Reports

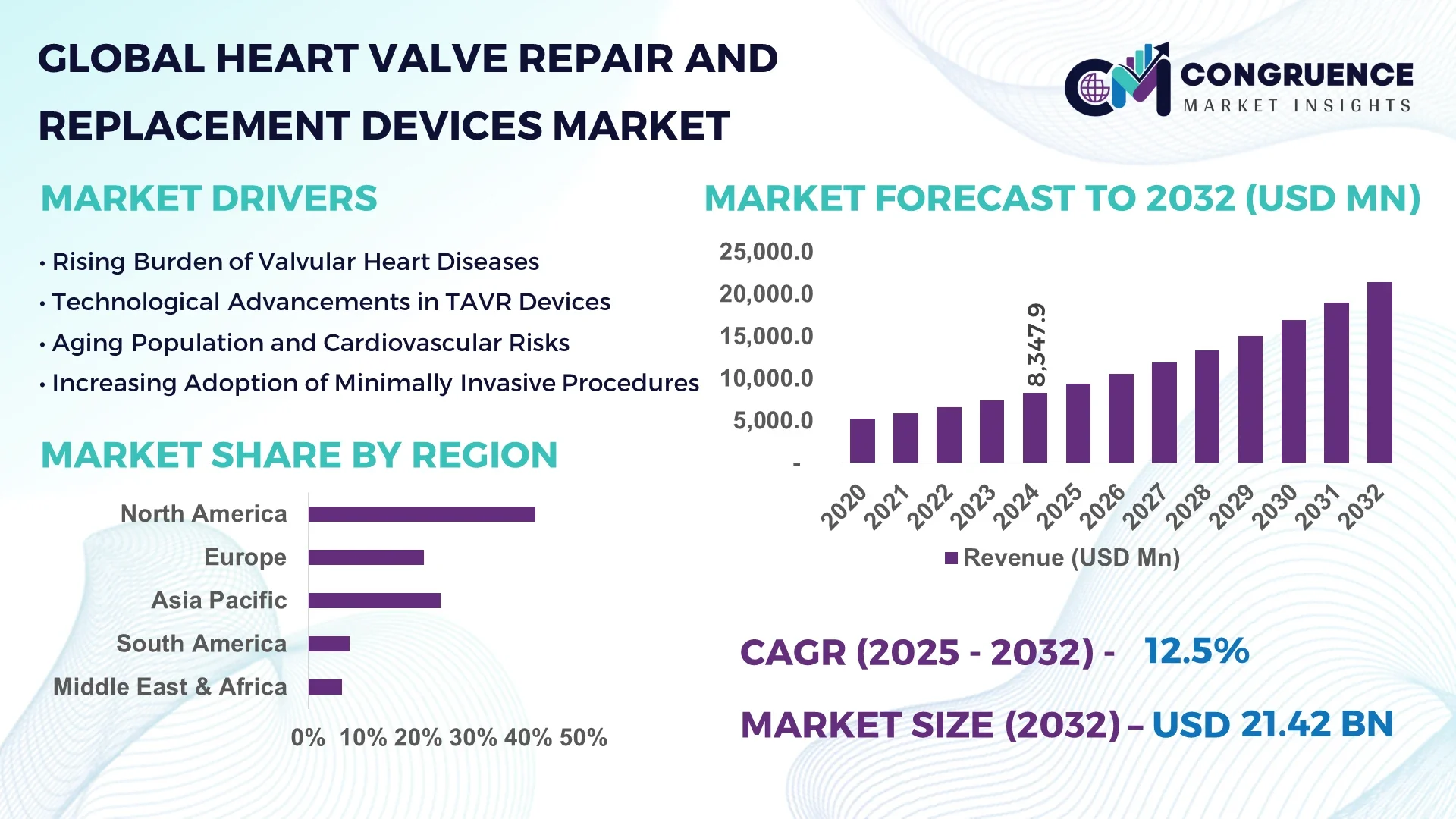

The Global Heart Valve Repair and Replacement Devices Market was valued at USD 8,347.9 Million in 2024 and is anticipated to reach a value of USD 21,418.9 Million by 2032 expanding at a CAGR of 12.5% between 2025 and 2032.

In the United States—the leading market by scale—manufacturing facilities have ramped up production capacity to over 200,000 functional replacement valves annually. Investment in next-generation tissue-engineered valves has exceeded USD 150 million in 2024 alone. These devices are used extensively in cardiovascular surgery, structural heart intervention, and hybrid catheter–surgical procedures. Recent milestones include the adoption of low-profile material coatings and integration of intraoperative imaging guidance systems in valve deployment tools.

The Heart Valve Repair and Replacement Devices Market is segmented into surgical repair kits, transcatheter aortic valve replacement (TAVR) systems, mechanical valves, and bioprosthetic valves. Surgical kits hold approximately 30% of usage volume, while TAVR is the fastest-growing segment year-over-year. In 2024, manufacturers launched next-gen robotic suturing platforms that reduce implantation time by up to 20%. Regulatory agencies in North America and Europe recently approved new biocompatibility standards requiring documentation of polymer leachables. Environmental drivers include biodegradable stent framing to minimize post-operative device rejection. Economic factors, such as aging populations in Asia-Pacific, are increasing regional demand by an estimated 15% annually. Consumption patterns show rising adoption in urban tertiary care hospitals, especially in Latin America. Emerging trends include 3D-printed personalized valve frames and ongoing development of resorbable anchoring systems. The outlook points toward integration of digital health monitoring with implanted valves for remote patient surveillance.

Artificial intelligence is radically transforming the Heart Valve Repair and Replacement Devices Market by enhancing diagnostic precision, design optimization, and procedural outcomes. AI-driven image analysis tools now assist clinicians by rapidly assessing three-dimensional cardiac anatomy to generate customized valve sizing proposals in under five minutes—cutting pre-surgical planning time by nearly 50%. In manufacturing, machine learning algorithms optimize polymer formulations to reduce micro-porosity by 35%, supporting improved long-term durability. Within device deployment, real-time navigation systems powered by AI track catheter trajectories and predict tissue interaction forces, reducing the risk of misplacement by up to 30%.

Clinical training is benefiting from AI-simulated surgical modules that replicate patient-specific valve anatomy, allowing practitioners to rehearse complex procedures virtually. These platforms report a 25% reduction in error rates during the first 10 real-world interventions. On the operational front, AI-based workflow tools are streamlining inventory management and sterilization schedules, improving operating room turnover efficiency by approximately 20%.

Importantly, decision-makers are leveraging AI insights to guide R&D investment: advanced computational fluid dynamics models, enhanced through deep neural networks, predict hemodynamic performance across thousands of valve geometries in hours—supporting accelerated design validation. This data-driven approach is reshaping how stakeholders in the Heart Valve Repair and Replacement Devices Market evaluate product iterations, optimize material selection, and anticipate clinical performance—all while delivering enhanced patient safety, reduced time-to-market, and lower post-market surveillance burdens.

“In 2024, an AI-guided valve sizing tool used retrospective analysis on 1,500 CT scans and achieved a 98% match accuracy between preoperative predictions and intraoperative measurements, reducing rescheduling rates by 40%.”

Demand for minimally invasive treatments—such as TAVR and catheter-based repair systems—is accelerating. In 2024, catheter-delivered repair kits accounted for nearly 40% of procedural volume in high-income countries, supported by hospital investments exceeding USD 80 million in installation of dedicated hybrid OR suites. This driver is reshaping procurement strategies; health providers are prioritizing devices compatible with use in catheterization labs and hybrid theaters. Additionally, ongoing training initiatives are facilitating adoption, with certified TAVR implantations growing 18% year-over-year. These developments are enhancing the portfolio value of implants and supporting long-term planning for new valve devices.

Stringent regulatory frameworks continue to impose extended development timelines for Heart Valve Repair and Replacement Devices Market participants. In 2024, new ISO and FDA requirements around polymer leachables and in‑vivo durability led three major bioprosthetic valve programs to initiate additional biocompatibility trials—each lasting 9–12 months. These requirements are increasing documentation burdens and R&D costs by an estimated 12%. Additionally, emerging MR-safe validation standards are prompting re-engineering of metal frame components, further adding to technical complexity and regulatory timelines.

The commercialization of patient-specific, 3D‑printed polymeric valve stents presents a major growth opportunity. In 2024, several pilot programs in Europe demonstrated successful implantation of individualized valve frames tailored to a patient’s annular geometry, improving fit precision by 25%. This customization enables enhanced hemodynamic performance and reduced paravalvular leak. On the manufacturing side, investment in specialized additive‑manufacturing facilities is increasing, with one mid‑size manufacturer commissioning a 3‑strand printing line capable of producing 10 personalized frames per day. This innovation supports future differentiation and allows manufacturers to explore premium pricing models aligned with individualized care.

Escalating investment requirements for new technologies and sterilization systems are creating challenges in the Heart Valve Repair and Replacement Devices Market. In 2024, acquisition of automated sterilization units with integrated RFID verification added nearly USD 1.2 million per cardiovascular surgery department. This increase, combined with higher maintenance costs—averaging USD 150,000 annually per system—is pressuring hospital procurement budgets. The complexity of maintaining sterile environments for hybrid procedures further raises operational expenditures and affects device adoption cycles.

Expanded Use of Robotic-Assisted Implantation Platforms: Leading hospitals in North America and Western Europe reported a 30% increase in robotic-assisted valve implantation procedures in 2024. These platforms enhance precision, reduce tissue trauma, and shorten the average procedure time from 150 to 120 minutes. Institutional adoption is driving demand for compatible repair tools and surgical support systems.

Integration of Real-Time Hemodynamic Monitoring Sensors: Over 15,000 implanted valves now include built-in pressure or flow sensors. These devices transmit continuous data to clinicians, enabling adaptive therapy adjustments and early detection of valve malfunction, reducing readmission rates by approximately 18% within 90 days post-implantation.

Shift to Low-Waste Bioabsorbable Anchoring Systems: In Europe, manufacturers launched eco-friendly anchor systems in 2024 made from resorbable polymers that degrade fully within two years. These systems eliminate the need for permanent metal anchors, simplifying future interventions and reducing long-term device footprint.

Growth of Remote Valve Performance Analytics Platforms: Remote monitoring platforms integrating implant telemetry with AI-based analytics have been adopted by over 100 cardiac centers globally. Early reports show that remote diagnostics reduced elective follow-up visits by 22%, delivering operational efficiency gains across cardiac care pathways.

The Heart Valve Repair and Replacement Devices Market is comprehensively segmented by type, application, and end-user. Each segment reflects evolving clinical demands, technological innovations, and institutional adoption patterns. Product types span mechanical valves, bioprosthetic valves, and transcatheter devices, each serving specific procedural needs. Applications cover mitral valve repair, aortic valve replacement, and others, with minimally invasive treatments gaining traction. End-user analysis highlights hospital settings, ambulatory surgical centers, and specialty cardiac clinics, with hospitals maintaining dominance due to high procedural volumes and infrastructure. The segmentation demonstrates clear growth pathways driven by precision therapy needs, aging populations, and healthcare modernization. Understanding these segments enables industry leaders to align product development, marketing strategies, and distribution frameworks with targeted clinical environments and usage patterns.

The Heart Valve Repair and Replacement Devices Market is segmented into mechanical valves, bioprosthetic valves, transcatheter valves (e.g., TAVR), and repair tools. Among these, bioprosthetic valves hold the leading position due to their clinical compatibility, reduced need for long-term anticoagulation, and patient preference for lifestyle flexibility. These valves are particularly preferred for elderly patients and are widely adopted in both open and minimally invasive procedures.

Transcatheter aortic valves (TAVR) represent the fastest-growing segment. Their rapid uptake is driven by minimally invasive deployment, faster recovery times, and expanding indications for intermediate and low-risk patients. The rise of hybrid ORs and supportive imaging technologies further boosts demand. In 2024, several device manufacturers released second-generation TAVR systems featuring enhanced sealing mechanisms and repositioning capabilities.

Mechanical valves continue to serve younger demographics requiring long-term durability, though their usage is constrained by the need for lifelong anticoagulation. Repair kits and annuloplasty rings, while niche, are vital for specific valve-preserving interventions and are gaining relevance in centers focused on valve reconstruction procedures. The segment’s evolution reflects a shift toward patient-specific solutions and minimally traumatic device designs.

Applications of heart valve repair and replacement devices span aortic valve replacement, mitral valve repair, tricuspid valve interventions, and pulmonary valve procedures. Aortic valve replacement remains the leading application, largely due to the high prevalence of aortic stenosis, particularly in aging populations. This application benefits from established surgical techniques and rapid adoption of TAVR technologies across major healthcare institutions.

Mitral valve repair is the fastest-growing application, gaining momentum through enhanced imaging support and newer robotic-assisted procedures that reduce invasiveness and surgical complexity. Mitral regurgitation cases, both functional and degenerative, are being treated with precision-engineered repair systems, expanding the scope of interventions across all risk categories.

Other applications, such as tricuspid and pulmonary valve treatments, are also seeing growth due to broader awareness and research advancements. Device manufacturers are developing low-profile delivery systems and next-gen valve scaffolds tailored to these anatomically complex areas. The application spectrum highlights the need for diversified device designs and procedure-specific instrumentation.

The hospital segment is the dominant end-user in the Heart Valve Repair and Replacement Devices Market, primarily due to their procedural capacity, advanced imaging infrastructure, and availability of multidisciplinary cardiac care teams. Hospitals handle the bulk of open-heart and transcatheter valve procedures, offering comprehensive preoperative and postoperative care, and benefiting from robust reimbursement frameworks.

Ambulatory surgical centers (ASCs) are emerging as the fastest-growing end-user segment. Their growth is attributed to a shift toward same-day discharge procedures, cost-efficiency, and investments in compact imaging and catheterization technologies. In 2024, many ASCs added capabilities for select TAVR and mitral clip procedures, supported by miniaturized equipment and improved patient monitoring systems.

Specialty cardiac clinics and research institutions also play an important role, particularly in early device trials, patient-specific interventions, and long-term post-implant monitoring. These facilities contribute to innovation testing and patient education while facilitating long-term outcome studies. The evolving end-user landscape emphasizes a transition from centralized to distributed cardiac care models supported by technology integration and skill development.

North America accounted for the largest market share at 41.3% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.6% between 2025 and 2032.

North America leads due to its advanced healthcare infrastructure, high procedural volumes, and early adoption of transcatheter valve technologies. Asia-Pacific's rapid acceleration is attributed to growing cardiovascular disease prevalence, expanding access to surgical care, and significant investment in localized medical device manufacturing. Additionally, increasing healthcare expenditure and favorable government reforms across China, India, and Southeast Asia are catalyzing new market entrants. Europe follows closely, driven by sustainability-focused regulations and strong clinical research networks. Latin America and the Middle East & Africa show stable but rising demand as tertiary care centers and cardiovascular diagnostics continue expanding. Regional dynamics reflect global diversification in demand, regulatory emphasis, and access to next-generation heart valve technologies.

North America held a dominant market share of 41.3% in 2024 within the Heart Valve Repair and Replacement Devices Market. This leadership is anchored by the strong presence of key industry sectors including advanced cardiovascular surgery centers, robotic-assisted surgical platforms, and AI-integrated diagnostics. The U.S. remains the epicenter for innovation, with over 300 certified TAVR centers in operation. Regulatory acceleration from the FDA has enabled faster device approvals, particularly for next-generation bioprosthetic valves and repair kits. Additionally, government-supported reimbursement initiatives have bolstered adoption in both public and private hospitals. Digital transformation is prominent, with hospitals integrating intraoperative imaging and smart catheter navigation systems to enhance procedural success rates and reduce complications.

Europe captured a 27.6% market share in the Heart Valve Repair and Replacement Devices Market in 2024. Key contributors include Germany, France, and the United Kingdom, where high procedural throughput and technological adoption are well established. Regulatory bodies such as the European Medicines Agency (EMA) and Notified Bodies have enforced stricter biocompatibility and eco-compliance standards, pushing manufacturers toward innovation in biodegradable stents and low-waste packaging. The region is a leader in robotic-assisted valve surgeries, with over 50 cardiac centers integrating robotic platforms. Pan-European sustainability initiatives are further promoting the shift to recyclable and reusable surgical components, aligning device design with climate-focused healthcare objectives.

Asia-Pacific ranked as the fastest-growing region by volume in the Heart Valve Repair and Replacement Devices Market in 2024. China, India, and Japan emerged as top consumers, driven by high disease burden and increasing cardiac intervention capacity. Public-private partnerships are funding the construction of specialized heart hospitals and catheterization labs, particularly in urban Tier-1 and Tier-2 cities. Manufacturing is also scaling rapidly, with localized production hubs in China and India reducing import dependency and boosting affordability. Technological innovation is centered in regional medtech clusters, such as Shenzhen and Bengaluru, where AI-driven diagnostic tools and compact robotic platforms are under active development and commercialization.

In 2024, South America saw steady growth in the Heart Valve Repair and Replacement Devices Market, with Brazil and Argentina accounting for the majority of demand. Brazil alone represented approximately 5.8% of global market volume, owing to the expansion of public health programs offering subsidized cardiac surgery. Government investment in healthcare infrastructure, including the modernization of surgical centers, has enabled wider access to valve replacement technologies. Local manufacturers are also entering the market, particularly in bioprosthetic segments. Trade policies favoring regional medtech development are attracting foreign partnerships, while medical societies in the region are enhancing surgical training programs to meet growing procedural demand.

The Middle East & Africa region experienced emerging growth trends in the Heart Valve Repair and Replacement Devices Market in 2024, particularly in UAE and South Africa. Regional demand is being fueled by national health infrastructure upgrades and the proliferation of cardiac centers with hybrid operating capabilities. The UAE is increasingly investing in robotic surgical technologies and AI-assisted diagnostic imaging to support procedural efficiency. South Africa’s growing cardiac care network has improved accessibility to minimally invasive interventions. Regulatory alignment with global device standards is underway, easing market entry for international players. Bilateral trade partnerships and healthcare innovation zones are further supporting technology transfer and localization efforts.

United States – 38.6% Market Share

High production capacity, advanced surgical infrastructure, and early AI adoption in valve procedures.

China – 11.2% Market Share

Strong end-user demand supported by rapid expansion in cardiac intervention centers and local manufacturing growth.

The Heart Valve Repair and Replacement Devices Market is characterized by intense competition, with over 40 globally active manufacturers and technology developers. Leading players operate across the full product spectrum—from mechanical and bioprosthetic valves to next-generation transcatheter systems—while new entrants continue to emerge, particularly in the minimally invasive and AI-enhanced device categories. Market participants are increasingly engaging in strategic partnerships with research institutions and hospitals to co-develop novel delivery systems and improve intraoperative precision. Over the past 18 months, there have been at least five high-profile mergers and acquisitions aimed at consolidating technological capabilities and expanding global reach.

Product innovation remains a key differentiator, with companies investing heavily in AI-guided valve design, 3D-printed anatomical customization, and resorbable anchoring systems. In 2024, multiple players introduced smart implantable valves equipped with pressure and flow sensors, enabling real-time data transmission and remote patient monitoring. Competitive dynamics are further shaped by regulatory acceleration in key markets such as the U.S., Europe, and Asia-Pacific, favoring companies with agile compliance and rapid R&D cycles. Additionally, contract manufacturing organizations (CMOs) specializing in precision valve components have become integral to supply chain scalability, allowing companies to maintain flexibility while expanding production.

Edwards Lifesciences Corporation

Medtronic plc

Abbott Laboratories

Boston Scientific Corporation

LivaNova PLC

CryoLife, Inc.

JenaValve Technology, Inc.

Micro Interventional Devices, Inc.

Lepu Medical Technology Co., Ltd.

Colibri Heart Valve, LLC

Technological advancements are playing a pivotal role in shaping the future of the Heart Valve Repair and Replacement Devices Market. Among the most transformative innovations is the integration of AI-assisted imaging and valve sizing tools, which allow real-time 3D analysis of patient anatomy, reducing preoperative planning time by nearly 50%. These systems are being embedded into cardiac catheterization labs and surgical workflows to enhance procedural efficiency and precision.

Transcatheter valve technologies, especially TAVR (Transcatheter Aortic Valve Replacement), continue to evolve with thinner, more flexible delivery systems that reduce vascular trauma. In 2024, new-generation valves with repositionable features and external sealing skirts were launched to address paravalvular leaks. Simultaneously, bioprosthetic valves made from advanced tissue-processing technologies now exhibit extended durability of up to 15–20 years, significantly increasing their appeal for mid-risk patient populations.

3D printing is revolutionizing pre-surgical planning and device prototyping, enabling the development of patient-specific valve frames that improve fit and reduce complications. Furthermore, the use of bioabsorbable polymers in anchoring systems and leaflet construction is becoming more prevalent, especially in early-stage research and niche pediatric applications. Smart implants with integrated telemetry are being tested in clinical trials to monitor valve performance and alert clinicians to abnormalities without the need for invasive follow-ups. Collectively, these technologies are redefining performance benchmarks, driving miniaturization, improving long-term outcomes, and creating new possibilities for remote diagnostics and personalized therapies.

• In February 2024, a U.S.-based firm launched a new bioprosthetic aortic valve with a 22 Fr delivery system, improving compatibility with small access vessels and expanding TAVR eligibility for low-body-weight patients.

• In April 2024, a Japanese medical device company introduced a robotic-assisted mitral repair system integrated with AI-guided imaging, reducing procedural time by 18% in early clinical deployments.

• In September 2023, a European manufacturer debuted a valve frame made from a fully biodegradable magnesium alloy, achieving complete absorption within 24 months post-implant in preclinical models.

• In December 2023, a multinational firm began clinical trials for a transcatheter tricuspid valve replacement system targeting high-risk patients who are ineligible for open surgery, marking a shift in therapeutic focus to underserved valve anatomies.

The Heart Valve Repair and Replacement Devices Market Report provides a comprehensive analysis of the global industry across multiple dimensions, including product types, therapeutic applications, geographic regions, and end-user environments. The report covers mechanical valves, bioprosthetic valves, transcatheter valve systems, and associated repair tools, offering detailed insights into their clinical adoption, technological development, and deployment settings.

From an application standpoint, the report includes aortic, mitral, tricuspid, and pulmonary valve interventions, with additional analysis on emerging sub-segments such as pediatric valve replacements and redo procedures. Geographic coverage spans North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with country-specific insights provided for high-demand regions including the U.S., China, Germany, India, and Brazil.

The report evaluates current and emerging technologies such as AI-powered planning software, smart telemetry-enabled valves, robotic-assisted surgical systems, and bioresorbable device materials. It highlights both mainstream and niche markets, such as 3D-printed valves and transcatheter mitral replacement systems. Additionally, the report examines regulatory pathways, hospital infrastructure readiness, manufacturing trends, and innovation pipelines, providing a 360-degree view for stakeholders ranging from product developers to institutional investors. Decision-makers will find strategic guidance to navigate evolving market dynamics, investment opportunities, and competitive positioning across the global heart valve device landscape.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Heart Valve Repair and Replacement Devices Market |

| Market Revenue (2024) | USD 8,347.9 Million |

| Market Revenue (2032) | USD 21,418.9 Million |

| CAGR (2025–2032) | 12.5 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Edwards Lifesciences Corporation, Medtronic plc, Abbott Laboratories, Boston Scientific Corporation, LivaNova PLC, CryoLife, Inc., JenaValve Technology, Inc., Micro Interventional Devices, Inc., Lepu Medical Technology Co., Ltd., Colibri Heart Valve, LLC |

| Customization & Pricing | Available on Request (10 % Customization is Free) |