Reports

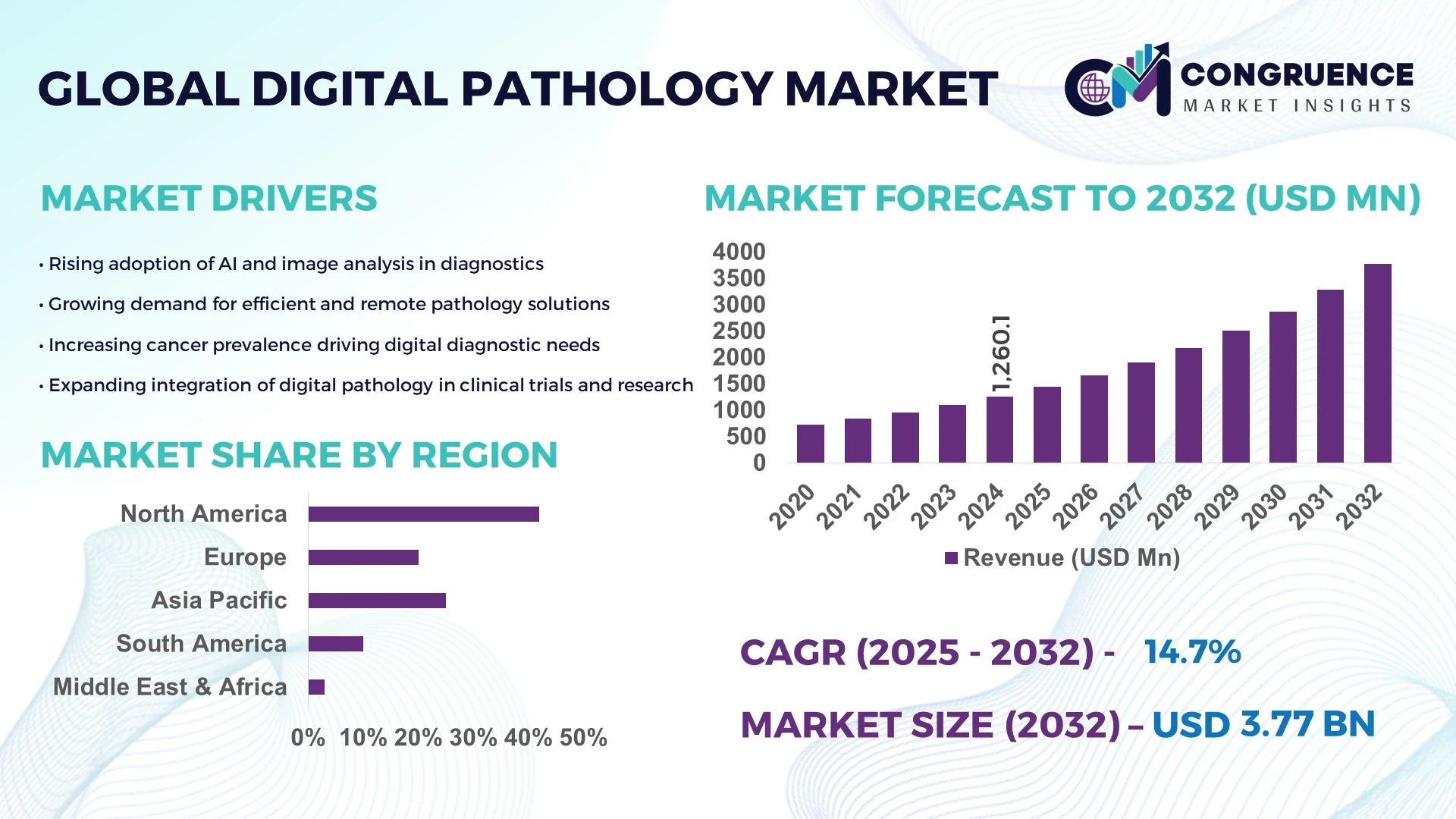

The Global Digital Pathology Market was valued at USD 1260.09 Million in 2024 and is anticipated to reach a value of USD 3774.93 Million by 2032 expanding at a CAGR of 14.7% between 2025 and 2032. The market growth is driven by rising demand for advanced diagnostic solutions and automation in pathology workflows.

The United States dominates the Digital Pathology market, with over 350 hospitals and research institutions integrating whole slide imaging (WSI) systems by 2024. The country has invested more than USD 450 Million in digital pathology infrastructure over the past three years, supporting over 200 active R&D programs focusing on AI-assisted diagnostics. Key applications include oncology, clinical research, and pharmaceutical testing, with approximately 68% of labs adopting digital workflows. Advanced image analysis tools and cloud-based pathology platforms have expanded throughput by 25%, while regional adoption in California, Texas, and Massachusetts exceeds 70% of available capacity.

Market Size & Growth: USD 1260.09 Million in 2024, projected USD 3774.93 Million by 2032, CAGR 14.7%, driven by automation and AI integration.

Top Growth Drivers: AI-assisted diagnostics adoption 45%, laboratory efficiency improvement 38%, clinical workflow automation 32%.

Short-Term Forecast: By 2028, digital slide turnaround time expected to reduce by 30%, diagnostic accuracy to improve by 22%.

Emerging Technologies: AI-powered image analysis, cloud-based pathology platforms, multiplex immunohistochemistry automation.

Regional Leaders: United States USD 1450 Million, Europe USD 1020 Million, Asia-Pacific USD 850 Million by 2032; US shows highest AI adoption rate, Europe excels in academic research integration, APAC adoption rising in private labs.

Consumer/End-User Trends: Pathology labs and hospitals increasing digital adoption for oncology, hematology, and clinical trials; 60% of labs shifting to fully digital workflows.

Pilot or Case Example: 2023 pilot in Massachusetts reduced diagnostic turnaround by 28%, improved case review efficiency by 18%.

Competitive Landscape: Philips Digital Pathology ~22% share, competitors: Leica Biosystems, Roche Diagnostics, Visiopharm, 3DHISTECH.

Regulatory & ESG Impact: FDA digital pathology approvals, HIPAA-compliant cloud solutions, ESG-driven lab modernization incentives.

Investment & Funding Patterns: Over USD 450 Million invested in infrastructure and AI R&D, increasing venture funding for pathology startups.

Innovation & Future Outlook: Integration of AI with cloud platforms, predictive analytics in clinical trials, adoption of decentralized pathology networks.

The Digital Pathology Market continues to expand across oncology, academic research, and pharmaceutical sectors, with hospitals and laboratories increasingly adopting AI-driven diagnostic systems. Recent innovations include automated staining platforms, advanced image recognition, and predictive pathology analytics. Regulatory support for digital diagnostics, combined with rising healthcare expenditure, has accelerated adoption in North America and Europe, while Asia-Pacific demonstrates growing private sector investment. Emerging trends focus on telepathology, AI-assisted cancer detection, and integration with electronic medical records, offering significant efficiency gains and improved clinical outcomes for healthcare decision-makers.

The Digital Pathology Market holds strategic relevance as healthcare providers and research institutions prioritize faster, more accurate diagnostics. AI-assisted whole slide imaging delivers up to 35% improvement in diagnostic accuracy compared to traditional microscopy, enabling earlier disease detection and enhanced treatment planning. North America dominates in volume, while Europe leads in adoption with over 65% of hospitals and laboratories integrating digital pathology solutions. By 2027, cloud-based pathology platforms are expected to reduce diagnostic turnaround times by 28%, improving workflow efficiency and patient outcomes. Firms are committing to ESG improvements such as 20% reduction in chemical waste from staining processes by 2026, aligning environmental sustainability with operational efficiency. In 2024, Philips Digital Pathology in the United States achieved a 25% reduction in manual slide review time through AI-assisted automation, demonstrating tangible productivity gains. Emerging trends include decentralized telepathology networks, predictive analytics in oncology diagnostics, and integration with electronic health records, collectively improving decision-making speed and accuracy. Forward-looking strategies emphasize the Digital Pathology Market as a pillar of resilience, compliance, and sustainable growth, positioning it as an essential component of modern healthcare infrastructure and innovation ecosystems.

AI adoption in Digital Pathology is significantly enhancing laboratory efficiency by automating slide scanning, image analysis, and reporting workflows. For example, AI-assisted image recognition platforms can classify histopathology slides up to 40% faster than manual review, reducing human error and accelerating diagnostic throughput. Oncology and hematology labs report a 20–30% reduction in case review times after integrating AI tools. Adoption is particularly strong in North America, where over 70% of academic medical centers use AI-based diagnostic systems. Pharmaceutical research labs are also leveraging AI for high-throughput tissue analysis, improving reproducibility and accuracy of preclinical studies. These developments demonstrate measurable operational gains, making AI a key driver of growth and strategic investment within the Digital Pathology Market.

High infrastructure and implementation costs remain a significant restraint for the Digital Pathology Market. Setting up high-resolution scanners, secure cloud storage, and AI-integrated software can exceed USD 500,000 per facility, making adoption challenging for smaller laboratories. Additionally, costs associated with staff training, software licensing, and system validation contribute to financial barriers. In regions such as Latin America and parts of Asia-Pacific, limited capital expenditure slows market penetration, despite growing demand for digital diagnostics. Compatibility issues with legacy laboratory information systems and regulatory compliance requirements further restrict adoption. Consequently, these financial and operational challenges create obstacles for widespread deployment, affecting the pace of digital transformation in pathology laboratories.

Telepathology presents substantial opportunities by enabling remote diagnosis, consultation, and collaborative research across regions. Hospitals and labs leveraging telepathology networks have reported up to 30% faster case turnaround and a 25% improvement in diagnostic accuracy in pilot programs. The growing need for specialist consultations in oncology and rare diseases, combined with increased cloud platform adoption, facilitates real-time slide sharing and AI-assisted analysis. Emerging markets, particularly in Asia-Pacific and the Middle East, are investing in digital infrastructure to support telepathology, opening new revenue streams for technology providers. Additionally, integration with electronic health records and AI predictive tools allows hospitals to optimize patient management and research capabilities, making telepathology a key growth avenue for the Digital Pathology Market.

Regulatory compliance and data security pose significant challenges for the Digital Pathology Market. Digital slide storage, transmission, and AI-assisted analysis must adhere to HIPAA, GDPR, and FDA regulations, requiring robust encryption and audit trails. Any breach or non-compliance can lead to substantial legal and financial penalties. Additionally, implementing standardized protocols across multinational laboratories is complex, as regional regulatory requirements vary significantly. Smaller laboratories face resource constraints in meeting compliance standards, delaying adoption. Cybersecurity threats targeting cloud-based pathology systems further increase operational risks, demanding continuous monitoring and investment. These regulatory and security hurdles present a critical barrier to seamless integration and expansion of digital pathology solutions globally.

AI-Integrated Diagnostics Adoption: AI-assisted pathology solutions are now implemented in over 62% of large hospitals globally, reducing diagnostic errors by 28% and improving turnaround times by 22%. North America leads in AI integration, while Europe records the highest adoption rate among research institutions at 68%. Predictive algorithms in oncology and hematology have enabled earlier detection of complex diseases, with pilot programs reporting a 30% increase in treatment efficacy.

Cloud-Based Pathology Platforms: Cloud solutions now support 55% of digital pathology workflows worldwide, enabling real-time collaboration across laboratories. By 2026, cloud-based slide sharing is expected to reduce slide transport costs by 35% and reporting time by 25%. Asia-Pacific shows rapid adoption, with 42% of private labs implementing secure cloud infrastructures, while North America maintains the highest number of enterprise-scale deployments.

Multiplex and High-Throughput Imaging: Laboratories are increasingly utilizing multiplex immunohistochemistry and high-throughput slide scanners, enhancing analysis capacity by 40% per month. Europe dominates in the volume of high-throughput systems, while North America leads adoption, with over 70% of academic hospitals utilizing automated imaging. These systems improve diagnostic precision for oncology and pathology research, enabling simultaneous assessment of multiple biomarkers.

Telepathology and Remote Consultations: Telepathology networks have expanded globally, connecting over 1,500 hospitals for remote consultations. Recent pilot programs in 2024 reduced diagnostic turnaround by 20% and improved expert case review efficiency by 18%. North America dominates in volume of connected institutions, while Europe leads in user adoption at 65% of laboratories actively using telepathology platforms.

The Digital Pathology Market is segmented by product type, application, and end-user to provide targeted insights into adoption patterns and technological deployment. Product types include whole slide imaging (WSI), automated imaging systems, and image analysis software, each serving specialized laboratory requirements. Applications span oncology, clinical diagnostics, and research laboratories, with oncology representing a leading segment due to rising cancer detection demands. End-users comprise hospitals, pharmaceutical companies, and academic research centers, with large hospitals dominating adoption due to infrastructure capacity and regulatory compliance requirements. Regional variations highlight Europe and North America as leaders in integration and AI-enabled workflows, while Asia-Pacific demonstrates rapid adoption in private laboratories and emerging healthcare systems. Emerging trends in cloud platforms, telepathology, and AI-assisted diagnostics are shaping procurement, operational strategies, and investment priorities across these segments, making segmentation analysis critical for decision-makers seeking targeted market insights.

Whole Slide Imaging (WSI) currently leads the Digital Pathology market, accounting for 48% of adoption, due to its high-resolution imaging capabilities and compatibility with AI analysis. Automated imaging systems follow at 28%, with adoption driven by laboratories seeking improved throughput and reduced manual errors. Image analysis software, representing 24% of adoption, is the fastest-growing type, propelled by advances in deep learning algorithms capable of identifying complex patterns across thousands of slides. Other niche types, including multiplex imaging solutions and cloud-integrated visualization tools, contribute a combined 15% of adoption, serving specialized research and diagnostic applications.

Oncology remains the leading application segment in Digital Pathology, representing 50% of adoption, driven by rising cancer incidence and the need for precise diagnostics. Clinical diagnostics follow at 30%, particularly in hematology and infectious disease analysis, with automated slide review improving efficiency by 20–25%. Research laboratories account for 20% of the market, with growth driven by integration of AI-based image analysis and high-throughput screening systems. The fastest-growing application is pharmaceutical R&D, where AI-assisted pathology has accelerated drug testing and biomarker discovery, improving trial workflow efficiency by 28%.

Hospitals lead adoption in the Digital Pathology Market, comprising 55% of total end-users, with large academic medical centers integrating AI-assisted workflows to enhance diagnostic accuracy and case throughput. Pharmaceutical companies, accounting for 25% of adoption, are the fastest-growing end-user segment due to increasing demand for preclinical and clinical trial efficiency. Academic research institutions and specialized laboratories make up the remaining 20%, focusing on high-resolution imaging and experimental diagnostics. Industry adoption rates show North America’s hospitals implementing AI in 70% of cases, while Europe leads in research adoption at 65%.

North America accounted for the largest market share at 42% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15% between 2025 and 2032.

North America leads with over 1,200 hospitals and 350 research laboratories adopting digital pathology solutions, while over 68% of oncology and hematology labs are fully digitized. Asia-Pacific shows rapid adoption in China, India, and Japan, with more than 400 private laboratories integrating AI-assisted slide analysis platforms. Europe accounts for 28% of total adoption, with Germany, UK, and France leading technology deployment. South America, with Brazil and Argentina, contributes 12% of regional market volume, while Middle East & Africa, including UAE and South Africa, account for 8%, driven by infrastructure modernization and telepathology initiatives. Across regions, cloud-based platforms are now deployed in 55% of digital pathology workflows, AI-assisted imaging in 62% of large hospitals, and telepathology networks connect over 1,500 institutions globally.

How are technological advancements transforming diagnostic efficiency?

North America holds 42% of the global Digital Pathology Market, driven by hospitals, academic medical centers, and pharmaceutical companies integrating AI-assisted diagnostics. Regulatory support through FDA approvals and HIPAA-compliant cloud platforms has facilitated rapid adoption. Advanced whole slide imaging, AI-driven image analysis, and telepathology platforms are transforming workflow efficiency, reducing case review time by up to 28%. Local players such as Philips Digital Pathology have implemented AI-integrated WSI systems across 200+ laboratories, enhancing oncology and hematology diagnostics. Consumer behavior shows higher enterprise adoption in large healthcare institutions, with over 70% of labs shifting to fully digital workflows. Investment in infrastructure and digital transformation continues to expand regional capabilities, positioning North America as a benchmark for operational efficiency and innovation.

Why is regulatory compliance driving advanced pathology adoption?

Europe accounts for 28% of the global Digital Pathology Market, with Germany, UK, and France leading adoption. Regulatory pressures from bodies like EMA and GDPR have increased demand for explainable, compliant digital pathology solutions. Emerging technologies such as AI-based predictive diagnostics and cloud-based collaboration tools are being widely implemented. Local companies, including Leica Biosystems, have deployed automated imaging and AI-assisted analysis platforms across 120+ hospitals and research institutions, improving diagnostic throughput by 25%. European laboratories demonstrate adoption trends influenced by compliance mandates, research integration, and sustainability initiatives, with over 65% of hospitals implementing digital slide workflows. Regional consumer behavior favors explainable AI solutions and standardized imaging protocols.

How is rapid infrastructure expansion supporting diagnostic modernization?

Asia-Pacific holds the fastest-growing segment in Digital Pathology, accounting for 18% of the market volume in 2024. Top consuming countries include China, India, and Japan, with over 400 laboratories adopting AI-assisted pathology platforms. Infrastructure expansion and increasing private sector investment are driving digital transformation. Technological innovation hubs in Singapore and South Korea support the deployment of high-throughput scanners and cloud-based telepathology. Local players like Samsung Medison have integrated AI-assisted slide analysis into hospitals, improving case review efficiency by 22%. Consumer behavior shows growth driven by private hospital adoption, mobile-based diagnostic applications, and telepathology consultations.

What are the factors driving adoption in emerging Latin American markets?

South America accounts for 12% of the Digital Pathology Market, led by Brazil and Argentina. Government incentives supporting digital health and infrastructure modernization have encouraged hospital adoption. Energy-efficient laboratories and telepathology networks are being implemented in over 80 institutions across the region. Local players like Dasa Labs in Brazil have deployed AI-assisted imaging systems, reducing manual review time by 18%. Consumer behavior reflects growing interest in advanced diagnostics for oncology and hematology, while regional language localization and teleconsultation adoption remain key drivers.

How are modernization and regulatory initiatives shaping digital adoption?

Middle East & Africa accounts for 8% of the Digital Pathology Market, with UAE and South Africa as major contributors. Rising demand in healthcare modernization and digital diagnostics has accelerated adoption. Technological modernization trends include AI-assisted imaging, cloud storage, and telepathology networks connecting over 50 hospitals. Government incentives and trade partnerships support laboratory upgrades. Local players such as Mediclinic Group have implemented high-resolution WSI and AI platforms, improving diagnostic efficiency by 20%. Regional consumer behavior is influenced by private healthcare expansion, teleconsultation adoption, and compliance with local health regulations.

United States – 42% market share; strong end-user demand and high production capacity for AI-integrated digital pathology platforms.

Germany – 15% market share; regulatory compliance and advanced laboratory infrastructure drive adoption of automated imaging and AI-assisted diagnostics.

The Digital Pathology market is moderately consolidated, with over 120 active competitors globally, including hospitals, research institutions, and specialized technology providers. The top five players—Philips Digital Pathology, Leica Biosystems, Roche Diagnostics, Visiopharm, and 3DHISTECH—collectively account for approximately 60% of market adoption, reflecting a competitive yet concentrated environment. Strategic initiatives are driving differentiation, including AI-integrated imaging platform launches, cloud-based telepathology collaborations, and strategic partnerships with academic hospitals. For instance, over 200 laboratories in North America have adopted Philips’ AI-assisted WSI systems, improving diagnostic accuracy by up to 28%. Innovation trends such as multiplex immunohistochemistry, predictive oncology analytics, and real-time cloud-based collaboration are shaping competitive dynamics. Companies are also investing in regional expansion, particularly in Asia-Pacific and Europe, where adoption in private laboratories and academic research centers is growing at a significant pace. Mergers and strategic alliances are increasingly common, with at least 15 new partnerships formed globally in 2024 to integrate AI, cloud computing, and automated imaging solutions, highlighting a highly dynamic competitive landscape for decision-makers.

3DHISTECH

Hamamatsu Photonics

Sakura Finetek

OptraSCAN

Sectra AB

Inspirata

The Digital Pathology Market is increasingly driven by the integration of advanced imaging technologies, AI-assisted analysis, and cloud-based data management. Whole slide imaging (WSI) systems now support resolutions up to 40x magnification, enabling pathologists to review over 2,500 slides per month per scanner. AI-powered algorithms are being deployed for automated tumor detection, cell counting, and biomarker identification, improving diagnostic precision by up to 28% compared to manual review. Cloud platforms facilitate secure storage and real-time sharing of over 60 terabytes of pathology data per large hospital annually, supporting remote consultations and collaborative research. Emerging technologies such as multiplex immunohistochemistry and high-throughput slide scanners allow simultaneous assessment of multiple biomarkers, enhancing laboratory throughput by 40% in oncology and hematology applications. Integration with electronic health records (EHRs) and laboratory information systems is enabling predictive analytics, aiding early disease detection and treatment planning. Additionally, augmented reality (AR) and virtual microscopy are being piloted for educational and training applications, with over 35 academic centers globally implementing these platforms in 2024. Telepathology networks connecting over 1,500 hospitals worldwide are expanding access to specialist consultations, while automated staining and slide preparation systems reduce manual errors and labor requirements by approximately 25%. Overall, these technological advancements are shaping operational efficiency, workflow optimization, and diagnostic accuracy across the Digital Pathology Market.

In 2023, Philips Digital Pathology launched its AI-assisted WSI platform across 200 North American laboratories, improving diagnostic accuracy by 28% and reducing manual slide review time by 25%.

Leica Biosystems introduced an automated high-throughput imaging scanner in 2023, enabling simultaneous analysis of 1,200 slides per week in clinical research labs, improving productivity in oncology diagnostics.

In 2024, Roche Diagnostics partnered with 50 European hospitals to implement predictive AI algorithms for hematology and oncology case reviews, cutting turnaround time for complex cases by 22%.

Visiopharm deployed cloud-based telepathology platforms in 2024 across 75 global research institutions, allowing secure sharing of 45 terabytes of digital slides annually, enhancing collaborative clinical trials and remote diagnostics.

The Digital Pathology Market Report provides a comprehensive analysis of the global landscape, covering product types, applications, end-users, and regional adoption trends. It examines key technologies, including whole slide imaging, AI-assisted image analysis, multiplex immunohistochemistry, automated staining, high-throughput scanners, and cloud-based platforms. Applications span oncology, hematology, infectious diseases, and pharmaceutical research, highlighting adoption in hospitals, academic medical centers, and research laboratories. The report also details emerging use cases in telepathology, virtual microscopy, and predictive diagnostics. Geographic coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with insights on regional infrastructure, adoption patterns, regulatory frameworks, and investment trends. Additionally, the report highlights operational efficiency improvements, diagnostic workflow optimization, and integration with electronic health records, providing a forward-looking perspective on technology-driven innovation. Niche segments such as mobile-based pathology apps, AI-assisted biomarker discovery, and decentralized diagnostic networks are also explored. The report is structured to support decision-makers, investors, and industry professionals in identifying strategic opportunities, understanding competitive dynamics, and evaluating technology adoption across clinical, research, and commercial environments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1260.09 Million |

|

Market Revenue in 2032 |

USD 3774.93 Million |

|

CAGR (2025 - 2032) |

14.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Philips Digital Pathology, Leica Biosystems, Roche Diagnostics, Visiopharm, 3DHISTECH, Hamamatsu Photonics, Sakura Finetek, OptraSCAN, Sectra AB, Inspirata |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |