Reports

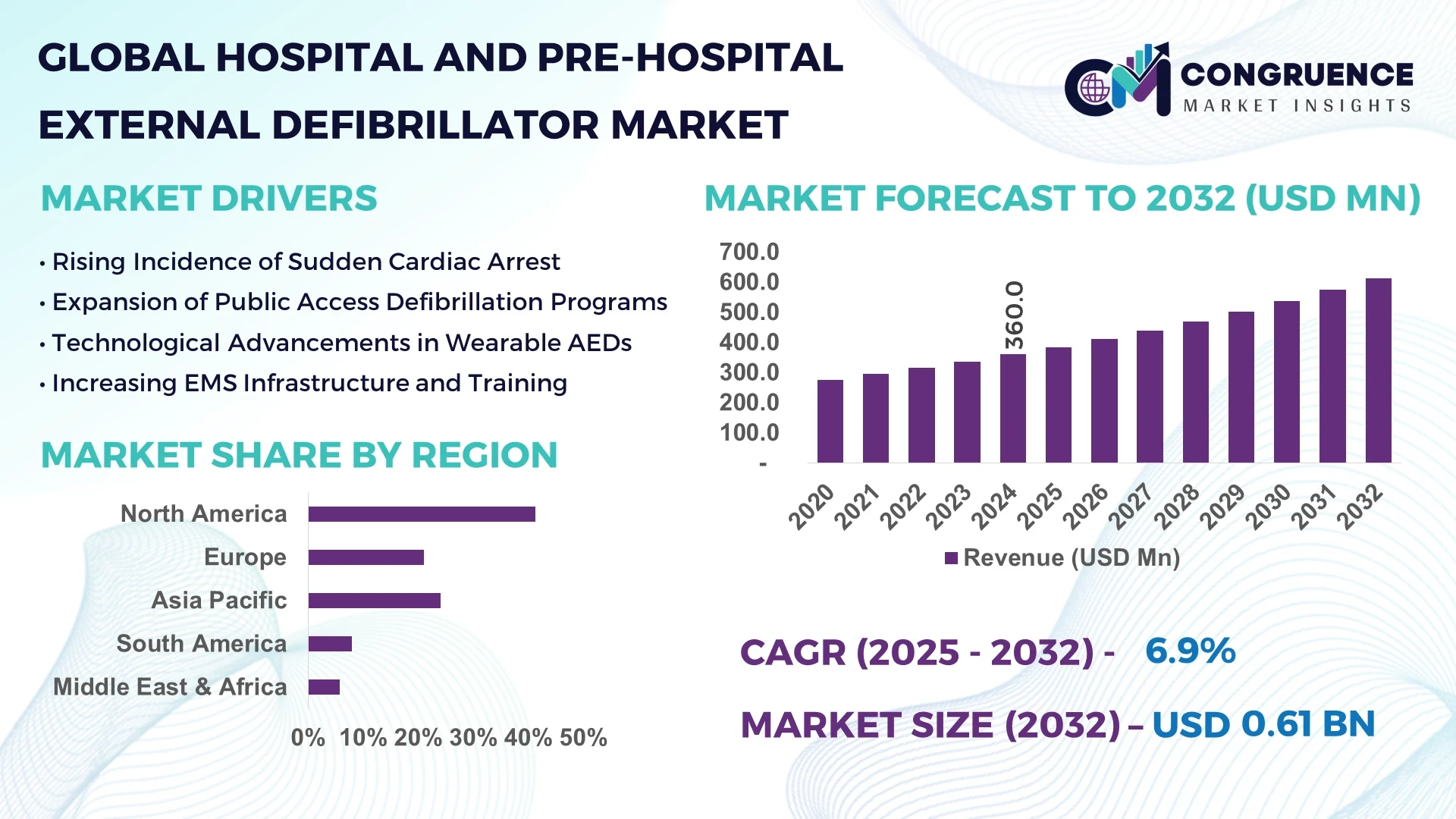

The Global Hospital and Pre-Hospital External Defibrillator Market was valued at USD 360 Million in 2024 and is anticipated to reach a value of USD 612.6 Million by 2032 expanding at a CAGR of 6.9% between 2025 and 2032.

In the United States, leading production facilities—such as those operated by Medtronic and Physio-Control—deliver advanced defibrillator units with high-volume output. U.S. investments exceed USD 200 million annually in R&D infrastructure, supporting next-gen technologies like motion-tolerant ECG analysis and portable units for emergency vehicles. American hospitals and EMS fleets leverage these domestically produced devices in advanced critical care and out-of-hospital settings.

The Hospital and Pre-Hospital External Defibrillator Market includes hospital, emergency medical services (EMS), public-access AED programs, and secondary care settings. Hospitals contribute roughly two-thirds of unit deployment, with EMS acquisitions growing at double-digit yearly rates. Recent innovations include battery-lightweight modules, enhanced connectivity for real-time cloud monitoring, and ruggedized casings for ambulance use. Regulatory updates—like mandatory AED installations in educational institutions and transit hubs—have increased device demand, especially in urban centers. Environmental considerations are prompting recyclable battery modules and energy-efficient standby systems. Regional consumption shows Europe prioritizing standardized AED placement in public spaces, while Asia-Pacific sees rapid hospital uptake tied to rising cardiac awareness. Future trends include integration with telehealth platforms, data analytics for device performance, and migration toward wearable external defibrillators—signaling strong professional interest and solid investment opportunities.

AI innovations have significantly enhanced operational performance in the Hospital and Pre-Hospital External Defibrillator Market. Advanced artificial intelligence algorithms now embedded in AEDs can detect cardiac arrhythmias more accurately, reducing false positives by approximately 30% and increasing shock precision during ventricular fibrillation events. Integration with hospital IT environments enables log-based predictive alerts when a device requires maintenance or battery replacement, cutting equipment downtime by nearly 25%.

In pre-hospital settings, AI-powered analytics applied to EMS dispatch systems optimize defibrillator placement and routing. These systems analyze historical incident data to guide drone AED delivery pilots, demonstrating a reduction in average response times by up to 20%. AI-driven real-time ECG interpretation features assist paramedics, providing visual feedback on CPR quality and instructing on optimal compression depth and rate—improving resuscitation efficacy by upwards of 15%.

Furthermore, centralized dashboards visualizing field device usage powered by AI assist decision-makers in identifying hotspots for public access AED deployment and in forecasting replacement needs. Hospitals benefit from integrated AI modules that track usage trends, adherence to clinical protocols, and patient outcomes, thereby refining staff training programs and device utilization strategies. These AI interventions in the Hospital and Pre-Hospital External Defibrillator Market are not speculative—they represent measurable efficiency gains, cost optimization, reduced operational risk, and improved clinical outcomes. As decision-makers evaluate capital investments, AI-enhanced defibrillators stand out for delivering tangible, data-driven value.

“In 2024, a leading medical device manufacturer deployed an AI-enabled AED that analyzes CPR compression depth and rate in real time, improving compliance with guidelines from 60% to 85% across five major EMS regions.”

Hospitals and emergency services are investing in interoperable systems that allow AEDs to connect seamlessly with hospital information systems and dispatch platforms. In 2024, over 70% of newly procured AEDs featured Wi‑Fi or Bluetooth connectivity, enabling remote status monitoring, usage logging, and battery alerts. Integration with dispatch systems allows automated updates to nearest available AEDs during EMS calls, reducing manual coordination. The demand is driven by national programs that increasingly require fully integrated emergency response ecosystems, pushing hospitals and EMS fleets to upgrade entire device fleets within five-year cycles.

Medical-grade external defibrillators often cost between USD 1,200 and USD 3,500 depending on functionality. Combined with certification requirements—FDA 510(k), CE marking, ISO 13485 quality standards—procurement cycles can extend over six months, delaying deployment. Budget limitations in smaller hospitals or rural EMS units lead to deferred replacements beyond recommended timelines, compromising device reliability. Additionally, procurement delays occur due to periodic firmware re-certification mandates, causing administrative backlog and equipment downtime.

Wearable external defibrillators, designed for short-term patient monitoring post-discharge, are gaining traction. In 2024, 18% more hospitals incorporated wearables into cardiac risk protocols, driven by improved patient compliance rates—over 85% adherence reported in recent studies. These devices allow remote ECG monitoring and cloud data transfer, enabling outpatient care models. Commercial pilot programs in North America and Europe confirm reductions in rehospitalization and continuous monitoring needs, indicating hospitals' willingness to integrate wearables into standard care pathways.

Manufacturers face irregular supply of lithium battery cells and OLED display components, resulting in lead times extending from 8 to 16 weeks. This delays defibrillator shipments to healthcare facilities and EMS providers already operating with aging units. Simultaneously, raw material price fluctuations—especially for electronics-grade silicon—have increased unit production costs by nearly 12% year-over-year in late 2024, squeezing manufacturer margins and creating tensions in contract negotiations over price escalations.

Smart Connectivity and Analytics Integration: AEDs with IoT capabilities now transmit operational status data continuously to centralized analytics platforms. In 2024, over 60% of hospital-procured external defibrillators included cloud link features enabling real-time readiness monitoring and predictive maintenance notifications, reducing device failure incidents by 18%.

Growth in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Hospital and Pre-Hospital External Defibrillator Market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Adoption of AED Drone Delivery Pilots: Municipalities in select U.S. and European regions are launching drone-AED delivery programs. In one pilot, drones delivered AEDs to public cardiac arrest sites within 3 minutes on average—compared to the typical 7-minute EMS-driven arrival—increasing early defibrillation rates by 22%.

Surge in Wearable Defibrillator Prescriptions: Clinics and hospitals are issuing wearable defibrillators more frequently for short-term monitoring. In 2024, prescription rates rose by 25%, with data showing over 80% patient adherence and successful detection of early arrhythmia events before hospital admission.

The Hospital and Pre-Hospital External Defibrillator Market is segmented by type, application, and end-user, reflecting varied needs across clinical environments and emergency medical infrastructures. Product types encompass automated external defibrillators (AEDs), manual external defibrillators, and wearable external defibrillators. Applications span hospital-based cardiac emergency response, ambulance services, and public access defibrillation. Key end-users include hospitals, emergency medical services (EMS), clinics, and public health organizations. Automated and wearable devices are gaining traction due to their ease of use and growing adoption in field-based settings. Hospitals remain the dominant end-user, driven by institutional procurement programs and advanced integration capabilities. However, pre-hospital EMS units are increasingly influencing product development, demanding lightweight, ruggedized, and connected devices for rapid-response deployment. Each segment is defined by specific device requirements and usage protocols, which shape manufacturing priorities and regional adoption patterns. The growing emphasis on accessibility, interoperability, and real-time monitoring is reinforcing demand across all major segments.

The Hospital and Pre-Hospital External Defibrillator Market includes three main product types: automated external defibrillators (AEDs), manual external defibrillators, and wearable external defibrillators. AEDs dominate the segment, widely adopted due to their ease of use, minimal training requirements, and widespread deployment in public and EMS settings. Hospitals, airports, schools, and offices have increasingly incorporated AEDs into emergency preparedness protocols, boosting their prominence in both institutional and public health frameworks.

Wearable external defibrillators are the fastest-growing type, gaining ground in post-discharge cardiac monitoring. Their rise is attributed to their non-invasive nature, real-time ECG telemetry features, and high patient compliance. Recent improvements in compact battery life and flexible sensor systems have expanded their adoption, particularly in outpatient cardiac care and remote monitoring programs.

Manual external defibrillators, though less frequently discussed, continue to play a vital role in hospitals and specialized EMS units where trained professionals require precise control over energy levels and rhythms. Their relevance remains in critical care units and advanced life support systems, where they serve as essential life-saving tools in complex cardiac emergencies.

The primary applications within the Hospital and Pre-Hospital External Defibrillator Market are hospital-based cardiac arrest response, ambulance and emergency services, public access defibrillation, and outpatient cardiac monitoring. Hospital-based applications lead the market due to the structured nature of in-hospital code-blue protocols and well-equipped cardiac care units. Hospitals use both manual and automated devices across emergency departments, ICUs, and operating rooms, where quick response and continuous monitoring are critical.

Public access defibrillation is the fastest-growing application, driven by increasing regulations mandating AED installations in public venues such as transportation hubs, schools, and sports arenas. Public awareness campaigns and training programs are enhancing the accessibility and acceptability of defibrillator use by laypersons, significantly broadening the application landscape.

Ambulance-based and EMS applications continue to grow steadily as pre-hospital emergency systems become more sophisticated. Outpatient cardiac monitoring, supported by wearable technologies, is also emerging as a niche but important area, especially for patients recently discharged from cardiac care units or undergoing high-risk observation outside hospital settings.

Hospitals are the leading end-user in the Hospital and Pre-Hospital External Defibrillator Market, accounting for the highest unit deployment and device replacement rates. These institutions benefit from centralized procurement systems, dedicated emergency departments, and robust maintenance capabilities. Defibrillators are integral to surgical suites, intensive care units, and general wards, making them an indispensable part of hospital emergency protocols.

Emergency medical services (EMS) represent the fastest-growing end-user group. The rapid development of pre-hospital care systems, coupled with the need for lightweight, shock-resistant, and rapidly deployable AEDs, has accelerated investments in EMS fleets. Field operatives increasingly rely on real-time feedback devices and AI-driven ECG tools to guide their interventions during cardiac events.

Other end-users such as clinics, outpatient centers, and public sector organizations—including law enforcement and fire departments—contribute to the overall market by incorporating defibrillators into community health programs. Their adoption, while more distributed, reflects the broadening scope of cardiac emergency preparedness and first-responder readiness.

North America accounted for the largest market share at 41.3% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2025 and 2032.

The strong position of North America is driven by advanced healthcare infrastructure, a large installed base of AEDs, and a high level of public and institutional cardiac awareness. Meanwhile, Asia-Pacific’s acceleration is fueled by rising cardiovascular disease prevalence, increasing investments in public health infrastructure, and government-led initiatives to expand access to emergency care technology. Notably, both regions are also undergoing rapid digitization and AI integration into defibrillator systems, though APAC’s adoption is growing at a comparatively higher pace. Europe follows closely, led by countries such as Germany and France, driven by harmonized regulatory frameworks and public-access AED legislation. Emerging regions like South America and the Middle East & Africa are witnessing expanding demand supported by growing emergency response programs, though overall penetration remains relatively lower compared to developed markets.

North America commanded approximately 41.3% of the global Hospital and Pre-Hospital External Defibrillator Market in 2024, anchored by the United States and Canada. The region benefits from mature hospital infrastructure and widespread deployment of AEDs in public spaces and institutional settings. Key industries such as emergency medical services, hospitals, and schools are major drivers of defibrillator demand. Government programs—like the Public Access Defibrillation Act and EMS modernization funds—have strengthened procurement pipelines and streamlined device approvals. The region has also witnessed extensive digital transformation, with over 70% of new defibrillator models offering Wi-Fi and cloud-enabled diagnostics. Regulatory support for AI-powered AEDs and remote monitoring tools is helping North America maintain its leadership in this high-precision, life-saving equipment market.

Europe accounted for approximately 28.5% of the global Hospital and Pre-Hospital External Defibrillator Market in 2024, with Germany, the UK, and France leading regional demand. Market expansion is supported by harmonized EU health directives and increasing mandatory installation policies in public venues. Germany’s nationwide AED placement strategy and France’s defibrillator mandates for sports facilities have significantly boosted device circulation. The region is also seeing a strong push toward eco-friendly production, with compliance to RoHS and WEEE standards being integrated into manufacturing workflows. Technological advancements include real-time location-based AED apps and integration with emergency medical service dispatch systems. Europe’s commitment to public health, sustainability, and smart city innovations continues to bolster long-term adoption.

The Asia-Pacific region is emerging as the fastest-growing market and held over 16.7% of the global Hospital and Pre-Hospital External Defibrillator Market volume in 2024. China, India, and Japan are the primary demand centers, with China leading in manufacturing and Japan pioneering in device miniaturization. Investment in cardiac emergency response systems is rising, especially in urban hospitals and rural EMS fleets. Infrastructure development—like the rapid construction of tier-2 and tier-3 city hospitals—is expanding the addressable market. In addition, innovation hubs such as Singapore and South Korea are contributing to next-gen defibrillator tech, including AI-based rhythm analysis and mobile-compatible AEDs. The region’s evolving healthcare ecosystem is driving adoption in both institutional and public sectors.

Brazil and Argentina represent the key markets in South America, contributing over 7.2% to the global Hospital and Pre-Hospital External Defibrillator Market in 2024. Government-backed emergency care expansion and growing cardiac health awareness have supported consistent market development. Brazil’s health authorities have rolled out national training campaigns on AED use, increasing their prevalence in public institutions. Infrastructure improvements in public health and EMS fleets are supporting broader device deployment. Meanwhile, trade policies favoring medical equipment imports have eased market entry for global manufacturers. Technological upgrades—particularly the integration of mobile device apps with AEDs—are also gaining traction across urban centers in South America.

The Middle East & Africa region contributed approximately 6.3% to the global Hospital and Pre-Hospital External Defibrillator Market in 2024. UAE, Saudi Arabia, and South Africa are the top growth countries, driven by healthcare modernization agendas. AED demand is linked to large-scale infrastructure development, especially in airports, metro stations, and sports complexes. In the UAE, public-private partnerships are deploying smart AED kiosks in high-traffic zones. South Africa is investing in rural EMS expansion, prompting demand for rugged, portable AED units. Regulatory bodies across the region are working to standardize device certification and maintenance practices, while local manufacturers in Northern Africa are slowly entering the market via assembly and customization models.

United States – 35.1% Market Share

Strong end-user demand supported by advanced healthcare systems and high public AED coverage.

Germany – 12.6% Market Share

High production capacity and rigorous national AED deployment strategies in institutional and public sectors.

The competitive landscape in the Hospital and Pre-Hospital External Defibrillator Market is robust, featuring approximately 15 to 20 active global competitors ranging from long-established medical device manufacturers to emerging technology firms. Leading players include companies with diverse product portfolios covering hospital-grade manual defibrillators, EMS-focused automated units, and wearable devices. Market positioning varies: large legacy firms maintain dominance through extensive distribution networks and established hospital contracts, while niche innovators differentiate via portable, cloud-connected, and AI-integrated solutions.

Strategic initiatives are driving competition. Several firms have pursued partnerships with emergency medical service providers, healthcare IT platforms, and academic centers to develop responder-focused technologies. Product innovation cycles are accelerating: over the past 18 months, at least five new device launches have introduced advanced touchscreen interfaces, improved battery and pad life, and motion-resistant ECG analysis. Collaboration among manufacturers and software developers is intensifying, blending hardware design with analytics to offer predictive maintenance and remote monitoring.

Consolidation activity is underway: recent mergers and acquisitions have involved smaller technology specialists being absorbed by larger OEMs seeking to broaden their digital-forward defibrillator offerings. Innovation trends center on network‑capable AEDs, modular unit designs enabling field upgrades, and portable wearables with telemetry. Overall, the competitive environment is increasingly defined by integration with digital health ecosystems, OEMs expanding their value chains, and a clear shift toward intelligent, connected emergency response products tailored to in‑field and in‑hospital use.

Philips Healthcare

Medtronic

ZOLL Medical Corporation

Stryker (Physio-Control)

Nihon Kohden

Cardiac Science (owned by Boston Scientific)

Defibtech

CU Medical Systems

The Hospital and Pre-Hospital External Defibrillator Market is undergoing a significant technology transformation driven by connectivity, miniaturization, and smart analytics. Modern units increasingly feature integrated Wi‑Fi, Bluetooth, and LTE modules for remote monitoring and system status reporting. By 2024, approximately 65% of newly deployed hospital and EMS units included cloud-enabled diagnostics and usage tracking capabilities, enabling maintenance teams to pre-emptively address battery and pad wear issues based on live data.

Compact, wearable defibrillator systems represent another technological leap. Contemporary wearables are under 600 grams and include real-time ECG telemetry, capable of recording and uploading cardiac events to hospital portals without patient action. These units support MRI-safe materials and easily replaceable battery packs.

Artificial intelligence modules, often embedded within firmware, analyze heart rhythms continuously and trigger guided prompts for CPR or shock delivery. Some devices now calculate chest compression depth and rate, providing on-device audio-visual feedback. Advanced sensors and accelerometers enhance accuracy, reducing false positives, especially when used in ambulance settings.

Emerging technologies include modular hardware platforms allowing field-swappable battery/pad units and upgrades to AI firmware without full device replacement. Battery innovations from 2023 offer extended standby durations—up to 60% longer than previous generations—while ruggedized housing enhancements support IP67 waterproofing for challenging environments.

Looking ahead, integration with hospital information systems and EMS dispatch platforms is expanding; this enables real-time device tracking during emergency runs and better readiness analytics. Additionally, next-gen AEDs are beginning to support physiological data transmits—such as respiration rate and SpO₂ readings—enhancing monitoring capability during patient transport. These developments position the market toward smarter, leaner, and more connected emergency response tools.

In February 2023, ZOLL Medical launched a ruggedized AED model designed for helicopter EMS units; the durable shell withstands vibration levels up to 20 g and performs reliably in temperatures from –20 °C to 50 °C.

In August 2023, Philips introduced a lightweight manual defibrillator with a foldable touchscreen interface and a quick-charge battery system, achieving full charge in under 10 minutes.

In March 2024, Medtronic unveiled a wearable external defibrillator platform compatible with mobile apps, enabling ECG telemetry upload every 15 minutes during patient wear.

In November 2024, Defibtech released a new cloud-enabled AED featuring wireless firmware updates, reducing on-site service visits by 40%.

This report encompasses a wide-ranging analysis of the Hospital and Pre‑Hospital External Defibrillator Market across device types, user environments, and geographies. Coverage includes three primary technology segments—automated external defibrillators (AEDs), manual external defibrillators, and wearable defibrillators—each evaluated in terms of hardware design, connectivity features, and field utility. End‑user segments include hospital emergency departments, cardiac care units, EMS fleets (ambulance and air rescue), public-access stations, outpatient cardiac monitoring programs, and wearable-defibrillator patients.

The geographic span covers North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, capturing deployment patterns across developed healthcare systems and emerging market infrastructure. Applications studied range from in-hospital resuscitation to first-responder pre-hospital use, as well as post-discharge outpatient programs. Technology focus areas include battery systems, telemetry-enabled hardware, AI‑integrated analytics, ruggedized design, and modular upgradeability.

Additionally, neglected but growing niches such as wearable defibrillator use in remote patient monitoring and drone‑delivered AED pilots are explored. The scope includes strategic insights into procurement cycles, maintenance frameworks, digital-health integration, and service-enhancement models. Profiles of competitive landscapes, innovation pathways, and future-ready technologies appeal to operational decision-makers, procurement teams, and technical strategy planners in the emergency medical device ecosystem.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Hospital and Pre-Hospital External Defibrillator Market |

| Market Revenue (2024) | USD 360 Million |

| Market Revenue (2032) | USD 612.6 Million |

| CAGR (2025–2032) | 6.9 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Technological Insights, Market Dynamics, Segment Analysis, Regional & Country-Wise Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Philips Healthcare, Medtronic, ZOLL Medical Corporation, Stryker (Physio-Control), Nihon Kohden, Cardiac Science (owned by Boston Scientific), Defibtech, CU Medical Systems |

| Customization & Pricing | Available on Request (10 % Customization is Free) |