Reports

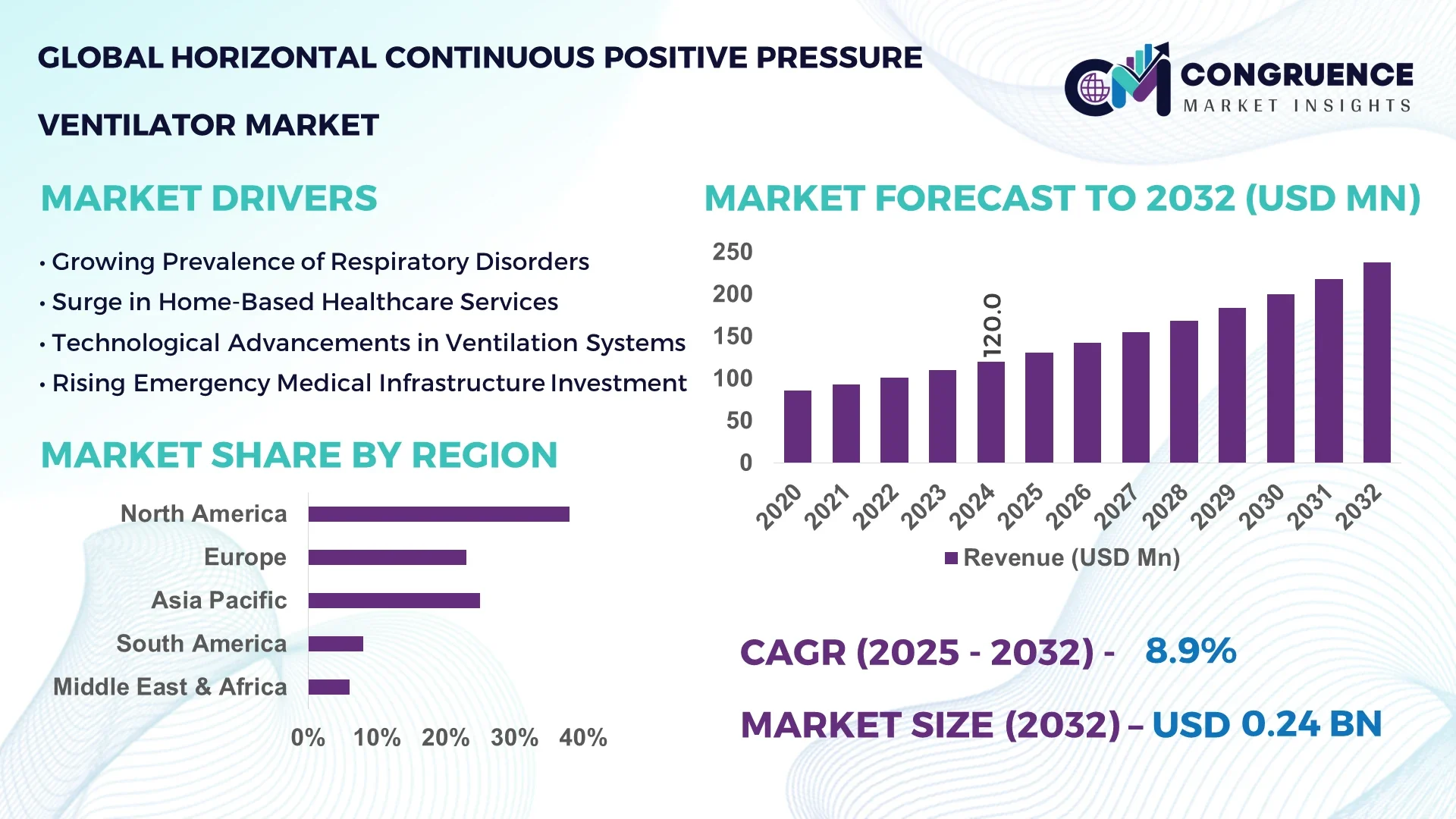

The Global Horizontal Continuous Positive Pressure Ventilator Market was valued at USD 120.0 Million in 2024 and is anticipated to reach a value of USD 237.4 Million by 2032, expanding at a CAGR of 8.9% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

In 2024, the United States led the market, accounting for over 35% of global sales, driven by its advanced critical care infrastructure, strong hospital purchasing power, and early adoption of specialized ventilator configurations. The country’s high prevalence of respiratory conditions and well-established ICU networks support robust uptake of horizontal continuous positive pressure ventilators.

Overall, demand is being fueled by expanding use in ERs, ambulatory surgery centers, and COVID‑long‑haul care clinics, where horizontal configurations are preferred for their portability and patient comfort. Moreover, manufacturers are improving interfaces and pressure cycling mechanisms to support more user‑friendly, non‑invasive ventilation workflows.

Artificial intelligence is increasingly playing a transformative role in ventilation, enhancing patient care and operational efficiency. Modern ventilators equipped with AI-driven algorithms can analyze breath-by-breath data—such as tidal volume, inspiratory flow, and airway pressure—to fine-tune support settings in real time. These systems detect patterns indicative of asynchrony, auto-adjust assist levels, and feature early alarms for potential complications like auto-PEEP or apnea events. This means patients receive tailored respiratory support with fewer manual adjustments required by clinicians.

In busy ICU environments, AI-powered ventilators help reduce clinician workload by automating adjustment protocols, allowing staff to monitor ventilation through centralized dashboards. Such platforms compile patient data across multiple devices, helping clinicians spot trends like declining lung compliance and intervene proactively. Additionally, smart ventilators support remote monitoring via hospital networks, enabling on-call respiratory therapists to supervise ventilator parameters off-site and respond to alerts immediately.

Enhanced predictive maintenance is another benefit—sensors track valve performance, motor cycles, and battery health, alerting biomedical engineers before a component approaches end-of-life. This reduces unexpected downtime in critical units. Integration with Electronic Health Records (EHR) systems ensures every ventilation parameter is logged automatically, supporting seamless data review, audit trails, and care documentation.

Such advancements elevate ventilator function from passive support tools to active participants in respiratory management, improving treatment precision and safety across hospital settings.

“In 2024, Medtronic introduced an AI‑enabled ventilator update that can recognize early signs of patient‑ventilator dyssynchrony and reduce it by up to 30%, based on pilot ICU data.”

The surge in chronic respiratory diseases—such as COPD, asthma, and post‑Covid pulmonary complications—is increasing demand for advanced ventilation technologies. Horizontal continuous positive pressure ventilators are increasingly chosen for their comfort, reduced sedation needs, and adaptability between non-invasive and invasive modes. With respiratory hospital admissions rising year-over-year, hospitals are prioritizing ventilator models that support weaning protocols, portable transport, and step-down care applications.

These ventilators typically cost 20–40% more than conventional upright units due to precision flow sensors, dual-mode protocols, and compact design. Sensitive hardware and complex pneumatics also drive up maintenance expenses. For smaller clinics and rural hospitals, budget constraints and limited biomedical engineering support create barriers. Volatile healthcare budgets and complex reimbursement systems further limit broad deployment of high-end horizontal devices.

Rising awareness of home-based long-term ventilation creates new opportunities. Compact horizontal units can be used under hospital discharge programs with remote telespirometry and analysis. Hybrid home-hospital models allow clinicians to review live ventilation data and adjust parameters remotely, reducing rehospitalizations. This creates recurring revenue channels through service subscriptions and remote monitoring packages.

These devices must comply with global standards (e.g., IEC 60601, ISO 80601), undergo rigorous clinical trials, and demonstrate safety across modes (bi-level, PSV, CPAP). Navigating approval pathways in multiple markets entails high documentation costs, long testing cycles, and variable reimbursement classifications. Delays at FDA or CE mark stages also defer product launch, increasing cash flow strain.

Shift Toward Modular Design for Flexible ICU Use: Hospitals are increasingly favoring modular ventilator systems with detachable control panels and swappable breathing circuits. This enables efficient cross-deployment between ICU pods and transport settings, reducing overall capital expenditure and inventory needs.

Rise in Cloud-Based Tele‑Ventilation Analytics: Vendors now offer platforms where ventilator data streams to secure cloud servers. Clinicians can remotely monitor airway pressures, usage patterns, and alarm trends, enabling tele‑ICU oversight from centralized command centers.

Integration of Wearable Chest Sensors: Advanced ventilator systems now sync with patient-worn chest bands that continuously measure respiratory rate, core temperature, and thoracic impedance. These wearables communicate wirelessly with the ventilator to auto-adjust support during sleep or movement.

AI‑Enhanced Breath Logging and Reporting Tools: Ventilators now generate comprehensive breath reports—detailing tidal volume variations, leak patterns, patient efforts, and asynchrony indexes. This data aids clinicians in therapy adjustment and supports insurance coding and billing compliance.

The Horizontal Continuous Positive Pressure Ventilator Market is segmented by Type, Application, and End-User. This segmentation reflects the diverse range of use cases and buying patterns across different healthcare settings. By type, ventilators are offered in Single-mode and Multi-mode configurations, catering to varied respiratory support needs. By application, the devices serve Critical Care, Post-Operative Recovery, Emergency Care, and Home Care markets. End-users include Hospitals, Ambulatory Surgical Centers (ASCs), Rehabilitation Centers, and Home Healthcare Providers. Increasing demand for versatility, portability, and AI-enhanced functions is driving product innovation across all segments. The multi-mode ventilators and critical care applications remain dominant, while the home healthcare segment is witnessing rapid growth due to the global trend towards decentralized patient management.

The Horizontal Continuous Positive Pressure Ventilator Market is segmented into Single-Mode Ventilators and Multi-Mode Ventilators.

Multi-Mode Ventilators dominate the market, contributing over 68% of total sales in 2024. Their flexibility to operate across CPAP, BiPAP, and Pressure Support Ventilation (PSV) modes makes them the preferred choice in ICUs and progressive care units. Multi-mode systems are particularly valued for managing complex respiratory failure cases where ventilation needs fluctuate rapidly.

In contrast, Single-Mode Ventilators, primarily used in home care and specific step-down hospital units, hold a smaller but stable market share. They offer simple, cost-effective solutions for patients requiring consistent positive airway pressure support.

The fastest growing segment is Multi-Mode Ventilators, driven by rising demand for adaptive therapy protocols, AI-driven mode switching, and dual-use capability for invasive and non-invasive support. Additionally, government investments in ICU capacity expansion further fuel adoption of versatile ventilator platforms across hospitals globally.

Horizontal Continuous Positive Pressure Ventilators are utilized across several clinical applications: Critical Care, Post-Operative Recovery, Emergency Care, and Home Care.

Critical Care remains the largest application segment, accounting for over 55% of the market. Ventilators in this segment must deliver highly customizable therapy, precise airflow monitoring, and superior patient comfort to manage severe respiratory distress and multi-organ failure scenarios. The focus is on minimizing sedation and promoting weaning.

Post-Operative Recovery is an established segment, where ventilators are used to stabilize respiratory function after major surgeries. Emergency Care applications are growing, as hospitals equip ERs with flexible, mobile ventilators for trauma and acute care cases.

The fastest growing segment is Home Care, driven by increasing prevalence of chronic respiratory conditions like COPD and post-COVID lung fibrosis. Advanced portable ventilators with cloud connectivity enable remote monitoring and therapy adjustments, allowing patients to be safely managed at home while reducing hospital readmissions.

The end-user landscape for Horizontal Continuous Positive Pressure Ventilators includes Hospitals, Ambulatory Surgical Centers (ASCs), Rehabilitation Centers, and Home Healthcare Providers.

Hospitals lead the market, representing more than 60% of global demand. Large acute care hospitals and tertiary ICUs invest heavily in premium multi-mode ventilators to enhance patient outcomes and streamline ventilation management across different care levels. Ventilators are now being deployed not only in ICUs but also in emergency rooms, operating rooms, and step-down units.

Ambulatory Surgical Centers are a niche but growing segment, driven by outpatient surgical volume expansion and the need for post-anesthesia ventilatory support. Rehabilitation Centers use horizontal ventilators to manage patients undergoing long-term recovery from trauma or neurological impairment.

Home Healthcare Providers represent the fastest growing end-user segment, thanks to advances in compact ventilator design, battery life, and remote monitoring capabilities. This shift supports healthcare system efforts to improve patient quality of life while controlling hospital costs and optimizing resource allocation.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.4% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

This regional dynamic is driven by mature healthcare infrastructure and strong reimbursement policies in North America, contrasted by rising healthcare investments and expanding access in Asia-Pacific. Europe maintains a solid position supported by progressive healthcare policies, while South America and Middle East & Africa are witnessing gradual adoption influenced by increasing awareness and international aid-driven healthcare programs. Each region presents unique demand drivers such as demographic trends, prevalence of respiratory diseases, and technological adoption.

Widespread Integration of AI-Driven Ventilator Platforms

North America leads the global Horizontal Continuous Positive Pressure Ventilator market, accounting for USD 45.6 Million in 2024. The region benefits from an advanced hospital infrastructure, high per capita healthcare spending, and well-established reimbursement pathways. Leading U.S. hospitals are rapidly integrating AI-powered ventilators to improve patient outcomes and optimize weaning protocols. Canada’s strong focus on aging population care is also driving demand for home-based ventilator solutions. Furthermore, collaborations between healthcare providers and MedTech companies have accelerated the deployment of portable and connected ventilator systems in rural and telehealth settings, supporting decentralized respiratory care.

Focus on Sustainable and Energy-Efficient Ventilator Technologies

Europe’s Horizontal Continuous Positive Pressure Ventilator market reached approximately USD 32.4 Million in 2024. The region is witnessing a growing trend toward sustainable medical device innovation, spurred by EU directives on green healthcare. Germany, France, and the U.K. are at the forefront, investing in energy-efficient ventilators with longer battery life and recyclable components. Additionally, the increasing incidence of sleep apnea and chronic respiratory conditions among the elderly population is fueling demand for both hospital-grade and home-use ventilators. The European market also benefits from high clinical awareness and robust government support for remote patient management solutions.

Rapid Expansion of Healthcare Infrastructure Driving Ventilator Demand

Asia-Pacific is the fastest-growing region, generating USD 28.8 Million in 2024. Massive healthcare infrastructure investments in China and India are driving demand for advanced ventilators across public and private sectors. Governments are allocating significant budgets toward ICU upgrades and expanding respiratory care capacity following lessons from the COVID-19 pandemic. Moreover, rising prevalence of COPD and sleep-disordered breathing, combined with growing health insurance coverage, is boosting sales of home-care ventilators. Japanese and South Korean manufacturers are innovating compact, IoT-enabled ventilators to meet the rising demand for portable respiratory support devices in the region.

Government Initiatives Catalyzing Adoption in Public Hospitals

South America’s Horizontal Continuous Positive Pressure Ventilator market stood at USD 7.2 Million in 2024. Brazil and Argentina are leading the regional demand, supported by government programs aimed at modernizing public hospital equipment. Increased procurement of horizontal ventilators for regional ICUs and emergency care units is helping to address the high burden of respiratory infections and chronic lung diseases in underserved populations. Additionally, rising medical tourism and expansion of private healthcare facilities are contributing to market growth. Manufacturers are entering into public-private partnerships to enhance ventilator availability across key urban centers.

Strategic Investments in ICU Ventilator Capacity Post-Pandemic

The Middle East & Africa market generated approximately USD 6.0 Million in 2024. The post-pandemic recovery has prompted countries like Saudi Arabia and the UAE to significantly invest in upgrading their ICU ventilator capacity. There is also growing demand for portable, battery-operated horizontal ventilators in regions with limited healthcare infrastructure. In Africa, donor-driven healthcare programs are facilitating ventilator adoption in public hospitals to combat a high prevalence of respiratory infections. Additionally, the market is benefiting from training programs aimed at increasing the clinical workforce’s familiarity with advanced ventilation technologies.

United States – With Market size of USD 41.2 Million, it's strong demand is driven by advanced ICU infrastructure, AI integration, and rising prevalence of chronic respiratory conditions.

Germany – With Market size of USD 14.8 Million has high healthcare spending, proactive government support for sustainable medical devices, and robust adoption of home-based ventilation solutions.

The Horizontal Continuous Positive Pressure Ventilator market is moderately fragmented, with several global and regional players competing on innovation, product reliability, and clinical performance. Major manufacturers are prioritizing technological advancements such as AI-driven ventilation modes, enhanced user interfaces, and integration with digital health platforms. Companies are also investing in portable and wearable ventilator models to address growing demand for home healthcare applications. The U.S., Germany, and Japan are the key innovation hubs driving the competitive landscape.

Strategic partnerships between medical device manufacturers and hospital networks are becoming common to drive adoption of advanced ventilator systems. Additionally, public health initiatives in emerging markets are creating new opportunities for global players. Product differentiation based on comfort, noise reduction, battery life, and seamless data integration is a key focus area. The market is witnessing continuous product launches as companies strive to cater to a wide range of patients, from ICU care to long-term home ventilation needs.

Philips Healthcare

ResMed Inc.

Drägerwerk AG & Co. KGaA

Hamilton Medical AG

Vyaire Medical Inc.

Fisher & Paykel Healthcare Corporation Limited

Getinge AB

Nihon Kohden Corporation

Smiths Medical

Air Liquide Medical Systems

Technological innovation is reshaping the Horizontal Continuous Positive Pressure Ventilator market. AI and machine learning are playing a pivotal role in optimizing ventilation modes, improving patient outcomes, and enhancing user-friendliness. Modern ventilators now incorporate predictive analytics that adjust airflow and pressure in real time based on patient respiratory patterns, thereby reducing lung injury risks.

Integration with IoT platforms allows healthcare providers to remotely monitor ventilator performance and patient data, enabling more proactive clinical interventions. Portable ventilator models are increasingly equipped with advanced battery technology, offering up to 24 hours of uninterrupted use, a key factor for home-care and transport applications.

User-centric design improvements, such as intuitive touchscreen interfaces and automatic leak compensation, are enhancing both patient comfort and clinical efficiency. Furthermore, innovations in materials—such as antimicrobial coatings and lightweight components—are improving safety and usability. With increasing demand for telehealth-enabled respiratory care, the market is witnessing rapid adoption of connected ventilators that support data-driven personalized therapy.

In May 2024, ResMed launched its new AirSense™ 11 CPAP device in Europe, featuring an integrated personal therapy assistant and remote patient monitoring capabilities to enhance adherence and patient experience.

In February 2024, Philips introduced the DreamStation 2 Auto CPAP Advanced in several Asia-Pacific markets, incorporating enhanced comfort features and cloud-connected data analytics for home-based respiratory care.

In November 2023, Drägerwerk AG unveiled the Oxylog® 3000 Plus, a portable emergency ventilator with horizontal CPAP functionality, designed to deliver optimal respiratory support during prehospital and intra-hospital transport.

In July 2023, Fisher & Paykel Healthcare expanded its SleepStyle™ CPAP range with the addition of advanced humidity control and Bluetooth connectivity to improve long-term patient outcomes and enable seamless clinician-patient interaction.

The Horizontal Continuous Positive Pressure Ventilator market report offers an in-depth analysis of global market dynamics, covering technological advancements, regulatory trends, and shifting clinical needs. The report examines how key factors such as rising prevalence of chronic respiratory diseases, post-pandemic demand for advanced ventilator systems, and increasing emphasis on home healthcare are driving market growth.

It provides comprehensive segmentation by type, application, and end-user, highlighting regional variations in adoption patterns. The report also explores competitive strategies, recent product innovations, and the role of emerging technologies such as AI and IoT in shaping future market landscapes.

In addition to evaluating the performance of key players, the report offers actionable insights into market entry opportunities and challenges. It serves as a valuable resource for medical device manufacturers, healthcare providers, investors, and policymakers seeking to navigate this evolving market. The scope encompasses both hospital-based and home-based care settings, with particular focus on innovations aimed at improving patient safety, comfort, and treatment outcomes.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Horizontal Continuous Positive Pressure Ventilator Market |

| Market Revenue (2024) | USD 120.0 Million |

| Market Revenue (2032) | USD 237.4 Million |

| CAGR (2025–2032) | 8.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Philips Healthcare, ResMed Inc., Drägerwerk AG & Co. KGaA, Hamilton Medical AG, Vyaire Medical Inc., Fisher & Paykel Healthcare Corporation Limited, Getinge AB, Nihon Kohden Corporation, Smiths Medical, Air Liquide Medical Systems |

| Customization & Pricing | Available on Request (10% Customization is Free) |