Reports

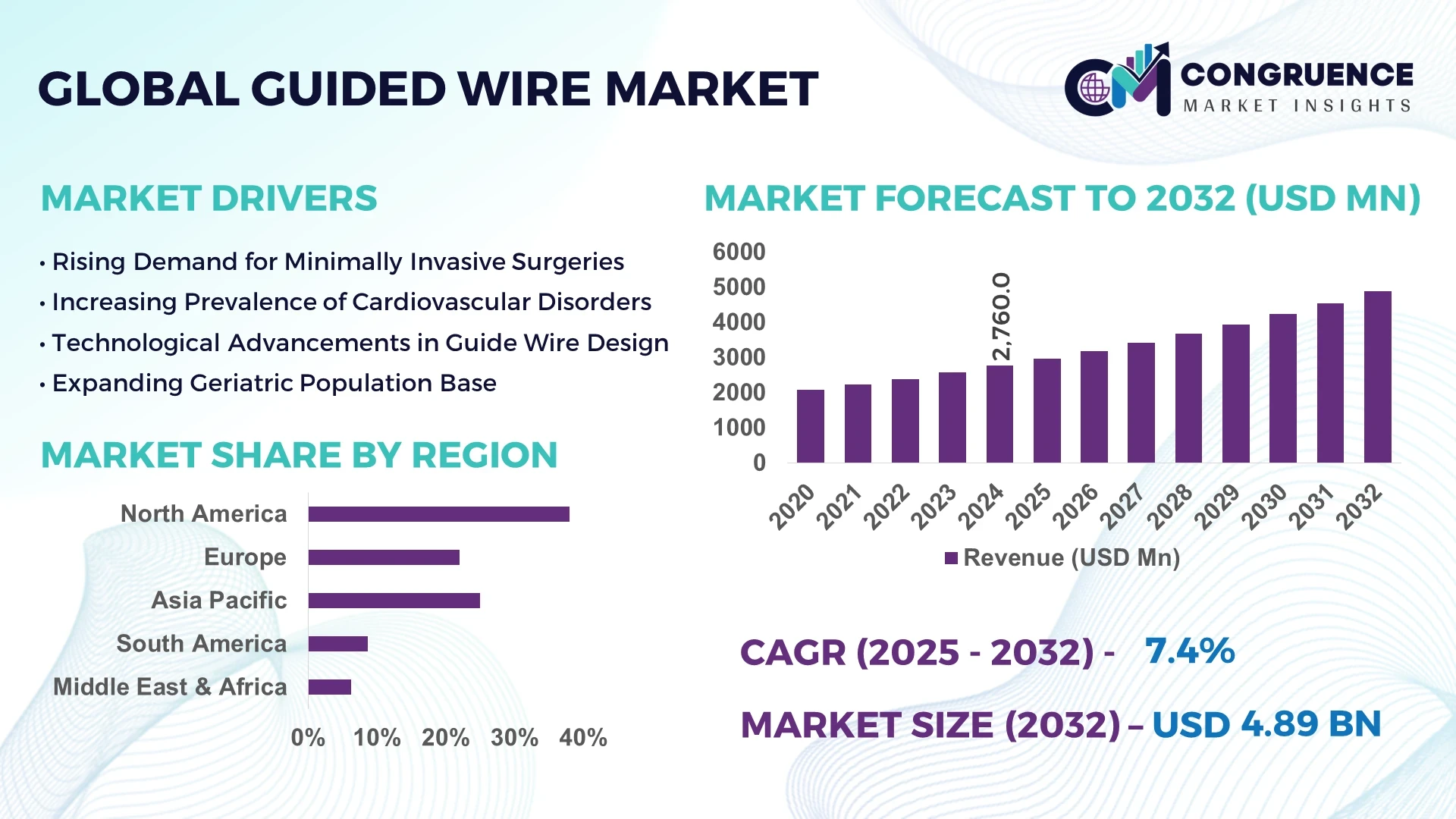

The Global Guide Wire Market was valued at USD 2,760 million in 2024 and is anticipated to reach a value of USD 4,885.8 million by 2032, expanding at a CAGR of 7.4% between 2025 and 2032.

The United States dominates the global Guide Wire Market, accounting for a significant share of overall revenue in 2024. The country shows widespread adoption of advanced guide wire technologies across cardiovascular and neurovascular procedures, with thousands of hospitals and specialty clinics utilizing these devices annually.

The Guide Wire Market is witnessing substantial growth driven by increasing prevalence of cardiovascular diseases and minimally invasive surgeries worldwide. In 2024, over 12 million guide wires were estimated to be used globally across various medical applications. Technological advancements such as coated and steerable guide wires have improved procedural success rates and reduced complications. The rising number of catheterization procedures, which surpassed 7 million in 2024, continues to propel market demand. Furthermore, emerging markets show a steady increase in guide wire consumption, contributing to expanding market size, with a focus on cost-effective and versatile guide wire options across different therapeutic areas.

Artificial Intelligence (AI) is revolutionizing the guide wire market by enhancing procedural precision and operational efficiency. AI-driven systems are now assisting clinicians with real-time navigation and tracking of guidewires during intricate procedures. These intelligent systems utilize advanced algorithms to interpret imaging data, enabling better visualization and refined control over wire positioning within vascular pathways. Innovative machine learning models are being trained to automatically identify and follow the trajectory of guidewires in fluoroscopic imaging, significantly improving the success rate of minimally invasive interventions. These technologies reduce the dependence on manual interpretation and enhance the decision-making process during surgeries. Furthermore, the application of AI in robotic systems is allowing partial automation of guidewire navigation, particularly in complex anatomical structures, thereby reducing human error.

Predictive analytics, powered by AI, are also playing a role in pre-operative planning by forecasting possible procedural challenges. This leads to better preparation, shorter operation times, and improved patient outcomes. As hospitals increasingly adopt AI-enhanced surgical tools, the integration of intelligent guidewire systems is becoming a key trend across global healthcare systems.

“In January 2025, researchers introduced 'SplineFormer,' a transformer-based AI model designed for autonomous endovascular navigation. This model predicts the continuous shape of guidewires, achieving a 50% success rate in cannulating the brachiocephalic artery during robotic procedures, marking a significant advancement in AI-assisted medical interventions.”

The demand for minimally invasive procedures has surged due to their reduced recovery times, lower complication risks, and increased procedural success rates. Guide wires are a critical component in such interventions, particularly in cardiovascular and neurovascular procedures. Globally, over 20 million interventional cardiology procedures are performed annually, most requiring guide wires for catheter placement. Additionally, advancements in steerability and torque response have made guide wires indispensable tools in complex surgeries. This growing trend in patient and clinician preference toward non-invasive alternatives is directly boosting guide wire demand across hospitals and specialty clinics worldwide.

While developed regions are rapidly integrating advanced guide wire technologies, many developing countries face barriers related to cost and reimbursement. The price of premium guide wires—enhanced with special coatings and integrated sensors—can significantly increase the overall procedural cost. Moreover, reimbursement structures in several healthcare systems do not cover advanced interventional devices adequately, deterring hospitals from adopting cutting-edge guide wire solutions. These economic constraints, particularly in cost-sensitive markets, limit the growth potential and widespread adoption of newer technologies. Hospitals in low-resource settings often rely on basic, reusable wires, impacting patient outcomes and procedural success.

The integration of artificial intelligence and robotics into surgical environments presents a lucrative opportunity for the guide wire market. AI-driven imaging platforms are being employed to enhance real-time guide wire tracking and improve navigation precision. Robotic-assisted procedures are growing in popularity, with over 1.5 million such operations conducted globally every year. These systems increasingly rely on advanced guide wires equipped with smart sensors and responsive materials. As the demand for precision-driven surgeries rises, so does the need for next-generation guide wire technologies that can seamlessly integrate into AI-assisted workflows, offering improved safety and clinical efficiency.

One of the key challenges faced by manufacturers in the guide wire market is navigating the stringent regulatory landscape. Medical devices, especially those used in vascular interventions, must meet rigorous safety and efficacy standards before entering clinical use. Obtaining approvals from bodies like the FDA or CE often involves lengthy clinical trials, high costs, and extensive documentation. This delays time-to-market for innovative guide wire solutions and deters smaller companies from investing in advanced R&D. Furthermore, any deviation in product materials or designs requires fresh validation, creating additional hurdles in bringing new technologies to the global marketplace.

• Advancements in Guide Wire Material Technology: Recent developments in guide wire materials have significantly improved their performance and durability. Manufacturers are increasingly using nitinol alloys and coated stainless steel to enhance flexibility, kink resistance, and biocompatibility. These material innovations are enabling guide wires to navigate complex vascular pathways more effectively, thereby improving procedural outcomes. The demand for specialized coatings like hydrophilic and hydrophobic finishes has also risen, reducing friction during insertion and minimizing vessel trauma.

• Growth in Minimally Invasive Surgical Procedures: The rising prevalence of cardiovascular diseases and peripheral artery disease is fueling the demand for guide wires used in minimally invasive interventions. Surgeons are increasingly adopting guide wires for procedures such as angioplasty, stent placements, and neurovascular interventions due to their ability to facilitate precise catheter navigation. This trend is evident in hospitals and ambulatory surgical centers worldwide, with an estimated 15 million endovascular procedures performed annually requiring guide wire support.

• Integration of Smart Technologies: The guide wire market is witnessing a shift toward smart guide wires embedded with sensors and AI-driven navigation systems. These innovations enhance real-time feedback during surgeries, allowing for better control and reduced risks. Robotic-assisted guide wire navigation is becoming more prevalent, particularly in complex cardiovascular and neurological surgeries. This trend is expected to improve patient outcomes by providing surgeons with enhanced visualization and precision.

• Expansion in Emerging Markets: Emerging economies in Asia-Pacific, Latin America, and the Middle East are showing increasing adoption of advanced guide wire technologies. Rising healthcare investments, expanding hospital infrastructure, and growing awareness about minimally invasive procedures contribute to this trend. The availability of cost-effective guide wire options and growing government initiatives to improve healthcare accessibility are driving market penetration in these regions.

The guide wire market is segmented by type, application, and end-user to better understand its diverse demand landscape. Different guide wire types cater to varying clinical needs, while applications span multiple surgical specialties such as cardiology, urology, and radiology. End users include hospitals, ambulatory surgical centers, and specialty clinics, each driving market growth based on procedural volume and technological adoption. This segmentation highlights key market dynamics, revealing which segments are leading and growing rapidly due to evolving clinical preferences and technological innovations.

The guide wire market is classified primarily into stainless steel guide wires, nitinol guide wires, and polymer-coated guide wires. Stainless steel guide wires hold the largest share due to their affordability and widespread use in general diagnostic and interventional procedures. However, nitinol guide wires are the fastest-growing segment, attributed to their superior flexibility, shape memory, and kink resistance, making them ideal for navigating complex and tortuous vascular anatomy. Polymer-coated guide wires, featuring hydrophilic or hydrophobic coatings, are also gaining traction for their reduced friction and enhanced maneuverability during procedures. In 2024, nitinol guide wires accounted for approximately 35% of market revenue, reflecting increased clinician preference for advanced materials in critical interventions.

Cardiovascular procedures dominate the application segment, representing over 50% of total guide wire demand globally. This is driven by the high volume of angioplasty, stenting, and diagnostic catheterization procedures. The neurovascular segment is witnessing the fastest growth, fueled by rising incidences of stroke and aneurysms requiring minimally invasive interventions. Guide wires used in urology and peripheral vascular procedures also contribute significantly, but growth rates there are moderate compared to cardiovascular and neurovascular applications. The expanding adoption of endovascular therapies in stroke treatment has pushed neurovascular guide wire sales by an estimated 18% in recent years.

Hospitals are the largest end-user segment for guide wires, accounting for nearly 70% of market consumption due to the high volume of inpatient surgeries and diagnostic interventions. Ambulatory surgical centers (ASCs) represent the fastest-growing segment, driven by a shift toward outpatient minimally invasive procedures. ASCs offer cost-effective treatment options, shorter patient recovery times, and increased procedural efficiency, which boosts guide wire demand. Specialty clinics focused on cardiology and interventional radiology also contribute notably, especially in urban areas with advanced healthcare infrastructure. The expanding outpatient care model and growing healthcare access in emerging regions are expected to drive sustained growth in ASC-based guide wire usage.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2025 and 2032.

North America dominates due to advanced healthcare infrastructure and widespread adoption of minimally invasive surgical procedures that extensively use guide wires. Asia-Pacific’s rapid growth is driven by increasing prevalence of cardiovascular diseases, rising healthcare expenditure, and expanding medical device manufacturing hubs. Europe holds a significant share with steady demand fueled by technological advancements and stringent regulatory frameworks. South America and Middle East & Africa regions exhibit moderate growth, supported by healthcare modernization and growing awareness of advanced treatment options involving guide wires.

“Leading Innovation and Advanced Adoption in Guide Wire Technologies”

North America leads with a 38% market share, largely propelled by the United States, which alone contributes nearly 30% of global demand. The region benefits from high procedural volumes in cardiovascular, neurovascular, and peripheral interventions. Advancements like hydrophilic coatings and flexible guide wire designs improve procedural success rates, driving adoption. Canada and Mexico show steady uptake due to healthcare infrastructure expansion. The focus on reducing patient recovery time through minimally invasive techniques continues to fuel guide wire market growth. Emerging technologies such as sensor-integrated guide wires are gaining traction within North American hospitals and specialty clinics.

“Driving Precision and Expansion in Guide Wire Applications”

Europe accounts for approximately 25% of the global guide wire market, with Germany and France as key contributors. The region emphasizes high safety standards and clinical efficacy, promoting adoption of shape-memory alloys and coated guide wires. Countries like the UK and Italy are increasing use of advanced guide wire technologies in interventional cardiology and neurology. European healthcare providers invest heavily in upgrading surgical equipment, boosting guide wire demand. Additionally, stringent regulatory oversight ensures only high-quality guide wires are available, enhancing market trust. There is a rising preference for disposable and single-use guide wires to prevent infections.

“Rapid Growth Fueled by Expanding Healthcare Infrastructure”

Asia-Pacific holds about 22% of the global guide wire market share and is the fastest-growing region. China and Japan dominate with large patient pools requiring cardiovascular and neurological interventions. India and South Korea are expanding healthcare access, leading to greater utilization of guide wires in minimally invasive procedures. The region benefits from increasing domestic production of cost-effective guide wires, which lowers overall healthcare costs. Government initiatives aimed at improving rural healthcare infrastructure also drive demand. The adoption of newer technologies such as coated and steerable guide wires is increasing across major hospitals in urban centers.

“Emerging Markets Embracing Modernization and Medical Advancements”

South America commands around 8% of the global guide wire market, led by Brazil and Argentina. Growing prevalence of cardiovascular diseases and improving healthcare infrastructure contribute to steady demand. The adoption of hydrophilic and nitinol guide wires is rising as hospitals modernize. Expanded health insurance coverage in Brazil allows greater patient access to advanced interventional procedures, driving guide wire sales. Regional manufacturers are beginning to produce more affordable guide wires, helping penetrate lower-income markets. The increase in minimally invasive surgeries across urban hospitals supports market growth in South America.

“Capitalizing on Healthcare Investments and Market Expansion”

The Middle East & Africa region holds approximately 7% of the guide wire market share, with the UAE and Saudi Arabia leading adoption. Significant investments in healthcare modernization and the expansion of specialty medical centers encourage the use of advanced guide wires. Rising cardiovascular and neurological disorder prevalence drives procedural demand. South Africa is enhancing healthcare access by incorporating newer guide wire technologies in public and private hospitals. The demand for coated and flexible guide wires is increasing as minimally invasive interventions become more common. Regional focus on reducing surgical complications boosts guide wire innovation uptake.

United States – 30% share: Leading due to well-established healthcare infrastructure and high volume of minimally invasive cardiovascular procedures.

China – 18% share: Rapid market expansion driven by increasing cardiovascular disease burden and growing healthcare access.

The guide wire market is characterized by intense competition among global players, driven by continuous innovation and product differentiation. Companies focus on developing technologically advanced guide wires with improved flexibility, durability, and enhanced coatings to minimize complications during procedures. Strategic partnerships and collaborations with healthcare providers and research institutions are common to accelerate product development. Market leaders invest significantly in expanding their product portfolios to cover various medical applications, including cardiovascular, neurovascular, and peripheral interventions. Additionally, mergers and acquisitions are prevalent strategies to increase market share and geographic presence. The increasing demand for minimally invasive procedures is encouraging players to innovate in guide wire design and materials, including hydrophilic coatings and nitinol cores. Companies also emphasize compliance with stringent regulatory standards across different regions to maintain product quality and safety. Competitive pricing strategies and expanding manufacturing capabilities, particularly in emerging markets, further intensify rivalry in the global guide wire market.

Terumo Corporation

Boston Scientific Corporation

Medtronic plc

Cook Medical Inc.

B. Braun Melsungen AG

Abbott Laboratories

Cordis Corporation

Asahi Intecc Co., Ltd.

Nipro Corporation

MicroVention, Inc.

The guide wire market is witnessing significant technological advancements aimed at enhancing precision, safety, and ease of use during minimally invasive procedures. Modern guide wires are increasingly designed with advanced core materials such as nitinol and stainless steel, offering superior flexibility and torque control. Innovations in hydrophilic and hydrophobic coatings have improved lubricity, reducing friction and enabling smoother navigation through complex vascular pathways. Additionally, the integration of radiopaque markers enhances visibility under fluoroscopy, allowing physicians to accurately track the wire’s position during interventions.

Recent developments include the use of braided and coiled shaft designs, which improve kink resistance and pushability, essential for reaching difficult anatomical regions. Smart guide wires embedded with sensors are also emerging, providing real-time feedback on pressure, temperature, and flow, which supports better clinical decision-making and patient outcomes. Furthermore, advancements in microfabrication technologies enable the production of ultra-thin guide wires that can access smaller vessels with minimal trauma.

The rise of robotic-assisted surgeries is pushing the development of guide wires compatible with automated systems, improving procedural precision. Additive manufacturing or 3D printing technologies are beginning to be explored for customized guide wire production, offering tailored solutions for specific patient anatomies. These technological trends are shaping the future of the guide wire market, emphasizing safer, more effective, and patient-centric interventions.

In June 2024, Haemonetics Corp. received CE mark certification for its Savvywire, a pioneering sensor-guided, three-in-one guidewire tailored for transcatheter aortic valve implantation (TAVI). This advancement sets new benchmarks for innovation in cardiovascular interventions.

In September 2024, Integer Holdings Corporation unveiled a significant expansion of its guidewire manufacturing facility in New Ross, County Wexford, Ireland. With a capital infusion of USD 60 million, the 80,000 sq. ft. expansion boosts the facility's manufacturing capacity by over 70%, strengthening the industry's supply chain resilience.

In March 2024, Baylis Medical Technologies announced the launch of its new PowerWire Pro guidewire, designed to facilitate venous stent recanalization for total occlusions. This advanced device provides better durability and flexibility, enhancing procedural success rates.

In April 2024, Teleflex expanded its structural heart portfolio by launching the limited market release of the Wattson temporary pacing guidewire. This innovative guidewire was designed to introduce and position catheters and other interventional devices within the heart's chambers, enhancing procedural efficiency.

The Guide Wire Market report offers a comprehensive analysis of the global market landscape, covering key segments including product types, applications, and end-user industries. It examines various guide wire types such as stainless steel, nitinol, and polymer-coated wires, highlighting their specific uses in cardiovascular, neurovascular, and peripheral interventions. The report delves into applications spanning diagnostic procedures, therapeutic interventions, and minimally invasive surgeries, offering detailed insights into market demand patterns. Geographically, the report covers major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing regional market size, growth drivers, and technological trends. It identifies leading countries contributing to the market share and tracks regional manufacturing capacities and regulatory environments influencing market dynamics.

In addition, the report discusses key market drivers such as technological innovations, rising prevalence of cardiovascular diseases, and increasing preference for minimally invasive surgical procedures. Challenges like stringent regulatory requirements and high manufacturing costs are also explored. The competitive landscape section profiles prominent global players and their strategic initiatives, including mergers, acquisitions, and new product launches. Overall, the report serves as a vital resource for manufacturers, investors, and healthcare professionals seeking to understand market opportunities, risks, and emerging trends in the guide wire industry worldwide.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2760 Million |

|

Market Revenue in 2032 |

USD 4885.8 Million |

|

CAGR (2025 - 2032) |

7.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Terumo Corporation, Boston Scientific Corporation, Medtronic plc, Cook Medical Inc., B. Braun Melsungen AG, Abbott Laboratories, Cordis Corporation, Asahi Intecc Co., Ltd., Nipro Corporation, MicroVention, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |