Reports

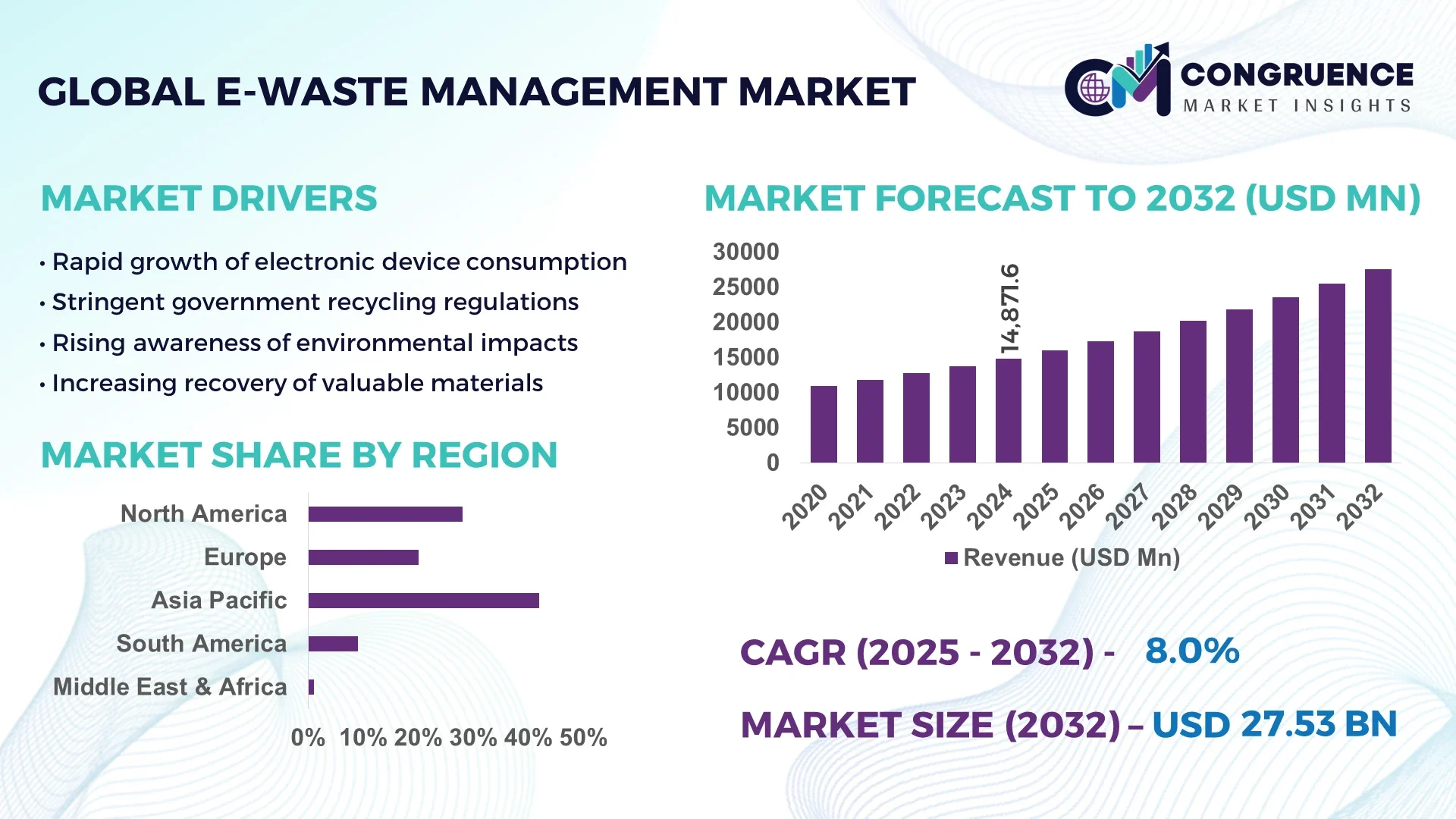

The Global E-waste Management Market was valued at USD 14,871.6 Million in 2024 and is anticipated to reach a value of USD 27,526.29 Million by 2032, expanding at a CAGR of 8.0% between 2025 and 2032. This growth is driven by increasing electronic consumption and stringent environmental regulations.

China, a dominant player in the e-waste management market, has significantly enhanced its recycling infrastructure. The nation has invested in advanced processing technologies, leading to improved recovery rates of valuable materials like gold, copper, and rare earth elements. In 2024, China processed over 10 million metric tons of e-waste, accounting for a substantial portion of the global total. Government support through policies such as Extended Producer Responsibility (EPR) and investment in recycling facilities has bolstered the industry's capacity. Additionally, China's focus on developing a circular economy has spurred innovation in e-waste recycling methods, positioning the country as a leader in sustainable electronic waste management.

Market Size & Growth: Valued at USD 14.87 billion in 2024, projected to reach USD 27.53 billion by 2032, with a CAGR of 8.0%. Growth is fueled by rising electronic consumption and stringent environmental regulations.

Top Growth Drivers: Adoption of recycling technologies: 35%, Implementation of EPR policies: 30%, Consumer awareness initiatives: 25%

Short-Term Forecast: By 2028, recycling efficiency is expected to improve by 15%, driven by technological advancements and policy enforcement.

Emerging Technologies: AI-driven waste sorting systems, Hydrometallurgical extraction techniques, Blockchain for waste tracking and transparency

Regional Leaders: Asia Pacific: USD 12.5 billion by 2032, focusing on electronic product recycling; North America: USD 7.8 billion by 2032, emphasizing consumer electronics recycling; Europe: USD 5.6 billion by 2032, driven by stringent environmental regulations

Consumer/End-User Trends: Increased adoption of recycling programs by consumers and businesses, with a growing preference for certified e-waste disposal services

Pilot or Case Example: In 2023, a pilot project in Germany demonstrated a 20% reduction in e-waste processing time through automated sorting technologies

Competitive Landscape: Leading companies include Sims Limited (25% market share), Umicore, Veolia, and Stena Recycling

Regulatory & ESG Impact: Implementation of the E-Waste (Management) Rules, 2022, has led to increased compliance and formalization of e-waste recycling practices

Investment & Funding Patterns: Recent investments totaling USD 2.5 billion have been directed towards developing recycling infrastructure and technology

Innovation & Future Outlook: Ongoing research into rare earth element recovery and the development of sustainable recycling processes are expected to shape the future of the industry

The e-waste management market is growing rapidly due to rising electronic consumption and stricter environmental regulations. Key sectors include consumer electronics, IT, and household appliances. Technological innovations like AI-driven sorting and hydrometallurgical extraction enhance material recovery. Asia Pacific leads in e-waste generation, while circular economy adoption drives sustainable growth globally.

The strategic relevance of the E-waste Management Market lies in its critical role in environmental sustainability, resource recovery, and regulatory compliance. Advanced recycling technologies, such as AI-driven sorting systems, deliver a 50% improvement in processing efficiency compared to traditional manual methods. Asia Pacific dominates in volume, while Europe leads in adoption with over 70% of enterprises implementing formal recycling practices. By 2027, AI-enabled recycling is expected to reduce contamination rates by 30%, improving the quality of recovered materials.

Firms are committing to ESG improvements, targeting a 50% reduction in e-waste sent to landfills by 2030. In 2024, a leading electronics manufacturer in Germany achieved a 25% reduction in e-waste through automated recycling technologies. The integration of machine learning, hydrometallurgical extraction, and circular economy principles supports measurable efficiency gains while ensuring compliance. Forward-looking strategies emphasize innovation, digitalization, and sustainable practices. The E-waste Management Market is poised to become a pillar of resilience, compliance, and sustainable growth, offering long-term value for stakeholders and the environment.

The E-waste Management Market is shaped by rising electronic consumption, shorter product lifecycles, and increasing regulatory pressure. Growing volumes of discarded electronics are driving demand for efficient recycling and recovery solutions. Policies such as Extended Producer Responsibility (EPR) and Waste Electrical and Electronic Equipment (WEEE) directives compel manufacturers to manage product end-of-life responsibly. Consumer awareness of sustainable disposal practices, coupled with corporate ESG commitments, is further accelerating adoption of advanced recycling technologies. Emerging trends include automation, AI-driven sorting, and integration of circular economy principles, ensuring resource conservation, environmental protection, and operational efficiency in the sector.

Technological innovations are key growth drivers for the E-waste Management Market. AI-driven sorting systems, robotics, and hydrometallurgical extraction techniques have significantly enhanced efficiency and recovery rates of valuable materials like gold, copper, and rare earth metals. AI-powered processes deliver 50% faster sorting accuracy compared to manual methods, reducing contamination and operational costs. Enterprises adopting these solutions report measurable improvements in processing capacity and sustainability compliance. Increased automation and integration of smart technologies are enabling recyclers to meet stricter environmental regulations while maximizing resource recovery, positioning technology adoption as a primary catalyst for market expansion.

High operational and infrastructure costs remain a significant restraint for the E-waste Management Market. Setting up automated recycling plants and advanced material recovery systems requires substantial capital investment, often exceeding USD 5–10 million per facility. Maintenance of AI-enabled sorting machinery and compliance with strict environmental standards further adds to expenditure. In regions with low regulatory enforcement, informal recycling remains prevalent due to cheaper alternatives, reducing the adoption of formal processes. These cost barriers hinder small and medium enterprises from scaling operations, limiting overall market penetration despite growing electronic waste volumes.

Urbanization and digital transformation offer significant opportunities for the E-waste Management Market. Rapid growth in smart cities, IoT adoption, and increased use of consumer electronics is generating higher volumes of e-waste, creating demand for efficient recycling solutions. Governments and enterprises are investing in AI-based sorting, blockchain tracking, and modular recycling plants to enhance efficiency. For example, pilot projects in India and Southeast Asia have demonstrated up to 35% higher material recovery using automated technologies. Expansion into untapped emerging markets and development of circular economy models are poised to deliver measurable environmental and operational benefits.

Regulatory compliance and workforce skill shortages present challenges for the E-waste Management Market. Navigating complex local and international e-waste regulations, such as EPR mandates, requires significant investment in reporting, certification, and operational upgrades. Moreover, skilled personnel for operating AI-driven sorting systems and hydrometallurgical plants are limited, causing operational bottlenecks. Informal recycling channels in developing regions further complicate compliance and reduce efficiency. Addressing these challenges requires targeted training programs, investments in technology, and stronger regulatory enforcement to ensure consistent, sustainable growth across the global market.

The E-waste Management market is segmented by type, application, and end-user to capture industry-specific insights. Types include large household appliances, IT and telecommunications equipment, consumer electronics, and lighting equipment, with large appliances leading adoption due to higher material volumes. Applications range from material recovery and recycling services to refurbishment and disposal solutions, with material recovery contributing the largest share. End-users include households, enterprises, and government organizations, with enterprises currently leading adoption due to regulatory compliance and sustainability commitments. Regional variations highlight Asia Pacific in volume generation, Europe in formal adoption, and North America in technology integration. Emerging trends include circular economy adoption, AI-driven recycling, and increased ESG compliance, providing targeted decision-makers with actionable market intelligence.

Large household appliances currently account for 40% of market adoption due to their high material content and established recycling channels. IT and telecommunications equipment represent 30%, while consumer electronics hold 20% of the market. Lighting equipment and other small electronics comprise the remaining 10%, serving niche applications or specialized recovery processes. The fastest-growing type is consumer electronics, driven by the proliferation of smartphones, laptops, and smart devices, with adoption expected to surpass 35% by 2032.

Material recovery is the leading application segment, representing 45% of the E-waste Management market, due to high demand for metals like copper, gold, and rare earth elements. Recycling services for consumer electronics are growing fastest, fueled by increased device turnover and regulatory compliance, expected to account for 35% of adoption by 2032. Other applications, including refurbishment and disposal, contribute 20% collectively. In 2024, more than 38% of enterprises globally reported piloting AI-based recycling systems to improve efficiency. Additionally, over 60% of Gen Z consumers prefer brands with sustainable e-waste practices.

Enterprises are the leading end-user segment, holding 50% of market adoption due to compliance with environmental regulations and sustainability goals. Households contribute 30%, driven by consumer awareness and collection programs, while government and public institutions account for the remaining 20%. The fastest-growing end-user segment is households, supported by digital collection initiatives and public awareness campaigns, projected to reach 40% adoption by 2032. In 2024, over 38% of households in Germany participated in formal e-waste collection programs.

Asia-Pacific accounted for the largest market share at 42% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 7.5% between 2025 and 2032.

In 2024, Asia-Pacific processed over 22 million metric tons of e-waste, with China alone contributing 10 million metric tons. India and Japan follow closely with 5.2 million and 3.8 million metric tons, respectively. Europe accounted for 25% of the market volume, with Germany handling 4.1 million metric tons. North America’s e-waste volume reached 6.5 million metric tons, with high adoption in corporate and healthcare sectors. South America contributed 5%, led by Brazil and Argentina, while the Middle East & Africa collectively held 3%, driven by emerging industrial and oil & gas sectors. Increasing electronic consumption, government initiatives, and investment in recycling infrastructure are shaping the regional dynamics and adoption patterns across all continents.

How is digital transformation influencing operational efficiency in recycling?

North America held 23% of the E-waste Management market in 2024, with high adoption across healthcare, finance, and IT industries. Regulatory support from agencies like the Environmental Protection Agency (EPA) has strengthened compliance and promoted formal recycling channels. Technological advancements such as AI-driven sorting, IoT-enabled tracking, and automation are improving material recovery rates and reducing processing times. Local players, such as Sims Lifecycle Services, are implementing robotic-assisted disassembly lines, achieving up to 30% faster throughput. Enterprise adoption is higher in the U.S. and Canada, with over 60% of large organizations integrating formal e-waste collection and recycling programs. Consumer awareness campaigns and sustainability mandates are further accelerating adoption, while digital tracking ensures compliance and ESG alignment.

What strategies are European firms using to comply with regulatory mandates in recycling?

Europe accounted for 25% of the E-waste Management market in 2024, with Germany, the UK, and France as leading contributors. Stringent regulations, including WEEE directives and Extended Producer Responsibility (EPR) mandates, have driven demand for formal recycling and explainable processes. Emerging technologies like AI-assisted sorting, blockchain tracking, and automated material recovery are increasingly adopted. Local players, including Umicore, have implemented advanced hydrometallurgical extraction techniques, improving precious metal recovery by 28%. Regional adoption trends are shaped by regulatory compliance, with enterprises and municipalities prioritizing traceable recycling programs and sustainable disposal practices. Consumers are more likely to engage in certified e-waste drop-off initiatives due to strong environmental awareness.

How are top Asian countries leveraging infrastructure to handle rising e-waste volumes?

Asia-Pacific represented the largest market share at 42% in 2024, led by China, India, and Japan. The region has heavily invested in recycling plants, modular processing facilities, and automated sorting infrastructure to manage over 22 million metric tons of e-waste. Local technology hubs are integrating AI, IoT, and robotics for improved material recovery and operational efficiency. Local players, such as TES-AMM in Singapore, are pioneering multi-step recycling processes for consumer electronics. Consumer adoption is driven by e-commerce growth, mobile device proliferation, and government initiatives promoting circular economy models. Regional innovation trends focus on sustainable recovery of precious metals and reducing landfill disposal.

What initiatives are driving e-waste processing and collection in key countries?

South America contributed approximately 5% of the global E-waste Management market in 2024, with Brazil and Argentina as key players. The region is witnessing infrastructure upgrades in urban centers, particularly in waste collection and energy-efficient recycling plants. Government incentives and trade policies encourage formal recycling, while private enterprises invest in AI-based sorting and material recovery. Local players, such as ReciclaBR in Brazil, have implemented automated collection systems that improved recovery efficiency by 20%. Consumer behavior is influenced by media campaigns and localized awareness programs, driving participation in recycling initiatives across major cities.

How are emerging industries shaping the adoption of e-waste solutions?

The Middle East & Africa held 3% of the E-waste Management market in 2024, with the UAE and South Africa leading demand. Growth is driven by oil & gas, construction, and telecom sectors, with increasing adoption of AI and automated recycling solutions. Technological modernization initiatives include digital tracking, robotics, and modular processing units. Local players like Enviroserve in the UAE are enhancing e-waste processing efficiency through smart sorting systems. Consumer adoption varies, with enterprises showing higher engagement in compliance-driven programs, while public participation is increasing via government-led awareness campaigns and incentive schemes.

China | Market share: 18% | Dominance due to high production capacity, advanced recycling infrastructure, and large-scale electronic consumption.

United States | Market share: 15% | Strong end-user demand and regulatory push for compliance and sustainable e-waste disposal.

The global E-waste Management market is highly competitive and fragmented, with over 3,900 active companies operating worldwide. The top five players—Veolia Environnement SA, Sims Lifecycle Services, Umicore SA, TES – Sustainable IT Lifecycle Services, and Electronic Recyclers International (ERI)—together hold approximately 25% of the market share, indicating significant influence while leaving substantial room for mid-sized and regional firms.

Key strategic initiatives among market leaders include mergers and acquisitions, partnerships, and expansion into emerging markets. Technological innovation is a major competitive driver, with companies increasingly implementing AI-driven sorting, IoT-based tracking, and automated recycling systems to enhance operational efficiency, material recovery, and compliance with stringent environmental regulations.

Smaller and regional players are leveraging local expertise and niche services to gain market share, while large players focus on global expansion and integrated recycling solutions. The growing emphasis on sustainability, ESG compliance, and circular economy principles is shaping competition, encouraging firms to adopt transparent and eco-friendly processes. Overall, innovation, strategic collaborations, and operational excellence are defining the competitive landscape of the E-waste Management market.

TES – Sustainable IT Lifecycle Services

Electronic Recyclers International (ERI)

Boliden AB

MBA Polymers, Inc.

Stena Technoworld AB

Tetronics (International) Ltd.

Enviro-Hub Holdings Ltd.

The E-waste Management market is witnessing significant technological advancements aimed at enhancing efficiency, sustainability, and regulatory compliance. AI-powered sorting systems are now widely adopted to automatically classify and separate e-waste components, achieving material recovery rates of up to 90% compared to conventional manual sorting methods. These systems use machine learning algorithms to detect metals, plastics, and circuit boards, improving precision while reducing operational risks. Robotic disassembly is another transformative technology, enabling safe and efficient dismantling of electronic devices. Automated robotic arms can disassemble complex electronics, such as smartphones and laptops, 30–40% faster than manual processes while minimizing exposure to hazardous materials like lead and mercury.

Emerging hydrometallurgical and bioleaching methods are being increasingly implemented to recover valuable metals such as gold, silver, and copper. Hydrometallurgy employs aqueous chemical solutions for selective metal extraction, while bioleaching utilizes microorganisms to leach metals in an eco-friendly manner. These techniques reduce energy consumption and lower environmental impact compared to traditional smelting. IoT-enabled e-waste tracking is revolutionizing logistics and supply chain transparency. Sensors and cloud-based monitoring systems allow real-time tracking of waste collection, transport, and processing, enabling precise reporting and compliance with regulatory requirements.

Furthermore, circular economy integration is driving manufacturers to adopt modular and recyclable designs, improving product lifecycle management and facilitating easier end-of-life recovery. Pilot programs in North America and Europe using AI-assisted recycling systems have improved operational efficiency by 25–30%, demonstrating measurable performance gains. These technologies collectively enhance the scalability, sustainability, and profitability of e-waste management operations.

In August 2024, the Royal Mint of the United Kingdom inaugurated a new facility in South Wales dedicated to extracting gold from electronic waste, including items like televisions, laptops, and mobile phones. Utilizing patented chemistry from the Canadian clean tech company Excir, the 3,700-square-meter plant aims to process up to 4,000 metric tons of printed circuit boards annually, contributing to decarbonizing operations and reducing reliance on traditional mining practices.

In May 2024, Mumbai's Brihanmumbai Municipal Corporation (BMC), in collaboration with Electrofine Recycling, collected over 15,000 kg of electronic waste from various establishments, including residential societies, schools, corporates, government offices, and small businesses. This initiative marks a significant step in the city's e-waste management efforts, as it previously lacked a dedicated e-waste collection service.

In March 2024, Delhi announced plans to establish India's first state-of-the-art e-waste eco park in Holambi Kalan. Spanning 11.4 acres, the facility is designed to process up to 51,000 metric tonnes of e-waste annually and is expected to generate more than ₹350 crore in revenue. The park will include zones for dismantling, refurbishing, plastic recovery, and second-hand electronics, along with training centers for informal workers, creating over 1,000 green jobs.

In February 2024, the Ahmedabad Municipal Corporation (AMC) relaunched its e-waste collection service, authorizing three agencies to manage the city's electronic waste and offering compensation to residents for their e-waste contributions. This initiative aims to streamline waste processing while improving working conditions and sustainability.

The E-waste Management Market Report delivers an in-depth assessment of the global landscape, offering a precise understanding of market segments, geographic regions, applications, and emerging technologies. It captures the scale of e-waste generation, which surpassed 62 million metric tons globally in 2023, and evaluates the infrastructure required to handle projected growth through 2032. This report examines market segmentation across key product categories, including consumer electronics, IT equipment, and household appliances, detailing their respective contributions to the overall volume. It highlights regional insights by analyzing leading markets in North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, identifying countries driving demand with notable recycling and collection capacities.

The report also investigates technological innovations shaping e-waste management, such as AI-based sorting, robotic disassembly, and advanced hydrometallurgical recovery methods. It assesses how these technologies enhance recovery rates and reduce environmental impact while improving operational efficiency. In addition, it explores the regulatory frameworks and policy initiatives influencing industry practices, such as Extended Producer Responsibility and mandatory recycling targets. The analysis offers valuable guidance for industry stakeholders, enabling strategic decisions across manufacturing, logistics, and material recovery to optimize operations in a rapidly expanding market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 14871.6 Million |

|

Market Revenue in 2032 |

USD 27526.29 Million |

|

CAGR (2025 - 2032) |

8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Veolia Environnement SA, Sims Lifecycle Services, Umicore SA, TES – Sustainable IT Lifecycle Services, Electronic Recyclers International (ERI), Boliden AB, MBA Polymers, Inc., Stena Technoworld AB, Tetronics (International) Ltd., Enviro-Hub Holdings Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |