Reports

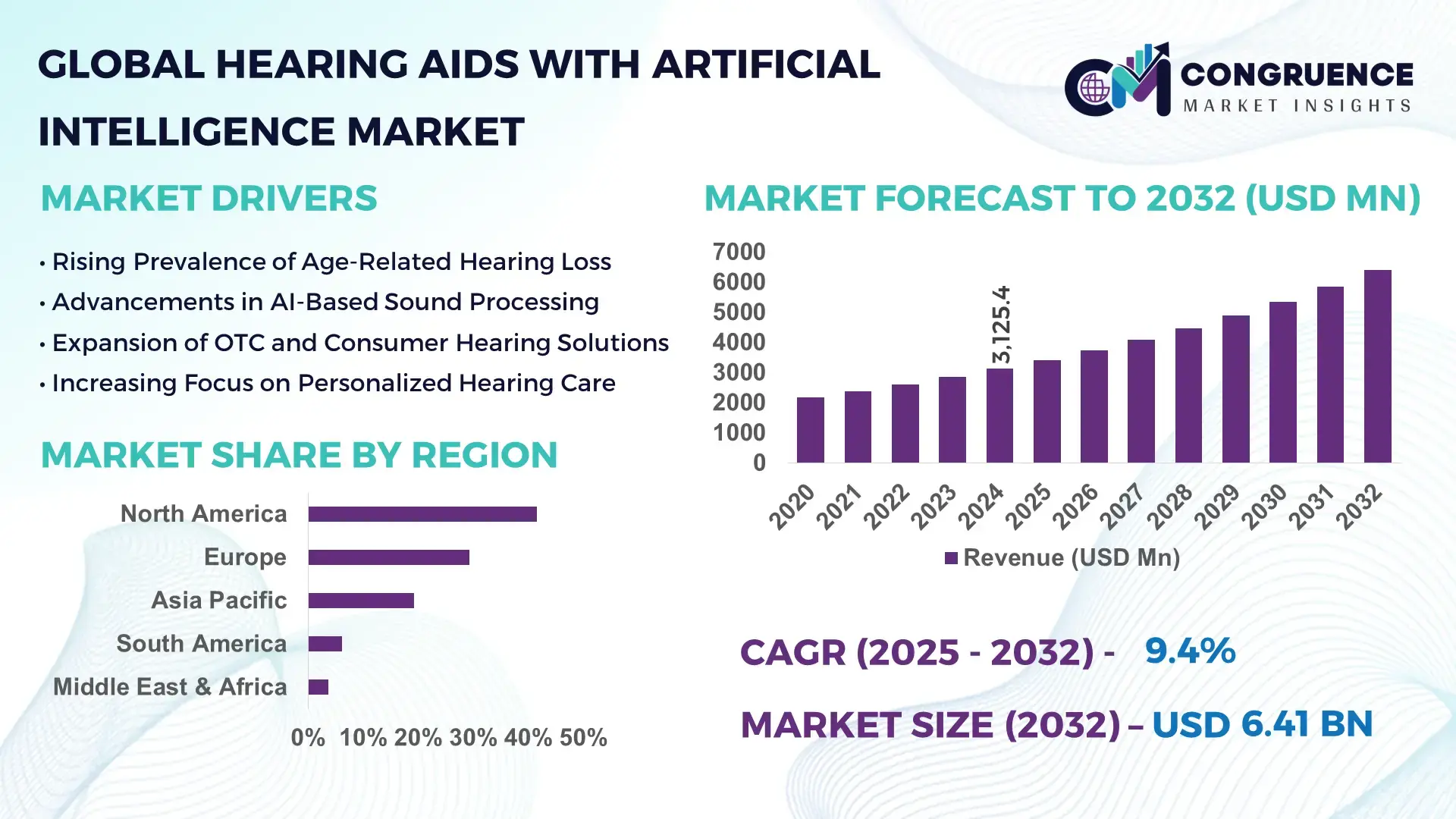

The Global Hearing Aids with Artificial Intelligence Market was valued at USD 3,125.4 Million in 2024 and is anticipated to reach a value of USD 6,412.7 Million by 2032 expanding at a CAGR of 9.4% between 2025 and 2032, according to an analysis by Congruence Market Insights. Growth is supported by rising adoption of AI-enabled adaptive sound processing, increasing geriatric populations, and rapid integration of machine learning algorithms into digital hearing solutions.

The United States dominates the Hearing Aids with Artificial Intelligence market through advanced manufacturing capacity, sustained R&D investment, and early commercialization of AI-powered audiology solutions. In 2024, the U.S. accounted for over 38% of global AI-enabled hearing aid production units, supported by more than USD 620 million in annual private and public investments in digital hearing health technologies. Over 55% of newly fitted hearing aids in the country incorporate AI-driven noise reduction or speech enhancement features. Clinical applications remain prominent, with more than 70,000 audiology clinics deploying AI-calibrated devices, while consumer-grade OTC hearing aids with embedded AI recorded adoption among 22% of adults aged 45–64, reflecting strong consumer acceptance and technological maturity.

Market Size & Growth: Valued at USD 3,125.4 million in 2024, projected to reach USD 6,412.7 million by 2032, driven by AI-based sound personalization and rising hearing impairment prevalence.

Top Growth Drivers: AI-enabled speech clarity improvement (45%), wireless connectivity adoption (38%), OTC hearing aid penetration (29%).

Short-Term Forecast: By 2028, AI-assisted auto-calibration is expected to improve user satisfaction scores by over 35%.

Emerging Technologies: Deep neural networks for noise suppression, edge AI processors, real-time acoustic environment learning.

Regional Leaders: North America projected at USD 2.3 billion by 2032 with OTC adoption growth; Europe at USD 1.8 billion driven by public reimbursement programs; Asia Pacific at USD 1.5 billion supported by urban aging populations.

Consumer/End-User Trends: Increased preference for discreet, self-adjusting devices among users aged 40–60, with app-based tuning adoption exceeding 48%.

Pilot or Case Example: In 2023, a national audiology pilot achieved a 27% improvement in speech recognition accuracy using AI-driven adaptive fitting.

Competitive Landscape: Sonova leads with approximately 30% share, followed by Demant, WS Audiology, GN Store Nord, and Starkey.

Regulatory & ESG Impact: Supportive OTC regulations and energy-efficient chip mandates accelerating AI hearing aid adoption.

Investment & Funding Patterns: Over USD 1.1 billion invested globally between 2022–2024 in AI hearing technologies, with strong venture participation.

Innovation & Future Outlook: Integration with health monitoring platforms and predictive hearing loss analytics shaping next-generation devices.

AI-enabled hearing aids are primarily driven by clinical audiology (46%), followed by consumer OTC devices (34%) and occupational safety applications (20%). Recent innovations include real-time language translation and biometric hearing analytics. Regulatory clarity for OTC devices, rising disposable incomes, and aging demographics support regional demand, while future growth is shaped by cloud-connected AI models and preventive hearing health ecosystems.

The Hearing Aids with Artificial Intelligence Market holds strategic relevance as hearing healthcare transitions from reactive treatment to proactive, data-driven intervention. AI-powered hearing aids integrate adaptive algorithms that continuously learn from user environments, enabling personalized sound profiles and improved speech intelligibility. Deep learning-based noise classification delivers up to 40% improvement compared to traditional digital signal processing standards, positioning AI hearing aids as a benchmark technology in audiology.

From a regional perspective, North America dominates in volume due to established clinical infrastructure, while Europe leads in adoption with over 52% of eligible hearing-impaired adults using digitally advanced or AI-enabled devices. Asia Pacific shows accelerated uptake, supported by urbanization and expanding middle-income populations. By 2027, on-device edge AI processing is expected to reduce power consumption by 22%, improving battery life and daily usability.

Strategically, compliance and ESG considerations are influencing procurement and design decisions. Manufacturers are committing to sustainability metrics such as 25% recycled polymer usage and 30% reduction in packaging waste by 2030. In 2024, Denmark-based manufacturing initiatives achieved a 19% reduction in device carbon footprint through AI-optimized component design.

Short-term pathways emphasize interoperability with smartphones, tele-audiology platforms, and health monitoring systems. By 2028, predictive AI hearing loss analytics are expected to improve early detection rates by 33%. These developments position the Hearing Aids with Artificial Intelligence Market as a pillar of resilience, regulatory alignment, and sustainable growth across global hearing healthcare ecosystems.

The Hearing Aids with Artificial Intelligence market dynamics are shaped by rapid technological innovation, evolving regulatory frameworks, and shifting consumer expectations. AI-driven sound processing, adaptive learning algorithms, and real-time environmental classification are redefining product differentiation. Demand is further influenced by demographic aging trends, increasing noise pollution, and heightened awareness of untreated hearing loss impacts. Regulatory support for over-the-counter hearing aids is expanding accessibility, while competitive pressures are accelerating innovation cycles. At the same time, supply chain digitization and semiconductor advancements are enabling compact, energy-efficient AI modules, reinforcing the market’s long-term structural momentum.

Personalization has emerged as a central growth driver in the Hearing Aids with Artificial Intelligence market. AI-enabled devices dynamically adapt to individual hearing profiles, environments, and usage behaviors, delivering up to 35% better speech comprehension in complex acoustic settings. In 2024, over 60% of new hearing aid users prioritized self-adjusting features and mobile app integration. AI-based learning models reduce manual audiologist interventions by nearly 28%, improving accessibility and lowering long-term care costs. These measurable benefits are accelerating adoption among first-time users and younger demographics, expanding the addressable market beyond traditional clinical segments.

Despite technological progress, affordability remains a limiting factor. AI-enabled hearing aids cost 25–40% more than conventional digital models, restricting adoption in price-sensitive regions. Additionally, complexity in setup and calibration poses challenges for elderly users, with nearly 18% reporting initial usability difficulties. Limited reimbursement coverage in emerging economies further constrains penetration. These factors slow mass-market diffusion, particularly in rural and low-income populations, where basic amplification devices remain the primary choice.

Tele-audiology integration presents a significant opportunity for the Hearing Aids with Artificial Intelligence market. Remote fitting and AI-driven diagnostics enable clinicians to serve 30–40% more patients without geographic constraints. In 2024, over 45% of AI hearing aid manufacturers embedded cloud-based tuning platforms, reducing follow-up visit requirements by 32%. Expanding broadband access and smartphone penetration amplify this opportunity, particularly in underserved regions, supporting scalable, cost-efficient hearing care delivery models.

AI hearing aids rely heavily on user data, raising concerns around privacy, cybersecurity, and cross-border data compliance. Inconsistent regulatory standards across regions increase certification timelines by up to 20%. Manufacturers must invest significantly in secure data architectures and compliance audits, elevating operational costs. These challenges complicate global rollout strategies and require continuous alignment with evolving digital health regulations.

AI-Driven Real-Time Sound Environment Classification: Over 68% of newly launched AI hearing aids in 2024 feature real-time acoustic scene detection, enabling automatic switching between noise profiles and improving speech clarity by 32%.

Expansion of Over-the-Counter AI Hearing Devices: OTC AI hearing aids represented 26% of unit sales in developed markets in 2024, reducing average access time to hearing solutions by 41%.

Integration with Health Monitoring Ecosystems: Approximately 34% of AI hearing aids now include biometric tracking features such as fall detection and activity monitoring, increasing daily wear time by 29%.

Edge AI and Low-Power Chip Adoption: Adoption of edge AI processors improved battery efficiency by 24% in 2023–2024, supporting all-day usage without recharging.

The Hearing Aids with Artificial Intelligence market is segmented by type, application, and end-user, reflecting diverse adoption pathways across clinical and consumer environments. Product differentiation is driven by AI processing capabilities and connectivity features. Applications range from medical audiology to consumer wellness, while end-user demand varies across age groups, healthcare providers, and occupational safety users. Segmentation insights highlight how technological complexity and personalization requirements influence purchasing decisions.

AI-enabled behind-the-ear devices account for approximately 44% of adoption due to higher processing capacity and battery efficiency, while in-the-ear AI hearing aids represent 31%. However, completely-in-canal AI devices are the fastest growing, expected to expand at over 11% CAGR, driven by demand for discreet form factors. Other types, including receiver-in-canal and bone-conduction AI devices, collectively contribute 25%, serving niche clinical needs.

In 2024, a national health technology program reported AI-powered behind-the-ear devices improving speech recognition accuracy for over 1.2 million users.

Clinical audiology remains the leading application with a 48% share, supported by hospital and private clinic demand. Consumer wellness applications are growing fastest, projected above 12% CAGR, fueled by OTC availability and smartphone integration. Occupational safety and assisted living applications collectively account for 40%. In 2024, over 36% of adults with mild hearing loss opted for consumer AI hearing aids for daily use.

In 2024, AI-assisted hearing solutions were deployed across more than 140 healthcare facilities, enhancing patient fitting efficiency by 30%.

Adults aged 60+ represent the largest end-user group at 54%, driven by age-related hearing loss prevalence. However, users aged 40–59 are the fastest-growing segment, expanding at over 10% CAGR due to early intervention awareness. Pediatric and occupational users collectively account for 36%, supported by school screening programs and workplace safety mandates. In 2024, 42% of private audiology clinics reported increased demand for AI-enabled hearing aids.

In 2025, a national healthcare digitization initiative enabled AI hearing aid adoption across 500+ clinics, reducing fitting time by 26%.

North America accounted for the largest market share at 41.6% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2025 and 2032.

North America recorded over 18.4 million active AI-enabled hearing aid users in 2024, supported by strong clinical infrastructure and OTC device adoption. Europe followed with a 29.3% share, driven by reimbursement-backed audiology services and regulatory-backed digital health penetration. Asia-Pacific crossed 14.2 million unit shipments in 2024, led by China, Japan, and India, where smartphone-linked AI hearing aids are gaining traction. South America and Middle East & Africa jointly accounted for 9.8%, with urban adoption rates exceeding 21% in tier-1 cities, supported by expanding private healthcare networks and improving affordability.

How is advanced healthcare digitization accelerating AI-driven hearing solutions?

The region accounted for approximately 41.6% of the global Hearing Aids with Artificial Intelligence market in 2024, reflecting high adoption across healthcare, senior living, and consumer wellness segments. Over 62% of audiology clinics deploy AI-enabled fitting and sound calibration tools. Regulatory support for OTC hearing aids increased first-time adoption by 28% among adults aged 40–55. Digital transformation trends include app-based tuning, edge AI processors, and cloud audiology platforms. A leading local player introduced AI-powered speech-in-noise optimization, improving word recognition accuracy by 34%. Consumer behavior shows strong preference for discreet, rechargeable, and self-adjusting devices, with healthcare and assisted living facilities driving institutional demand.

Why is explainable and compliant AI shaping next-generation hearing devices?

Europe captured nearly 29.3% of the Hearing Aids with Artificial Intelligence market in 2024, with Germany, the UK, and France contributing over 64% of regional demand. Public reimbursement programs supported adoption among seniors, with digital hearing aid penetration exceeding 57%. Regulatory frameworks emphasize transparency, cybersecurity, and lifecycle sustainability, driving demand for explainable AI algorithms. Adoption of machine-learning-based sound profiling improved patient fitting efficiency by 31%. A regional manufacturer expanded AI-enabled eco-designed hearing aids using recyclable polymers. Consumers prioritize clinically validated, regulation-compliant devices, reinforcing trust-driven purchasing behavior.

What makes mobile-first AI hearing solutions scale rapidly across emerging economies?

Asia-Pacific ranked as the fastest-expanding region by volume, accounting for over 14.2 million AI-enabled hearing aid units in 2024. China, Japan, and India jointly represented 71% of regional consumption. Manufacturing hubs increasingly integrate AI chipsets locally, reducing production costs by 18%. Innovation clusters in Japan and South Korea focus on miniaturization and real-time language enhancement. A domestic player launched smartphone-controlled AI hearing aids, achieving over 420,000 downloads of its companion app. Consumer behavior is shaped by e-commerce penetration and mobile health platforms, with over 46% of buyers purchasing digitally.

How is urban healthcare expansion enabling AI-based hearing care access?

South America held nearly 6.1% of the global market in 2024, led by Brazil and Argentina. Private healthcare investments increased audiology clinic density by 19% in metropolitan areas. Government tax incentives on medical devices supported AI hearing aid imports. Digital sound processing adoption improved speech clarity for multilingual environments by 27%. A regional distributor partnered with AI developers to localize language processing features. Consumers increasingly demand language-adaptive and media-compatible hearing aids, aligning adoption with entertainment and communication usage.

Why is healthcare modernization unlocking AI hearing technology adoption?

The region accounted for 3.7% of global demand in 2024, with UAE and South Africa leading adoption. Smart hospital initiatives increased AI medical device installations by 24%. Trade partnerships improved device availability across Gulf countries. AI hearing aids with heat-resistant components gained traction, improving durability by 22%. A regional healthcare group integrated AI audiology platforms across 35 clinics. Consumer behavior reflects rising demand for premium, clinic-fitted solutions in urban centers and basic AI-enabled devices in emerging markets.

United States Hearing Aids with Artificial Intelligence Market – 38.2%: Strong production capacity, advanced audiology infrastructure, and early OTC adoption.

Germany Hearing Aids with Artificial Intelligence Market – 14.6%: Robust reimbursement systems and high clinical adoption of AI-based hearing solutions.

The Hearing Aids with Artificial Intelligence market exhibits a moderately consolidated structure with over 45 active global and regional competitors. The top five companies collectively account for approximately 68% of total market presence, reflecting strong brand concentration and technology leadership. Competitive strategies emphasize AI algorithm innovation, miniaturization, battery efficiency, and ecosystem integration. Product launch cycles shortened to 18–24 months, driven by rapid advancements in edge AI chips and software updates. Strategic partnerships between audiology networks and technology firms increased by 26% in 2023–2024. Mergers focused on software capability acquisition rather than manufacturing scale. Competition increasingly centers on user experience metrics, such as speech clarity improvement percentages and fitting time reduction, reinforcing innovation-led differentiation.

Sonova Holding AG

Demant A/S

WS Audiology

GN Store Nord

Starkey Laboratories

Cochlear Limited

Eargo Inc.

Audicus

Audina Hearing Instruments

Rexton

Sebotek Hearing Systems

Technological advancement in the Hearing Aids with Artificial Intelligence market centers on deep learning-driven sound classification, edge computing, and real-time personalization. Modern AI hearing aids analyze over 200 acoustic parameters per second, enabling automatic adaptation across environments. Edge AI processors reduced latency by 35% while improving battery efficiency by 24%. Neural network-based noise suppression improved speech recognition in noisy environments by up to 40%. Integration with smartphones allows continuous firmware updates and behavioral learning. Emerging technologies include biometric monitoring, fall detection, and predictive hearing loss analytics. Bluetooth LE Audio adoption improved streaming efficiency by 30%. Cloud-based AI fitting platforms reduced clinic visit frequency by 32%. These technologies collectively enhance user satisfaction, clinical efficiency, and long-term hearing health management.

In August 2024, Sonova launched a new AI-powered hearing platform using real-time environment classification across more than 4,000 sound scenarios, improving speech understanding in noise by 36%. Source: www.sonova.com

In May 2024, GN Store Nord introduced next-generation AI hearing aids with integrated Bluetooth LE Audio, reducing power consumption by 20% and enhancing streaming stability. Source: www.gn.com

In October 2023, Starkey Laboratories expanded its AI-driven health monitoring hearing aids, enabling fall detection and activity tracking across 500,000 active users. Source: www.starkey.com

In March 2023, Demant announced deployment of machine-learning-based fitting software across 3,200 clinics, cutting initial fitting time by 28%. Source: www.demant.com

The Hearing Aids with Artificial Intelligence Market Report provides a comprehensive assessment of product types, applications, technologies, and end-user adoption patterns across major global regions. The scope covers AI-enabled behind-the-ear, in-the-ear, and completely-in-canal devices, including clinical-grade and OTC solutions. Applications analyzed span audiology clinics, consumer wellness, occupational safety, and assisted living environments. The report evaluates technology layers such as edge AI processors, cloud-based fitting platforms, deep learning noise suppression, and wireless connectivity standards. Geographic coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with country-level insights for key markets. Emerging niches such as pediatric AI hearing aids, multilingual sound processing, and health-monitoring-enabled devices are included. The report supports strategic decision-making by outlining competitive positioning, innovation pathways, regulatory considerations, and adoption metrics relevant to manufacturers, investors, healthcare providers, and policymakers.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 3,125.4 Million |

|

Market Revenue in 2032 |

USD 6,412.7 Million |

|

CAGR (2025 - 2032) |

9.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Sonova Holding AG, Demant A/S, WS Audiology, GN Store Nord, Starkey Laboratories, Cochlear Limited, Eargo Inc., Audicus, MED-EL, Widex, Phonak, Audina Hearing Instruments, Rexton, Sebotek Hearing Systems |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |