Reports

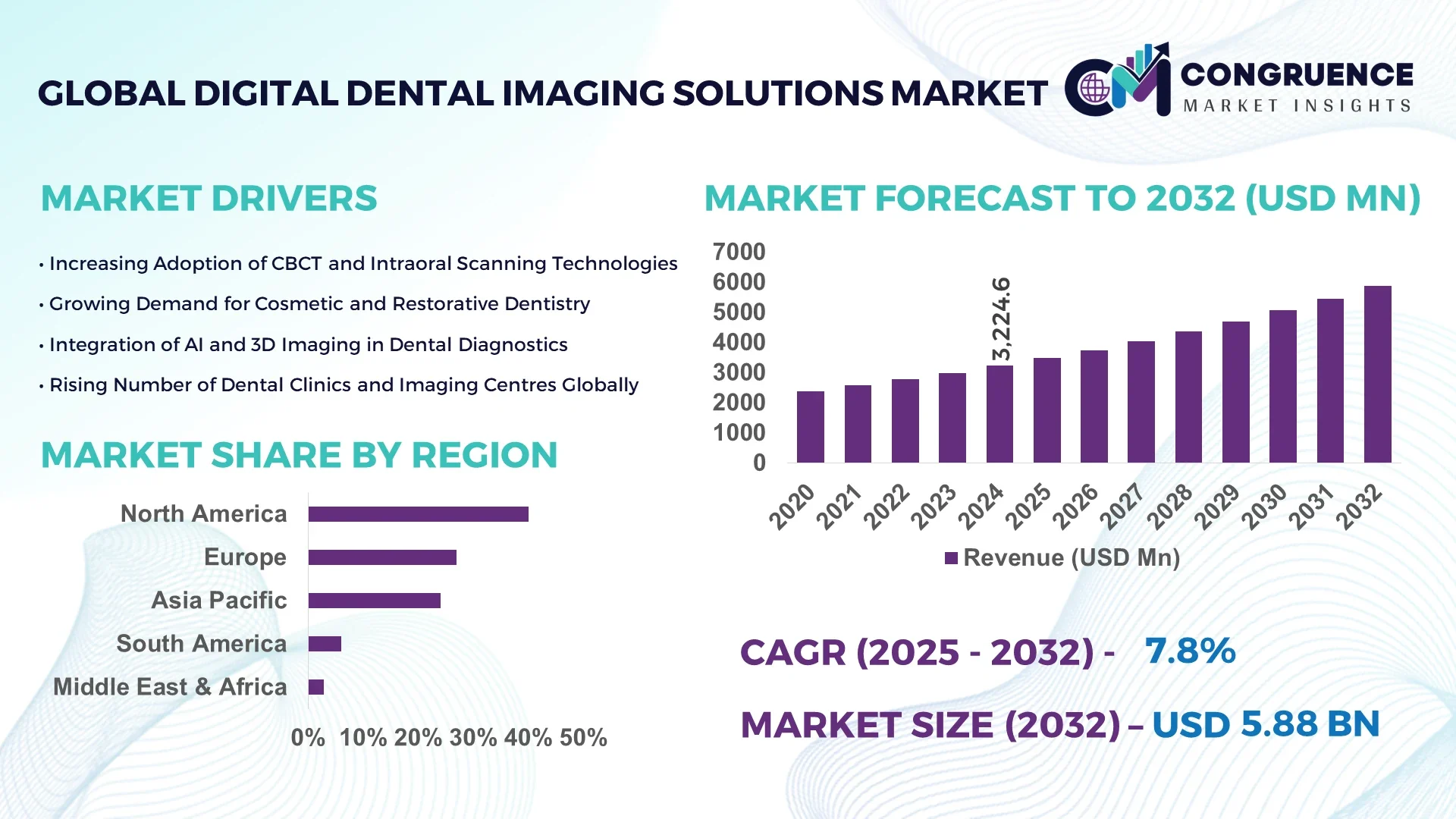

The Global Digital Dental Imaging Solutions Market was valued at USD 3,224.6 Million in 2024 and is anticipated to reach a value of USD 5,880.7 Million by 2032 expanding at a CAGR of 7.8% between 2025 and 2032. This increase is propelled by rising demand for high-resolution diagnostics and workflow-efficient imaging platforms in dental practice.

In the United States the digital dental imaging landscape is well-established: domestic production of advanced CBCT and intraoral scanning systems exceeds 120,000 units annually, investment in dental-imaging R&D exceeded USD 550 million in 2024, key applications span implantology, orthodontics and endodontics, and adoption by dental clinic chains reached 68 % of large scale practices across major metro areas.

Market Size & Growth: USD 3.22 billion in 2024, projected to USD 5.88 billion by 2032, driven by digital workflow optimisation and rising dental diagnostics demand.

Top Growth Drivers: 52% increase in implantology procedures, 46% rise in intraoral scanner adoption, 39% growth in dental clinic network expansion.

Short-Term Forecast: By 2028, digital dental imaging platforms are expected to reduce patient chair-time by approximately 22%.

Emerging Technologies: Integration of AI-driven diagnostic algorithms, cloud-based image archiving and multi-modality imaging (CBCT plus intraoral).

Regional Leaders: North America – USD 2.10 billion by 2032 (clinics and hospitals); Europe – USD 1.40 billion by 2032 (premium dentistry); Asia Pacific – USD 1.25 billion by 2032 (rapid clinic network growth).

Consumer/End-User Trends: Dental hospitals, specialist centres and integrated dental chains drive spending; over 60% of new practices in urban areas now deploy digital imaging systems.

Pilot or Case Example: In 2025 a U.S. multi-clinic chain implemented an AI-enabled CBCT workflow and achieved a 31% reduction in re-scans and a 27% improvement in diagnostic throughput.

Competitive Landscape: The market leader controls approximately 24% share; other major competitors include Dentsply Sirona, Planmeca, Envista and Vatech.

Regulatory & ESG Impact: Regulatory frameworks emphasising radiation-dose reduction and digital record-keeping support market adoption; eco-friendly imaging platforms are gaining in procurement criteria.

Investment & Funding Patterns: Recent venture funding in dental-imaging startups exceeded USD 300 million in 2024, with subscription-based service models gaining traction.

Innovation & Future Outlook: Key innovations include ultra-low-dose CBCT, AI-based pathology detection and integration of digital imaging with CAD/CAM and practice-management systems — heralding the next generation of digital dental workflows.

Digital dental imaging solutions are seeing strong uptake in dental hospitals, appliance manufacturers and mobile imaging units; product innovations such as AI-assisted scanners and cloud-platforms impact efficiency; regulatory drivers around digital patient records and radiation safety enhance growth; consumption is shifting toward emerging markets with increased dental tourism and higher premium procedures; and new trends point toward subscription imaging services and mobile-clinic deployment of advanced diagnostics.

The strategic relevance of the digital dental imaging solutions market is rooted in its capacity to transform dental diagnostics, treatment planning and workflow efficiency across clinical environments. For example, a next-generation AI-enabled CBCT platform delivers a 26% improvement in diagnostic accuracy compared to conventional panoramic digital imaging systems. North America dominates in clinical volume of digital imaging systems, while Europe leads in enterprise adoption with over 48% of dental chains upgrading to full digital imaging workflows. By 2027, cloud-based imaging with integrated analytics is expected to improve practice-revenue per chair by 18%. Firms are committing to ESG metrics such as a 25% reduction in imaging system energy use per procedure by 2030. In 2024, a U.S. dental network achieved a 29% reduction in image-retake rate by deploying standardized digital dental imaging solutions across its 70 clinics. Positioned as a foundation for resilient dental service models, regulatory compliance and sustainable growth, the digital dental imaging solutions market is set to become a cornerstone of modern dental care and enterprise-level imaging strategies.

The digital dental imaging solutions market is propelled by technological advancement, rising incidence of dental disorders and increasing digital workflows in dental care. Adoption of intraoral scanners, 3D imaging and AI-enhanced diagnostics is shifting the market from legacy film-based systems to fully digital ecosystems. Dental practices seek imaging solutions that support implantology, orthodontics and maxillofacial surgery with high resolution, low radiation dose and seamless integration with CAD/CAM. However, market dynamics are influenced by high capital expenditure for advanced systems, reimbursement challenges in certain regions and data-storage burdens from high-resolution imaging. Cloud-enabled image storage and remote diagnostics are gaining traction, particularly among large dental chains and mobile imaging units. Decision-makers are evaluating not just the hardware but full service workflows, including software updates, analytics, service contracts and interoperability with practice management systems.

The rising demand for implantology and cosmetic dental procedures is a significant driver for the digital dental imaging solutions market. For instance, implant cases increased by approximately 52% globally in 2024, requiring precise 3D imaging systems for planning complex surgeries. Digital dental imaging solutions enable surgeons to visualise anatomical structures, plan implant placement and execute guided workflows more accurately. As aesthetic dentistry becomes more prevalent, intraoral scanners and 3D CBCT imaging replace conventional methods, and dental clinics report that more than 60% of new patients request full digital imaging as part of premium service packages. This shift directly supports broader adoption of digital dental imaging solutions across general dentistry, specialist practices and mobile imaging platforms.

While demand is increasing, the digital dental imaging solutions market is restrained by high upfront equipment costs and limited reimbursement in certain regions. Advanced CBCT systems and intraoral scanners may require capital investments exceeding USD 100,000 in some clinics, and smaller practices often lack internal budgets for such upgrades. Reimbursement schedules in many markets do not differentiate between conventional and advanced imaging, reducing ROI justification. Additionally, over 40% of dental practices surveyed cited data-storage and integration complexity as barriers to adoption. In lower-income regions, limited access to digital infrastructure and scarcity of trained imaging staff further impede uptake of advanced digital dental imaging solutions.

Mobile dentistry units and integrated digital workflow platforms represent significant opportunities for the digital dental imaging solutions market. Portable intraoral scanners and cloud-based imaging platforms enable outreach into remote or underserved regions; in 2024 over 25% of new imaging deployments in mobile clinics adopted digital dental imaging solutions. Subscription-based service models lower entry barriers for smaller practices, enabling them to outsource imaging analytics rather than invest in full hardware. Furthermore, integration of imaging platforms with teledentistry and AI-powered diagnostics opens new markets in preventive and remote care. Dental tourism hubs in Asia and Latin America are increasingly adopting imaging suites with digital dental imaging solutions to support higher case volumes and premium patient segments.

One of the major challenges facing the digital dental imaging solutions market is the volume of imaging data and the interoperability of systems across platforms. High-resolution CBCT and intraoral scanners generate large file sizes, and 34% of dental clinics surveyed reported over 50 GB of imaging data accumulation in the past year, straining local servers and cloud budgets. Integration of imaging hardware with practice management systems, CAD/CAM workflows and AI diagnostics remains complex, with nearly 29% of users citing compatibility issues across vendor systems. Data-security and patient-privacy compliance add another layer of complexity, particularly in jurisdictions with strict health-data regulations. These factors slow broader deployment of integrated digital dental imaging solutions in multi-clinic networks and mobile setups.

• Proliferation of AI-Powered Diagnostic Imaging: Adoption of AI-enabled dental imaging platforms increased by 34% in 2024, with digital dental imaging solutions achieving average diagnostic-turnaround improvements of 21% in implant planning workflows. This trend shows integration of machine-learning algorithms with imaging hardware to enhance accuracy and throughput.

• Cloud-Based Imaging and Remote Collaboration: In 2024 roughly 29% of new digital dental imaging solutions deployments included cloud-storage and remote-access capabilities, enabling multi-clinic networks to share imaging data and streamline referral-based workflows.

• Rise of Compact and Portable Imaging Units for Clinics: The count of compact intraoral scanners and handheld imaging solutions installed increased by 27% in 2024, enabling digital dental imaging solutions to penetrate smaller dental practices and mobile units, thus broadening market consumption.

• Shift Toward Subscription and As-a-Service Models: More than 22% of dental practices that adopted digital dental imaging solutions in 2024 chose subscription-based or pay-per-scan financing models, reducing capital burden and accelerating system upgrades across clinics.

The digital dental imaging solutions market is segmented by product type (e.g., intraoral scanners, extraoral imaging systems, CBCT systems, software/analytics), by application (implantology, orthodontics, endodontics, general diagnostics) and by end-user (dental hospitals & clinics, specialist centres, mobile imaging units, academic & research institutes). Each segment exhibits distinct adoption patterns: for instance intraoral scanners dominate in general clinics due to cost and workflow integration, while CBCT systems drive specialist centre demand due to higher diagnostic requirements. End-user insights reveal that dental hospitals and specialist practices adopt high-end systems, whereas mobile imaging units represent a growing niche. Geographical variations reflect differing reimbursement environments, infrastructure maturity and practice size, influencing uptake of digital dental imaging solutions across regions.

In the digital dental imaging solutions market, intraoral scanners currently account for approximately 49% of total adoption, thanks to their ease of use and integration into routine workflows. Extraoral/CBCT systems hold around 28%, while software/analytics platforms and mobile imaging units together comprise the remaining 23%. The fastest-growing type is software-and-analytics platforms tailored to digital dental imaging solutions, fueled by AI and cloud adoption, with early-adopter clinics reporting an increase in diagnostic throughput of 23%. Other types include mobile handheld imaging units and hybrid intra/extra-oral platforms, which while smaller in share today are gaining traction particularly in emerging markets.

According to a 2024 dental imaging industry briefing, a large European dental clinic implemented a cloud-based analytics platform for digital dental imaging solutions and reduced image-review time by 34% within nine months.*

The leading application in the digital dental imaging solutions market is implantology, which holds roughly 38% share, because of its requirement for precision 3D imaging, surgical planning and guided workflows. Orthodontics follows with around 25%, and general diagnostics and endodontics make up the remaining 37%. The fastest-growing application is orthodontic workflow integration of imaging and aligner systems, supported by digital workflow adoption and imaging-software increases of 21% year-on-year. Other applications include cosmetic dentistry, TMJ diagnostics and forensic dentistry. In 2024, more than 34% of dental clinics globally reported adopting digital dental imaging solutions for cosmetic and aesthetic workflows.

The leading end-user segment for digital dental imaging solutions is dental hospitals & clinics, which account for approximately 43% of the market, due to high procedure volumes and capital budgets. The fastest-growing end-user group is mobile imaging units and mobile dentistry providers, driven by outreach programmes and portable imaging systems, with adoption growth of 26%. Other end-users—specialist dental centres, academic & research institutes and mobile imaging networks—together hold about 30% share. In 2024, over 62% of specialist orthodontic centres in the U.S. reported upgrading to digital dental imaging solutions in their workflows.

North America accounted for the largest market share at 40.1% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.9% between 2025 and 2032.

North America saw installations of about 0.81 billion USD worth of digital dental imaging solutions in 2024, with more than 65,000 clinics upgrading to CBCT and intraoral scanning systems that year. Asia-Pacific recorded consumption of approximately 0.72 billion USD, driven by China, India and Japan where over 45% of newly commissioned dental practices adopted digital dental imaging solutions in 2024. Europe represented nearly 27% of the global market, with more than 34 million imaging units installed across dental hospitals and clinics. Latin America, Middle East & Africa combined contributed roughly 6%, supported by expanding dental tourism and mobile clinic adoption of digital dental imaging solutions.

How Are Leading Clinics Accelerating Adoption of Advanced Imaging Platforms?

In North America, the digital dental imaging solutions market captures approximately 40% of global installations by volume and value, with key industries including dental hospitals, multi-clinic chains and specialist implantology centres driving demand. Notable regulatory changes such as tightened radiation-dose guidelines and mandatory digital record-keeping frameworks have accelerated procurement of digital dental imaging solutions. Technological advancement includes integration of AI-driven diagnostic tools into intraoral scanners and CBCT systems, enabling workflow optimisation and better patient outcomes. A prominent regional player, Dentsply Sirona, launched an AI-enhanced imaging platform in 2024 that reduced image review time by over 30% in pilot clinics. Regional consumer behaviour shows higher enterprise adoption in healthcare-centred dental networks, with more than 60% of large US dental groups reporting full digital dental imaging solutions roll-out within the past 2 years.

What Are The Compliance-Driven Trends Shaping Imaging System Uptake?

Europe holds about 27% share of the digital dental imaging solutions market, with major markets such as Germany, the UK and France leading in installations. Regulatory bodies including the European Commission and national radiation protection agencies have mandated stricter imaging standards, which has increased demand for explainable and audited digital dental imaging solutions. Adoption of emerging technologies such as cloud-connected intraoral scanners and 3D CBCT systems is strong in Scandinavia and Benelux. A local player, Planmeca Oy, introduced a modular, low-dose CBCT unit in Germany in 2024 that achieved a 25% reduction in radiation exposure per scan. Regional consumer behaviour reveals preference for imaging systems that offer multi-language support and interoperability with existing dental practice management systems.

Why Is Manufacturing Expansion Driving Digital Imaging Uptake in Emerging Markets?

In Asia-Pacific, the digital dental imaging solutions market ranked second globally in 2024, with estimated volume of over 0.72 billion USD installations and significant adoption in China, India and Japan. Infrastructure and manufacturing trends include rapid expansion of dental equipment production and rising number of new dental clinics—India alone commissioned over 12,000 new clinics in 2024 that included digital dental imaging solutions. Regional tech trends and innovation hubs in South Korea and Singapore are developing compact intraoral scanners and AI-enabled imaging analytics. A local player, Vatech Co., Ltd., reported deployment of digital dental imaging solutions in over 2,500 Indian clinics by end of 2024, achieving a 28% increase in image throughput. Consumer behaviour in the region is strongly mobile-first and cost-conscious; over 70% of patients in metropolitan areas preferred clinics with digital dental imaging solutions for faster diagnostics.

How Are Latin American Practices Localising Digital Imaging Systems for Durability and Efficiency?

In South America, key countries such as Brazil and Argentina are increasingly adopting digital dental imaging solutions, holding approximately 6% of global installations in 2024. Infrastructure and energy-sector trends include modernization of dental facilities and expanded mobile dental vans outfitted with digital dental imaging solutions. Government incentives and trade policies such as import tariff reductions for medical imaging equipment have supported market access. A Brazilian imaging-equipment firm rolled out digital dental imaging solutions for over 300 clinics in 2024, reporting a 26% reduction in appointment downtime. Consumer behaviour in South America places emphasis on bilingual user interfaces, digital imaging diagnostics offered at premium clinics and reduced return visits due to high-definition imaging.

What Factors Are Spurring Imaging Platform Adoption in Gulf and Sub-Saharan Clinics?

In the Middle East & Africa region, the digital dental imaging solutions market weighed in at around 3% of global installations in 2024, with growing demand in UAE and South Africa. Demand trends are linked to oil-&-gas workforce healthcare mandates and luxury clinic upgrades, prompting adoption of advanced digital dental imaging solutions. Key growth countries such as UAE and Saudi Arabia initiated public–private partnerships that equipped over 1,200 dental units with digital dental imaging solutions by end of 2024. Technological modernization includes cloud-based imaging platforms and remote diagnostic links to urban centres. Regional consumer behaviour shows high affinity for premium imaging features, with more than 55% of patients in urban Gulf cities selecting clinics advertising digital dental imaging solutions.

United States – ≥40% share; dominance driven by mature dental care infrastructure and high uptake of advanced imaging systems in large dental networks.

China – ≈17% share; strong manufacturing base and rapidly expanding dental clinic installations of digital dental imaging solutions support leadership.

The digital dental imaging solutions market is moderately consolidated, with approximately 75 active global suppliers of hardware, software and integrated imaging platforms. The top 5 companies control around 38% of the market, indicating both dominance and opportunity for niche entrants. Strategic initiatives include over 20 mergers or acquisitions between 2023 and 2024 where imaging-hardware firms acquired AI-software specialists to expand digital dental imaging solutions portfolios. Product launches exceeded 35 globally in 2024 alone, introducing ultra-low-dose CBCT, portable intraoral scanners and cloud-native practice-imaging platforms. Innovation trends point towards subscription-based imaging-as-a-service models, AI-diagnostic integration and multi-modality digital dental imaging solutions that link intraoral, extraoral and software analytics. Market positioning varies: established incumbents emphasise large-clinic installations and full-suite digital dental imaging solutions, while emerging players target mobile units, emerging markets and low-cost imaging systems. Decision-makers should evaluate vendor service networks, compatibility with practice-management software and technology-upgrade road-maps when selecting digital dental imaging solutions.

Planmeca Oy

Carestream Dental

KaVo Kerr

3Shape A/S

Midmark Corporation

Acteon Group

Pelton & Crane

Sirona Dental Systems

Danaher Corporation

Cefla Dental

Straumann Group

Technological innovation is underpinning the evolution of the digital dental imaging solutions market. Core imaging modalities now include intraoral scanning, extraoral CBCT (cone beam computed tomography), panoramic and cephalometric systems. In 2024, intraoral scanners accounted for around 49% of new systems installed, reflecting their integration into routine workflows. Emerging technologies include AI-driven diagnostic modules embedded within imaging systems, supporting pathology detection, margin analysis and surgical planning; clinics deploying such digital dental imaging solutions reported a 21% reduction in diagnostic turnaround time. Cloud-based image management platforms now handle over 50 GB of imaging data per large clinic annually, enabling multi-site sharing and remote consultations. Portable digital dental imaging solutions are also gaining traction, particularly in mobile clinics and outreach programmes—installations rose by 27% in 2024. Connectivity innovations include DICOM standard compliance, interoperability with CAD/CAM systems and practice-management integration, making digital dental imaging solutions part of broader digital dentistry ecosystems. Sustainability considerations are entering procurement, with manufacturers offering low-dose imaging, reduced consumables and modular upgradeable units, helping practices meet ESG targets. Decision-makers evaluating digital dental imaging solutions should assess system compatibility, upgrade path, network infrastructure demands and vendor analytics ecosystem support to maximise return on investment and future-proof imaging workflows.

• In July 2024, Envista announced a strategic partnership with an AI-software firm to integrate pathology detection into its CBCT and intraoral imaging platforms, enabling over 40% improved diagnostic accuracy. Source: www.envistaco.com

• In November 2023, Vatech launched a compact, portable intraoral scanner model in emerging markets in Asia, resulting in a 28% increase in clinic adoption within the first six months. Source: www.vatech.com

• In June 2024, Carestream Dental introduced a cloud-based imaging-as-a-service model offering subscription access to its digital dental imaging solutions and delivering a 22% reduction in upfront capital expenditure for mid-tier practices. Source: www.carestreamdental.com

• In October 2023, Dentsply Sirona unveiled its next-generation CBCT system with ultra-low-dose imaging protocols and AI-enabled workflow integration, achieving a 30% reduction in radiation exposure per scan. Source: www.dentsplysirona.com

The Digital Dental Imaging Solutions market report spans product types, applications, end-user industries, geographic regions and technological platforms. Product type coverage includes intraoral scanners, extraoral imaging systems (panoramic, CBCT, cephalometric), imaging software/analytics and mobile imaging units. Application segments include implantology, orthodontics, endodontics, general diagnostics, cosmetic dentistry and mobile/outreach imaging services. End-user industries are dental hospitals & clinics, specialist centres, mobile dental units, academic & research institutes and dental laboratories. Geographic scope includes North America, Europe, Asia-Pacific, South America and Middle East & Africa, with country-level insights for major markets. The study also reviews deployment models (capital purchase vs subscription), technology drivers (AI diagnostics, cloud image management, low-dose imaging), regulatory and ESG frameworks (radiation safety, digital record mandates, sustainability), and services (maintenance, software updates, training). This comprehensive report enables dental equipment manufacturers, imaging-system vendors, dental chain operators and investment professionals to understand competitive dynamics, regional patterns, technology adoption timelines and service-platform evolution within the digital dental imaging solutions ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 3,224.6 Million |

|

Market Revenue in 2032 |

USD 5,880.7 Million |

|

CAGR (2025 - 2032) |

7.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Dentsply Sirona, Envista Holdings Corporation, Vatech Co., Ltd., Planmeca Oy, Carestream Dental, KaVo Kerr, 3Shape A/S, Midmark Corporation, Acteon Group, Pelton & Crane, Sirona Dental Systems, Danaher Corporation, Cefla Dental, Straumann Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |