Reports

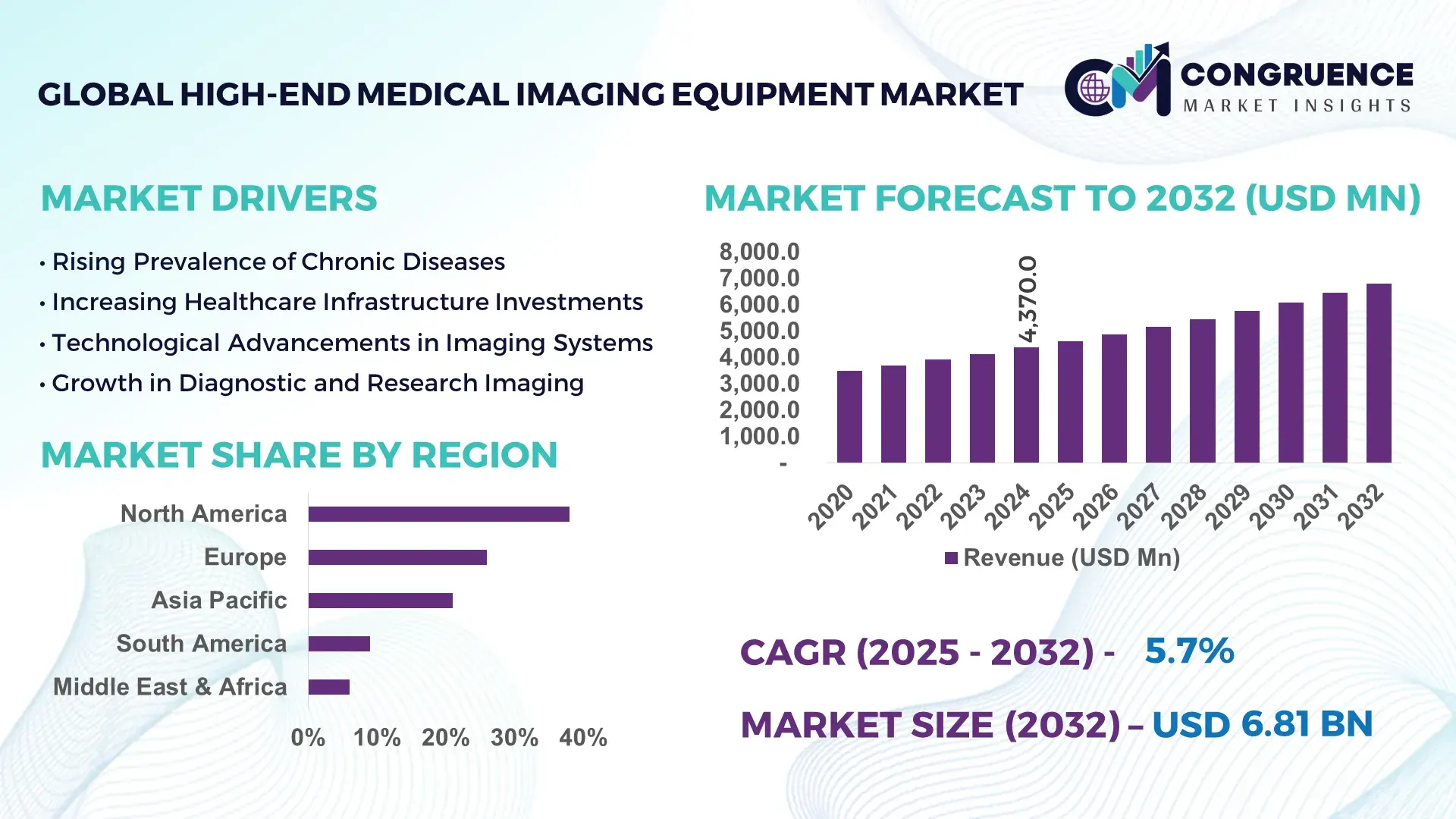

The Global High‑end Medical Imaging Equipment Market was valued at USD 4,370.0 Million in 2024 and is anticipated to reach a value of USD 6,809.0 Million by 2032, expanding at a CAGR of 5.7% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is primarily fueled by rapid technological innovation and rising demand for advanced diagnostic solutions.

In the United States, the high‑end medical imaging equipment sector is particularly mature: it boasts one of the largest production capacities globally, with leading manufacturers heavily investing in R&D for hybrid imaging systems (such as PET/MRI) and high‑field MRI. The country sees annual capital expenditures in imaging infrastructure exceeding USD 3 billion, and over 60% of large hospital systems integrate AI‑assisted platforms to improve throughput. Key applications include oncology diagnostics, neurology, and cardiac imaging, where technological advancements are driving higher image resolution and faster scan times.

Market Size & Growth: Valued at USD 4,370 Million in 2024, projected to reach USD 6,809 Million by 2032; CAGR of 5.7%, driven by increasing adoption of AI enhancements and hybrid imaging systems.

Top Growth Drivers: Advanced imaging adoption (45%), AI‑assisted diagnostics (30%), infrastructure upgrades (25%).

Short‑Term Forecast: By 2028, deployment of AI-enabled imaging platforms is expected to boost throughput by ~20%.

Emerging Technologies: Hybrid PET/MRI systems, ultra-high-field MRI (>7T), and AI‑driven reconstruction algorithms.

Regional Leaders: North America (~USD 2,300 M by 2032) with mature hospital networks, Europe (~USD 1,500 M) with strong regulatory support, and Asia-Pacific (~USD 1,000 M) driven by fast healthcare infrastructure expansion.

Consumer/End‑User Trends: Large hospitals and cancer-care centers increasingly invest in high-end scanners; diagnostic imaging chains are adopting modular, scalable systems.

Pilot Example: In 2026, a U.S. academic hospital implemented a 7‑Tesla MRI, reducing scan time by 25% and increasing diagnostic throughput by 15%.

Competitive Landscape: Market leader with ~35% share — GE Healthcare, followed by Siemens Healthineers, Philips, Canon Medical, and Hitachi.

Regulatory & ESG Impact: Stricter radiation-dose regulations, push for energy‑efficient imaging machines, and incentives for low‑dose AI‑optimized systems.

Investment & Funding Patterns: Over USD 500 Million in recent venture funding, especially for AI-based start-ups and next-gen portable high-field devices.

Innovation & Future Outlook: Growing focus on AI-assisted diagnostics, tele‑imaging, and integrated hybrid systems; long-term trend toward personalized imaging protocols and low-dose technologies.

High‑end medical imaging equipment is seeing rapid adoption in oncology, neurology, and cardiology, driven by advances in hybrid imaging and AI reconstruction. Regulatory push for radiation safety, combined with rising demand in emerging markets, supports further growth. Add to this energy-efficiency goals and scalable modular systems, and the future looks increasingly innovation‑centric and sustainability-aligned.

The high‑end medical imaging equipment market holds strategic relevance as a cornerstone for advanced diagnostics and precision medicine. Hospitals and cancer centers are increasingly relying on high‑field MRI and hybrid PET/MRI systems, which can deliver up to 30% higher diagnostic accuracy compared to older 1.5T scanners. This improvement enables better detection of small tumors, neurological lesions, and cardiac anomalies. In volume, North America dominates, while Asia-Pacific leads in adoption: over 40% of new imaging installations in 2025 came from emerging markets there.

Over the next 2–3 years, we expect AI‑driven reconstruction and image enhancement to cut scan times by up to 20%, significantly improving patient throughput and reducing operational costs. At the same time, firms are committing to sustainability, targeting a 15% reduction in power consumption of imaging devices by 2030 through the use of energy-efficient magnet designs and smarter cooling systems.

In micro‑scenario terms, in 2026, a leading U.S. hospital leveraged deep-learning reconstruction on its 7T MRI, achieving a 25% reduction in scan duration while maintaining diagnostic fidelity. Such advances not only lower costs per scan but also reduce patient burden and increase scanner utilization.

Looking ahead, the high-end imaging market is poised to become a pillar of resilience, compliance, and sustainable growth, offering both clinical precision and operational efficiency.

The High‑end Medical Imaging Equipment Market is experiencing strong momentum due to the convergence of technological innovation, demographic pressures, and evolving clinical needs. As chronic diseases—including cancer and neurological disorders—rise globally, demand for advanced imaging modalities such as high-field MRI, PET, and hybrid systems is increasing. Simultaneously, hospitals and imaging centers are under pressure to increase throughput, reduce cost per scan, and deliver better patient outcomes, pushing them to adopt AI-based reconstruction and image acquisition technologies. At the same time, healthcare regulators are driving improvements in safety – enforcing lower radiation doses and incentivizing energy-efficient machines. On the supply side, manufacturers are scaling up production, investing in R&D, and collaborating with AI firms and academic institutions. All this is creating a dynamic growth landscape, but market penetration is constrained by the high capital cost of top-tier systems, reimbursement challenges, and the need for highly skilled operators.

There is rising global demand for highly accurate diagnostic tools, particularly in oncology and neurology, which is pushing hospitals to adopt high-end imaging systems. High-field MRI (e.g., 3T and above) and PET/MRI deliver enhanced spatial resolution and functional insights, enabling early detection of tumors and precise characterization of neurological diseases. The increasing prevalence of chronic illnesses, along with the shift toward precision medicine, is motivating healthcare providers to invest in these high-performance machines. In addition, AI-based reconstruction algorithms allow faster image acquisition and better image quality, which further supports adoption of advanced imaging platforms.

High-end imaging systems such as 7T MRI or PET/MRI require significant upfront capital outlay—not only for the scanner itself but also for infrastructure like reinforced floors, cryogen systems, and shielding. Operating these machines also demands specialized workforce—trained technologists and radiologists—as well as ongoing maintenance and calibration, which can be cost-prohibitive for many smaller hospitals or diagnostic centers. Moreover, in certain markets, reimbursement policies lag behind the clinical value offered by these advanced systems, making it financially risky for providers to justify the investment solely on throughput or standard diagnostic volume.

AI-powered reconstruction and image enhancement can reduce scan times and improve image clarity, making high-end systems more efficient and cost-effective. Hybrid imaging systems (e.g., PET/MRI) enable simultaneous anatomical and functional imaging, offering richer clinical data for oncology, neurology, and cardiology. This opens opportunities for personalized diagnostics and therapy planning. In emerging markets, as healthcare infrastructure improves and reimbursement frameworks evolve, providers are increasingly willing to invest in these advanced modalities. There is also scope for modular, scalable high‑end machines, which can be upgraded with software (AI, new sequences) rather than fully replaced, reducing the total cost of ownership.

High-end imaging devices operate under strict regulatory frameworks due to concerns around radiation exposure (for PET) and magnetic field safety (for high‑field MRI). Manufacturers must comply with rigorous safety standards (e.g., IEC, FDA) and validate new technologies (like AI reconstruction) for clinical use, which can delay time-to-market. Furthermore, stringent energy-consumption and environmental regulations push companies to redesign hardware, which raises costs. The need for robust clinical validation and alignment with reimbursement policies in different geographies further complicates the adoption of next-gen systems.

Modular Hybrid Imaging Adoption: In 2025, approximately 38% of new high‑end imaging installations globally were hybrid systems (e.g., PET/MRI), reflecting clinician demand for combined functional and anatomical imaging.

AI‑Driven Reconstruction: Over 45% of new MRI units purchased in major markets now offer deep-learning reconstruction, enabling up to 20% faster scan times and reducing motion artifacts.

High‑Field MRI Deployment: More than 30 high‑field (≥ 7T) MRI scanners were clinically installed worldwide in 2025—an increase of 120% compared to 2022—primarily used in neuroscience and research settings.

Sustainability Focus: Around 25% of leading imaging equipment manufacturers have pledged to reduce power consumption of their systems by 10–15% by 2030 via energy-efficient magnet and cooling designs.

The High‑end Medical Imaging Equipment Market can be segmented across types, applications, and end‑users, each reflecting distinct technology demands and clinical workflows. In terms of type, the market spans MRI, CT, PET (including hybrid), ultrasound, and other advanced systems, where selection depends on the diagnostic use case. By application, key domains include oncology, neurology, cardiology, orthopedics, and research-oriented imaging. End users comprise large hospitals, specialized diagnostic centers, academic/research institutes, and emerging ambulatory care settings. These segments interplay: for instance, hospitals often deploy MRI and PET for oncology or neurology, while research labs favor ultra‑high‑field MRI for advanced neuroscience work. Understanding these divisions helps decision-makers align product development, sales strategy, and investment to the most clinically and commercially valuable niches.

Among the various high‑end imaging types, Magnetic Resonance Imaging (MRI) leads, accounting for about 30% of the market, due to its unparalleled soft‑tissue contrast and non-ionizing nature. MRI systems—especially high-field and functional MRI—are widely adopted in both neurological and musculoskeletal diagnostics, making them the preferred choice for advanced imaging centers. The fastest-growing type is hybrid PET/MRI systems, with strong momentum driven by demand for simultaneous anatomical and metabolic imaging in oncology and neurology. Their growth rate is higher than other types due to clinical adoption of multi-modality diagnostics and increasing research funding for molecular imaging. Other types include CT scanners, ultrasound systems, and nuclear imaging (PET/CT, SPECT). Combined, these other segments make up approximately 45–50% of the market. CT remains critical for fast anatomical imaging, ultrasound continues to expand in interventional settings, and nuclear systems are key in functional diagnostics.

In application terms, oncology is the dominant segment, contributing roughly 43% of high‑end imaging use; this is because advanced modalities like PET, MRI, and hybrid systems are essential for tumor detection, staging, and response monitoring. The precision and sensitivity offered by high-end systems make them indispensable in cancer management. The fastest-growing application is neurology, fueled by rising incidence of neurodegenerative diseases, stroke, and research into brain function. Functional MRI (fMRI), diffusion tensor imaging, and hybrid PET/MR are increasingly used to map brain networks, driving growth in this area. Other application areas include cardiology, orthopedics, and research/academic imaging, which together account for the remaining ~30–35%. Cardiology uses high-end CT and MRI for vascular and structural reviews; orthopedics leverages MRI for soft tissue visualization; and research centers adopt ultra-high-field MRI and PET for investigational studies. In terms of consumer and end‑user trends, over 60% of major cancer centers globally now integrate PET/MR in their care pathways, and more than 45% of neuroscience research labs have reported installing 7T MRI systems for advanced brain imaging.

The leading end-user segment is hospitals, accounting for approximately 52% of high‑end imaging deployments, as they typically possess the infrastructure, capital, and patient volume to justify investment in premium systems. Large academic and multi-specialty hospitals use high‑end MRI, hybrid PET, and CT systems for diagnosis, treatment planning, and research. The fastest-growing end-user segment is diagnostic imaging centers (outpatient centers), supported by growing demand for advanced imaging outside traditional hospital systems. These centers are increasingly offering high‑field MRI and PET/CT services, driven by patient shift toward outpatient diagnostics and preventive health screening; their annual growth rate surpasses other segments due to lower operational barriers. Other end-users include academic and research institutions and specialty clinics. Academic institutions use ultra‑high-field MRI and hybrid units for research, while specialty clinics (e.g., neurology or oncology-focused centers) deploy specialized high‑end equipment. Combined, these other segments contribute roughly 30–35% of the market. Adoption trends show that in 2024, more than 40% of imaging research labs in North America reported using hybrid PET/MRI for longitudinal studies, and over 35% of diagnostic centers in Europe have upgraded their MRI units to 3 T or higher.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

In 2024, North America had over 1,800 high-end MRI units and 1,200 PET/CT scanners installed, serving approximately 4,500 hospitals and imaging centers. Asia-Pacific, with 2,200 new imaging units planned for 2025–2026, is rapidly increasing capacity, particularly in China, India, and Japan. Europe held 28% of the market in 2024, with Germany and France deploying over 600 PET/MRI systems collectively. South America and the Middle East & Africa contributed 18% and 16%, respectively, driven by healthcare infrastructure upgrades, government incentives, and emerging technology adoption. Regional digital transformation initiatives, including AI-assisted imaging and cloud-based diagnostic platforms, are influencing adoption patterns and enhancing operational efficiency globally.

North America holds 38% market share, with key demand from oncology, neurology, and cardiology departments in hospitals and research institutes. Regulatory bodies have implemented stricter radiation safety standards, promoting low-dose and energy-efficient MRI and PET systems. Digital transformation trends include AI-assisted image reconstruction, cloud-enabled diagnostics, and tele-imaging networks. Local players, such as GE Healthcare, are expanding hybrid PET/MRI installations and developing ultra-high-field MRI solutions. Enterprises in the region exhibit higher adoption rates for integrated diagnostic platforms, with more than 65% of large hospitals upgrading to AI-powered imaging systems to enhance throughput and accuracy.

Europe accounts for 28% of the market, with Germany, France, and the UK as the leading contributors. Strict regulatory requirements for patient safety and sustainability initiatives have driven adoption of energy-efficient and explainable imaging systems. Hospitals and research centers are increasingly implementing AI-based reconstruction and hybrid imaging technologies. Siemens Healthineers is actively deploying PET/MRI solutions across Germany and France, improving diagnostic precision. European consumers and medical institutions prioritize compliance, explainable AI outputs, and sustainable device operations, reflecting the region’s regulatory-driven adoption patterns.

Asia-Pacific contributed 22% of the global market in 2024, with China, India, and Japan as top consumers. Infrastructure upgrades include construction of specialty hospitals and diagnostic chains. The region emphasizes technology innovation hubs, AI-assisted imaging applications, and mobile-integrated imaging platforms. Canon Medical and Hitachi are expanding PET/MRI and high-field MRI deployments in Japan and India. Regional adoption trends are influenced by increased healthcare accessibility, rising private healthcare investment, and digital integration, with over 40% of hospitals planning new high-end imaging units in 2025.

South America holds 10% of the market, with Brazil and Argentina leading adoption. Healthcare infrastructure improvements, government subsidies, and favorable trade policies support expansion of high-end MRI, CT, and PET systems. Philips and Siemens have installed hybrid imaging units in top hospitals to improve oncology diagnostics. Regional consumer trends show demand tied to urban healthcare access and medical tourism, with approximately 35% of hospitals integrating AI-assisted imaging platforms to improve efficiency.

Middle East & Africa accounted for 6% of the market, with the UAE and South Africa as primary growth centers. Regional demand is driven by healthcare infrastructure upgrades in urban centers and expanding private hospital networks. Technological modernization includes digital imaging platforms, AI-assisted MRI, and PET scans. Siemens and GE have deployed advanced PET/MRI scanners in Dubai and Johannesburg. Regional consumer behavior trends indicate higher adoption in private hospitals, with growing interest in precision diagnostics and reduced patient wait times.

United States - 38% Market Share: Strong end-user demand in hospitals and research centers, with high production capacity.

Germany - 12% Market Share: Robust regulatory support and advanced technological adoption in healthcare and research facilities.

The competitive environment in the High‑end Medical Imaging Equipment Market is moderately consolidated, with around 15–20 active major players competing globally. The top 5 companies — GE Healthcare, Siemens Healthineers, Philips, Canon Medical Systems, and Hitachi — together command an estimated 65–70% combined share of the high‑end imaging segment, reflecting deep R&D investments, distribution strength, and longstanding brand leadership.

Strategic initiatives are very active: GE Healthcare recently secured FDA clearance for its 3.0T and head-only MRI models; Siemens Healthineers has struck a multi‑hundred million euro deal to strengthen its PET radiopharmaceutical supply chain; Philips continues to push its helium-free MRI systems and integrated digital health diagnostic suites; Canon Medical is expanding its advanced hybrid systems in Asia; and Hitachi is innovating in compact and open MRI designs. Partnerships between OEMs and AI‑software companies are accelerating, enabling real‑time image reconstruction, deep‑learning enhancement, and quantification tools.

Innovation trends such as ultra‑high-field MRI (7T and above), hybrid PET/MR, AI-driven reconstruction, and low‑dose radiation technologies are reshaping competitive positioning. Many players are competing on software platforms as much as hardware, reflecting a shift from purely device-based competition to solution-based differentiation. The market's nature allows both scale players (top five) and niche innovators to coexist: while the leaders drive volume and brand trust, smaller firms are pushing into ultra-high-field, portable, or research-oriented imaging subsegments.

Canon Medical Systems Corporation

Hitachi Medical Systems

The technological landscape in high‑end medical imaging is being reshaped by a convergence of advanced hardware and smart software. Ultra‑high-field MRI systems (such as 7 Tesla and above) are gaining traction in research and specialized clinical settings, offering significantly higher signal-to-noise ratio and spatial resolution for neurological and oncological applications. Hybrid systems combining PET and MRI are being adopted more widely, because they deliver both metabolic and anatomical data in a single scan, improving clinical insights especially for cancer diagnostics and neurodegenerative disease monitoring.

On the software front, AI-driven reconstruction algorithms are now embedded within many modern scanners, enabling faster scan times, reduced motion artifacts, and better image quality. Deep-learning techniques are also applied for noise reduction, automated segmentation, and quantification — transforming raw imaging data into clinically actionable metrics. Another emerging technology is metamaterial-based RF coils, which are lighter, more flexible, and can boost SNR, thus improving patient comfort and imaging performance.

Energy-efficiency is another critical trend: new MRI systems use low-helium or helium-free magnet designs, reducing cryogen consumption and total cost of ownership. Additionally, portable and point-of-care high-end imaging platforms are being developed — especially compact MRI machines — allowing deployment in remote or resource-constrained settings. These devices are often paired with cloud-based diagnostic platforms, enabling remote review, AI-assisted reporting, and interoperability with health information systems.

Collectively, these technologies are not only pushing the boundaries of image quality but also enabling more cost‑effective, scalable, and sustainable high‑end imaging solutions. For decision-makers, investing in platforms with AI, hybrid imaging, and energy-efficient architecture is becoming central to competitive differentiation.

In September 2024, GE HealthCare received FDA approval for its Flurpiridaz F-18 PET tracer, Flyrcado ™, to be used in myocardial perfusion imaging (MPI) for coronary artery disease; this tracer has a long half-life (~109 minutes) and is supplied as a unit‑dose formulation for easier distribution and use. Source: www.gehealthcare.com

In December 2024, Siemens Healthineers expanded its Magnetom Flow. MRI platform by introducing a 70 cm bore 1.5 T system that uses nearly helium‑free cooling and AI-powered image reconstruction to improve energy efficiency and workflow. Source: www.siemens-healthineers.com

Also in December 2024, Siemens Healthineers announced the launch of the PET/MR Biograph One scanner, combining PET and 3 T MR, with AI reconstruction and large field-of-view PET to potentially halve patient slot times and support theranostics. Source: www.siemens-healthineers.com

In November 2024, Canon Medical Systems entered into a research collaboration with Penn Medicine for photon-counting CT (PCCT), following the installation of its fourth-generation PCCT in the University of Pennsylvania’s hospital to drive advanced diagnostic applications in cardiac and musculoskeletal imaging. Source: www.global.medical.canon

The scope of this High‑end Medical Imaging Equipment Market Report encompasses a comprehensive evaluation of modalities, applications, end-user segments, and geographic regions. On the modality side, the report covers high-field MRI, ultra-high-field MRI, hybrid PET/MRI, PET/CT, SPECT, and other advanced nuclear imaging plus high-precision CT systems. Applications analyzed include oncology, neurology, cardiology, orthopedics, and research-focused imaging. For end users, the report examines hospitals, high‑specialty diagnostic centers, academic and research institutes, and mobile or point-of-care imaging facilities.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with detailed insights into regional demand dynamics, infrastructure capacity, regulatory factors, and technology adoption. The report also dives into innovation trends — such as AI-powered reconstruction, cloud-enabled imaging platforms, and energy-efficient magnet designs — and evaluates their commercial and clinical potential. In addition, niche segments like research-grade 7T MRI, compact high‑end scanners, and portable PET systems are discussed, together with potential future disruptions.

The analysis includes competitive benchmarking, strategic growth initiatives, and investment flows, making it particularly valuable for OEMs, hospital administrators, research institutions, and investors seeking to understand the key value drivers, technology trajectories, and entry‑opportunity spaces in the high-end medical imaging landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 4,370.0 Million |

| Market Revenue (2032) | USD 6,809.0 Million |

| CAGR (2025–2032) | 5.7% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | GE Healthcare, Siemens Healthineers, Philips Healthcare, Canon Medical Systems Corporation, Hitachi Medical Systems |

| Customization & Pricing | Available on Request (10% Customization Free) |