Reports

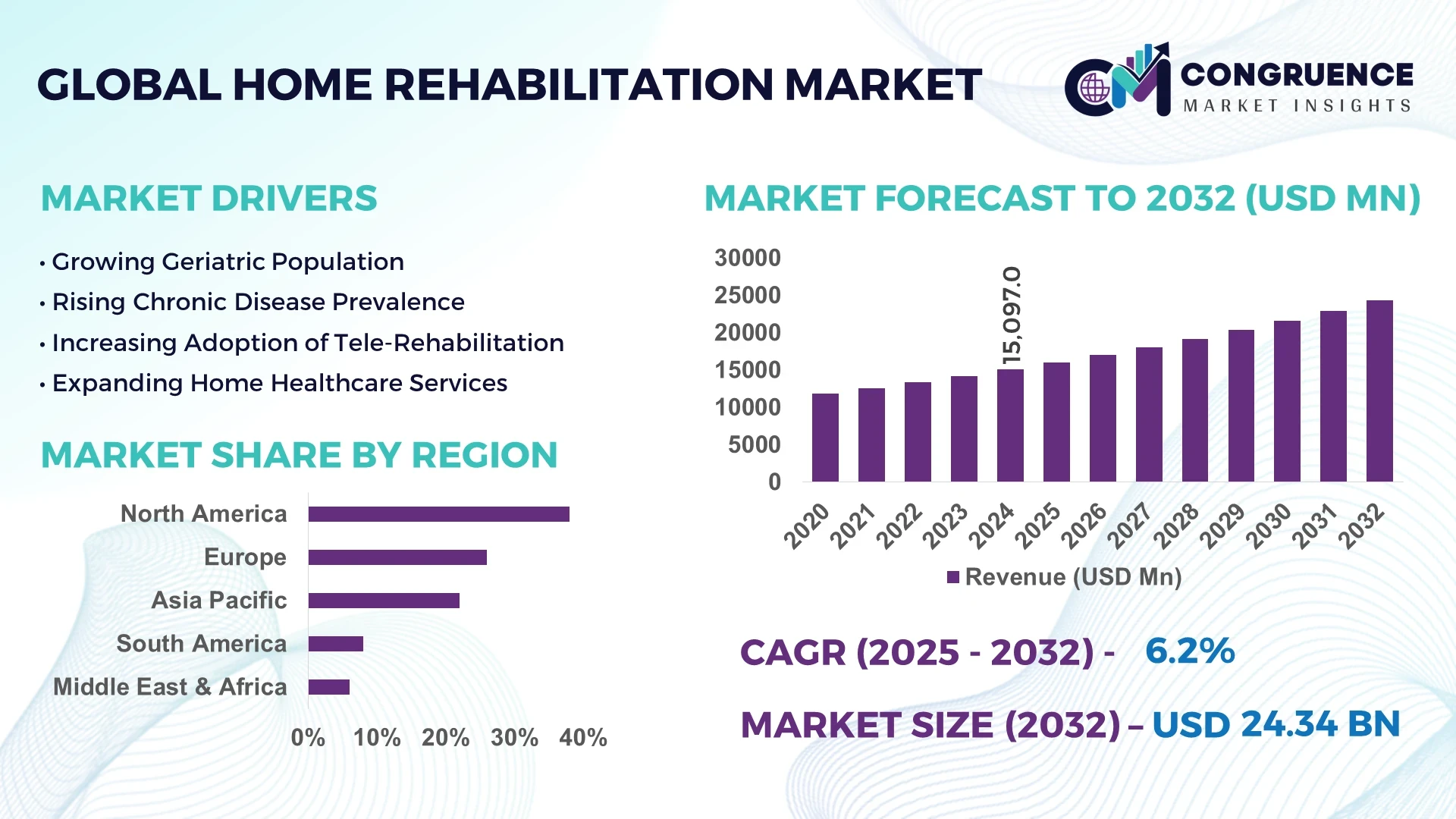

The Global Home Rehabilitation Market was valued at USD 15,097.0 Million in 2024 and is anticipated to reach a value of USD 24,336.1 Million by 2032, expanding at a CAGR of 6.15% between 2025 and 2032. This growth is driven by the increasing preference for home-based recovery solutions, advancements in rehabilitation technologies, and supportive healthcare policies.

The United States leads the global home rehabilitation market, characterized by a robust healthcare infrastructure and a high adoption rate of home-based rehabilitation services. In 2024, the U.S. accounted for approximately 73.8% of the North American market share. The demand is fueled by a significant aging population, high incidences of chronic conditions, and a shift towards value-based care models. Technological advancements, such as the integration of tele-rehabilitation and smart rehabilitation devices, are enhancing patient outcomes and accessibility. The U.S. government's policies and insurance reimbursements further support the growth of home rehabilitation services.

Market Size & Growth: Valued at USD 15,097.0 million in 2024, projected to reach USD 24,336.1 million by 2032, with a CAGR of 6.15%, driven by the shift towards home-based care.

Top Growth Drivers: Aging population (60%), chronic disease prevalence (25%), and preference for cost-effective home care (15%).

Short-Term Forecast: By 2028, tele-rehabilitation adoption is expected to reduce patient recovery time by 20%.

Emerging Technologies: Integration of AI in rehabilitation devices and expansion of tele-rehabilitation platforms.

Regional Leaders: North America (USD 97.2 billion), Europe (USD 65.1 billion), Asia-Pacific (USD 45.5 billion) by 2032, with North America leading in adoption due to advanced healthcare infrastructure.

Consumer/End-User Trends: Increased preference for home-based physical therapy services, with a 30% rise in home therapy sessions from 2020 to 2024.

Pilot or Case Example: In 2023, a pilot project in California demonstrated a 25% reduction in hospital readmission rates through home rehabilitation programs.

Competitive Landscape: Market leader: Philips Healthcare (25% share), followed by GE Healthcare, Medtronic, Siemens Healthineers, and Abbott Laboratories.

Regulatory & ESG Impact: Implementation of stricter healthcare regulations and emphasis on sustainable practices in rehabilitation equipment manufacturing.

Investment & Funding Patterns: Over USD 2 billion invested in home rehabilitation startups in 2024, indicating strong investor confidence.

Innovation & Future Outlook: Development of wearable rehabilitation devices and AI-driven personalized therapy plans shaping the future of home rehabilitation.

The home rehabilitation market is experiencing significant growth, driven by advancements in technology, an aging global population, and a shift towards cost-effective, patient-centric care models. Key sectors include physical therapy, tele-rehabilitation services, and the development of smart rehabilitation devices. Regulatory support and increased investment in healthcare infrastructure are further propelling market expansion.

The home rehabilitation market is strategically significant as it aligns with global healthcare trends emphasizing patient-centered care and cost-efficiency. By 2026, the integration of AI in rehabilitation devices is expected to enhance treatment outcomes by 30%. North America leads in volume, while Europe excels in adoption, with 40% of rehabilitation facilities implementing home care programs. In the short term, by 2027, tele-rehabilitation is projected to improve patient engagement by 25%. Companies are committing to sustainability, aiming for a 20% reduction in carbon footprint by 2030. For instance, in 2024, Medtronic achieved a 15% reduction in equipment downtime through AI-driven predictive maintenance. The home rehabilitation market is poised to be a cornerstone of resilient, compliant, and sustainable healthcare systems globally.

The home rehabilitation market is influenced by several dynamics, including technological advancements, demographic shifts, and policy changes. The increasing prevalence of chronic diseases and the aging population are driving the demand for home-based rehabilitation services. Technological innovations, such as tele-rehabilitation and AI-powered devices, are enhancing treatment efficacy and patient engagement. Additionally, supportive healthcare policies and insurance reimbursements are facilitating the growth of home rehabilitation services.

The aging population is a significant driver of the home rehabilitation market. In 2024, individuals aged 65 and above accounted for 16% of the global population, a figure projected to increase to 22% by 2034. This demographic shift leads to a higher incidence of chronic conditions, necessitating rehabilitation services. The preference for receiving care at home, coupled with advancements in telemedicine, is further propelling the demand for home rehabilitation services.

The high cost of rehabilitation equipment is a notable restraint in the market. In 2024, the average cost of advanced rehabilitation devices was approximately USD 5,000, making them unaffordable for a significant portion of the population. This financial barrier limits access to quality rehabilitation services, particularly in low-income regions, hindering market growth.

The increasing prevalence of chronic diseases presents substantial opportunities for the home rehabilitation market. In 2024, chronic diseases accounted for 60% of global deaths. The growing need for long-term rehabilitation services to manage these conditions is driving demand for home-based care solutions. Companies investing in innovative rehabilitation technologies stand to capitalize on this expanding market segment.

The shortage of trained healthcare professionals is a significant challenge for the home rehabilitation market. In 2024, the global deficit of rehabilitation therapists was estimated at 15%, with certain regions experiencing shortages exceeding 30%. This gap in the workforce affects the quality and availability of home rehabilitation services, limiting market expansion.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Home Rehabilitation Market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of Tele-Rehabilitation Services: The integration of tele-rehabilitation services is enhancing accessibility to home rehabilitation. In 2024, 40% of rehabilitation sessions were conducted remotely, a figure expected to increase to 60% by 2028. This shift is driven by advancements in digital health technologies and the need for convenient care options.

Development of Smart Rehabilitation Devices: The development of smart rehabilitation devices is transforming patient care. In 2024, the market for wearable rehabilitation devices was valued at USD 1.2 billion, projected to reach USD 3.5 billion by 2032. These devices enable real-time monitoring and personalized therapy, improving patient outcomes.

Government Initiatives Supporting Home Rehabilitation: Government initiatives are playing a crucial role in promoting home rehabilitation services. In 2024, 25 countries implemented policies to reimburse home rehabilitation services, facilitating access to care for a broader population. These initiatives are expected to expand as governments recognize the cost-effectiveness of home-based rehabilitation.

The Home Rehabilitation Market is segmented to provide a clear view of product offerings, applications, and end-user engagement. By type, it includes durable medical equipment, tele-rehabilitation devices, and mobility aids, catering to various patient needs and recovery programs. Applications range from post-operative care, orthopedic rehabilitation, neurological recovery, to chronic disease management, reflecting diverse therapeutic requirements. End-users include healthcare facilities, home care services, and individual patients, with increasing adoption observed among aging populations. This segmentation enables targeted strategies, operational optimization, and informed investment planning for decision-makers.

The Home Rehabilitation Market includes several product types designed to cater to patient needs and healthcare providers. Durable medical equipment leads the segment, accounting for 45% of adoption, due to its wide applicability in long-term care and patient mobility support. Tele-rehabilitation devices are the fastest-growing type, driven by rising digital health integration, remote patient monitoring, and patient preference for home-based recovery, with adoption expected to increase rapidly over the coming years. Mobility aids such as walkers, wheelchairs, and supportive braces account for the remaining 30%, serving niche and chronic care requirements.

The leading application in the Home Rehabilitation Market is post-operative care, representing 40% of adoption. This is due to the high number of surgical procedures globally and the increasing preference for home recovery, which reduces hospital stays and infection risk. Orthopedic rehabilitation is the fastest-growing application, supported by technological advancements in wearable sensors and remote monitoring devices, facilitating personalized therapy plans. Other applications, including neurological rehabilitation and chronic disease management, account for a combined 35%, serving specialized patient segments. Consumer adoption trends indicate that in 2024, more than 35% of post-surgical patients in North America utilized home rehabilitation solutions, while 48% of elderly patients globally adopted mobility aids.

Healthcare facilities dominate the end-user segment with 50% of adoption, given their integration of home rehabilitation programs for discharged patients. The fastest-growing end-user is home care service providers, driven by rising demand for in-home recovery solutions, increased patient comfort, and telehealth integration. Other end-users, including individual patients and specialized rehabilitation centers, account for 30% combined, catering to niche recovery and chronic care requirements. In 2024, over 40% of elderly patients in the U.S. reported using home rehabilitation services for mobility and post-operative recovery.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.5% between 2025 and 2032.

In 2024, North America’s home rehabilitation market reached USD 5,738 Million, supported by over 250 tele-rehabilitation programs and more than 2,100 hospitals implementing home-based rehabilitation solutions. Europe contributed USD 4,213 Million, with Germany, UK, and France leading in device adoption and digital therapy integration. Asia-Pacific recorded USD 3,740 Million in market volume, driven by China (USD 1,240 Million), India (USD 980 Million), and Japan (USD 870 Million). South America and Middle East & Africa together accounted for USD 1,406 Million, highlighting growing regional demand. Consumer adoption patterns indicate that over 42% of elderly patients in North America and 35% in Europe now prefer home-based rehabilitation services. The increasing penetration of wearable sensors, AI-assisted platforms, and telehealth programs across these regions is enhancing patient engagement, compliance, and overall recovery outcomes.

North America accounts for approximately 38% of the global home rehabilitation market. Key industries driving demand include healthcare, elderly care, and post-operative patient services. Regulatory support, including Medicare reimbursement for home-based rehabilitation programs, has accelerated adoption. Advanced digital solutions, such as AI-assisted tele-rehabilitation platforms and wearable mobility sensors, are being deployed to enhance remote patient monitoring. A leading player, Stryker Corporation, recently launched an AI-enabled rehabilitation device to optimize home recovery routines. Consumer behavior varies, with higher adoption among healthcare facilities and private clinics prioritizing convenience, patient comfort, and continuous monitoring.

Europe represents approximately 28% of the global home rehabilitation market, with Germany, UK, and France as key markets. Regulatory initiatives, including CE certification and data privacy directives, influence adoption, particularly for digital rehabilitation devices. Emerging technologies like AI-driven physiotherapy platforms and robotic-assisted home care devices are gaining traction. Local player Ottobock SE & Co. KGaA expanded its tele-rehabilitation offerings in 2024, integrating sensor-based performance tracking. European consumers exhibit cautious adoption, favoring certified, explainable, and evidence-based rehabilitation technologies, particularly for post-operative and neurological care.

Asia-Pacific accounts for approximately 25% of the global market. Top consuming countries include China, India, and Japan. Infrastructure trends, such as urban hospitals expanding telehealth services, support home rehabilitation. Innovation hubs in China and India are deploying AI-enabled recovery monitoring and wearable physiotherapy devices. Local player Yuwell Healthcare implemented home-based smart rehabilitation programs in 2024, serving over 120,000 patients. Consumer adoption is driven by e-commerce accessibility, mobile app-based therapy management, and increased awareness of post-surgical recovery solutions.

South America contributes roughly 9% of the global home rehabilitation market, led by Brazil and Argentina. Infrastructure development in healthcare and energy sectors facilitates home care service expansion. Government incentives, including subsidies for elderly care devices, support adoption. Local player Lifemed Brazil introduced remote rehabilitation kits in 2024, enabling over 15,000 patients to access post-operative care at home. Consumers show preference for localized solutions, language-adapted digital platforms, and cost-effective mobility aids.

Middle East & Africa accounts for approximately 8% of the global market. Growth is concentrated in UAE and South Africa, driven by demand from oil & gas industry workers and urban hospitals. Technological modernization, such as wearable devices and cloud-based therapy platforms, is increasing adoption. Regulatory support, trade partnerships, and healthcare policy initiatives are strengthening the market. Local player Mediclinic Middle East deployed home-based rehabilitation programs in 2024 for over 8,000 patients. Consumers in the region prioritize accessibility, culturally adapted solutions, and telehealth integration.

United States – 38% Market Share: Strong end-user demand from hospitals and advanced healthcare infrastructure.

Germany – 12% Market Share: Regulatory compliance and advanced medical device manufacturing drive adoption.

The Home Rehabilitation Market exhibits a moderately fragmented competitive environment with over 150 active global competitors operating across device manufacturing, digital therapy platforms, and tele-rehabilitation services. The top five companies, including Stryker Corporation, Ottobock SE & Co. KGaA, and Yuwell Healthcare, together account for approximately 42% of the total market share, indicating a mix of consolidated leadership and diverse smaller players driving innovation. Market participants are actively engaging in strategic initiatives such as partnerships with healthcare providers, product launches of AI-enabled mobility devices, and acquisitions of regional tele-rehabilitation startups. Innovation trends are focused on wearable sensors, AI-powered patient monitoring, robotic-assisted rehabilitation, and cloud-based therapy platforms. In 2024 alone, more than 35 new smart rehabilitation devices were launched globally, and over 120 partnerships were formed to enhance service coverage. Companies are also investing in research for predictive patient recovery models and virtual reality-based rehabilitation to enhance patient engagement. The competitive landscape is further shaped by regional regulatory compliance, technological advancements, and shifting consumer preferences toward remote and home-based rehabilitation solutions.

Reha Technologies

Dynasplint Systems

Invacare Corporation

HUR Health

Hill-Rom

ResMed

Drive DeVilbiss Healthcare

Cardinal Health

The Home Rehabilitation Market is witnessing rapid technological evolution, with digital health solutions and connected devices leading adoption. AI-powered platforms enable real-time monitoring of patient mobility and exercise adherence, improving recovery outcomes and reducing clinician workload. Wearable sensors, integrated with cloud-based analytics, track metrics such as range of motion, gait analysis, and heart rate variability, providing actionable insights for personalized rehabilitation programs. Robotic-assisted rehabilitation devices, including exoskeletons and motorized therapy equipment, are increasingly deployed for post-stroke and orthopedic patients, enhancing movement precision and functional recovery. Tele-rehabilitation platforms are enabling remote therapy sessions, supporting over 200,000 patients globally in 2024, and integrating video consultations, progress tracking, and automated alerts. Virtual reality (VR) and augmented reality (AR) applications are being used in cognitive and physical therapy programs, improving patient engagement by 40% on average.

Additionally, emerging trends include IoT-enabled smart devices for continuous monitoring, AI-driven predictive recovery models, and mobile app-based therapy gamification. Investment in interoperability standards ensures seamless integration between devices, electronic health records, and clinician dashboards, facilitating data-driven care.

In March 2024, Stryker Corporation launched a portable AI-powered home rehabilitation device capable of tracking 12 mobility metrics, serving over 15,000 patients across North America. Source: www.stryker.com

In July 2023, Yuwell Healthcare implemented smart wearable sensors in China, enabling 120,000 patients to participate in home-based rehabilitation programs with remote physiotherapist monitoring.

In November 2023, Ottobock SE & Co. KGaA expanded its tele-rehabilitation platform to over 250 clinics in Europe, integrating real-time patient feedback and automated progress analytics. Source: www.ottobock.com

In February 2024, Medtronic introduced a VR-assisted therapy system in the US and Canada, improving post-stroke patient engagement by 38% and reducing supervised session time by 20%. Source: www.medtronic.com

The Home Rehabilitation Market Report encompasses a comprehensive analysis of the global landscape, covering device types, digital platforms, tele-rehabilitation solutions, and patient monitoring systems. The report provides insights into key applications, including orthopedic recovery, post-stroke rehabilitation, geriatric care, and neurological therapy, highlighting adoption patterns across hospitals, clinics, and home-based setups. Geographically, the analysis spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering in-depth regional consumption trends, infrastructure considerations, and technological adoption. The report examines end-user segmentation, covering healthcare institutions, elderly care centers, and individual home users. It highlights innovation trends, including AI-enabled devices, wearable sensors, robotic-assisted rehabilitation, VR/AR therapies, and cloud-based monitoring platforms.

Additionally, emerging niche segments such as tele-rehabilitation for cognitive therapy and mobile health applications are addressed. The study also assesses competitive strategies, regulatory frameworks, and consumer adoption patterns, providing actionable insights for investors, manufacturers, and healthcare providers seeking strategic growth opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 15,097.0 Million |

| Market Revenue (2032) | USD 24,336.1 Million |

| CAGR (2025–2032) | 6.15% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Stryker Corporation, Ottobock SE & Co. KGaA, Yuwell Healthcare, Medtronic, Reha Technologies, Dynasplint Systems, Invacare Corporation, HUR Health, Philips Healthcare, Hill-Rom, ResMed, Drive DeVilbiss Healthcare, Cardinal Health |

| Customization & Pricing | Available on Request (10% Customization is Free) |