders are raising the profile of IVIG therapies within the medical community.

Health Sector Digitization and Trade Alliances Expanding Accessibility

The Human Immune Globulin Intravenous market in this region is gaining traction due to increasing demand from UAE, Saudi Arabia, and South Africa. Regional health authorities are prioritizing immune-related therapies as part of chronic disease control programs. Demand is particularly high in hospital neurology departments and transplant centers. Technological modernization is underway, with AI-enabled diagnostic systems and electronic health records supporting more targeted treatment. Trade partnerships with Europe and Asia are boosting plasma product availability, while regulatory authorities such as the GCC-DR are aligning standards to international norms, accelerating market access. Infrastructure investments in specialty clinics further support uptake.

United States – 43.2% Market Share

High production capacity, advanced healthcare infrastructure, and wide clinical acceptance of IVIG therapy in immunology and neurology.

China – 14.6% Market Share

Strong end-user demand from hospitals, rapid healthcare expansion, and strategic investments in domestic plasma fractionation capacity.

The Human Immune Globulin Intravenous market is characterized by a moderately consolidated competitive landscape with approximately 25 to 30 actively operating global and regional players. Market competition is driven by technological advancements in plasma fractionation, strategic geographic expansions, and consistent product innovations. Leading companies are leveraging proprietary purification techniques and high-throughput manufacturing systems to achieve higher immunoglobulin yield and enhanced product stability. Strategic partnerships with plasma donation centers and healthcare institutions are key to securing raw material availability and ensuring uninterrupted supply chains.

In recent years, competition has intensified due to growing demand across neurology and immunology applications. Key players are diversifying their product portfolios by launching IVIG formulations with fewer side effects and improved infusion tolerability. Mergers and acquisitions remain a dominant strategy to gain regional presence and increase production capacity, especially in Asia-Pacific and Latin America. Additionally, digital transformation through AI-enhanced production and supply chain optimization tools is becoming a differentiating factor among top-tier companies. Competitive focus has also shifted toward environmental sustainability in manufacturing and adherence to evolving global regulatory standards, reinforcing brand trust and long-term market relevance.

Grifols S.A.

Takeda Pharmaceutical Company Limited

CSL Behring

Octapharma AG

Kedrion Biopharma

Bio Products Laboratory Ltd (BPL)

Shanghai RAAS Blood Products Co., Ltd.

China Biologic Products Holdings, Inc.

Biotest AG

LFB S.A.

The Human Immune Globulin Intravenous market is witnessing significant technological transformation, primarily driven by innovations in plasma fractionation, cold-chain logistics, digital integration, and bioprocess automation. Advanced chromatographic purification systems and solvent-detergent virus inactivation methods have enhanced the safety and consistency of IVIG formulations. These technologies help minimize protein aggregation and ensure higher immunoglobulin purity, reducing adverse infusion reactions and boosting therapeutic efficacy.

Real-time monitoring systems embedded with IoT sensors are increasingly used in plasma collection and processing facilities to maintain temperature, humidity, and other critical environmental parameters. AI and machine learning models are now integrated across plasma yield forecasting, inventory optimization, and infusion dosage prediction, resulting in operational efficiency and better treatment outcomes. In manufacturing, high-capacity centrifuges and membrane filtration techniques are being utilized to streamline large-scale immunoglobulin production, reducing cycle times.

Digital health solutions such as infusion monitoring apps and remote patient management tools are supporting home-based IVIG therapy, particularly in North America and Europe. Cold-chain innovations, including active thermal packaging and condition monitoring devices, ensure product integrity across long-distance shipments. These technological advancements are enabling manufacturers and healthcare providers to meet increasing global demand, improve safety profiles, and reduce operational bottlenecks in the Human Immune Globulin Intravenous market.

• In May 2024, CSL Behring expanded its Kankakee, Illinois manufacturing site with an added plasma fractionation line, increasing its capacity by 20%, aiming to meet the rising demand for intravenous immunoglobulin therapies in North America and Latin America.

• In September 2023, Grifols announced a strategic agreement with Canadian Blood Services to establish a new plasma collection center in Ontario. The facility targets the collection of over 100,000 liters of plasma annually to support IVIG production.

• In January 2024, Takeda launched a digital patient support program for individuals receiving IVIG therapy in Europe, integrating AI-powered reminders and symptom tracking to improve treatment adherence and reduce infusion-related complications.

• In November 2023, Octapharma completed a clinical trial assessing its new 10% liquid IVIG formulation in treating CIDP. The study demonstrated a 30% reduction in relapse rates and higher tolerability compared to earlier generation formulations.

The Human Immune Globulin Intravenous Market Report provides an in-depth analysis of the global industry, examining product types, clinical applications, geographic regions, technological innovations, and major end-user segments. It covers various formulation types including 5% and 10% liquid concentrations, lyophilized powders, and specialty immunoglobulins used in targeted therapies. Application areas span primary immunodeficiency, autoimmune diseases, neurology, hematology, and off-label indications such as organ transplant rejection management.

Geographically, the report addresses market activity and trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing demand drivers, healthcare infrastructure, and regulatory frameworks unique to each region. It evaluates major growth areas such as home infusion therapy, hospital-based treatments, and specialty clinic adoption.

The report also highlights the role of digital transformation in IVIG therapy delivery, cold-chain innovations, and the impact of AI on plasma collection and dosage personalization. Furthermore, it explores emerging segments such as recombinant immunoglobulin products and biosimilar development. Strategic insights are included on regulatory landscapes, competitive positioning, distribution networks, and patient access programs, making this report a comprehensive resource for stakeholders in manufacturing, distribution, clinical research, and healthcare delivery within the Human Immune Globulin Intravenous market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 14308.56 Million |

|

Market Revenue in 2032 |

USD 24769.18 Million |

|

CAGR (2025 - 2032) |

7.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Grifols S.A., Takeda Pharmaceutical Company Limited, CSL Behring, Octapharma AG, Kedrion Biopharma, Bio Products Laboratory Ltd (BPL), Shanghai RAAS Blood Products Co., Ltd., China Biologic Products Holdings, Inc., Biotest AG, LFB S.A. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |