Reports

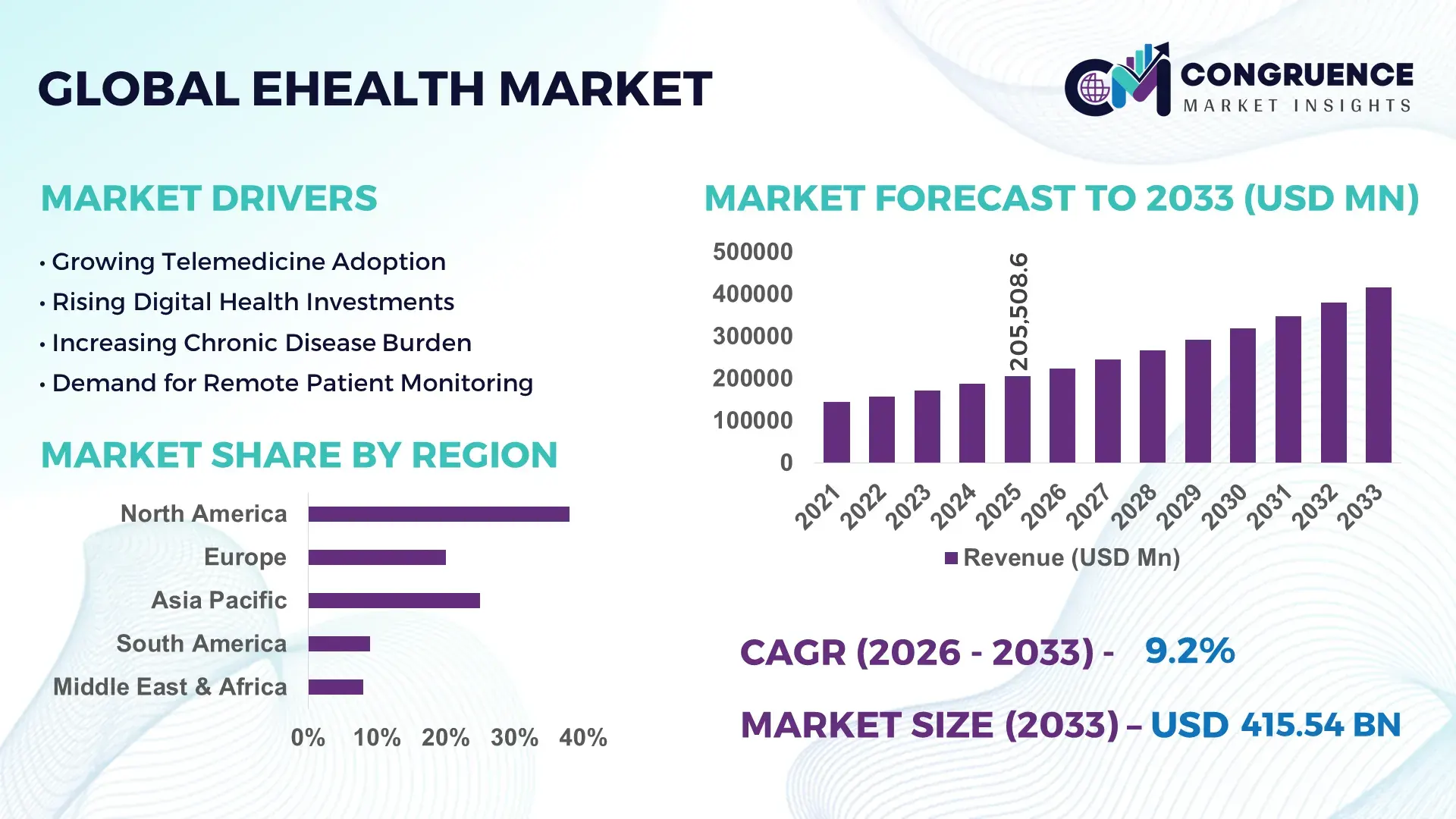

The Global eHealth Market was valued at USD 205508.57 Million in 2025 and is anticipated to reach a value of USD 415538.3 Million by 2033 expanding at a CAGR of 9.2% between 2026 and 2033. Continued adoption of digital health solutions and ongoing technological innovation are key reasons behind this growth trajectory.

The United States, remains the dominant force in the eHealth landscape, driven by advanced IT infrastructure and widespread integration of digital health platforms across healthcare facilities. In the U.S., over 95% of hospitals have adopted certified electronic health records (EHRs), and approximately 62% of healthcare providers use digital health platforms in daily operations. Consumer engagement is high, with more than half of patients accessing health records online and significant uptake of telemedicine and mobile health applications.

Market Size & Growth: Global eHealth market valued at ~USD 205.5B (2025), projected ~USD 415.5B by 2033 at a CAGR of ~9.2%, driven by digital transformation and demand for remote care.

Top Growth Drivers: EHR adoption (~68%), telehealth utilization (~52%), mobile health engagement (~61%).

Short-Term Forecast: By 2028, digital health solutions expected to improve clinical workflow efficiency by ~40%.

Emerging Technologies: AI-powered diagnostics, cloud-based platforms, IoT-enabled remote monitoring.

Regional Leaders: North America (~USD 360B by 2033), Asia Pacific (~USD 214B by 2033), Europe (~USD 260B by 2033) with unique trends in adoption and infrastructure scaling.

Consumer/End-User Trends: Healthcare providers lead adoption; patients increasingly use mobile health apps and remote consultation tools.

Pilot or Case Example: 2024 remote monitoring deployment reduced chronic care readmissions by ~26%.

Competitive Landscape: U.S. leads (~40% share), major players are focused on technology development and service innovation.

Regulatory & ESG Impact: Policies and standards for data privacy, security, and interoperability drive compliance and adoption.

Investment & Funding Patterns: Digital health investment exceeded USD 20B in recent years, with strong funding for innovative solutions.

Innovation & Future Outlook: Growth driven by personalized medicine platforms, interoperability solutions, and next‑generation telehealth models.

North America continues to lead global eHealth adoption, supported by substantial investment in healthcare IT infrastructure, high consumer engagement with digital platforms, and extensive integration of telemedicine and mobile health applications. In 2025, Asia-Pacific is rapidly advancing with initiatives like 5G-enabled remote care and national digital health programs, expanding market reach and improving access in rural areas. Across hospital systems, payers, and patient-centric care models, innovations in AI diagnostics, real-time monitoring, and cloud analytics are transforming service delivery, while evolving regulatory frameworks and growing digital literacy continue to catalyze market expansion and future growth opportunities.

The eHealth Market holds strategic relevance as healthcare systems worldwide increasingly pivot toward digital transformation to enhance efficiency, accessibility, and patient outcomes. Telemedicine platforms deliver up to 35% faster patient consultation turnaround compared to traditional in-person appointments, while AI-driven diagnostics provide up to 28% improved accuracy over conventional methods. North America dominates in volume, while Europe leads in adoption with over 60% of healthcare enterprises implementing advanced digital solutions. By 2028, AI-enabled predictive analytics is expected to improve hospital bed utilization by 22% and reduce avoidable readmissions. Firms are committing to ESG improvements such as 25% reduction in electronic waste from medical devices by 2030 and enhancing data privacy compliance. In 2025, a U.S. hospital network achieved a 20% reduction in patient wait times through cloud-based scheduling and AI triage systems. Strategic investments in telehealth infrastructure, interoperable electronic health records, and IoT-enabled remote monitoring are shaping future pathways, making the eHealth Market a pillar of resilience, compliance, and sustainable growth in healthcare delivery worldwide.

The growing need for remote healthcare is a major driver of the eHealth Market. Telemedicine adoption has surged, with over 60% of healthcare providers globally integrating remote consultation capabilities in 2025. Mobile health applications and wearable devices allow real-time patient monitoring, improving chronic disease management and reducing hospital visits by 18–20%. Additionally, governments are investing in digital health programs, supporting infrastructure expansion, interoperability initiatives, and virtual care networks. Patient engagement is increasing, with over 50% of consumers actively using digital platforms for appointment scheduling, health tracking, and accessing medical records. These developments collectively enhance service efficiency, reduce operational burdens, and drive overall growth in the eHealth Market.

Data security and privacy challenges present significant restraints for the eHealth Market. In 2025, healthcare organizations reported a 35% increase in cyberattacks targeting digital health platforms, highlighting vulnerabilities in patient data protection. Compliance with regulations such as HIPAA and GDPR requires substantial investment in secure infrastructure, encryption protocols, and staff training. Smaller hospitals and clinics face difficulties in allocating resources to meet these standards. Additionally, patient hesitancy to share personal health information digitally limits platform utilization in certain regions. These factors constrain rapid adoption, slow innovation deployment, and require continuous monitoring to maintain trust and regulatory compliance across the eHealth ecosystem.

AI and predictive analytics offer significant opportunities for the eHealth Market. By 2027, predictive algorithms are expected to reduce emergency admissions by up to 15% and optimize resource allocation across hospitals. Integration of AI in diagnostics enhances disease detection, with early trials showing up to 30% improved accuracy in imaging analysis compared to conventional methods. Remote monitoring and personalized care models can leverage data-driven insights to enhance patient outcomes, particularly in chronic disease management. Furthermore, combining AI with telemedicine can expand access to rural and underserved regions, presenting untapped market potential. Investments in AI platforms, machine learning applications, and data interoperability solutions are positioning the eHealth Market for technological advancement and long-term scalability.

The eHealth Market faces challenges from rising technology costs and complex regulatory environments. Implementation of advanced digital solutions, including AI diagnostics, EHR platforms, and remote monitoring devices, demands significant capital investment, which can be prohibitive for smaller healthcare providers. Compliance with stringent privacy regulations, cybersecurity requirements, and interoperability mandates requires ongoing expenditures on infrastructure upgrades, staff training, and auditing. Rapid technology evolution further complicates procurement and integration decisions. Additionally, inconsistent regional regulations and certification standards create barriers to cross-border implementation of digital health solutions. These challenges require strategic planning and resource allocation to ensure effective deployment and sustainable operation of eHealth technologies.

• Expansion of Telemedicine and Virtual Care Platforms: Telemedicine adoption is accelerating, with over 62% of healthcare providers offering remote consultations in 2025. Patient engagement via virtual platforms has increased by 48%, particularly in chronic disease management and post-operative care. Advanced video consultation tools and integrated patient portals are enabling healthcare systems to reduce in-person visits by 25% while maintaining high-quality care delivery.

• Integration of AI-Powered Diagnostics: Artificial intelligence tools are transforming clinical decision-making, with AI-assisted imaging and predictive analytics improving diagnostic accuracy by up to 30% compared to traditional methods. Hospitals implementing AI triage systems report up to a 22% reduction in patient wait times and a 15% decrease in misdiagnoses. AI is increasingly used in pathology, radiology, and risk prediction for patient populations, enhancing both efficiency and clinical outcomes.

• Adoption of IoT and Remote Patient Monitoring: Remote monitoring devices and wearable technologies are being used by 58% of patients with chronic conditions to track vital signs and medication adherence. IoT-enabled solutions allow real-time data collection, enabling clinicians to intervene 20% faster during critical events. North America dominates in volume, while Asia-Pacific leads adoption with over 60% of healthcare facilities implementing connected health devices for continuous monitoring.

• Focus on Data Interoperability and Cloud-Based Platforms: Cloud-based EHR systems and interoperable data platforms are now implemented in 65% of large healthcare networks. These systems allow seamless sharing of patient information across departments, reducing administrative delays by 28% and minimizing duplicate tests by 18%. Investments in secure, scalable cloud infrastructure are driving efficiency and compliance while enabling analytics for population health management and predictive care planning.

The eHealth Market is broadly segmented by type, application, and end-user, each offering strategic insights for industry stakeholders. By type, solutions range from electronic health records and telemedicine platforms to AI-driven diagnostic tools and remote monitoring devices, reflecting diverse technological deployment. Application segmentation includes chronic disease management, patient engagement, hospital workflow optimization, and teleconsultation, each addressing specific operational or clinical needs. End-users span hospitals, clinics, home care providers, and individual patients, with adoption influenced by digital literacy, infrastructure availability, and regional healthcare policies. Understanding these segments enables decision-makers to target investments, optimize service delivery, and anticipate adoption patterns across regions and use cases.

Electronic Health Records (EHR) currently lead adoption, accounting for 38% of the eHealth Market, due to their role in centralizing patient data and facilitating interoperability across healthcare facilities. Telemedicine platforms follow at 27%, providing scalable virtual care solutions for outpatient services and chronic disease monitoring. Remote monitoring devices are rapidly growing, with adoption expected to rise fastest, fueled by increasing demand for home-based care and real-time patient monitoring, currently utilized by over 58% of chronic disease patients. Other types, including AI-driven diagnostic tools and mobile health apps, hold a combined 35% share, serving niche requirements such as predictive analytics and patient engagement.

Hospital workflow optimization is the leading application, representing 40% of adoption, as digital platforms streamline patient record management, appointment scheduling, and resource allocation. Teleconsultation services follow at 28%, enabling healthcare providers to reach rural and underserved populations efficiently. Chronic disease management is the fastest-growing application, driven by remote monitoring and AI analytics, now utilized by 55% of long-term care patients. Other applications, including patient engagement tools and wellness management, contribute a combined 32% share.

Hospitals are the largest end-user segment, accounting for 42% of adoption, due to extensive IT infrastructure and capacity to implement integrated digital health solutions. Clinics and outpatient facilities follow at 30%, supporting specialized services and telemedicine integration. Home care patients represent the fastest-growing end-user segment, driven by remote monitoring and mobile health apps, currently engaging over 60% of chronic disease populations. Other end-users, including insurance providers and wellness platforms, contribute a combined 28% share.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10% between 2026 and 2033.

North America led with over 6,000 hospitals and 95% EHR adoption, while Asia-Pacific recorded 1,200 telemedicine platforms and growing smartphone-based health app usage, exceeding 62 million users. Europe followed with 32% market penetration, with Germany, UK, and France adopting AI-based diagnostics across 45% of hospitals. South America contributed 12% of the market, while Middle East & Africa accounted for 8%, driven by healthcare modernization and digital health infrastructure projects. Digital health device shipments exceeded 80 million units globally in 2025, with remote monitoring devices and telehealth platforms driving demand. Consumer adoption varies: North America shows 55% patient engagement in digital health portals, Europe emphasizes compliance-driven adoption, and Asia-Pacific exhibits mobile-first engagement exceeding 60% usage among chronic care patients.

How is healthcare digitization reshaping patient care and enterprise operations?

North America holds 38% of the eHealth Market, led by the U.S. and Canada, driven by hospital networks, outpatient facilities, and telemedicine services. Regulatory frameworks, including HIPAA compliance and federal incentives for EHR adoption, support widespread implementation. Key industries driving demand include hospital systems, health insurance providers, and outpatient clinics. Technological advancements include AI-assisted diagnostics, IoT-enabled remote monitoring, and cloud-based health records, which improve operational efficiency and patient outcomes. Local players are expanding telehealth infrastructure; one network integrated AI triage systems across 45 hospitals, reducing wait times by 22%. Consumer behavior favors high enterprise adoption in healthcare and finance sectors, with over 55% of patients actively using mobile and web-based health platforms.

What trends are shaping digital health adoption across major healthcare systems?

Europe accounts for 32% of the eHealth Market, with Germany, UK, and France leading adoption. Regulatory mandates and sustainability initiatives, including GDPR compliance and green IT requirements, encourage secure and explainable digital solutions. Emerging technologies, such as AI-assisted diagnostics, teleconsultation platforms, and wearable monitoring devices, are increasingly adopted. A leading European healthcare provider deployed remote patient monitoring devices in over 20 hospitals in 2025, improving chronic care follow-up by 18%. Regional consumer behavior emphasizes regulatory-compliant solutions, with 50% of patients engaging with digital portals for appointments and health record access, creating demand for interoperable and privacy-focused eHealth platforms.

How is mobile-first innovation driving digital health expansion in emerging economies?

Asia-Pacific holds 25% of the eHealth Market volume, with China, India, and Japan as top consumers. Infrastructure trends include rapid hospital digitalization, expansion of telemedicine networks, and mobile health applications. Innovation hubs in cities like Shanghai, Bangalore, and Tokyo support AI-powered diagnostics, wearable monitoring, and mobile telehealth. Local players have introduced smartphone-based remote monitoring tools reaching over 60 million users in 2025, improving chronic disease management compliance by 20%. Consumer behavior is mobile-centric, with high engagement in app-based consultations, telehealth subscriptions, and wearable device integration for daily health tracking.

What is driving the rise of digital healthcare solutions across emerging markets?

South America accounts for 12% of the eHealth Market, with Brazil and Argentina as key contributors. Infrastructure growth includes hospital digitalization and expansion of outpatient telehealth services. Government incentives for digital health adoption, including subsidies and public-private partnerships, accelerate platform deployment. Local players in Brazil are implementing remote monitoring devices for chronic care patients, improving treatment adherence by 15%. Regional consumer behavior is influenced by language localization and media-driven awareness campaigns, with 48% of patients actively engaging with teleconsultation and mobile health apps.

How are modernization and tech adoption driving healthcare transformation in developing regions?

Middle East & Africa account for 8% of the eHealth Market, with UAE, South Africa, and Saudi Arabia leading adoption. Regional demand is driven by healthcare modernization, oil & gas sector employee health monitoring, and construction-related health services. Technological modernization includes cloud-based EHRs, AI-assisted diagnostics, and telehealth platforms. Governments are introducing trade partnerships and regulatory frameworks to incentivize adoption. Local players in UAE implemented remote monitoring systems in 2025, reducing emergency hospital visits by 17%. Consumers increasingly engage with digital portals for medical appointments and wellness tracking, with over 40% of urban populations using health apps regularly.

United States: Market share 38%; dominance due to extensive hospital IT infrastructure, high consumer engagement, and regulatory support for digital health platforms.

Germany: Market share 15%; strong end-user adoption in hospitals and clinics, coupled with regulatory mandates and rapid implementation of AI-enabled diagnostics.

The eHealth Market is highly competitive and moderately fragmented, with over 120 active global players offering diverse solutions across telemedicine, electronic health records, AI-powered diagnostics, and remote patient monitoring. The top 5 companies collectively hold approximately 42% of the market, highlighting both concentration among leaders and opportunities for emerging innovators. Strategic initiatives such as partnerships, joint ventures, and product launches are frequent; in 2025 alone, more than 25 major collaborations were executed to expand cloud-based health solutions and AI integration. Innovation trends, including predictive analytics, wearable devices, and interoperable health platforms, are reshaping competitive positioning, with companies emphasizing differentiation through technology, scalability, and regulatory compliance. North American firms dominate with 55% of top-tier market presence, followed by Europe (28%) and Asia-Pacific (17%). Companies are increasingly investing in cybersecurity, AI, and mobile health apps to capture patient engagement, reduce operational bottlenecks, and address regional regulatory requirements. Market leaders are also focusing on M&A to consolidate smaller players and accelerate platform adoption, reflecting the dynamic and evolving competitive landscape.

Athenahealth

McKesson Corporation

Philips Healthcare

Siemens Healthineers

GE Healthcare

Medtronic

Teladoc Health

The eHealth Market is being significantly shaped by advanced technologies that enhance operational efficiency, patient care, and clinical outcomes. Electronic Health Records (EHR) remain foundational, with over 95% of hospitals in North America and 78% in Europe implementing certified EHR systems by 2025. Cloud-based platforms are enabling seamless data sharing across multiple facilities, reducing administrative delays by 28% and minimizing duplicate tests by 18%.

Artificial intelligence (AI) and machine learning are increasingly integrated into diagnostics, predictive analytics, and patient monitoring. AI-assisted imaging has improved diagnostic accuracy by up to 30%, while predictive algorithms deployed in hospitals have reduced emergency readmissions by 15–20%. Telemedicine platforms are expanding rapidly, with over 62% of healthcare providers offering remote consultations, and mobile health apps are used by more than 60 million chronic care patients globally for real-time monitoring and adherence tracking.

Internet of Things (IoT) devices, including wearable sensors and connected medical devices, provide continuous patient data, enabling clinicians to intervene 20% faster during critical events. Interoperability standards and application programming interfaces (APIs) are facilitating integration of disparate systems, supporting coordinated care and population health analytics.

Emerging technologies, such as virtual reality (VR) for rehabilitation, blockchain for secure patient data, and edge computing for real-time analytics, are gaining traction. Hospitals piloting VR programs in 2025 reported a 22% improvement in patient engagement during therapy sessions. Collectively, these technologies are driving digital transformation, improving clinical efficiency, and positioning the eHealth Market as a technology-first, patient-centric ecosystem.

• In February 2024, Epic Systems launched a unified patient mobile application that integrates medical records, appointment scheduling, and telehealth services, enhancing patient engagement and streamlining access to care across its extensive provider network.

• In March 2025, Teladoc Health introduced an integrated virtual care model that combines primary care, mental health support, and chronic condition management under a single subscription service, aimed at increasing user retention and expanding its reach among employers and health plans.

• In April 2024, Siemens Healthineers unveiled a cloud-based imaging informatics platform connecting radiology departments across multi-hospital networks, enhancing centralized reporting and accelerating AI-assisted diagnosis workflows in large health systems.

• In August 2025, Teladoc Health expanded its digital health offerings through the acquisition of UpLift for approximately $30 million in cash, strengthening its mental health services and broadening comprehensive digital care solutions.

The eHealth Market Report provides a comprehensive view of digital healthcare solutions, addressing coverage across product types, applications, technologies, and regional markets in the global healthcare ecosystem. It examines key segments, including electronic health records (EHR), telemedicine platforms, remote patient monitoring devices, AI-enabled diagnostics, and mobile health applications, offering insights into feature differentiation, adoption drivers, and implementation strategies. The report analyzes application areas like hospital workflow optimization, teleconsultation services, chronic disease management, and patient engagement tools, highlighting how digital tools enhance clinical efficiency and patient care delivery.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa, providing volume-based segmentation and demand patterns across heterogeneous healthcare infrastructures. It profiles technology trends influencing the market, such as cloud-based interoperability, IoT-connected devices, AI-powered analytics, and secure data platforms, describing how these innovations support organizational objectives and clinical workflows without repeating previously detailed historical developments. Emerging niches such as digital therapeutics, predictive care solutions, and integrated care ecosystems are evaluated for their impact on healthcare practices and strategic investments.

The report also addresses end-user dynamics, covering hospitals, clinics, home care providers, and individual patient adoption behaviors, emphasizing variations in digital literacy, infrastructure readiness, and regional regulatory frameworks that shape implementation. It underscores operational, compliance, and security considerations crucial to stakeholders in technology planning and deployment. Overall, the report equips business leaders, healthcare administrators, and technology investors with a clear and structured understanding of the eHealth landscape, enabling data-informed decisions across competitive, technological, and consumer engagement dimensions.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD V2025 Million |

Market Revenue in 2033 | USD V2033 Million |

CAGR (2026 - 2033) | 9.2% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Epic Systems, Cerner Corporation, Allscripts Healthcare Solutions, Athenahealth, McKesson Corporation, Philips Healthcare, Siemens Healthineers, GE Healthcare, Medtronic, Teladoc Health |

Customization & Pricing | Available on Request (10% Customization is Free) |