Reports

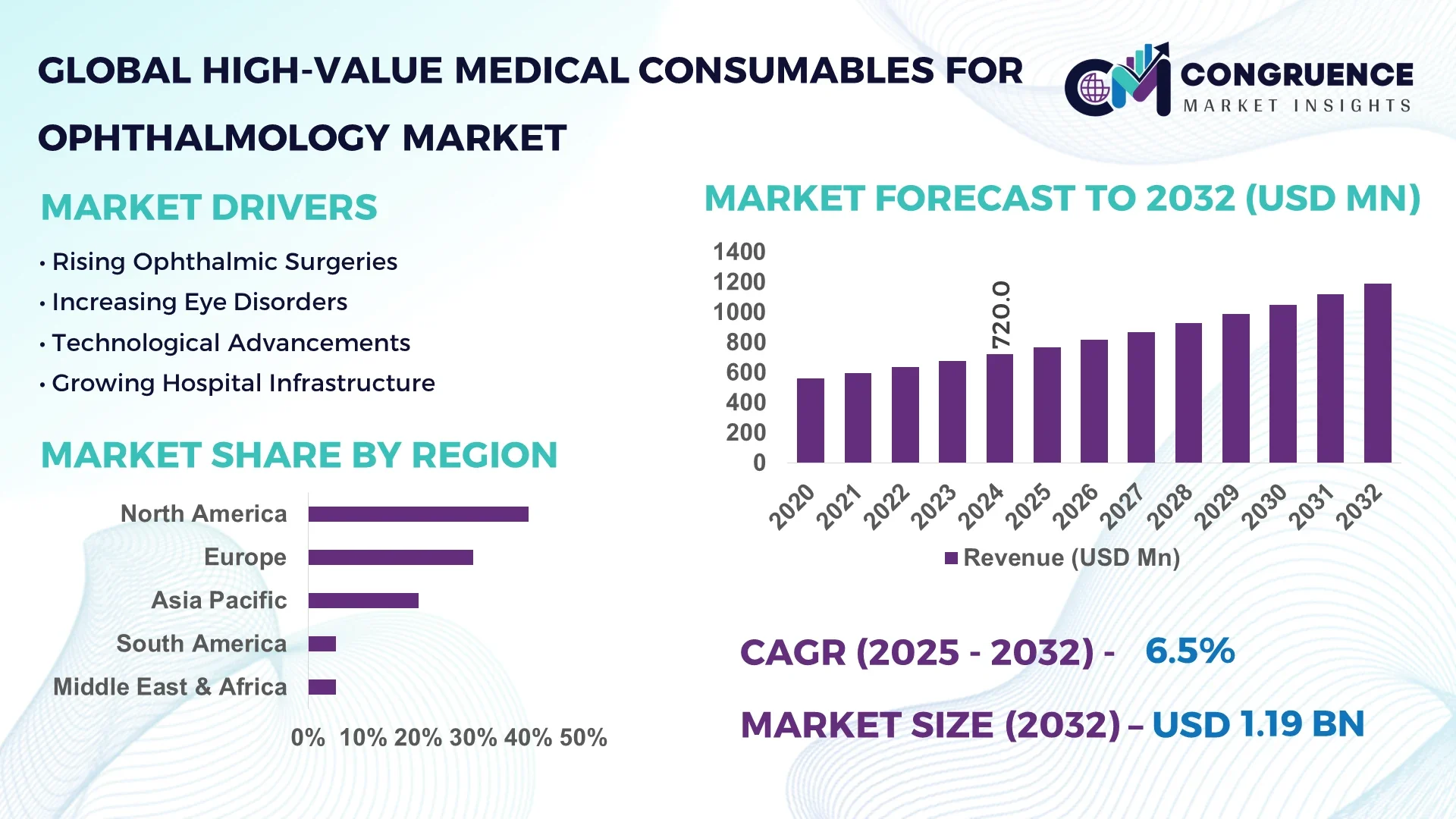

The Global High-value Medical Consumables for Ophthalmology Market was valued at USD 720.0 Million in 2024 and is anticipated to reach a value of USD 1,191.5 Million by 2032, expanding at a CAGR of 6.5% between 2025 and 2032. The market growth is primarily driven by increasing prevalence of ophthalmic disorders, rising geriatric population, and growing adoption of minimally invasive surgical solutions.

The United States holds a leading position in the High-value Medical Consumables for Ophthalmology Market due to its strong production capacity and technological innovation. The country’s ophthalmic consumables industry benefits from more than 120 advanced manufacturing facilities and annual investments exceeding USD 1.8 billion in R&D. The U.S. market is characterized by extensive application of microinjection technologies, precision lens manufacturing, and AI-based vision diagnostics. More than 68% of ophthalmic surgical centers in the country utilize high-value consumables such as intraocular lenses (IOLs), viscoelastic agents, and micro-surgical instruments, reflecting its advanced clinical adoption rate.

Market Size & Growth: The market was valued at USD 720.0 Million in 2024 and is projected to reach USD 1,191.5 Million by 2032, growing at a CAGR of 6.5%. Growth is driven by technological advancements and increased demand for precision ophthalmic consumables.

Top Growth Drivers: Rising adoption of advanced surgical lenses (42%), improvements in diagnostic accuracy (35%), and increased procedural efficiency (28%).

Short-Term Forecast: By 2028, production efficiency in ophthalmic consumables is expected to improve by 22% through automation and supply chain optimization.

Emerging Technologies: Integration of AI-assisted surgical visualization, bioresorbable implants, and 3D-printed ocular components are transforming the market landscape.

Regional Leaders: North America projected at USD 390.5 Million by 2032, Europe at USD 325.4 Million, and Asia Pacific at USD 296.7 Million, with Asia Pacific showing accelerated adoption in outpatient surgical applications.

Consumer/End-User Trends: Hospitals and specialized ophthalmic clinics represent the largest end-user segment, with over 60% adoption of high-value consumables in complex surgeries.

Pilot or Case Example: In 2024, a pilot initiative in Japan’s Shizuoka region reported a 24% reduction in cataract surgery time using advanced viscoelastic agents.

Competitive Landscape: Alcon Inc. leads the market with approximately 21% share, followed by Johnson & Johnson Vision, Bausch & Lomb, Carl Zeiss Meditec, and Hoya Corporation.

Regulatory & ESG Impact: New FDA and EU MDR standards mandate traceability and biocompatibility compliance; firms target a 15% improvement in waste recycling by 2030.

Investment & Funding Patterns: Over USD 2.1 billion invested globally in ophthalmic consumables manufacturing between 2022–2024, with growing venture capital in AI-integrated consumables.

Innovation & Future Outlook: Development of hybrid polymer-based consumables and AI-guided surgical tools is expected to redefine ophthalmic precision and cost efficiency.

The High-value Medical Consumables for Ophthalmology Market is witnessing transformative innovation in microsurgical instruments, lens materials, and automated consumable systems. With stronger regulatory focus on quality assurance and sustainability, the market is poised for balanced expansion across emerging and developed regions, driven by rapid technology adoption and healthcare digitization.

The High-value Medical Consumables for Ophthalmology Market holds strategic significance in enhancing global eye care outcomes through innovation, sustainability, and technological convergence. Strategic pathways revolve around digital integration, localized production, and cross-border collaborations to ensure affordability and accessibility. For instance, AI-assisted micro-suturing systems deliver 32% precision improvement compared to conventional manual methods, optimizing surgical outcomes.

Regionally, North America dominates in volume due to established healthcare infrastructure, while Asia Pacific leads in adoption with 46% of ophthalmic centers integrating smart consumable tracking systems. By 2027, automation technologies in ophthalmic consumable production are expected to reduce manufacturing costs by 18%, improving overall supply chain efficiency.

Compliance and ESG frameworks are shaping the industry’s roadmap. Firms are committing to 25% reductions in non-biodegradable waste and 30% material recycling rates by 2030. In 2024, Germany achieved a 19% operational cost reduction through implementation of precision molding and robotic packaging systems for ophthalmic consumables.

The future of the High-value Medical Consumables for Ophthalmology Market lies in digitized ecosystems, sustainable manufacturing, and AI-driven customization. These elements collectively position the market as a pillar of resilience, compliance, and sustainable growth in global healthcare delivery.

The High-value Medical Consumables for Ophthalmology Market is evolving through continuous innovation, healthcare modernization, and rising procedure volumes across developed and emerging economies. Growing adoption of premium intraocular lenses, micro-surgical devices, and AI-assisted diagnostics is redefining ophthalmic treatment standards. Additionally, increased public and private investment in vision care infrastructure, coupled with rising awareness of early disease detection, contributes to consistent market expansion and technological diffusion.

The rising incidence of ophthalmic disorders such as cataracts, glaucoma, and diabetic retinopathy is substantially increasing the demand for high-value medical consumables. More than 280 million global cases of visual impairment necessitate frequent ophthalmic procedures, boosting the use of intraocular lenses, viscoelastic materials, and surgical blades. Technological advances in laser-assisted cataract surgery have enhanced precision and reduced complication rates, further accelerating consumable adoption across hospitals and ambulatory surgical centers.

Regulatory frameworks governing ophthalmic consumables are becoming increasingly stringent, particularly concerning biocompatibility, sterilization, and traceability. Compliance with ISO and MDR standards adds significant testing and documentation costs, often extending product approval timelines by 8–12 months. Moreover, the cost of medical-grade polymers and precision manufacturing continues to rise, constraining production scalability and profitability for smaller manufacturers within the global market.

AI-based process automation and smart tracking systems are creating new opportunities in ophthalmic consumables. Intelligent lens assembly lines and predictive maintenance technologies can increase productivity by up to 30%. The integration of machine learning algorithms in surgical consumables manufacturing enhances defect detection and reduces wastage, paving the way for higher operational efficiency and improved global accessibility of advanced ophthalmic products.

Limited access to advanced surgical infrastructure, especially in low- and middle-income regions, restricts the uptake of high-value ophthalmic consumables. Over 40% of global eye-care facilities still lack automated equipment necessary for precision lens and instrument utilization. Shortages in skilled ophthalmic professionals further hinder widespread adoption, resulting in slower market penetration despite growing clinical awareness and healthcare investments.

Growth in AI-integrated Surgical Consumables: The integration of AI systems in ophthalmic surgeries has improved procedural accuracy by 28% and reduced operation time by 18%. Automated consumable calibration systems are being rapidly adopted in Japan and the U.S., enhancing productivity and reducing wastage during lens implantation and corneal correction procedures.

Expansion of 3D Printing in Consumable Manufacturing: 3D printing technologies have enabled the production of customized ophthalmic devices with 35% faster turnaround times. Europe and South Korea are leading adopters, focusing on polymer-based intraocular lens manufacturing for personalized patient solutions, thereby reducing procedural complications and enhancing patient satisfaction rates.

Sustainable Materials and Recycling Initiatives: With sustainability at the forefront, over 45% of manufacturers have shifted toward bio-based or recyclable materials. By 2030, companies aim for a 25% reduction in single-use plastics in ophthalmic consumables, promoting greener production practices and compliance with global ESG goals.

Adoption of Smart Supply Chain Systems: Integration of IoT-enabled tracking and analytics has improved global inventory accuracy by 33% and reduced wastage by 21%. These digital platforms ensure timely availability of high-value consumables, particularly in high-volume ophthalmic surgical centers across North America and Asia Pacific.

The High-value Medical Consumables for Ophthalmology Market is segmented by type, application, and end-user, reflecting a diversified ecosystem of ophthalmic care solutions. By type, the market includes intraocular lenses, viscoelastic devices, ophthalmic surgical instruments, and diagnostic consumables, each contributing to clinical precision and patient outcomes. Application-wise, cataract and refractive surgeries account for a major share, followed by glaucoma and retinal procedures. In terms of end-users, hospitals and specialty eye clinics dominate the market due to their advanced infrastructure and higher procedural volumes. Growing investments in outpatient surgical centers and ophthalmic diagnostic laboratories are reshaping demand patterns across emerging regions.

Intraocular lenses (IOLs) currently lead the High-value Medical Consumables for Ophthalmology Market, accounting for approximately 38% of total adoption due to their essential role in cataract and refractive surgeries. Their precision optics, durability, and enhanced visual outcomes have made them indispensable in modern ophthalmic care. Viscoelastic devices represent around 25% of usage, vital for maintaining ocular structure during intraocular procedures. However, the ophthalmic surgical instruments segment is growing fastest, projected to expand at a CAGR of 7.2%, driven by technological advancements such as laser-assisted microinstruments and ergonomic handheld tools. Diagnostic consumables, including dyes and disposable surgical drapes, collectively hold around 22% share, serving niche procedural needs in retinal and corneal treatments. According to recent industry data, over 32 million intraocular lenses were implanted globally in 2024, marking a 15% increase from 2022.

Cataract surgery dominates the application landscape of the High-value Medical Consumables for Ophthalmology Market, representing about 41% of total adoption. The demand is supported by a rapidly aging population and continuous innovation in lens implantation and phacoemulsification technologies. Refractive surgeries account for approximately 28%, driven by growing interest in vision correction among younger demographics. However, glaucoma treatment applications are expanding fastest, projected to grow at a CAGR of 7.5%, as minimally invasive glaucoma surgeries (MIGS) gain traction across advanced ophthalmic centers. Retinal and corneal applications collectively contribute around 22% of market use, catering to increasing diabetic and age-related vision impairments. In 2024, more than 47% of global ophthalmic clinics reported implementing advanced diagnostic consumables for early glaucoma detection. Furthermore, over 55% of patients in Asia-Pacific preferred laser-based cataract procedures for improved recovery outcomes.

Hospitals constitute the leading end-user segment in the High-value Medical Consumables for Ophthalmology Market, holding approximately 46% share due to their comprehensive surgical capabilities and patient inflow. Specialized ophthalmic clinics follow with 32% adoption, favored for precision procedures and outpatient flexibility. However, ambulatory surgical centers (ASCs) represent the fastest-growing segment, projected to expand at a CAGR of 7.8%, driven by rising demand for minimally invasive eye procedures and cost-effective service models. Diagnostic laboratories and academic institutes collectively account for about 18% of the market, contributing to research, testing, and procedural innovation.

In 2024, over 58% of ophthalmic ASCs in North America reported using disposable viscoelastic syringes and high-definition surgical blades to improve operational safety. Globally, 62% of hospitals implemented AI-supported lens positioning systems for cataract surgeries.

North America accounted for the largest market share at 40% in 2024; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 8% between 2025 and 2032.

North America’s leadership in 2024 is supported by high procedural volume and advanced healthcare infrastructure: hospitals and clinics in this region perform millions of eye surgeries annually, and about 35–40% of global high-value ophthalmic consumable usage is concentrated here. In contrast, Asia Pacific held roughly 20% of total revenues in 2024 for high-value medical consumables in ophthalmology but is seeing accelerating investment in healthcare access, infrastructure expansion, and aging demographics. Europe held about 30%, with Germany, UK, and France leading in adoption of new intraocular lens technologies. Latin America and Middle East & Africa each contributed about 5%. The shift in growth toward Asia Pacific is driven by rising disposable incomes in China and India, expanding outpatient clinic networks, and government-led healthcare spending increases.

North America held around 40% market share of global high-value medical consumables for ophthalmology in 2024. Surge in demand is driven largely by hospital-based cataract surgery volumes, increasing number of outpatient ophthalmic clinics, and high utilization of premium intraocular lenses and viscoelastic agents. Regulatory bodies and reimbursement programs in the U.S. and Canada have implemented stricter sterilization, traceability, and quality control standards, pushing manufacturers to innovate. Digital transformation is evident: surgical planning software, AI-assisted diagnostics, and precision manufacturing (e.g., ultra-thin lens optics, nanocoated materials) are becoming standard. Local players such as Bausch + Lomb and Alcon are introducing next-generation hydrophobic acrylic intraocular lenses with enhanced biocompatibility, and deploying automated packaging for disposables to reduce contamination risk. Consumer behavior varies: patients in North America increasingly demand faster recovery times and premium lens features; clinics respond with elective refractive procedures, while hospitals focus on volume and regulatory compliance.

Europe contributed approximately 30% of the global market for high-value ophthalmologic consumables in 2024. Key markets include Germany, the United Kingdom, and France, where premium IOLs and advanced diagnostic consumables are more prevalent. Regulatory bodies such as the European Medicines Agency (EMA) and national agencies enforce stringent quality, biocompatibility, and traceability regulations, leading to high demand for explainable production processes and sterile, single-use consumables. Emerging technologies—such as femtosecond laser cutting, premium multifocal IOLs, and AI-guided diagnostic tools—are being adopted more rapidly in Germany and France. Local manufacturers in the UK are investing in lens surface innovations and hybrid polymer materials. Consumer behavior in Europe tends toward cautious adoption, with regulatory and reimbursement approvals being major determinants of consumable use; consumers and providers favor proven safety and long clinical histories.

Asia-Pacific accounted for about 20% of global revenue from high-value ophthalmology consumables in 2024. Top consuming countries include China, India, and Japan. China led in consumption volume of ophthalmic instruments (≈ 71 million units) and accounted for nearly 49% of the regional unit volume demand; India remains a major producer with ~24 million units. Infrastructure expansion includes increased number of outpatient surgical centers and adoption of sterile, single-use consumables. Tech trends include mobile AI-based vision screening apps, tele-ophthalmology in rural areas, and local manufacturing of premium IOLs. A local player example: Indian firms are increasingly producing premium hydrophobic acrylic lenses domestically, reducing reliance on imports. Regional behavior shows faster uptake in urban centers with rising middle-class demand, while rural adoption lags but is growing via outreach programs.

South America contributed about 5% of the global market for high-value ophthalmic consumables in 2024. Key countries include Brazil and Argentina. Infrastructure has been improving, with investment in specialized eye hospitals and import of premium IOLs and disposable surgical tools. Government incentives and trade policies have lowered tariffs on medical consumables in several countries, promoting better access. Local players are beginning to partner with multinational manufacturers for co-development or distribution of high-quality consumables. Consumer behavior in South America shows increasing preference for advanced lens options and quicker recovery features, particularly in Brazil, where elective refractive surgery demand is rising.

Middle East & Africa accounted for approximately 5% of global high-value ophthalmology consumables revenue in 2024. Major growth countries include UAE and South Africa. There is a trend toward modernization: upgrading hospital infrastructure, increasing import of premium consumables, and government programs to enhance eye care access. Local regulations are being strengthened to ensure quality and biocompatibility for consumables; trade partnerships with international firms are common. Local manufacturers in South Africa are establishing cleanroom production for surgical blades and disposables. Consumer behavior varies: in affluent urban centers, there is demand for premium lens options and advanced surgical consumables; in rural or less affluent zones, cost sensitivity dominates and lower-price alternatives are more commonly used.

United States – 40% Market Share: Dominance due to strong production capacity, high procedural volumes, high legal/regulatory standards, and rapid adoption of advanced consumable technologies.

Germany – 10% Market Share: Leadership comes from high surgical rates, strong local manufacturing in premium IOLs and diagnostic consumables, and early adoption of emerging technologies.

The High-value Medical Consumables for Ophthalmology Market is characterized by a fragmented competitive environment, with numerous players vying for market share. As of 2024, the combined share of the top five companies in this sector is estimated to be approximately 45%, indicating a diverse landscape with significant opportunities for both established and emerging players. Key industry leaders include Alcon, Johnson & Johnson, Bausch + Lomb, HOYA Corporation, and Carl Zeiss, each contributing to the market through a combination of product innovation, strategic partnerships, and geographic expansion.

Strategic initiatives such as mergers and acquisitions, product launches, and collaborations with healthcare institutions are prevalent among these companies. For instance, Alcon has recently expanded its portfolio of intraocular lenses, while Johnson & Johnson has focused on enhancing its surgical instruments segment. Additionally, companies are investing in digital transformation trends, including the development of smart ophthalmic devices and integration of artificial intelligence in diagnostic tools, to stay competitive.

Innovation trends are heavily influencing market dynamics, with a strong emphasis on minimally invasive surgical consumables, advanced diagnostic equipment, and personalized treatment solutions. These innovations not only improve patient outcomes but also drive demand across various ophthalmic procedures. The competitive landscape is further shaped by regulatory developments, reimbursement policies, and the increasing adoption of telemedicine, all of which impact the strategies of market participants.

In summary, the High-value Medical Consumables for Ophthalmology Market presents a dynamic and competitive environment, with a blend of established players and new entrants driving innovation and growth through strategic initiatives and technological advancements.

HOYA Corporation

Carl Zeiss

Lucid Korea

Autek China

Haohai Biological Technology

Eyebright Medical Technology

Wuxi Vision Pro

Brighten Optix

Paragon

Contamac

Aaren Scientific

HexaVision

Menicon

The High-value Medical Consumables for Ophthalmology Market is experiencing significant technological advancements that are reshaping the landscape of eye care. One of the most notable developments is the integration of artificial intelligence (AI) and machine learning (ML) into diagnostic tools. These technologies enable ophthalmologists to detect and analyze eye conditions with greater accuracy and speed, leading to improved patient outcomes. For instance, AI algorithms are now capable of interpreting retinal scans to identify early signs of diseases such as diabetic retinopathy and macular degeneration, often before symptoms become apparent.

Another key technological trend is the development of minimally invasive surgical instruments. These devices are designed to reduce patient recovery times and minimize the risk of complications. Innovations such as femtosecond lasers and micro-incision surgical tools allow for more precise procedures, enhancing the overall efficiency and safety of ophthalmic surgeries.

Additionally, there is a growing emphasis on the use of biodegradable and bio-compatible materials in the manufacturing of ophthalmic consumables. These materials not only reduce the environmental impact of medical waste but also improve patient safety by minimizing the risk of adverse reactions.

The adoption of telemedicine in ophthalmology is also on the rise, facilitated by advancements in digital imaging and remote monitoring technologies. Patients can now receive consultations and follow-up care from the comfort of their homes, expanding access to eye care services, particularly in underserved areas.

These technological innovations are driving the growth of the High-value Medical Consumables for Ophthalmology Market, as they offer enhanced capabilities, improved patient experiences, and greater operational efficiencies for healthcare providers.

In June 2024, Alcon announced the launch of its new line of intraocular lenses (IOLs) designed to provide enhanced visual outcomes for patients undergoing cataract surgery. The new IOLs incorporate advanced materials and design features aimed at reducing glare and improving contrast sensitivity. Source: www.alcon.com

In August 2024, Johnson & Johnson Vision unveiled a next-generation surgical microscope equipped with augmented reality capabilities. This innovation allows surgeons to visualize real-time data overlays during procedures, enhancing precision and reducing the risk of errors. Source: www.jjvision.com

In October 2024, Bausch + Lomb received regulatory approval for its new line of disposable ophthalmic surgical instruments. These single-use tools are designed to reduce the risk of cross-contamination and improve operational efficiency in ophthalmic surgeries. Source: www.bausch.com

In December 2024, HOYA Corporation introduced a new series of contact lenses incorporating advanced moisture-retention technology. These lenses aim to provide longer-lasting comfort for users, addressing common issues such as dryness and irritation. Source: www.hoya.com

The High-value Medical Consumables for Ophthalmology Market Report provides a comprehensive analysis of the global ophthalmic consumables sector, encompassing a wide range of specialized products utilized in diagnostic, therapeutic, and surgical procedures related to eye care. The report delves into various market segments, including intraocular lenses (IOLs), surgical instruments, disposable contact lenses, viscoelastic devices, and surgical kits, offering insights into their respective market dynamics and growth trajectories.

Geographically, the report covers key regions such as North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, highlighting regional market trends, growth drivers, and challenges. It examines the adoption rates of advanced technologies across different regions and assesses the impact of regulatory frameworks on market development.

The report also explores emerging applications of ophthalmic consumables, such as their integration into telemedicine platforms and the increasing use of digital imaging in remote diagnostics. Additionally, it provides an overview of the competitive landscape, profiling major market players and analyzing their strategic initiatives, including product innovations, mergers and acquisitions, and partnerships.

Furthermore, the report addresses consumer behavior trends, such as the growing preference for minimally invasive surgical options and the demand for personalized eye care solutions. It also discusses the implications of demographic shifts, particularly the aging global population, on the demand for ophthalmic consumables.

In summary, the High-value Medical Consumables for Ophthalmology Market Report offers a detailed and multifaceted perspective on the ophthalmic consumables market, serving as a valuable resource for stakeholders seeking to understand current trends, future opportunities, and strategic directions in this dynamic industry.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 720.0 Million |

| Market Revenue (2032) | USD 1,191.5 Million |

| CAGR (2025–2032) | 6.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Alcon, Johnson & Johnson, Bausch + Lomb, HOYA Corporation, Carl Zeiss, Lucid Korea, Autek China, Haohai Biological Technology, Eyebright Medical Technology, Wuxi Vision Pro, Brighten Optix, Paragon, Contamac, Aaren Scientific, HexaVision, Menicon |

| Customization & Pricing | Available on Request (10% Customization is Free) |