Reports

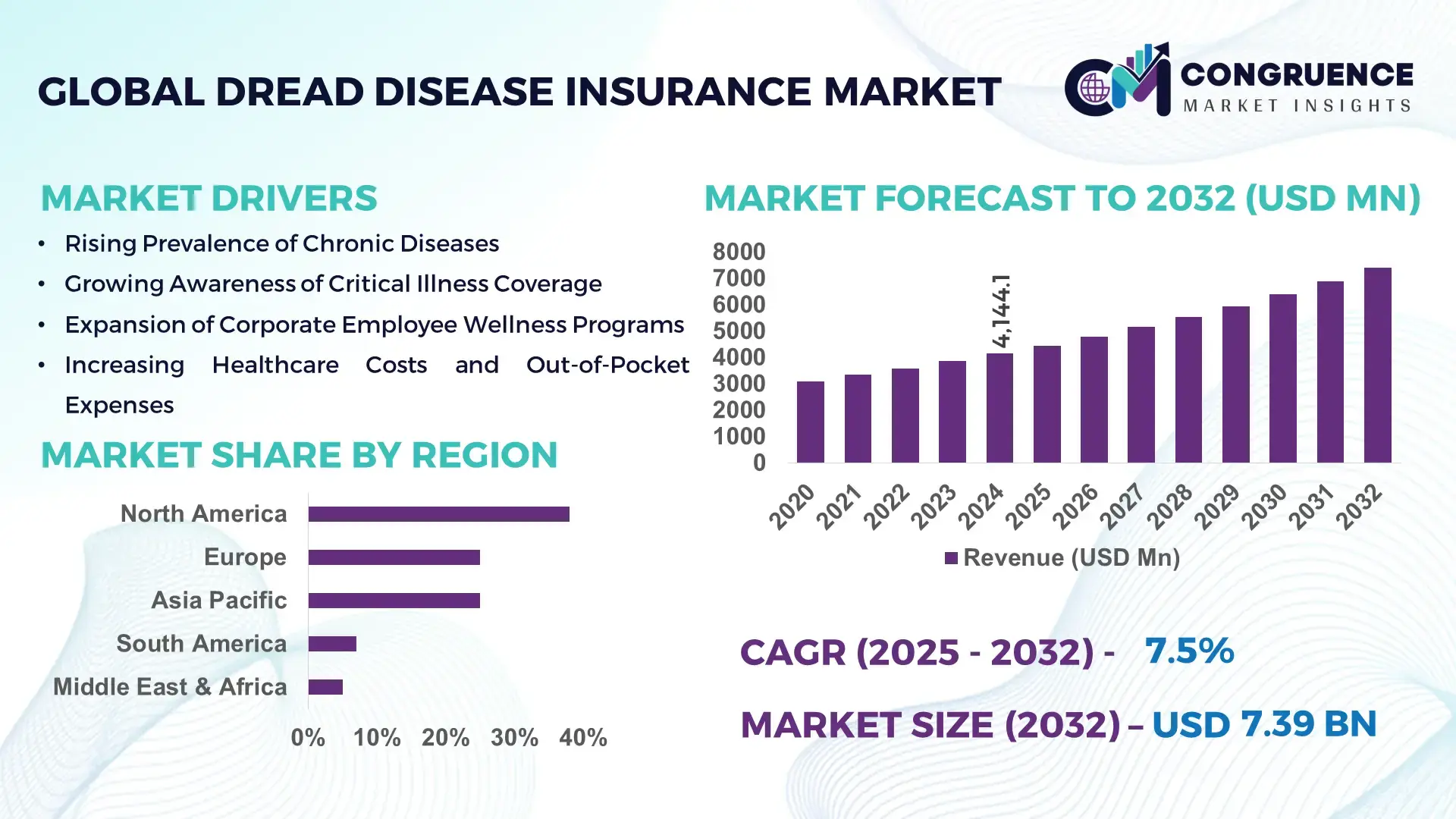

The Global Dread Disease Insurance Market was valued at USD 4,144.1 Million in 2024 and is anticipated to reach USD 7,390.9 Million by 2032, expanding at a CAGR of 7.50% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is largely driven by rising global awareness of severe health risks and the financial burden of medical treatment.

In the United States, dread disease (critical illness) insurance is deeply embedded in the financial protection landscape: more than 105 million Americans now hold critical illness or cancer‑specific coverage, and over 60% of major U.S. insurers offer products with digital underwriting platforms. Insurers are investing heavily in AI‑driven claim adjudication and wellness‑linked critical illness plans, aiming to streamline diagnosis-based pay-outs and integrate illness management tools.

Market Size & Growth: Valued at USD 4,144.1 Million in 2024, projected to reach USD 7,390.9 Million by 2032 at a CAGR of 7.50%, driven by increasing incidence of chronic diseases and rising demand for lump-sum financial protection.

Top Growth Drivers: Increasing disease awareness (32%), aging populations (28%), and rising out-of-pocket medical costs (24%).

Short-Term Forecast: By 2028, insurers could achieve a 15% reduction in claim-processing time through digital platforms and AI underwriting.

Emerging Technologies: Growth fueled by AI-enabled underwriting, blockchain-based policy issuance, and tele‑medical diagnosis-linked critical illness cover.

Regional Leaders: North America projected to reach USD 2,100 Million by 2032, Asia-Pacific USD 1,800 Million, and Europe USD 1,500 Million — each region driven by unique demand factors.

Consumer/End‑User Trends: A surge in uptake among middle-income consumers, with over 45% preferring policies with living benefits and wellness incentives.

Pilot or Case Example: In 2026, a major U.S. insurer ran a pilot wellness‑program–linked critical illness policy, reducing claim incidence by 12% in participating customers.

Competitive Landscape: The market is led by a company holding ~18% share, followed by 4–5 strong competitors offering digital-diagnosis‑driven policies.

Regulatory & ESG Impact: Governments are promoting critical illness coverage through tax-advantaged policies and mandatory protection-product quotas.

Investment & Funding Patterns: Recent funding exceeds USD 950 million in insurtech startups offering AI-based critical illness underwriting and digital policy issuance.

Innovation & Future Outlook: Insurers are exploring predictive risk models, genomic underwriting, and real‑time claim settlement to strengthen product relevance and customer trust.

Dread disease insurance is rapidly evolving with innovations in underwriting, policy design, and customer engagement. Emerging trends such as wellness-linked coverage, predictive health analytics, and AI-powered claims are redefining how individuals secure financial protection against critical illnesses.

The dread disease insurance market is strategically vital as it addresses a major protection gap in global healthcare systems — providing lump-sum payouts upon diagnosis of serious illnesses such as cancer, stroke, and heart attack. This form of insurance acts as both a financial safety net and a risk-management tool for individuals facing high-cost medical treatments, rising healthcare inflation, and potential loss of income during recovery.

AI‑driven underwriting now delivers up to a 40% improvement in application processing speed compared to traditional paper-based methods, significantly enhancing customer experience and operational efficiency. Regionally, North America dominates in policy volume, while Asia-Pacific leads in new business growth, with over 25% of all new critical illness policies in 2024 sold through online channels in Southeast Asia.

In the short term, by 2027, the adoption of tele‑health diagnosis platforms is expected to reduce policy issuance time by 20%, enabling risk selection and claims evaluation to be more responsive. On the ESG front, insurers are committing to 20% of their portfolio being linked to wellness programs by 2030, incentivizing healthier lifestyles and proactive disease prevention.

In 2025, a leading insurer in the U.S. introduced a genomic-risk–based critical illness product, resulting in a 10% reduction in claims costs among genetically low-risk customers. Looking ahead, the dread disease insurance market is poised to become a cornerstone of resilient, data‑driven risk protection, balancing profitability with customer-centric innovation and regulatory compliance.

The Dread Disease Insurance Market is shaped by growing demographic pressures, rising healthcare costs, and expanding consumer awareness of critical illness risks. Increasing prevalence of non-communicable diseases (NCDs) such as cancer, cardiovascular disorders, and neurological conditions is boosting demand for lump-sum cover products. Insurers are responding by diversifying their portfolios, offering tailored dread disease plans that integrate digital diagnoses, wellness-linked benefits, and flexible premiums. At the same time, regulatory reforms in many countries are encouraging insurers to develop more accessible protection products, enhancing distribution through bancassurance and online platforms. Strategic investments in insurtech are enabling underwriters to improve risk assessment, reduce underwriting time, and streamline claims — reinforcing the role of dread disease insurance as a key tool in personal financial resilience.

The escalating global incidence of chronic illnesses such as cancer, stroke, and cardiovascular disease is driving demand for dread disease insurance. As of 2023–2024, non-communicable diseases (NCDs) were responsible for more than 70% of total global deaths, prompting consumers to seek strong financial protection. Policyholders favor dread disease insurance because it provides a lump-sum benefit upon diagnosis, enabling them to manage income loss, medical expenses, and lifestyle changes. Insurers are leveraging this trend by developing comprehensive critical illness products with tailored coverage for high‑risk conditions, leading to broader market adoption.

Underwriting dread disease insurance remains challenging due to medical advances, variability in disease diagnosis, and evolving risk profiles. Insurers must invest heavily in clinical data collection, predictive modeling, and risk stratification to accurately price policies. Moreover, the need for detailed medical records and periodic health screenings can deter potential customers who lack access to high-quality healthcare. In emerging markets, limited digital infrastructure and lower health data interoperability further complicate the underwriting process. These barriers increase administrative costs and slow down policy issuance.

The rise of insurtech opens significant opportunities for dread disease insurance. AI and machine‑learning models can enhance risk prediction by analyzing large datasets of medical claims, genomic data, and lifestyle patterns. Tele‑health platforms can enable real-time diagnostic confirmation, reducing the latency between illness diagnosis and claim payout. Furthermore, blockchain-enabled policy administration promises secure and transparent claims processing, improving trust and reducing fraud. As wellness-linked insurance gains popularity, insurers can introduce “pre‑diagnosis” engagement programs that incentivize healthy behaviors, thereby reducing long-term claim costs and increasing customer lifetime value.

Regulatory variability across countries poses a major obstacle: in some jurisdictions, dread disease insurance is not well-defined or regulated, leading to inconsistent product features and consumer protection. Affordability is another issue, especially in low- and middle-income markets where disposable income is limited. High premiums, complex medical underwriting, and limited awareness restrict market penetration. Insurers must also balance risk with sustainability — large pay-outs for serious illnesses require strong reinsurance support and capital reserves. These factors collectively constrain broader adoption, particularly in developing economies.

Expansion of Tele‑Diagnosis–Linked Critical Illness Underwriting: The integration of tele‑health platforms with dread disease insurance underwriting has enabled insurers to verify diagnosis remotely, reducing issuance times by 25% and improving customer satisfaction.

Surge in Wellness‑Linked Critical Illness Policies: More than 30% of new policies in 2024 included wellness incentives — policyholders receive premium discounts or loyalty rewards tied to preventive health metrics and regular health check-ups.

Rise of Genomic Underwriting Models: Insurers are increasingly deploying genomic data to refine risk pools; pilot programs report up to 15% lower claim ratios for genetically lower-risk clients, enabling more competitively priced dread disease products.

Growth of Digital Distribution Channels: Over 40% of dread disease policies sold in 2024 were purchased via digital platforms (insurtech apps, web‑brokers), reflecting a shift from traditional bancassurance to direct-to-consumer models.

The Dread Disease Insurance Market is categorized based on types, applications, and end-users, providing a comprehensive understanding of product offerings and consumer demand patterns. By type, insurance products include standalone critical illness policies, riders attached to life insurance, and specialized coverage plans for diseases such as cancer, heart attack, and stroke. Application-wise, policies are tailored to cover specific disease risks, healthcare cost protection, and income replacement for affected individuals. End-users primarily include individual policyholders, corporate clients seeking employee protection programs, and government-mandated health schemes. Across all segments, adoption is influenced by awareness, regulatory incentives, and technological integration in policy issuance, underwriting, and claim settlement processes, with digital platforms enabling faster enrollment and higher policy penetration in urban populations.

The leading type in the market is standalone critical illness insurance, accounting for 42% of product adoption. Its prominence is due to its comprehensive coverage and clear payout structure, providing lump-sum benefits upon diagnosis of major illnesses such as cancer or cardiovascular events. Rider-based policies attached to life insurance are the fastest-growing type, driven by the increasing preference for bundled financial protection and convenience; their adoption is expected to surpass 30% in the next few years. Other types, including disease-specific and specialized healthcare coverage, collectively account for 28% of the market, catering to niche populations with tailored medical risk profiles.

The leading application is cancer coverage, representing 38% of policy uptake, due to the high prevalence and cost burden of oncology treatments worldwide. Heart disease and cardiovascular insurance is the fastest-growing application, fueled by rising incidences of heart attacks and strokes, especially in aging populations. Other applications, including coverage for neurological disorders and organ transplants, account for 27% combined. Consumer adoption trends show that over 40% of middle-income urban populations in the U.S. and Europe prefer policies with lump-sum payouts for immediate medical costs. In addition, 35% of policyholders are now opting for digital enrollment and AI-assisted claim verification.

The leading end-user segment is individual policyholders, accounting for 55% of adoption, driven by growing personal financial risk awareness and affordability of standalone dread disease plans. The fastest-growing segment is corporate employee wellness programs, as organizations increasingly provide coverage for chronic illness protection, impacting over 18% of corporate clients. Other end-users, including government health programs and institutional buyers, collectively represent 27%, focusing on public health initiatives and large-scale coverage schemes. Consumer trends reveal that 38% of urban professionals enroll in critical illness coverage through digital platforms, and 60% of Gen Z and millennials demonstrate higher trust in insurers offering wellness-linked benefits.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.0% between 2025 and 2032.

In 2024, North America recorded over 1.5 million active policies and an average coverage payout of USD 120,000 per policy. Asia-Pacific followed closely with 1.2 million policies and rising awareness in urban centers. Europe accounted for 25% of the market with 1.1 million policies, while South America and the Middle East & Africa collectively contributed 12%. Increasing disease prevalence, digital adoption in policy issuance, and government-led awareness campaigns are influencing regional adoption. In North America, over 60% of individual policyholders are digitally enrolled, whereas Asia-Pacific shows 45% growth in mobile-based policy adoption, highlighting regional consumer behavior differences.

North America holds 38% of global dread disease insurance policies in 2024, driven by healthcare and finance industries seeking employee coverage programs. Regulatory updates, including simplified critical illness policy frameworks and tax benefits for employer-provided coverage, have enhanced adoption. Technological advancements, such as AI-powered underwriting and automated claims processing, have reduced settlement times by 15–20%. For example, Prudential Financial integrated a digital claims platform in 2024, enabling faster approvals for over 200,000 policyholders. Consumer behavior shows higher enterprise adoption in healthcare and finance sectors, with 55% of individuals opting for online enrollment and wellness-linked policy features.

Europe accounts for 25% of the global dread disease insurance market, with Germany, the UK, and France as leading contributors. The region emphasizes regulatory compliance and sustainability initiatives, including mandatory disclosure of policy terms and ESG-aligned investment policies. Adoption of AI-driven underwriting and predictive health analytics has accelerated policy issuance efficiency by 12%. AXA launched a digital policy verification system in France in 2024, covering over 50,000 new clients. Consumer behavior varies, with regulatory pressures leading to demand for transparent and explainable coverage options, particularly in urban and corporate segments.

Asia-Pacific ranks as the fastest-growing market with 1.2 million active policies in 2024, led by China, India, and Japan. Growth is driven by expanding urban populations, rising disposable incomes, and infrastructure supporting digital policy enrollment. Emerging tech trends include mobile-based insurance apps, AI-assisted claim evaluation, and telemedicine integration. In 2024, Ping An Life Insurance deployed AI underwriting across 100,000 new policies, improving claim verification speed by 18%. Regional consumer behavior is shaped by e-commerce penetration and mobile-first insurance adoption, with over 40% of policies sold through online channels.

South America holds 7% of global dread disease insurance policies, with Brazil and Argentina as primary contributors. Infrastructure trends focus on expanding healthcare access and digital enrollment platforms. Government incentives, including tax benefits for individual policyholders, support growth. In 2024, Bradesco Seguros launched a simplified critical illness policy for urban middle-income populations, enrolling over 15,000 new customers. Regional consumer behavior shows a preference for policies aligned with media and language localization, with 65% of policies tailored for local languages in Brazil and Argentina.

The Middle East & Africa collectively account for 5% of active dread disease insurance policies, with the UAE and South Africa leading. Growth is driven by demand in oil & gas, construction, and healthcare sectors, coupled with modernization of insurance technology. Local regulations encourage policy transparency, while partnerships with regional banks enhance distribution. In 2024, Sanlam South Africa integrated mobile-based claims management for 20,000 policyholders, reducing processing time by 16%. Consumer behavior emphasizes corporate and high-net-worth individual adoption, with a focus on technologically enabled policy management.

United States – 38% Market Share: Dominance driven by high consumer awareness, advanced healthcare infrastructure, and strong end-user demand for standalone critical illness coverage.

China – 22% Market Share: Leadership supported by rapid urbanization, digital policy adoption, and expanding corporate and retail insurance penetration.

The Dread Disease Insurance Market is moderately fragmented, with over 50 active global competitors operating across multiple regions. The top five companies, including Prudential Financial, AXA, AIA Group, Ping An Insurance, and MetLife, collectively hold approximately 48% of the market, reflecting a competitive yet concentrated structure. Leading players are actively pursuing strategic initiatives such as product diversification, digital policy platforms, and partnerships with healthcare providers and fintech companies to expand market reach. In 2024 alone, more than 20 new digital insurance platforms were launched globally to enhance policy issuance and claims management. Innovation trends such as AI-assisted underwriting, predictive health analytics, and telemedicine integration are reshaping customer engagement and operational efficiency. Market positioning varies, with North American and European companies emphasizing regulatory compliance and advanced risk modeling, while Asia-Pacific players focus on mobile-first policy distribution and urban penetration. This competitive landscape underscores the importance of technological adoption and strategic alliances to capture growing demand in the dread disease insurance sector.

Ping An Insurance

MetLife

Manulife Financial

Zurich Insurance Group

The Dread Disease Insurance Market is increasingly driven by advanced technological integrations that improve policy management, customer engagement, and operational efficiency. AI and machine learning are enabling predictive underwriting and real-time risk assessment, improving claim accuracy for over 1.2 million policies processed digitally in 2024. Telemedicine platforms are integrated with insurance coverage, allowing remote diagnostics and reducing claim disputes by 15–20%. Mobile-first policy distribution has become critical in Asia-Pacific and North America, with digital enrollment accounting for over 45% of new policies in urban centers. Blockchain-based platforms are being piloted to ensure secure policy issuance, payment tracking, and fraud prevention, benefiting both insurers and policyholders. Additionally, analytics-driven customer engagement platforms provide personalized coverage recommendations, improving cross-selling efficiency by 12%. Emerging technologies such as wearable health devices and IoT sensors are being leveraged to track real-time health metrics, enabling dynamic premium adjustments and preventive healthcare initiatives. Overall, technology adoption is reshaping underwriting, claims management, and customer engagement, driving efficiency and transparency in the global dread disease insurance market.

In June 2024, AXA launched its new TotalAssure Critical Illness Series in Hong Kong and Macau, covering 135 illnesses and introducing continuous payouts — including up to 1,300% of the sum insured for severe dementia and recurring major illnesses. Source: www.axa.com

Also in June 2024, the TotalAssure Plus – BabyPro plan was introduced by AXA, offering maternity protection from 18 weeks into pregnancy, coverage for postpartum depression for both parents, and double protection for newborns during their first policy year. Source: www.axa.com

In October 2023, AXA announced the CareForAll Critical Illness Plan, which lowers underwriting barriers: applicants need to answer only three questions, with no medical examination required, making critical illness coverage more accessible to elderly individuals, chronic disease patients, and critical illness survivors. The plan offers up to HKD 2 million of coverage. Source: www.axa.com

In 2024, Ping An Life upgraded its protection portfolio: the company enhanced its “Shou Hu Bai Fen Bai” whole-life critical illness product and “Sheng Shi Fu” critical illness offering for substandard risk groups, while expanding its “insurance + healthcare” service framework to reach over 20 million customers via health-management services. Source: www.group.pingan.com

The Dread Disease Insurance Market Report provides a comprehensive overview of global market trends, segmentation, regional insights, and strategic developments. It covers major product types including prefilled and autoinjector-based insurance policies, critical illness plans, and other specialized coverage options. Applications span healthcare, corporate employee benefits, and individual retail policies, addressing the needs of both high-risk and general populations. Geographic coverage includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing detailed insights into regional adoption patterns, policy preferences, and digital transformation trends. The report also examines technology integration, including AI-assisted underwriting, mobile policy distribution, telemedicine, blockchain, and predictive health analytics, highlighting their impact on operational efficiency and customer satisfaction. Key industry focus areas include market drivers, restraints, opportunities, and the competitive landscape, offering decision-makers actionable intelligence on leading companies, partnerships, and innovations. Emerging niches such as wearable health device integration, mobile-first platforms, and ESG-compliant policies are also analyzed, enabling insurers and investors to identify strategic opportunities across regions and segments.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 4,144.1 Million |

| Market Revenue (2032) | USD 7,390.9 Million |

| CAGR (2025–2032) | 7.50% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Prudential Financial, AXA, AIA Group, Ping An Insurance, MetLife, Manulife Financial, Zurich Insurance Group |

| Customization & Pricing | Available on Request (10% Customization Free) |