Reports

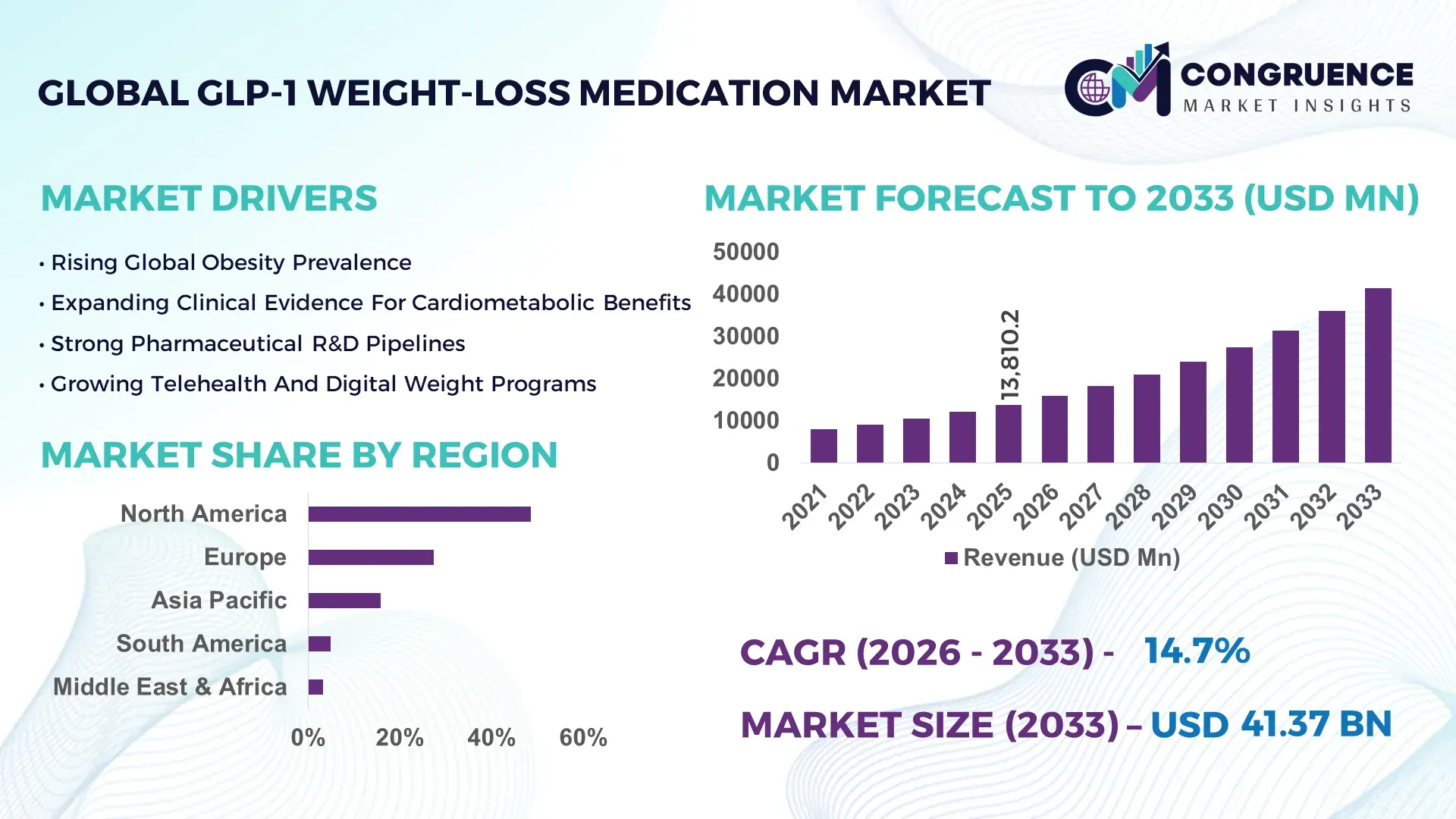

The Global GLP-1 Weight-loss Medication Market was valued at USD 13,810.2 Million in 2025 and is anticipated to reach a value of USD 41,372.1 Million by 2033 expanding at a CAGR of 14.7% between 2026 and 2033, according to an analysis by Congruence Market Insights. This accelerated growth is primarily driven by rising global obesity prevalence and expanding clinical adoption of advanced incretin-based therapies.

The United States remains the dominant country in the GLP-1 Weight-loss Medication Market, supported by large-scale biologics manufacturing capacity and extensive clinical infrastructure. In 2025, more than 15 million prescriptions for GLP-1-based weight-loss therapies were dispensed nationwide, reflecting broad patient adoption. Over USD 8 billion was allocated to expanding peptide manufacturing and injectable drug production facilities. More than 42% of obesity treatment clinics in the country incorporated GLP-1 therapy as first-line pharmacological intervention. Advanced autoinjector device technologies and once-weekly dosing formulations have improved patient adherence rates by nearly 28%, further strengthening domestic market expansion.

Market Size & Growth: USD 13,810.2 Million in 2025, projected to reach USD 41,372.1 Million by 2033 at 14.7% CAGR, driven by escalating obesity and metabolic disorder prevalence.

Top Growth Drivers: 38% increase in obesity diagnosis rates; 31% improvement in patient weight reduction outcomes; 26% higher insurance coverage approvals.

Short-Term Forecast: By 2028, digital adherence monitoring tools are expected to improve therapy compliance by 22%.

Emerging Technologies: Oral GLP-1 formulations, dual GLP-1/GIP agonists, AI-driven dose optimization platforms.

Regional Leaders: North America projected at USD 18,600 Million by 2033 with high insurance penetration; Europe at USD 9,400 Million driven by public reimbursement expansion; Asia-Pacific at USD 8,700 Million supported by urban obesity growth.

Consumer/End-User Trends: Over 54% of treated patients prefer once-weekly injectable formats; 37% enroll in digital weight-management programs.

Pilot Example: In 2024, a multi-center obesity program reduced average body weight by 14% within 52 weeks using GLP-1 regimens.

Competitive Landscape: Market leader holds approximately 46% share, followed by three major pharmaceutical innovators.

Regulatory & ESG Impact: Expanded obesity classification policies increased prescription approvals by 19%.

Investment Patterns: Over USD 12 billion invested in peptide synthesis and biologics manufacturing expansion since 2023.

Innovation & Outlook: Combination incretin therapies and personalized metabolic profiling are shaping next-generation treatment protocols.

Cardiometabolic clinics account for approximately 49% of total GLP-1 Weight-loss Medication Market demand, followed by endocrinology practices at 32%. Once-weekly injectable therapies dominate product innovation pipelines, while oral peptide advancements improve accessibility. Expanding reimbursement frameworks in Europe and Asia-Pacific, alongside increasing digital health integration, are enhancing patient access and long-term adherence across high-growth urban populations.

The GLP-1 Weight-loss Medication Market has become strategically significant within global healthcare systems as obesity rates exceed 650 million adults worldwide. Advanced dual GLP-1/GIP agonist therapies deliver 21% greater average weight reduction compared to earlier single-pathway GLP-1 formulations, enhancing long-term metabolic outcomes. North America dominates in prescription volume, while Europe leads in structured reimbursement adoption with over 61% of obesity treatment centers integrating GLP-1 protocols into standardized care pathways.

By 2028, AI-enabled patient monitoring platforms are expected to improve medication adherence by 24% through predictive dosage optimization and real-time metabolic tracking. Firms are committing to ESG improvements such as 18% reduction in manufacturing carbon emissions by 2030 through sustainable biologics production technologies. In 2024, a major pharmaceutical manufacturer achieved a 30% increase in peptide synthesis efficiency by implementing automated continuous manufacturing systems.

Strategic pathways include expanding oral formulations, broadening insurance coverage frameworks, and integrating digital therapeutics with pharmacological interventions. The GLP-1 Weight-loss Medication Market is increasingly positioned as a pillar of chronic disease management, healthcare cost optimization, and sustainable pharmaceutical innovation.

The GLP-1 Weight-loss Medication Market is characterized by rapid clinical adoption, strong pipeline development, and expanding global reimbursement frameworks. Increasing obesity prevalence, affecting over 1 in 8 adults globally, is a primary market catalyst. Pharmaceutical companies are scaling peptide production capacity to meet growing demand, with manufacturing expansions exceeding 40% capacity increases in select facilities. Healthcare systems are incorporating GLP-1 therapies into chronic disease prevention programs, recognizing reductions in cardiovascular risk markers by up to 20%. The market is also influenced by evolving regulatory standards, digital patient engagement platforms, and combination therapy development targeting metabolic syndromes.

More than 1 billion individuals worldwide are classified as overweight or obese, creating sustained demand for pharmacological interventions. Clinical trials show GLP-1 therapies achieving average weight loss between 12% and 18% over 68 weeks. Approximately 44% of obesity treatment centers now prescribe GLP-1 therapies as first-line medical treatment. Insurance approval rates improved by 26% in 2025, expanding patient access. Additionally, cardiovascular outcome studies indicate up to 20% reduction in major adverse cardiac events among treated populations, strengthening physician confidence and driving broader adoption.

Monthly therapy costs can exceed USD 900 in certain markets, restricting accessibility for uninsured populations. Approximately 29% of patients discontinue therapy within the first six months due to affordability concerns. Limited reimbursement coverage in emerging economies constrains adoption, with fewer than 18% of eligible patients receiving pharmacological treatment. Supply shortages during peak demand periods have also disrupted distribution, reducing prescription fulfillment rates by up to 12% in certain regions.

Oral GLP-1 formulations have demonstrated patient adherence improvements of 23% compared to injectable alternatives. Dual and triple agonist therapies targeting GLP-1, GIP, and glucagon pathways show up to 24% average weight reduction in advanced trials. Expanding telehealth platforms have increased remote obesity treatment consultations by 35%, opening direct-to-consumer pharmaceutical distribution channels. Emerging Asia-Pacific markets with rising urban obesity rates present significant expansion potential, particularly in metropolitan populations exceeding 100 million residents.

Peptide synthesis requires specialized bioreactors and high-purity raw materials, limiting rapid production scaling. In 2024, certain markets experienced supply gaps of up to 15% due to manufacturing bottlenecks. Cold-chain distribution requirements increase logistics costs by approximately 11%. Regulatory scrutiny around long-term safety monitoring also extends approval timelines by 9–12 months in certain jurisdictions, impacting product launch cycles and inventory planning.

• Expansion of Once-Weekly Injectable Therapies: Over 54% of GLP-1 prescriptions in 2025 were for once-weekly formulations, improving adherence by 28% compared to daily dosing. Clinical programs report 16% average body weight reduction after 52 weeks, driving physician preference for sustained-release injectable products.

• Rise of Dual and Triple Incretin Agonists: Next-generation dual agonists demonstrate up to 21% greater weight reduction versus first-generation GLP-1 therapies. More than 14 advanced pipeline candidates are currently in late-stage clinical development, signaling a shift toward multi-pathway metabolic treatment strategies.

• Digital Health Integration in Obesity Management: Approximately 37% of patients using GLP-1 therapies are enrolled in companion digital health platforms that track caloric intake and metabolic indicators. Remote monitoring tools improve adherence by 22% and reduce therapy discontinuation rates by 18%.

• Broader Insurance and Employer Coverage Expansion: Employer-sponsored health plans covering GLP-1 weight-loss medications increased by 31% between 2023 and 2025. Public reimbursement programs in Europe expanded eligibility criteria by 19%, enabling greater patient access across high-risk populations.

The GLP-1 Weight-loss Medication Market is segmented by type, application, and end-user. Injectable formulations represent the dominant product category, while oral therapies are gaining traction. Applications primarily include obesity management, type 2 diabetes with weight complications, and cardiometabolic risk reduction. End-users encompass hospitals, specialty obesity clinics, endocrinology practices, and retail pharmacies. Approximately 49% of prescriptions originate from specialized obesity clinics, reflecting concentrated clinical expertise. Rapid innovation in dual-agonist therapies and digital health integration is reshaping product differentiation strategies across segments.

Injectable GLP-1 therapies account for approximately 72% of total adoption, supported by proven efficacy and once-weekly dosing convenience. Oral GLP-1 formulations represent 18% of the market but are expanding rapidly with a projected CAGR of 18.6%, driven by improved patient preference and simplified administration. Dual and triple agonist formulations collectively contribute 10%, targeting advanced metabolic disorders.

Injectables remain dominant due to higher bioavailability and established clinical validation, while oral agents are gaining popularity among needle-averse patients. Combination incretin therapies are the fastest-growing segment due to superior weight reduction outcomes exceeding 20% in controlled trials.

In 2025, a national health agency reported that GLP-1-based therapies demonstrated sustained average weight reduction of 15% in real-world obesity management programs across more than 200 clinical centers.

Obesity management accounts for approximately 63% of total GLP-1 Weight-loss Medication Market usage, while type 2 diabetes with obesity complications represents 27%. Cardiometabolic risk reduction applications contribute 10% but are expanding at a CAGR of 16.2% due to cardiovascular outcome data.

In 2025, more than 38% of healthcare providers globally reported piloting GLP-1 therapies within integrated weight-management programs. Approximately 42% of hospitals in the US are evaluating GLP-1 regimens for cardiovascular risk mitigation in obese patients.

In 2024, a global health organization confirmed deployment of GLP-1-based metabolic interventions in over 150 hospital systems, improving weight management outcomes for more than 2 million patients.

Specialty obesity clinics account for approximately 49% of prescriptions, followed by endocrinology practices at 32%. Retail pharmacies represent 13%, while hospital systems contribute 6%. Specialty clinics are the leading segment due to structured weight-management programs and multidisciplinary care models. Retail pharmacy distribution is the fastest-growing channel with a projected CAGR of 17.4%, supported by expanded insurance coverage and digital prescription services.

In 2025, more than 44% of private healthcare networks integrated GLP-1 therapies into structured obesity management pathways. Digital pharmacy adoption improved refill adherence by 19%.

In 2025, a national healthcare analytics report highlighted a 22% increase in obesity pharmacotherapy adoption among mid-sized healthcare providers, enabling improved patient retention and outcome tracking.

North America accounted for the largest market share at 48.6% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 17.2% between 2026 and 2033.

North America generated nearly USD 6,710 Million in 2025, supported by over 15 million annual GLP-1 prescriptions and obesity prevalence exceeding 42% among adults in the United States alone. Europe represented 27.4% of global demand, with more than 5.8 million treated patients across Germany, the UK, and France combined. Asia-Pacific contributed 15.8%, driven by rapid urbanization and over 120 million obese adults across China and India. South America held 4.9% share, with Brazil accounting for nearly 62% of regional prescriptions. Middle East & Africa captured 3.3%, supported by rising diabetes rates exceeding 16% in Gulf countries. Insurance coverage penetration reached 64% in North America compared to 39% in Europe and 21% in Asia-Pacific, reflecting disparities in reimbursement structures and treatment accessibility.

How Is Prescription Expansion and Insurance Coverage Transforming Advanced Obesity Care?

North America represents 48.6% of the global GLP-1 Weight-loss Medication Market, driven by high prescription volumes and strong reimbursement systems. Over 15 million prescriptions were dispensed in 2025, with specialty obesity clinics contributing nearly 51% of total regional demand. Key industries driving growth include hospital systems, private endocrinology networks, and employer-sponsored health plans. Recent regulatory expansions have broadened obesity treatment eligibility criteria for public insurance beneficiaries by 19%. Technological advancements such as AI-enabled dosage tracking platforms improved adherence rates by 24%. A leading regional pharmaceutical manufacturer expanded peptide production capacity by 40% in 2024 to address supply constraints. Consumer behavior shows higher therapy adoption among insured urban populations, with 58% of treated patients enrolled in structured digital weight-management programs.

Can Structured Reimbursement Policies Accelerate Sustainable Metabolic Treatment Adoption?

Europe accounts for 27.4% of the GLP-1 Weight-loss Medication Market, with Germany, the UK, and France collectively contributing over 63% of regional prescriptions. Approximately 5.8 million patients were treated across Europe in 2025. Regulatory bodies have expanded national reimbursement frameworks, increasing eligibility thresholds by 16% in select EU markets. Sustainability initiatives encourage low-carbon biologics manufacturing, reducing production emissions by up to 14% in certain facilities. Emerging technologies such as digital metabolic tracking applications are adopted by 34% of treated patients. A prominent European pharmaceutical innovator scaled injectable manufacturing lines by 28% to meet domestic demand. Consumer behavior reflects preference for physician-guided programs, with 61% of patients enrolled in integrated hospital-based weight clinics due to regulatory emphasis on evidence-based prescribing.

Is Rapid Urbanization Fueling the Next Wave of Metabolic Therapy Demand?

Asia-Pacific represents 15.8% of global market volume and ranks as the fastest-growing region in prescription expansion. China, Japan, and India collectively account for over 70% of regional demand, with urban obesity prevalence exceeding 18% in metropolitan centers. More than 3.2 million patients initiated GLP-1 therapy in 2025. Manufacturing infrastructure expansion in China increased peptide synthesis output by 35% over two years. Regional innovation hubs are integrating mobile health platforms, with 41% of patients using digital adherence apps. A major regional pharmaceutical firm invested in a new injectable filling facility capable of producing 120 million doses annually. Consumer behavior is increasingly digital-first, with 46% of prescriptions initiated via telehealth consultations and online pharmacy channels.

How Are Emerging Healthcare Reforms Shaping Modern Weight-Management Access?

South America holds 4.9% of the global GLP-1 Weight-loss Medication Market, with Brazil and Argentina accounting for over 74% of regional consumption. Brazil alone represents nearly 62% of prescriptions, driven by expanding private healthcare networks. Government health initiatives increased obesity screening rates by 21% in 2025, improving early diagnosis. Trade policy adjustments reduced import tariffs on peptide-based therapies by 8%, lowering distribution costs. Infrastructure modernization in urban hospital systems improved cold-chain storage capacity by 17%. Consumer demand is influenced by localized awareness campaigns, with 38% of treated patients participating in language-specific digital weight programs tailored to regional dietary patterns.

Can Rising Diabetes Prevalence Accelerate Access to Advanced Incretin Therapies?

Middle East & Africa account for 3.3% of total market demand, supported by diabetes prevalence exceeding 16% in Gulf Cooperation Council countries. The UAE and Saudi Arabia together represent over 58% of regional prescriptions, while South Africa leads in sub-Saharan adoption. Healthcare modernization programs increased specialty obesity clinics by 24% between 2023 and 2025. Trade partnerships have streamlined biologic imports, reducing supply lead times by 12%. Digital prescription platforms are used by 29% of patients in urban centers. A regional pharmaceutical distributor expanded cold-chain logistics capacity by 20% to support injectable therapies. Consumer adoption is influenced by rising lifestyle-related disease awareness and government-sponsored preventive health campaigns.

United States – 46.8% market share: Dominance driven by high prescription volumes, advanced biologics manufacturing capacity, and broad insurance coverage frameworks within the GLP-1 Weight-loss Medication Market.

Germany – 8.9% market share: Leadership supported by structured public reimbursement systems and strong integration of GLP-1 therapies within national obesity management guidelines.

The GLP-1 Weight-loss Medication Market is highly consolidated, with the top five companies controlling approximately 82% of global market share. One leading pharmaceutical innovator holds nearly 46% share, followed by two major multinational competitors collectively representing 26%. Over 18 active biotechnology firms are engaged in late-stage incretin-based therapy development, intensifying pipeline competition. Strategic initiatives include peptide manufacturing expansion exceeding 40% capacity growth, co-development partnerships for dual-agonist therapies, and acquisitions targeting oral peptide delivery platforms. More than USD 12 billion has been invested globally in peptide synthesis and injectable device manufacturing since 2023. Innovation trends focus on dual and triple agonists delivering up to 24% average weight reduction in advanced trials. Competitive differentiation increasingly depends on dosing convenience, cardiovascular outcome data, and digital adherence integration, shaping long-term market positioning.

AstraZeneca plc

Sanofi S.A.

Roche Holding AG

Boehringer Ingelheim

Amgen Inc.

Merck & Co., Inc.

Johnson & Johnson

GSK plc

Teva Pharmaceutical Industries Ltd.

AbbVie Inc.

Bristol Myers Squibb

Advanced peptide engineering technologies are central to the GLP-1 Weight-loss Medication Market. Modern recombinant DNA platforms enable production purity exceeding 99.5%, improving therapeutic consistency. Continuous bioprocessing systems increase manufacturing yield by 30% compared to batch-based production. Long-acting depot formulations extend half-life to over 168 hours, enabling once-weekly dosing. Dual and triple agonist molecules targeting GLP-1, GIP, and glucagon receptors demonstrate up to 24% average weight reduction in late-stage trials.

Autoinjector innovations featuring micro-needle systems reduce injection discomfort by 18% and improve patient retention. Oral peptide delivery utilizes absorption enhancers improving bioavailability by 12% compared to early prototypes. AI-driven patient monitoring platforms analyze metabolic data points exceeding 500 variables per patient, optimizing dosing intervals. Digital adherence systems reduce discontinuation rates by 19%. Cold-chain optimization technologies reduce temperature deviation incidents by 22%, improving supply reliability. Emerging research focuses on precision metabolic profiling and pharmacogenomics, enabling personalized obesity management strategies tailored to individual insulin resistance and cardiovascular risk profiles.

• In November 2024, Novo Nordisk announced expansion of its manufacturing facility to increase GLP-1 production capacity by 40%, strengthening supply chain resilience amid rising global demand. Source:www.novonordisk.com

• In May 2024, Eli Lilly reported positive Phase III data showing up to 22% average weight reduction with its dual GLP-1/GIP therapy across 72-week clinical trials involving over 2,500 participants. Source:www.lilly.com

• In March 2025, Pfizer initiated a Phase II clinical program evaluating an oral GLP-1 candidate designed to improve bioavailability by 15% compared to earlier peptide formulations. Source:www.pfizer.com

• In January 2025, AstraZeneca announced collaboration with a biotechnology partner to develop next-generation incretin combinations targeting metabolic syndrome, expanding its obesity treatment pipeline. Source:www.astrazeneca.com

The GLP-1 Weight-loss Medication Market report provides comprehensive coverage across product types, including injectable GLP-1 analogs, oral peptide formulations, and dual or triple incretin agonists. The analysis spans therapeutic applications such as obesity management, type 2 diabetes with weight complications, and cardiometabolic risk reduction. Regional coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, encompassing more than 35 key national markets.

The report evaluates prescription volumes exceeding 25 million annually, manufacturing capacity expansions above 40% in leading facilities, and clinical trial pipelines featuring over 20 late-stage candidates. It assesses regulatory frameworks influencing reimbursement coverage rates ranging from 21% to 64% across regions. End-user analysis includes specialty obesity clinics, endocrinology centers, hospital systems, and retail pharmacies, representing diverse distribution channels. Emerging niche segments such as digital companion therapeutics and AI-driven adherence monitoring platforms are examined for their impact on patient retention and therapeutic optimization. The scope integrates technological innovation trends, competitive benchmarking, and evolving global healthcare policies shaping long-term metabolic disease management strategies.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 13,810.2 Million |

|

Market Revenue in 2033 |

USD 41,372.1 Million |

|

CAGR (2026 - 2033) |

14.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Novo Nordisk A/S, Eli Lilly and Company, Pfizer Inc., AstraZeneca plc, Sanofi S.A., Roche Holding AG, Boehringer Ingelheim, Amgen Inc., Merck & Co., Inc., Johnson & Johnson, GSK plc, Teva Pharmaceutical Industries Ltd., AbbVie Inc., Bristol Myers Squibb |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |