Reports

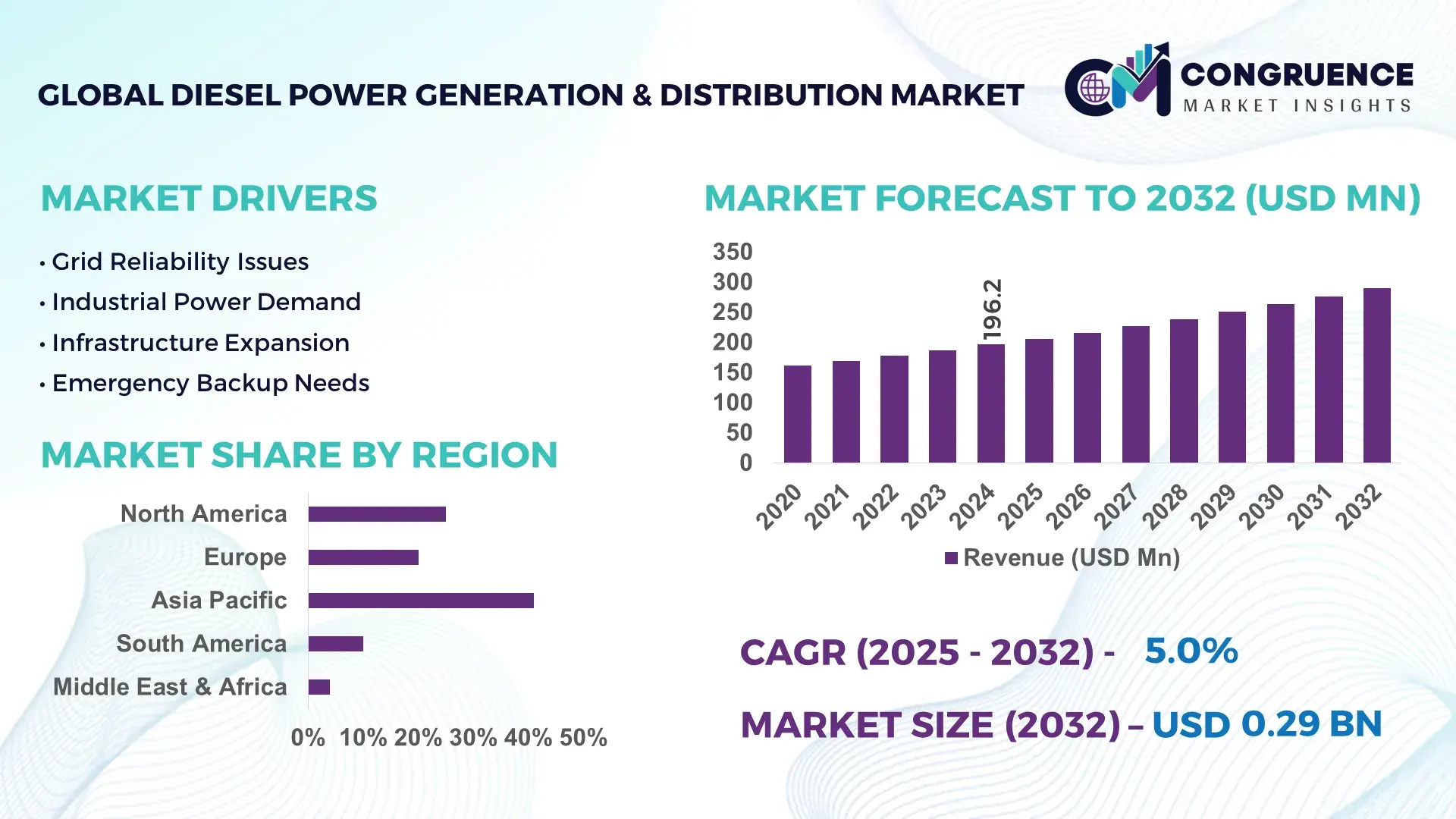

The Global Diesel Power Generation & Distribution Market was valued at USD 196.24 Million in 2024 and is anticipated to reach a value of USD 289.94 Million by 2032, expanding at a CAGR of 5.0% between 2025 and 2032. This growth is driven by increasing demand for reliable backup and off‑grid power solutions across industrial and commercial applications.

China’s diesel power generation and distribution sector demonstrates robust production capacity, with manufacturers deploying advanced Tier‑compliant engines across industrial, construction, and data center segments. China’s extensive investment in digital control systems has enabled over 70% of new industrial gensets to feature remote monitoring and predictive maintenance capabilities, enhancing operational uptime and efficiency. Large‑scale infrastructure projects and manufacturing facilities across the country drive continuous demand, supported by over 10.5 million operational units in the Asia‑Pacific region, with China as the focal point for adoption and technological integration in diesel power systems.

• Market Size & Growth: Current value estimated at USD 196.24 Million in 2024, projected to USD 289.94 Million by 2032 at a CAGR of 5.0%, reflecting sustained demand for resilient power systems.

• Top Growth Drivers: Rising industrial backup requirements (60% adoption), digital monitoring integration (70% adoption), hybrid diesel‑solar system uptake (37% increase).

• Short‑Term Forecast: By 2028, expected cost reduction of up to 12% through enhanced fuel efficiency technologies and performance gains via IoT‑enabled predictive maintenance.

• Emerging Technologies: Hybrid diesel‑battery systems, IoT remote diagnostics, digital twin‑enabled genset management.

• Regional Leaders: Asia Pacific ~USD 10.3B by 2030 with high infrastructure power demand; North America strong in data center and healthcare applications; Europe focusing on emission‑compliant models.

• Consumer/End‑User Trends: Industrial and commercial sectors increasingly adopt mid‑range gensets for continuity, while remote rural deployments integrate diesel systems with microgrids.

• Pilot or Case Example: In 2023, hybrid diesel‑solar gensets implementation in Southeast Asia showed a 27% increase in energy reliability for remote facilities.

• Competitive Landscape: Market leaders include Caterpillar, Cummins, Generac, Kohler, and MTU Onsite Energy.

• Regulatory & ESG Impact: Stricter emissions standards like Tier 4 and Euro Stage V are accelerating adoption of cleaner diesel technologies and hybrid systems.

• Investment & Funding Patterns: Global investments in diesel generator production and hybrid solutions exceeded USD 3.4B with additional funding for smart control R&D.

• Innovation & Future Outlook: Growing integration of predictive analytics, modular system design, and hybrid configurations are shaping forward‑looking deployments.

China’s diesel power market sees extensive adoption in the manufacturing, construction, and data center sectors, with advanced gensets featuring IoT-enabled remote monitoring and predictive maintenance. Recent technological upgrades have enhanced fuel efficiency by up to 15% and reduced operational downtime by approximately 20%. Regulatory compliance with Tier 4 emission standards and investments exceeding USD 1.2 billion in modern genset production and hybrid solutions reflect the country’s focus on operational efficiency and technological advancement. The integration of digital twin systems and smart control modules further enables real-time performance monitoring, positioning China as a leader in high-capacity diesel power generation and distribution infrastructure.

The Diesel Power Generation & Distribution Market remains strategically relevant as global industries and critical infrastructure sectors demand highly reliable and resilient power solutions where grid stability is uncertain. Modern diesel gensets with digital control systems deliver up to 15% improvement in fuel efficiency compared to older analogue models, reducing operational costs while supporting compliance with tightening environmental standards. Asia Pacific dominates in volume, driven by rapid urbanization and infrastructure expansion, while North America leads in adoption with over 29% of enterprises deploying smart monitoring and IoT‑enabled diesel systems to enhance reliability and uptime. Digital transformation is reshaping market pathways; by 2027, advanced AI‑enabled predictive maintenance is expected to reduce unplanned downtime by more than 30%, improving key performance indicators such as availability and lifecycle costs for end users. ESG and compliance pressures are increasing investments in emissions reduction technologies, with firms committing to measurable environmental improvements such as SCR and DPF systems that cut NOx emissions significantly, aligning with global air quality regulations.

In 2025, several industrial parks implemented predictive analytics and cloud‑based monitoring across genset fleets, achieving up to 12% reduction in fuel consumption and extending equipment life by virtual simulation initiatives, showcasing measurable gains through tech adoption. The Diesel Power Generation & Distribution Market’s future pathways combine digitization, hybridization with renewable sources, and stringent emissions management practices, positioning it as a pillar of operational resilience, regulatory compliance, and sustainable growth for energy‑dependent sectors worldwide.

The adoption of digital and smart technologies is reshaping the Diesel Power Generation & Distribution Market by enhancing efficiency, uptime, and operational predictability. Advanced digital control systems and IoT‑enabled sensors allow real‑time performance monitoring, enabling predictive maintenance that reduces unplanned failures and extends equipment life. For example, digital twin systems have shown the ability to reduce downtime by up to 30% compared to traditional maintenance regimes, improving operational continuity for critical infrastructure operations. Integration of cloud analytics allows centralized management of distributed diesel genset fleets, optimizing fuel consumption and reducing operational expenses, particularly in large industrial parks and data centers. Remote diagnostics and automated alerts help service teams address emerging issues before they result in costly outages, increasing overall reliability. This driver is further supported by regulatory incentives for digital upgrades and emissions reduction, which have propelled investments into smart diesel genset technologies across segments such as telecom, healthcare, and construction, where continuity of power supply is indispensable.

Stringent emissions regulations represent a significant restraint on the Diesel Power Generation & Distribution market by increasing the complexity and cost of compliant genset systems. Governments across major economies are tightening emissions standards, requiring advanced after‑treatment systems such as selective catalytic reduction (SCR) and diesel particulate filters (DPF), which can add significant upfront cost and technical complexity compared to legacy systems. Compliance with lower emission thresholds often necessitates redesigns in engine architecture, fuel systems, and exhaust treatments, delaying deployment and increasing manufacturing costs. Additionally, retrofit requirements for existing fleets to meet new standards create logistical and financial burdens for operators, particularly in regions where older gensets remain widely deployed. These factors can slow sales cycles and adoption rates, especially in price‑sensitive markets or projects with constrained capital budgets. However, the added environmental benefits, though substantial, have made compliance a cost‑intensive challenge for some stakeholders.

The integration of hybrid and renewable energy sources presents significant opportunities for the Diesel Power Generation & Distribution market by addressing both sustainability and reliability needs. Hybrid systems that combine diesel gensets with solar, wind, or battery storage can reduce fuel consumption and emissions, making them appealing in off‑grid and remote applications where renewables help offset operational costs. Depending on the configuration and site conditions, hybrid systems can lower operating expenses by 50–85% and cut carbon emissions by up to 80% compared to diesel‑only setups. This creates new revenue streams for manufacturers and service providers who can offer integrated energy solutions rather than standalone gensets. Additionally, energy transition policies and incentives for cleaner energy investments are encouraging enterprises to adopt hybrid solutions to meet both operational and environmental goals. Such opportunities span rural electrification, telecom base stations, and microgrids for industrial clusters, enabling diesel gensets to remain a core component of resilient, low‑emission power architectures.

Supply chain constraints and component shortages present a significant challenge to the Diesel Power Generation & Distribution market by delaying production and delivery timelines. Diesel gensets increasingly rely on sophisticated electronic components such as microcontrollers, sensors, and communication modules to support digital monitoring and control functionalities. A shortage in semiconductors and specialized control system parts has extended lead times for these components by several weeks, disrupting manufacturing schedules and slowing down deployment for end users. In addition, logistics bottlenecks affecting the supply of critical mechanical parts and materials can further delay project timelines, increasing costs for both manufacturers and customers. These challenges are particularly acute for large‑capacity gensets used in industrial and infrastructure projects, where timely delivery is crucial to meet commissioning deadlines and ensure operational continuity. Mitigating these constraints requires strategic inventory planning, diversified supplier networks, and investments in localized production capabilities to reduce dependency on global supply chains.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction is reshaping Diesel Power Generation & Distribution demand. Approximately 55% of new industrial and commercial projects reported significant cost savings and 20–25% reduction in construction timelines through off-site prefabrication of structural and electrical components. Europe and North America are leading in adoption, with over 60% of large-scale projects integrating prefabricated diesel power modules to enhance installation speed and operational reliability. High-precision automated machinery for cutting, bending, and assembly is increasingly deployed, driving demand for compact, easily transportable diesel gensets compatible with modular frameworks.

• Integration of IoT and Predictive Analytics: Over 68% of newly deployed diesel gensets now incorporate IoT-enabled monitoring and predictive analytics for real-time operational insights. These systems have demonstrated a 30% reduction in unplanned downtime and a 15% improvement in fuel efficiency by identifying maintenance needs before failures occur. Remote diagnostics and automated alerts have accelerated adoption in data centers, industrial plants, and healthcare facilities, enabling centralized fleet management across multiple sites. North America leads in high adoption rates, while Asia Pacific shows rapid growth in mid-scale commercial applications.

• Expansion of Hybrid Diesel-Renewable Solutions: Hybrid diesel-solar and diesel-battery systems are being adopted in approximately 42% of off-grid and remote industrial deployments. These systems reduce fuel consumption by up to 50% and lower carbon emissions by nearly 80%, particularly in mining, telecom, and rural infrastructure projects. Countries in Asia Pacific and Africa are increasingly investing in hybrid configurations to optimize operational costs and meet environmental compliance standards, reflecting a strategic shift toward cleaner energy integration alongside diesel power.

• Demand for High-Capacity, Rapid-Deployment Gensets: Large infrastructure projects and emergency power requirements are driving demand for high-capacity diesel gensets capable of rapid deployment. Nearly 35% of recent industrial projects reported faster commissioning using transportable, containerized gensets with advanced control panels. Europe emphasizes precision-engineered, high-capacity units for industrial and commercial zones, while Asia Pacific focuses on scalable systems for urban development and critical infrastructure continuity. The trend is further supported by automation in installation, reducing labor requirements by 20% and deployment timelines by 18%.

The Diesel Power Generation & Distribution market is segmented to address diverse operational requirements and industry applications. By type, the market ranges from compact units for residential and light commercial use to heavy-duty generators for continuous industrial power. Mid-range gensets (60–300 kW) constitute a significant portion of installations, while high-capacity units above 300 kW are increasingly deployed in large infrastructure and industrial projects. Application segmentation covers standby, prime/continuous, and peak shaving uses, with standby systems widely implemented to ensure operational continuity in critical facilities. End-user segmentation highlights industrial, commercial, residential, and specialized sectors such as healthcare and telecom, each with distinct reliability and performance demands. These segmentations enable stakeholders to optimize product portfolios, deployment strategies, and service offerings tailored to regional and sector-specific needs.

The Diesel Power Generation & Distribution market includes several product types tailored to varied power requirements. 60–300 kW gensets currently account for the largest share at approximately 40% of total installations, serving mid-sized commercial buildings, healthcare facilities, and industrial sites for both standby and prime power. Units below 60 kW represent around 35% of installations, typically used in residential and light commercial settings where compact size and low noise are critical. Units above 300 kW comprise roughly 25% of the market, deployed in large industrial complexes, microgrids, and infrastructure projects, with advanced bi-fuel capabilities reducing diesel consumption by up to 20%. The fastest-growing segment is the high-capacity >300 kW category, driven by industrial demand for reliable, high-capacity power solutions.

Diesel Power Generation & Distribution applications are diverse and sector-specific. Standby power dominates with around 60–67.5% share, ensuring continuity for hospitals, data centers, and commercial facilities during grid outages. These systems automatically activate within seconds of power loss, safeguarding critical operations. Prime and continuous power applications serve off-grid industrial sites, remote infrastructure, and mining operations, where generators operate as the primary energy source. Peak shaving applications optimize utility costs and reduce peak demand charges in commercial buildings. Other niche applications include telecom installations and temporary construction power, where deployment flexibility and rapid response are essential.

End-user segmentation illustrates varying reliability needs across sectors. Industrial users lead with 45–60% of installations, driven by manufacturing, mining, and oil & gas facilities that require high-capacity gensets for both standby and continuous power in areas with unstable grids or remote operations. Commercial users, including offices, shopping complexes, and data centers, hold a significant share, with nearly 45% of medium-capacity gensets deployed to maintain uninterrupted operations. Residential adoption is notable in regions with frequent power outages, where compact generators support essential household loads. Specialized sectors such as healthcare and telecom rely on diesel gensets for mission-critical uptime, ensuring continuity of life-safety and communication services.

Asia‑Pacific accounted for the largest market share at approximately 41% in 2024, however, Asia‑Pacific is expected to register the fastest growth, expanding at a CAGR of around 5–7% between 2025 and 2032 given rapid infrastructure expansion and electrification programs.

Asia‑Pacific’s dominance reflects over 10.5 million operational diesel gensets, driven by extensive industrial, data center, and residential demand, particularly in China and India where urbanization and grid supplementation are priorities. North America follows with about 22–27% market share, supported by strong backup power needs in healthcare, finance, and industrial sectors, where over 60% of critical facilities maintain standby diesel systems. Europe holds roughly 18–19% share, with Germany, the UK, and France leading adoption through industrial manufacturing and emergency energy solutions. Middle East & Africa contribute nearly 12–13%, notably in oil & gas and remote infrastructure applications, while South America holds a smaller yet significant portion near 7–8%, driven by construction and mining sectors. These regional dynamics underscore differentiated adoption patterns and strategic deployment of diesel power solutions across the globe.

Is industrial backup and resilience shaping energy security solutions?

North America Diesel Power Generation & Distribution Market accounted for about 24–27% of global installations, with the United States contributing roughly 73% of regional volume through widespread deployment of diesel gensets in data centers, hospitals, manufacturing, and telecom. The region’s evolving infrastructure landscape is driving demand for standby power, with over 60% of industrial facilities adopting diesel backups due to grid vulnerabilities and extreme weather events. Regulatory emphasis on infrastructure resilience and federal spending on modernization supports technology upgrades, including IoT‑enabled remote monitoring systems in nearly 25% of new units to enhance predictive maintenance and efficiency. Local players are expanding service portfolios; for example, major OEMs are partnering with regional service networks to offer extended maintenance contracts and smart control retrofits. Consumer behavior shows higher enterprise adoption in sectors such as healthcare and finance, where uninterrupted power is critical, while residential buyers increasingly procure compact units for home backup in areas with frequent outages.

Is compliance and low‑emission innovation driving advanced power reliability solutions?

Europe Diesel Power Generation & Distribution Market holds around 18–19% of global share, with key markets including Germany, the UK, and France leading installations in industrial, commercial, and public infrastructure segments. Regulatory bodies across the EU are enforcing stringent emission standards, prompting adoption of low‑emission gensets and hybrid configurations that meet evolving environmental directives. Nearly 40% of new installations in Europe incorporate emission‑compliant technologies, reflecting strong sustainability focus. Emerging technologies like remote monitoring and low‑noise acoustic enclosures are increasingly integrated, especially in urban and industrial zones. A notable example is the deployment of advanced low‑emission units by major European manufacturers to support modernization in manufacturing and healthcare facilities. Regional consumer behavior emphasizes regulatory pressure that drives demand for explainable and compliant power solutions, with commercial sectors prioritizing backup reliability alongside environmental performance standards.

Is rapid industrial growth shaping scalable energy capacity platforms?

Asia‑Pacific Diesel Power Generation & Distribution Market leads globally with approximately 41% of total volume in 2024, anchored by major economies such as China, India, and Southeast Asian nations. China contributes roughly 45% of regional capacity, while India accounts for about 25%, with extensive adoption across manufacturing, data centers, and infrastructure projects. Urban expansion and electrification initiatives have accelerated mid‑range genset deployments, with sub‑60 kW units representing over 35% of regional installations and 60–300 kW units at about 40%. Advanced technologies such as smart control interfaces appear in around 42% of new units, enhancing operational flexibility. Local players are responding to demand; for instance, Chinese manufacturers supply high‑volume gensets integrated with hybrid options to support rural electrification and urban mobile infrastructure. Consumer behavior in Asia‑Pacific is driven by e‑commerce logistics, telecom expansions, and localized power needs where grid reliability remains inconsistent, prompting widespread diesel genset adoption.

Is infrastructure development fuelling resilient power deployment?

South America Diesel Power Generation & Distribution Market holds approximately 7–8% of global share, with Brazil and Argentina as key contributors. Regional demand is influenced by expansions in agriculture, mining, and construction sectors where power reliability is essential. Frequent grid fluctuations in rural and peri‑urban areas drive diesel genset adoption, particularly portable and mid-capacity units. Government incentives for infrastructure modernization and energy security programs are supporting diesel genset procurement, especially for emergency and project‑based power needs. Local manufacturers and service providers are focusing on tailored solutions that address remote electrification challenges. Consumer behavior in South America shows a strong preference for mobile generators and rental solutions in sectors such as events and temporary installations, reflecting varied energy reliability requirements across urban and rural markets.

Is energy intensity and remote infrastructure growth driving customized power resilience?

Middle East & Africa Diesel Power Generation & Distribution Market represents roughly 12–13% of the global share, led by UAE, Saudi Arabia, and South Africa. The region’s energy-intensive industries—particularly oil & gas and large-scale construction—drive demand for robust diesel solutions capable of prime and standby power duties. Technological modernization trends include ruggedized gensets with extended operational capacity, hybrid integration for improved fuel efficiency, and remote maintenance features suited to harsh operational environments. Local demand patterns vary, with oil & gas operations and urban infrastructure projects requiring high-capacity units, while rural communities and off-grid sites adopt compact models for basic electrification support. Consumer behavior shows reliance on diesel power where grid infrastructure is limited, and a preference for heavy-duty systems that ensure continuity for critical sectors.

• China – ~16% market share: High industrial deployment volume and extensive infrastructure expansion underpin China’s leading position.

• United States – ~7–8% market share: Strong demand from data centers, healthcare, and commercial facilities sustains the U.S. diesel power generation market.

The Diesel Power Generation & Distribution market exhibits a moderately concentrated competitive environment shaped by a mix of global giants and numerous regional specialists. Approximately 40–50 active competitors vie for market positioning, with the top five companies collectively holding an estimated 40–50% combined share of global diesel generator shipments. This reflects a balance between established OEMs and emerging regional manufacturers addressing localized demand. Leading firms pursue strategic initiatives such as partnerships with service networks in over 190 countries, product launches of hybrid and IoT‑enabled gensets, and expansion of digital monitoring platforms to differentiate offerings. Over 30% of new products now feature remote diagnostics systems, enhancing predictive maintenance capabilities across commercial and industrial applications. Innovation trends in low‑emission technologies, digital control systems, and hybrid power integrations continue to drive competition. Mergers and acquisitions are also occurring as companies broaden portfolios and enter new regional markets. Strong brand equity, extensive distribution networks, and comprehensive after-sales support remain key differentiators in this evolving market.

Kohler Co.

Mitsubishi Heavy Industries Ltd.

MTU Onsite Energy

Wartsila Corporation

Atlas Copco AB

FG Wilson

HIMOINSA

Yanmar Co.

Briggs & Stratton

Kirloskar Oil Engines Ltd.

Perkins Engines Company Ltd.

Doosan Portable Power

The Diesel Power Generation & Distribution market is increasingly driven by the adoption of advanced technologies that enhance efficiency, reliability, and operational flexibility. IoT-enabled monitoring systems are now integrated into over 35% of newly deployed diesel gensets, enabling real-time performance tracking, predictive maintenance, and remote diagnostics. These systems reduce unscheduled downtime by up to 20% and optimize fuel consumption by 10–15% in industrial and commercial applications. Hybrid diesel-electric solutions are gaining traction, combining traditional diesel engines with battery storage or solar integration, providing load leveling and reducing fuel dependency by approximately 25% in microgrid and off-grid installations.

Automation in control systems is another key advancement, with over 30% of medium- to high-capacity units adopting automated load management, remote start/stop, and grid-synchronization features to improve operational efficiency in multi-generator setups. Noise reduction and emission control technologies are also being prioritized; nearly 40% of urban installations now use low-noise enclosures and advanced exhaust treatment systems to meet stringent environmental and regulatory standards. Emerging trends include AI-driven predictive analytics for power demand forecasting and modular genset architectures that allow rapid deployment in construction, industrial, and emergency applications.

Additionally, digital twin simulations are being employed in design and maintenance planning, enhancing lifecycle management and reducing service intervention times by 15–18%. Companies are also investing in fuel-flexible engines capable of running on biodiesel blends and synthetic fuels, enabling compliance with evolving global emission mandates. These technological developments collectively position diesel power generation as a resilient, efficient, and environmentally adaptable solution for industrial, commercial, and critical infrastructure sectors.

The scope of the Diesel Power Generation & Distribution Market Report encompasses a comprehensive examination of global deployment patterns, technology integration, and end‑use applications across diverse industry sectors. It assesses segmentation by product types, including compact units below 60 kW, mid‑range gensets between 60–300 kW, and high‑capacity units above 300 kW, detailing configuration preferences and performance indicators across sectors such as industrial, commercial, residential, and critical infrastructure. Geographic coverage spans key regions including Asia‑Pacific, North America, Europe, South America, and the Middle East & Africa, offering insights into regional deployment volumes, operational priorities, and consumer behavior variations.

The report also evaluates application segments such as standby, prime/continuous, and peak shaving scenarios, with contextual analysis of usage dynamics in sectors like healthcare, data centers, construction, oil & gas, and telecom operations. Technology trends such as IoT‑enabled remote monitoring, hybrid diesel‑renewable systems, automation in control architectures, and emissions control mechanisms form a dedicated section, highlighting adoption levels and integration challenges. Additionally, emerging niches like microgrid integrations, portable mobile gensets, and modular scalable solutions are examined for their strategic relevance.

Industry focus areas include regulatory compliance landscapes, emissions thresholds, and fuel diversification initiatives, while performance benchmarking across over 150 diesel genset models provides a detailed view of competitive positioning and product differentiation. The report’s breadth ensures actionable insights for decision‑makers assessing market opportunities, technological innovations, and deployment strategies across global markets.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 196.24 Million |

|

Market Revenue in 2032 |

USD 289.94 Million |

|

CAGR (2025 - 2032) |

5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Caterpillar Inc. , Cummins Inc. , Generac Holdings Inc. , Kohler Co., Mitsubishi Heavy Industries Ltd., MTU Onsite Energy, Wartsila Corporation, Atlas Copco AB, FG Wilson, HIMOINSA, Yanmar Co., Briggs & Stratton, Kirloskar Oil Engines Ltd., Perkins Engines Company Ltd., Doosan Portable Power |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |