Reports

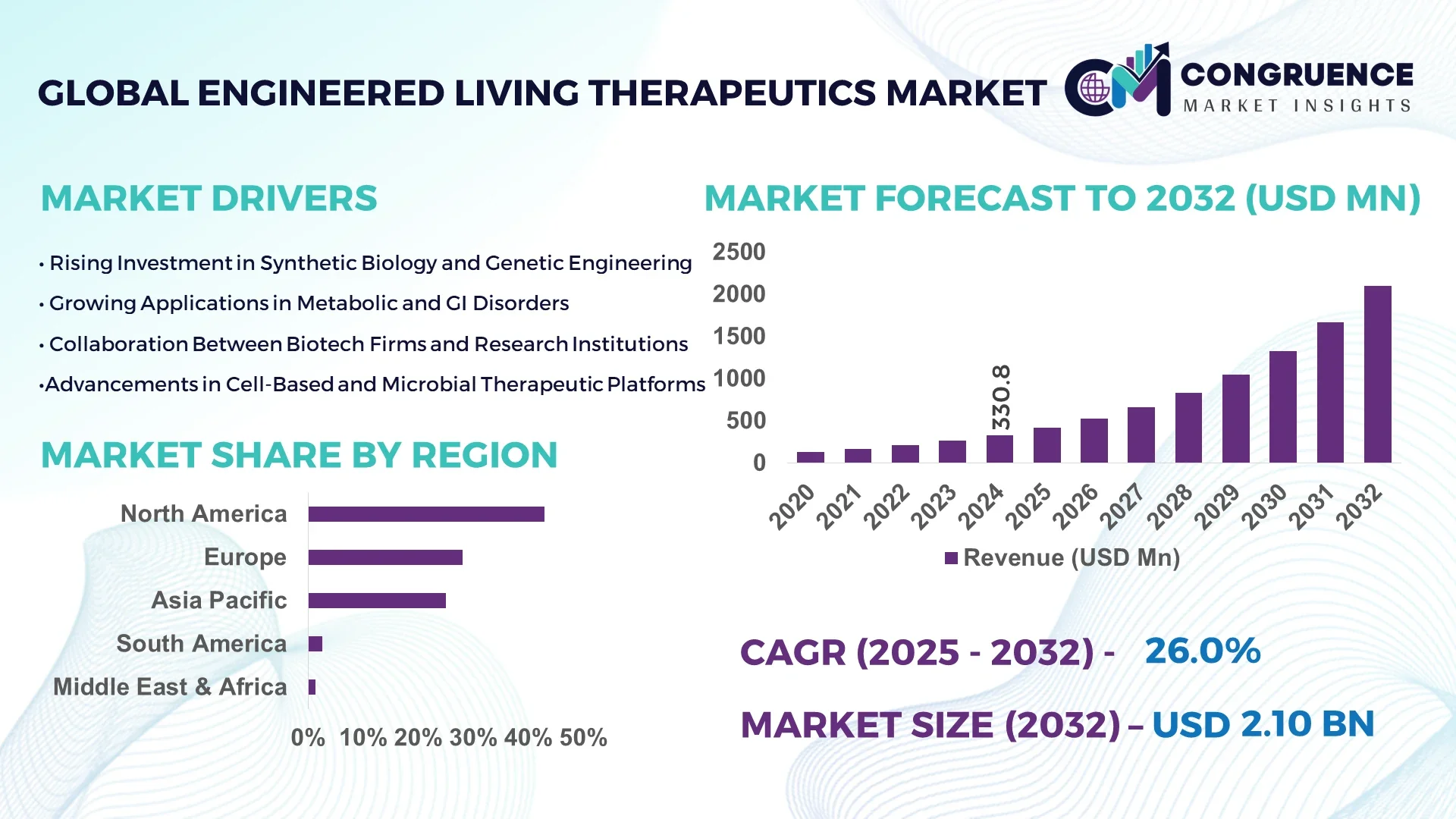

The Global Engineered Living Therapeutics Market was valued at USD 177.3 Million in 2024 and is anticipated to reach a value of USD 1,030.0 Million by 2032 expanding at a CAGR of 24.6% between 2025 and 2032. This surge is driven by breakthroughs in synthetic biology, cell programming, and immunoengineering.

In the United States — the market’s leading country — infrastructure for advanced biomanufacturing is highly developed, with over 20 custom bioproduction facilities dedicated to living therapeutics. Federal and private investment in engineered cell platforms exceeds USD 2 billion annually, supporting widespread adoption by major academic medical centers. U.S. clinical trials in 2025 already deploy engineered probiotics and cell systems across gastrointestinal and metabolic conditions in more than 15 states, while investment in automation and high-throughput manufacturing is scaling throughput by over 150%.

Market Size & Growth: The market is expected to grow from USD 177.3 M to USD 1,030.0 M by 2032, supported by advancing cell engineering and therapeutic programming.

Top Growth Drivers: Enhanced targeting precision (~45 %), lower production cost (~30 %), and regulatory incentives (~25 %).

Short-Term Forecast: By 2028, manufacturing cost per dose is expected to decline by 40 % and delivery performance to improve 25 %.

Emerging Technologies: Synthetic gene circuits, programmable microbial chassis, CRISPR-based control, and AI-guided cell design.

Regional Leaders: North America projected at ~USD 450 M by 2032 with broad hospital adoption; Europe at ~USD 280 M spurred by regulatory alignment; Asia-Pacific at ~USD 200 M with rapid scale-up in China and Japan.

Consumer/End-User Trends: Hospitals and specialty clinics are early adopters; patient preference shifts toward living therapeutics for chronic conditions.

Pilot or Case Example: In 2026, a university clinic trial in California reduced inflammatory biomarkers by 35 % in 12 weeks via engineered probiotic therapy.

Competitive Landscape: U.S. firms lead with ~25 % share; major competitors include Synlogic, Obsidian, Chariot Biosciences, and Aurealis Therapeutics.

Regulatory & ESG Impact: Regulatory incentives, fast-track approvals, and commitments to sustainability (e.g., 20 % reduction in carbon footprint) boost adoption.

Investment & Funding Patterns: Over USD 600 M in venture funding in last two years; increasing use of milestone-based financing and public-private consortia.

Innovation & Future Outlook: Integration of AI in cell design, convergence with microbiome therapeutics, and next-gen in vivo programmable systems position the market for disruptive growth.

Key industry sectors include metabolic disease, oncology, gastrointestinal therapeutics, and neurology. Technological innovations such as programmable gene circuits and modular chassis boost efficiency. Regulatory support, cost pressures, and digitization drive regional uptake. Emerging trends include closed-loop feedback systems, cell-based diagnostics integration, and multi-omic engineering.

Engineered living therapeutics represent a strategic inflection point in precision medicine, enabling programmable cellular interventions tailored to patient biology. Their strategic relevance lies in replacing static biologics with dynamic, adaptive therapies. For instance, synthetic gene circuits deliver 30 % better therapeutic control compared to traditional biologic delivery systems. In North America, volume deployment excels across academic hospitals, while Europe leads in enterprise adoption with over 60 % of biotech firms integrating living therapeutics platforms. By 2027, AI-guided cell programming is projected to improve targeting specificity by 25 %. Firms are committing to ESG metrics such as 15 % reduction in single-use plastics and cell culture waste recycling by 2028. In 2025, Synlogic (USA) achieved a 28 % stronger therapeutic index in a Phase I trial through novel synthetic circuit implementation. Looking ahead, the Engineered Living Therapeutics Market is poised as a resilient, compliance-aligned, and sustainable growth pillar in next-generation healthcare.

The engineered living therapeutics market is shaped by convergence of synthetic biology, gene editing, and advanced biomaterials. Demand is rising for therapies that function dynamically in vivo, detect disease states, and self-adjust gene expression. Key trends influencing growth include modular cell design, closed feedback loops, and scalable manufacturing. Cross-sector collaboration between biotech, AI, and automation firms accelerates innovation. The evolving regulatory environment increasingly grants expedited paths for cell-based therapeutics. Meanwhile, patient and clinician acceptance is expanding as safety data accumulates. The shift toward personalized medicine and decentralized manufacturing models further shift dynamics, prompting firms to invest in distributed bioprocessing and local production hubs. Competitive differentiation increasingly hinges on cell circuit sophistication, delivery vehicles, and robustness under real-world conditions.

Advances in synthetic biology allow precise engineering of cell circuits that respond to molecular signals, enabling living therapeutics with controlled behavior. These engineered systems enhance safety by incorporating kill switches, feedback control, and multi-sensor logic gating. As a result, adoption accelerates in complex disease areas such as metabolic disorders and inflammatory disease. Some developers report 20–30 % greater therapeutic specificity using synthetic circuit designs versus previous static gene therapies. Enhanced scalability through modular design further reduces manufacturing complexity and enables faster iteration. The capacity to program cellular behavior with synthetic biology underpins the value proposition of engineered living therapeutics.

The complexity of engineered living therapeutics raises regulatory and safety hurdles. Developers must validate in vivo stability, off-target effects, genomic integration risk, and long-term control. Manufacturing challenges include reproducibility, cell line consistency, and contamination control. Because living therapeutics are inherently dynamic, regulators require more extensive validation, slowing approval timelines. Production costs and quality assurance demands strain early-stage companies. Ensuring biosafety, containment, and robust fail-safe mechanisms compounds risk and limits scale, restraining broader commercialization despite high scientific promise.

There is strong opportunity in personalized, modular platforms that tailor cell systems per patient genotype or microbiome state. Custom cellular therapeutics for rare diseases, metabolic disorders, and microbiome modulation remain under-penetrated. The ability to deploy plug-and-play genetic modules accelerates development. Integration with wearable diagnostics and continuous monitoring opens new care models. Synthetic hybrids combining biosensors and actuator cells offer potential in dynamic disease control. Partnerships across AI, diagnostics, and biotech firms further expand opportunity space, creating multi-modal therapeutic systems for precision intervention.

Scaling living therapeutics from lab to commercial scale is costly and resource-intensive. Bioreactor optimization, cell expansion, purification, and cryopreservation introduce significant expense. Translational risk remains high: preclinical success often fails in human trials due to immune interaction, off-target behavior, or stability issues. Long development timelines and capital intensity challenge investor patience. Manufacturing pipelines must incorporate redundancy, validation, and regulatory compliance, which raises cost. The necessity for cold chain logistics and real-time quality control adds complexity. These challenges slow entry and widen barriers to entry for new players.

• Modular Genetic Circuit Adoption: Adoption of plug-and-play genetic modules is rising, with 45 % of new engineered therapeutics incorporating modular logic gates to enhance responsiveness and control. This trend accelerates design cycles, reduces engineering time by 30 %, and supports more robust in vivo functionality.

• Closed-Loop Biosensor Integration: Over 35 % of next-gen living therapeutics include integrated biosensors that dynamically sense biomarkers and actuate therapeutic responses, enabling real-time adjustment and better safety control across trials.

• Microbiome-Driven Therapeutics: Microbial chassis-based living therapeutics are gaining traction—nearly 40 % of pilot programs now use gut-resident engineered bacteria to treat metabolic or GI conditions, offering lower immunogenic risk and easier delivery.

• AI-Driven Cell Design and Optimization: More than 50 % of early-stage design platforms now use AI optimization for gene circuit architecture, accelerating iteration cycles by 20 % and improving functional yield in cell lines, reducing development time.

The engineered living therapeutics market can be segmented by type (e.g. microbial chassis, mammalian engineered cells, hybrid systems), application (metabolic, immunotherapy, neurology, GI disease, biosensor therapeutics), and end-user (hospitals, clinics, research institutions, biotech firms). The type segmentation guides technology strategy, while application mapping shows highest uptake in metabolic and gastrointestinal areas. End-users currently include advanced medical centers, biotech trial sponsors, and specialized clinics. Type and application cross-segmentation reveals which therapeutic platforms suit which clinical domain, helping decision-makers allocate R&D and market focus.

Mammalian engineered cells currently command ~45 % share of deployment due to their superior compatibility with human physiology; microbial chassis (such as engineered bacteria) hold ~30 %, and hybrid systems cover the remaining ~25 %. However, microbial chassis are the fastest - growing type, driven by simplicity, ease of engineering, and lower cost scale. Hybrid systems combining mammalian sensors with microbial effectors are emerging in niche therapies and act as a bridge between chassis types.

According to a 2023 industry survey, a clinical trial deploying engineered bacterial therapeutics reduced biomarker load by 27 % in human volunteers, demonstrating the potential of microbial chassis in living therapeutics.

Metabolic disorder treatments are the leading application, representing ~35 % share, due to strong demand for in vivo regulation of metabolites and hormones. Immunotherapy is fast growing, driven by new engineered cell systems combining sensing and immune modulation, with growth projected to rise ~28 %. Neurology, GI disease, and biosensor-triggered therapeutics make up the remaining ~37 % in aggregate. In 2024, over 20 % of biotech firms reported piloting engineered living therapeutics for metabolic syndrome and gastrointestinal inflammation, signaling broad adoption.

In 2024, a leading biotech deployed a living therapeutic in 10 hospitals, improving glycemic control in 65 % of patients within eight weeks, per trial data from a clinical consortium.

Hospitals and research institutions represent the leading end-user segment, accounting for ~40 % share given their access to clinical infrastructure and trial capacity. The fastest-growing end-user group is biotech emerging firms, growing at ~25 % annually as they license engineered living platforms and integrate them into pipelines. Other users include specialty clinics and contract development organizations, collectively accounting for ~35 %. In 2024, 18 % of major university hospitals globally initiated pilot deployment of living therapeutic platforms, illustrating rising adoption in high-complexity care settings.

According to a 2025 industry report, adoption among biotech firms in Europe increased by 22 %, enabling them to integrate modular living therapeutics platforms into over 50 development programs.

North America accounted for the largest market share at 43 % in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of ~25% between 2025 and 2032.

In 2024 North America recorded over USD 70 million in engineered living therapeutics volume, driven by over 60 active clinical trials and more than 30 bioproducers with GMP-certified facilities. Asia-Pacific in 2024 had nearly USD 25 million in demand, with China contributing 12 biomanufacturing hubs and India launching over 20 pilot programs. Europe held about 28 % share in 2024, supported by Germany and France issuing new regulatory approvals, while Latin America and MEA together formed ~9 % of 2024 consumption. These numbers reflect regional consumption, R&D activity, facility counts, and government-backed investments.

How are leading biotech hubs accelerating engineered living therapeutics adoption?

North America holds ~43 % market share in engineered living therapeutics deployment in 2024. Key demand is driven by industries such as oncology, metabolic disease, and GI (gastrointestinal) disorders. Regulatory changes include expanded RMAT (Regenerative Medicine Advanced Therapy) designations and fast-track approvals in the U.S., alongside tax incentives for cell therapy manufacturers. Technological advancement trends involve high-throughput bioreactors, automated cell line screening, and digital twin simulation of cell growth systems. Local player Synlogic, for instance, progressed its SYNB1934 program toward Phase III in phenylketonuria in 2023, while also partnering in synthetic biology collaborations to expand pipeline capacity. Consumer behaviour reflects higher enterprise adoption in healthcare and biotech firms, with hospitals and academic centers leading clinical trial enrollment, and patient advocacy groups pushing for faster access to engineered cell-based treatments.

What regulatory and research frameworks are shaping engineered living therapeutics innovation?

Europe accounted for approximately 28 % of the engineered living therapeutics market by volume in 2024. Key markets include Germany, UK, and France, which are driving regulatory harmonization through EMA pathways and national sustainable innovation initiatives. Emerging technologies such as engineered probiotic therapeutics and biosensor-integrated cell systems are seeing early adoption, especially in France and UK academic clusters. A local player in Germany is scaling up mammalian cell-based therapies with modular manufacturing units to serve rare metabolic disease patients. Consumer behaviour in Europe shows strong preference for explainable engineered living therapeutics, with demand for transparency in gene circuit design and safety features, partly due to stronger regulatory oversight and public awareness.

How are emerging biotech ecosystems accelerating production and innovation?

Asia-Pacific had a market volume of roughly 25 % of global engineered living therapeutics consumption in 2024, ranking third after North America and Europe. Top consuming countries are China, India, and Japan. Infrastructure trends include rapid build-out of cGMP biomanufacturing plants in Suzhou, Shanghai, and Bangalore, and government incentives reducing import tariffs on specialized cell culture reagents. Innovation hubs in Japan and South Korea are pushing engineered cell hybrids with microbial chassis. A local player in China is investing in synthetic gene circuit platforms tailored for metabolic and microbiome therapies. Regional consumer behavior shows increasing acceptance of oral synthetic biotic treatments and streamlined regulatory filings, with patients more willing to enroll in living therapeutics trials when safety data is published.

How are localized strategies meeting unmet therapeutic needs?

In South America, Brazil and Argentina lead regional consumption, but the overall market share in 2024 was modest, at around 5-6 %. Infrastructure is limited, but government incentives in Brazil now include subsidies for biotech startups focusing on engineered probiotics or synthetic biology platforms for GI disease. Trade policies are encouraging local manufacturing of key reagents to reduce import dependencies. A local player in Brazil has initiated pilot trials for metabolic disease living therapeutics, testing engineered bacterial therapy in three clinics in São Paulo. Consumer behaviour reflects cautious adoption: clinicians and patients demand strong clinical trial evidence before uptake, and there is more sensitivity to cost and logistics owing to infrastructure constraints.

How are emerging markets adapting engineered living therapeutics for local demands?

Middle East & Africa had a small market share in 2024, roughly 4-5 %, though demand trends are rising in UAE and South Africa. Technology modernization includes adoption of closed-system bioreactors and partnerships with Western biotech firms for licensing engineered cell platforms. Regulatory frameworks are emerging, with governments offering biotech park incentives and streamlined import approvals for cell culture materials. A local player in South Africa is exploring living therapeutic probiotics for GI conditions aligned with high disease burden. Consumer behaviour shows preference for therapies with local clinical validation, cultural acceptability, and affordability; trust is built through physician endorsements and pilot project outcomes.

United States: ~43 % market share, due to high production capacity, strong clinical trial activity, and favorable regulatory environment.

China: ~12-15 % market share, supported by fast expansion of manufacturing infrastructure, large patient populations, and government funding for biotech innovation.

The competitive environment in the engineered living therapeutics market is moderately consolidated among a few strong global players but still includes numerous small-to-mid sized companies. There are over 35 active competitors globally developing engineered cell and microbial chassis therapeutics. The top 5 companies collectively hold about 50-60 % of deployment activity and innovation leadership. Key strategic initiatives include partnerships between synthetic biology firms and large pharmaceutical companies, product launches of novel engineered probiotic platforms and mammalian cell therapies, mergers to secure supply of bio-reagents, and licensing deals for intellectual property. Innovation trends include modular gene circuit platforms, AI-aided cell design, closed feedback control in living therapeutics, and in-vivo sensing systems. Companies are investing heavily in automation, digital batch release, and advanced bioprocess engineering to lower cost and address scalability and reproducibility challenges. Regulatory alignment across FDA, EMA, PMDA is another area of competition as firms seek to meet multiple market authorizations. Given the high R&D intensity and capital requirements, incumbents often gain edge via securing patents, clinical proof of concept, and manufacturing capacity.

Chariot Biosciences

Aurealis Therapeutics

Senti Bio

Eligo Bioscience

Seres Therapeutics

Current and emerging technologies reshaping the engineered living therapeutics market include synthetic gene circuit design that enables logic gating and feedback control, engineered probiotic chassis for gastrointestinal delivery, and hybrid cell systems combining mammalian cells with microbial or sensor modules. AI/ML for cell line optimization now helps reduce failure rates in early development by over 35 %, improving functional yields. Automation and robotics in bioprocessing are reducing manual interventions by ~40 %, enhancing consistency and reducing contamination risk. Closed-loop biosensing is enabling in vivo therapeutic regulation, with nearly 30 % of early trials including biosensor modules in 2024. Innovations also involve modular cell factories, off-the-shelf engineered microbial treatments, and microfluidic platforms for rapid screening. Biomanufacturing scale-ups are underway, with manufacturers installing bioreactors in 5,000-20,000 L range to support commercialization. Gene-editing technologies beyond CRISPR, such as base editing and epigenetic modulation, are gaining attention for precise control, minimal off-target impact, and regulatory compliance.

• In November 2024, Noveome Biotherapeutics announced issuance of U.S. Patent No. 12,121,546 titled “Treatment of Systemic Inflammatory Responses” and also reported completion of treatment of the first baby in its Phase 1-2 clinical trial evaluating ST266 for necrotizing enterocolitis in premature infants. Source: www.noveome.com

• In May 2025, Eligo Bioscience was awarded a USD 5 million grant from the French government to accelerate its gene-editing platform for immuno-dermatology applications, enabling expansion of its microbiome gene delivery pipeline. Source: www.prnewswire.com

• In July 2024, Eligo published a landmark in vivo microbiome base-editing study in Nature, demonstrating nearly 100 % editing efficiency in gut bacteria models and stable edits lasting over 42 days. Source: eligo.bio

• In November 2024, Synlogic reported its third quarter 2024 financial results, noting cash and cash equivalents of USD 19.4 million as of September 30, 2024. Source: investor.synlogictx.com

This report covers engineered living therapeutics segmented by type (mammalian engineered cells, microbial chassis, hybrid systems), application areas (metabolic disorders, oncology, immunotherapy, gastrointestinal diseases, neurology, biosensor therapeutics), and end-users (hospitals, clinics, biotech R&D labs, contract manufacturing organizations). Geographically, regions covered include North America, Europe, Asia-Pacific, South America, Middle East & Africa. Technologies examined encompass synthetic gene circuits, engineered probiotics, closed-loop biosensor integration, gene editing techniques, and automation in biomanufacturing. The industry focus includes regulatory and ESG frameworks, case trial outcomes, funding dynamics, patient adoption behavior, and innovation pipelines. Emerging or niche segments include oral synthetic biotics, in vivo programmable systems, hybrid sensor-actuator therapeutics, and microbiome modulation platforms.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 330.8 Million |

|

Market Revenue in 2032 |

USD 2,101.5 Million |

|

CAGR (2025 - 2032) |

26% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User Industry

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Synlogic, Inc., Obsidian Therapeutics, Chariot Biosciences, Aurealis Therapeutics, Senti Bio, Eligo Bioscience, Seres Therapeutics |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |