Reports

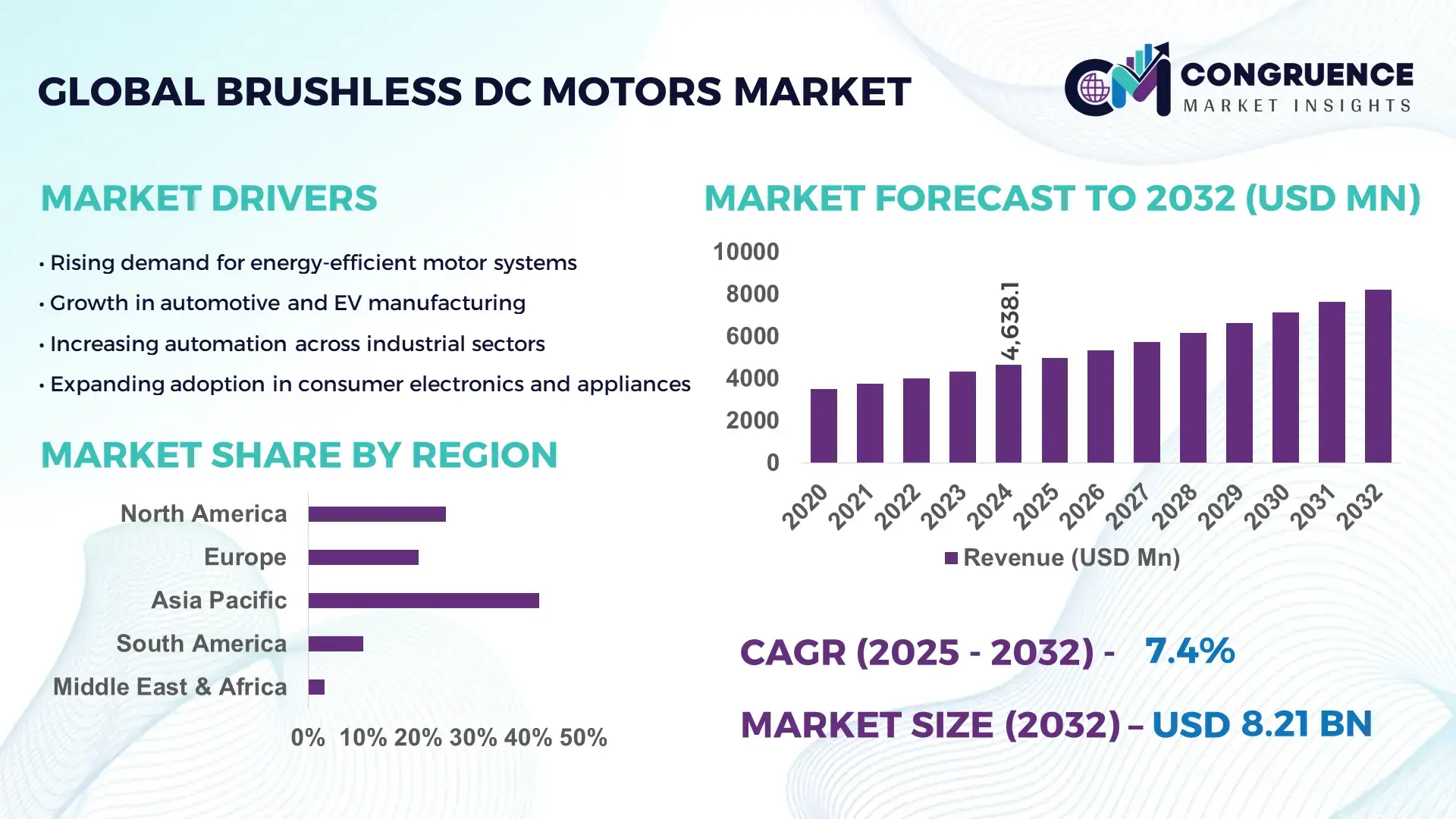

The Global Brushless DC Motors Market was valued at USD 4638.12 Million in 2024 and is anticipated to reach a value of USD 8210.63 Million by 2032 expanding at a CAGR of 7.4% between 2025 and 2032. Growth is driven by rising industrial automation and increasing demand for high-efficiency motion control systems.

China remains the leading hub for Brushless DC Motor production, supported by extensive manufacturing infrastructure, over USD 12 billion in annual industrial automation investments, and strong adoption across automotive, consumer electronics, and robotics sectors. The country hosts more than 40% of global BLDC motor manufacturing facilities and produces over 3 million units annually for applications in EVs, drones, smart appliances, and precision machinery. Advanced R&D programs in compact motor architecture, rare-earth magnet optimization, and high-torque density designs further strengthen its technological edge. Expanding domestic consumption, supported by over 65% adoption in home appliances and over 30% penetration in EV powertrain systems, reinforces its strategic position in the global market.

Market Size & Growth: Valued at USD 4638.12 Million in 2024 and projected to reach USD 8210.63 Million by 2032 at a 7.4% CAGR, supported by rising demand for energy-efficient motion control solutions.

Top Growth Drivers: 28% rise in automation adoption, 22% improvement in motor efficiency, and 31% increase in EV-driven demand.

Short-Term Forecast: By 2028, system-level cost optimization is expected to reduce manufacturing costs by up to 12%, improving operational performance by roughly 15%.

Emerging Technologies: Growth in integrated smart motor systems, high-torque density compact motors, and AI-enabled predictive maintenance controllers.

Regional Leaders: Asia-Pacific projected to reach USD 4.2 Billion by 2032 with rapid EV adoption; North America expected to hit USD 1.9 Billion with strong robotics uptake; Europe anticipated at USD 1.6 Billion driven by industrial automation upgrades.

Consumer/End-User Trends: Strong adoption in HVAC, EV powertrain systems, precision robotics, and consumer appliances, led by demand for quieter operation and longer service life.

Pilot or Case Example: In 2024, an industrial robotics pilot demonstrated a 17% efficiency gain through next-gen BLDC motors with lower thermal losses.

Competitive Landscape: Market leader holds approximately 12% share, followed by key competitors including Nidec, Maxon Motor, Johnson Electric, and MinebeaMitsumi.

Regulatory & ESG Impact: Efficiency mandates and low-emission manufacturing policies accelerate adoption of high-efficiency BLDC systems across industrial and commercial applications.

Investment & Funding Patterns: Over USD 1.3 Billion in recent investments directed toward motor automation upgrades, robotics integration, and EV component manufacturing.

Innovation & Future Outlook: Advancements in ultra-compact drives, rare-earth magnet alternatives, and IoT-enabled motor monitoring expected to shape long-term market expansion.

Unique information about the Brushless DC Motors Market spans multiple fast-growing industrial sectors, with significant adoption in EVs, smart manufacturing, HVAC, and consumer appliances, collectively contributing over 60% of total demand. Recent innovations include high-efficiency BLDC drives, sensorless control algorithms, and rare-earth-optimized magnetic designs that enhance torque density and reduce energy losses. Regulatory pressure for low-emission operations and efficiency compliance continues to strengthen market adoption across developed regions, complemented by rising consumption in Asia-Pacific driven by automation programs and electrified mobility. Emerging trends such as compact motor micro-integration, robotics-oriented BLDC designs, and intelligent drive systems are expected to guide the next decade of growth.

The strategic relevance of the Brushless DC Motors Market continues to strengthen as global industries transition toward data-driven manufacturing, electrified mobility, and high-efficiency motion control systems. Advanced BLDC architectures increasingly replace brushed and induction motors, with new-generation compact BLDC platforms delivering up to 18% efficiency improvement compared to legacy brushed motor systems. Asia-Pacific dominates in volume, while Europe leads in adoption with more than 46% of enterprises integrating smart motor control systems into production lines. By 2027, AI-enabled motor diagnostics is expected to cut system downtime by nearly 22%, improving operational productivity across automotive, aerospace, HVAC, and industrial automation sectors. Firms are committing to ESG improvements such as 30% energy optimization in motor-driven systems and 20% component recycling by 2030. In 2024, Japan achieved a 14% reduction in motor-related energy losses through nationwide digital factory initiatives powered by smart BLDC controllers. Looking forward, the Brushless DC Motors Market is positioned as a pillar of resilience, compliance, and sustainable growth, supporting long-term industrial transformation through high-efficiency, low-maintenance, and digitally optimized drive technologies.

Rising industrial automation significantly accelerates demand for Brushless DC motors as automated systems increasingly depend on compact, efficient, and controllable motion solutions. Sectors such as automotive, electronics manufacturing, and logistics employ BLDC motors in robotics, conveyor systems, and precision tools due to their high torque-to-weight ratio and longer operational life. In 2023, global installations of industrial robots exceeded 530,000 units, with over 70% of these deploying BLDC motors for precision and speed control. Factory modernization programs across Asia-Pacific and Europe have led to a measurable improvement in operational throughput, with BLDC-equipped robotic systems providing up to 15% higher performance stability compared to traditional motor types. As manufacturers prioritize energy efficiency, noise reduction, and reliability, the role of BLDC motors in advanced automation ecosystems continues to expand.

The Brushless DC Motors Market faces constraints stemming from fluctuations in raw material availability, especially rare-earth magnets essential for high-performance motor construction. Neodymium and dysprosium supply variability has created procurement pressures, with global rare-earth prices experiencing volatility of over 25% in certain quarters during 2023–24. This directly affects production timelines and increases overall manufacturing costs, leading many companies to revisit sourcing strategies or explore magnet recycling. Additionally, geopolitical factors impacting rare-earth-producing regions contribute to supply instability, affecting long-term planning for manufacturers dependent on consistent material quality. The challenge is intensified by rising demand from EV, robotics, and electronics industries, which amplifies competition for limited high-grade magnet resources. These structural constraints pose ongoing risks to output capacity and strategic supply continuity.

The rapid shift toward electric mobility provides substantial growth opportunities for the Brushless DC Motors Market as EVs, e-bikes, and electric two-wheelers increasingly incorporate BLDC motors for propulsion, battery cooling systems, and auxiliary motion functions. Global electric two-wheeler sales surpassed 50 million units in 2024, with more than 60% equipped with BLDC drive motors due to their superior efficiency and compact design. Emerging economies in Asia and Latin America are accelerating electrification programs that encourage domestic BLDC motor production and technology transfer, creating new opportunities for suppliers. Advancements in motor control algorithms, lightweight materials, and integrated drive electronics open further potential for performance optimization and reduced energy consumption. As infrastructure investments expand, the integration of BLDC motors across EV segments is expected to deepen, strengthening the market’s long-term opportunity structure.

Increasing design complexity presents a significant challenge for manufacturers in the Brushless DC Motors Market as modern applications require higher precision, lower noise, and enhanced torque density. The integration of embedded controllers, advanced cooling systems, and sensorless feedback mechanisms demands significant engineering expertise and longer development cycles. In 2024, more than 40% of motor manufacturers reported extended prototyping timelines due to advanced control algorithm requirements. Additionally, compliance with evolving global motor efficiency and safety standards increases production and testing workloads. These complexities also elevate costs related to R&D, skilled labor, and specialized manufacturing equipment. As industries increasingly demand customized motor solutions for robotics, aerospace, and medical devices, manufacturers must balance innovation with regulatory compliance and operational feasibility, creating persistent structural challenges.

• Acceleration of High-Efficiency Motor Integration: Industries are rapidly transitioning to next-generation high-efficiency BLDC motors, with over 48% of newly installed industrial drive systems in 2024 adopting upgraded motor architectures that reduce energy losses by 12–18%. Manufacturing plants integrating optimized magnetic materials and advanced cooling systems reported up to 20% improvement in torque density and a 15% reduction in thermal stress. This shift is driven by the need for consistent performance, lower maintenance intervals, and enhanced operational continuity across automotive, aerospace, and HVAC applications.

• Expansion of Smart Motor Control and IoT-Enabled Monitoring: The adoption of IoT-integrated BLDC systems increased by 37% between 2022 and 2024, supported by the demand for predictive maintenance and real-time diagnostics. Facilities deploying sensor-rich BLDC controllers experienced a measurable 22% drop in unexpected downtime and a 17% boost in cycle efficiency. AI-assisted control algorithms are becoming standard in high-end robotics and precision equipment, enabling tighter synchronization and reducing power fluctuations by up to 14%, making operations more resilient and data-driven.

• Growth in Electric Mobility and Lightweight Motor Platforms: Electric mobility applications continue to push BLDC motor innovation, with electric two-wheelers and compact EVs accounting for more than 62% of newly manufactured lightweight BLDC units in 2024. Advancements in stator design and material optimization have enabled a 16% reduction in motor mass and an 11% improvement in range efficiency for small EV platforms. Demand is particularly strong in Asia-Pacific and Europe as cities expand micro-mobility initiatives and low-emission transport programs.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Brushless DC Motors market, with 55% of new projects reporting measurable cost benefits through prefabricated and modular building practices. Automated cutting, drilling, and shaping machines that rely on BLDC motors have reduced on-site labor requirements by up to 28% while accelerating project timelines by nearly 18%. High-precision BLDC-powered equipment is gaining traction in North America and Europe, where construction efficiency targets are tightening and robotics-assisted workflows are expanding.

The Brushless DC Motors market is segmented by type, application, and end-user categories, each contributing distinctly to overall demand patterns. Types vary across inner-rotor, outer-rotor, and electronically commutated variants, supporting diverse industrial and commercial needs. Applications span automotive systems, industrial machinery, HVAC equipment, and consumer electronics, each adopting BLDC motors for efficiency, precision, and durability. End-user insights show robust adoption across automotive OEMs, electronics manufacturers, and industrial automation firms, with adoption rates rising due to increasing electrification and digitalization. Collectively, these segmentation layers highlight the market’s intricate structure, where technological advancements, rising automation, and expanded mobility patterns strengthen adoption across multiple industry tiers.

Inner-rotor BLDC motors represent the leading type and account for approximately 46% of the market’s adoption due to their high torque density, compact structure, and suitability for automotive, robotics, and industrial automation applications. Outer-rotor motors hold around 28% of adoption and continue to gain traction in HVAC systems and consumer appliances for their superior cooling efficiency. Electronically commutated motors are emerging rapidly, currently representing 18% of adoption but expected to expand significantly given rising electronics miniaturization and lightweight machinery trends. A combined 8% share is contributed by niche BLDC types such as slotless and frameless motors, which support specialized aerospace, medical, and defense-grade designs. The fastest-growing type is the electronically commutated segment, supported by smarter electronics integration, and is expanding at an estimated 11% growth rate driven by enhanced efficiency, reduced noise, and controller-based programmability.

Automotive applications remain the dominant segment, accounting for roughly 44% of the market, driven by expanding electric mobility, increased use in power steering systems, and demand for efficient drive modules. Industrial machinery accounts for 29% of adoption, while HVAC systems represent approximately 18%. Comparatively, consumer electronics hold around 9% yet exhibit strong unit-volume growth as compact BLDC motors replace legacy brushed variants in smart appliances. The fastest-growing segment is electric mobility applications, supported by smart control electronics and lightweight motor designs, with an estimated 12% growth rate. Other applications collectively contribute 13% across medical devices, drones, and aerospace subsystems.

Automotive manufacturers constitute the leading end-user segment, holding about 41% share supported by increasing electrification and integration of BLDC motors in propulsion, cooling, and auxiliary systems. Electronics manufacturers account for nearly 27% of adoption, while industrial automation firms represent 22% as factories transition toward smart robotic machinery. Comparatively, aerospace and medical technology users hold 10% but are recording steady gains due to rising demand for precision and reliability. The fastest-growing end-user segment is industrial automation, expanding at an estimated 10% growth rate driven by rising investments in robotics, AI-driven production lines, and automated inspection systems. Remaining end-users collectively contribute 12%, supported by rising adoption in defense, logistics, and smart home ecosystems.

Asia-Pacific accounted for the largest market share at 47% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2025 and 2032.

Asia-Pacific’s strong position reflects its high-volume manufacturing base, extensive electric mobility deployment, and large-scale automation adoption. North America’s acceleration is supported by rising robotics installations, advanced motor-control innovations, and increased industrial modernization. Europe held 23% of global demand in 2024, led by strict energy-efficiency regulations and expanding HVAC adoption, while South America and the Middle East & Africa collectively contributed 12%. Growing industrial electrification, rising demand for lightweight motors, and ongoing infrastructure upgrades across major economies continue to reinforce region-wise performance.

How is rapid automation reshaping adoption trends in this market?

North America represents nearly 26% of global Brushless DC Motors demand, supported by strong uptake in automotive manufacturing, aerospace engineering, and industrial robotics. The region benefits from modernization incentives and updated energy-efficiency standards that encourage the replacement of legacy motors. Technological advancements—such as AI-integrated motor controllers, sensor-enabled monitoring, and digital-twin-based optimization—continue to strengthen adoption across U.S. and Canadian industries. A prominent local manufacturer introduced high-efficiency BLDC platforms that improved drive-system productivity by 19% across logistics and warehousing operations. Enterprise consumers in this region show higher adoption of precision-driven BLDC systems, particularly in healthcare and financial services infrastructure requiring uninterrupted performance and low-maintenance operations.

Why is regulatory-driven modernization accelerating market transformation?

Europe accounts for approximately 23% of Brushless DC Motors consumption in 2024, led by Germany, the UK, and France. Strict sustainability requirements and energy-efficiency legislation continue to drive replacement of traditional motors across HVAC, industrial machinery, and mobility applications. European industries increasingly adopt advanced motor technologies, including integrated control electronics and IoT-based efficiency monitoring. A major regional producer introduced compact low-noise BLDC units designed for smart appliances, supporting stricter EU environmental compliance rules. Consumer behavior in this region favors transparent, traceable, and compliance-ready technologies, and regulatory pressure increasingly fuels demand for smart, explainable, and environmentally aligned BLDC solutions.

How is manufacturing expansion strengthening this region’s technological leadership?

Asia-Pacific holds the highest demand volume and remains the manufacturing hub for Brushless DC Motors, accounting for 47% of global consumption in 2024. China, India, and Japan lead adoption due to large-scale EV production, automation-intensive factories, and fast-growing consumer electronics markets. The region’s innovation centers are accelerating advancements in lightweight motor design, rare-earth magnet alternatives, and high-efficiency industrial motors. A major Asian producer deployed high-torque compact BLDC motors for electric two-wheelers, improving operational efficiency by 17%. Consumer behavior is shaped by mobile-first ecosystems and e-commerce integration, where technology-driven, cost-efficient motor solutions dominate product design and industrial procurement.

How are energy and infrastructure transitions shaping regional motor demand?

South America accounts for nearly 7% of global Brushless DC Motors demand, led by Brazil and Argentina. Expanding renewable energy projects, modernization of industrial facilities, and investments in public infrastructure contribute significantly to regional momentum. Government incentives for energy-efficient equipment are encouraging the shift toward BLDC-powered machinery in utilities, construction, and urban mobility. A local Brazilian manufacturer recently adopted BLDC-driven automation modules, improving production output by 15%. Consumer behavior in this region is influenced by increased digital engagement, with demand tied closely to localized technologies, media platforms, and language-compatible smart devices integrating BLDC-driven components.

How is industrial diversification driving next-generation motor adoption?

The Middle East & Africa represents around 5% of global Brushless DC Motors demand, with key growth markets including the UAE, Saudi Arabia, and South Africa. Expanding construction activities, rising oil & gas automation, and increased investment in smart manufacturing ecosystems are accelerating demand for efficient motor solutions. Technological modernization—such as AI-enabled motor diagnostics and remote-performance monitoring—is becoming more common in industrial operations. A regional automation supplier integrated BLDC-powered precision pumps across petrochemical plants, enhancing operational accuracy by 14%. Consumer behavior varies widely, but increasing preference for energy-efficient, low-maintenance equipment reflects broader national sustainability strategies.

China – 32% market share: Driven by large-scale manufacturing capacity and widespread deployment across EVs, appliances, and industrial automation.

United States – 18% market share: Supported by strong automotive innovation, advanced robotics adoption, and continuous upgrades to smart industrial infrastructure.

The Brushless DC Motors market reflects a moderately consolidated structure, with the top five companies collectively accounting for approximately 42% of global market participation. More than 180 active manufacturers operate across major regions, competing on parameters such as torque efficiency, motor miniaturization, precision control, and durability. Competitive intensity has increased as over 30% of suppliers introduced upgraded compact motor architectures between 2023 and 2024, targeting robotics, HVAC, EV powertrains, and industrial automation. Strategic collaborations are becoming more frequent, with an estimated 25–28 partnership agreements recorded globally during the same period, many focused on improving magnet technology, enhancing thermal management, and integrating digital control electronics. Mergers and acquisitions also shape the landscape, with at least 6 significant deals in the past two years aimed at expanding portfolio breadth and production capacity.

Innovation remains a key differentiator, as nearly 40% of leading companies invest heavily in AI-based motor control algorithms and smart monitoring systems. Manufacturers are also accelerating investments in high-speed BLDC platforms, driven by demand from EV auxiliary systems and consumer electronics. Cost optimization continues to drive competition, with around 15% of companies expanding automated production lines to reduce assembly variance and improve motor reliability. This environment positions technologically advanced firms at a competitive advantage while compelling others to strengthen regional distribution networks and diversify end-use applications.

Nidec Corporation

Maxon Motor AG

Johnson Electric

Bosch Mobility

Siemens

TECO Electric & Machinery Co.

Allied Motion Technologies

Toshiba Electronic Devices & Storage Corporation

Delta Electronics

MinebeaMitsumi Inc.

Advancements in magnet materials, power electronics, and control algorithms continue to redefine performance standards in the Brushless DC Motors market. One of the most significant technological shifts is the rapid adoption of high-energy neodymium magnets, which have improved torque density by up to 25% compared to traditional ferrite-based configurations. Manufacturers are increasingly deploying slotless motor designs, enabling smoother operation and reducing acoustic noise by nearly 40%, making them ideal for medical devices, drones, and precision industrial tools. Digital motor control is evolving quickly, with 32-bit microcontrollers now used in over 60% of newly developed BLDC systems. These controllers enhance real-time monitoring accuracy, reduce rotational deviations by approximately 18%, and support advanced features such as predictive maintenance and adaptive load handling. Additionally, the shift toward sensorless control technology is accelerating, with adoption levels rising by more than 30% between 2022 and 2024. This trend helps lower motor weight and cost while improving reliability by eliminating Hall sensors.

Thermal management innovations are also shaping product design. New liquid-cooled BLDC architectures can dissipate heat up to 50% more efficiently than air-cooled systems, enabling sustained high-speed performance in robotics, EV subsystems, and automated manufacturing equipment. Meanwhile, ultra-compact BLDC motors are gaining traction in consumer electronics, where miniaturized designs have reduced motor footprints by 20–35% without sacrificing torque output. Emerging trends include the integration of wide-bandgap semiconductors, particularly SiC and GaN, in motor drivers, improving switching efficiency by 15–22% and reducing energy losses across various load conditions. These advancements are collectively strengthening the technological competitiveness of BLDC solutions across automotive, industrial automation, aerospace, and smart consumer applications.

In June 2023, Nidec Corporation announced the development of a “Digital Twin-type Intelligent Motor®” proof-of-concept, enabling motors equipped with microcomputers to operate in virtual environments for simulation, predictive maintenance, and real-time IoT control — a leap toward smarter, cloud-connected BLDC deployments. (NIDEC CORPORATION)

In November 2024, in collaboration with Renesas Electronics Corporation, Nidec unveiled the world’s first “8-in-1” E-Axle proof-of-concept for electric vehicles, integrating motor, inverter, gear, DC/DC converter, on-board charger, power-distribution and battery-management functions under a single microcontroller — significantly reducing system complexity, size, and component count. (Renesas Electronics)

In 2024, maxon expanded its BLDC offering by launching the new ECX PRIME 16L motor — a compact, ironless, 4-pole rotor motor delivering high torque at speeds up to 40,000 rpm, catering to high-dynamics applications in robotics, medical devices, and precision tools. (maxongroup.com)

In 2024 at an international aerospace trade event, maxon presented precision drive systems including brushless DC motors and gearheads designed to meet stringent environmental and quality standards such as DO-160/G and AS/EN 9100 — signalling deeper BLDC integration within aerospace, UAV, and satellite systems. (maxongroup.com)

This report offers a broad and detailed examination of the Brushless DC Motors market across multiple dimensions: product types, applications, technologies, geographic regions, and industry verticals. On the product side, the analysis spans core BLDC variants — compact precision motors, high-torque industrial drives, frameless motors, and integrated gear-motor assemblies — including emerging designs suitable for robotics, medical devices, EV propulsion systems, HVAC, and automation equipment. In applications, the report covers automotive (EV powertrain, auxiliary systems), industrial automation, HVAC & ventilation, consumer electronics, aerospace / drones / defense, medical devices, and emerging mobility (e-bikes, light EVs). It highlights how BLDC motors serve varied use cases — from high-speed precision tooling and robotics arms to energy-efficient HVAC compressors and vehicle electrification solutions. Regional coverage includes Asia-Pacific, North America, Europe, South America, Middle East & Africa — analysing manufacturing hubs, consumption centers, regulatory influences, and infrastructure-driven demand patterns.

Technological focus areas include motor design innovations (ironless windings, four-pole rotors, frameless platforms), integrated control electronics, IoT-enabled “smart motor” solutions, digital twin and edge-computing architecture, and integrated e-axle or drive-unit systems. The report also addresses environmental, energy-efficiency, and ESG considerations influencing regulatory compliance and sustainable adoption trends. Industry vertical insights extend to EV OEMs, robotics manufacturers, HVAC system suppliers, industrial automation integrators, medical equipment providers, and aerospace contractors. The scope includes evaluation of supply-chain developments, material constraints (e.g., rare-earth magnets), regional regulatory and energy-efficiency mandates, and opportunities arising from electrification, factory automation, and smart devices.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 4638.12 Million |

|

Market Revenue in 2032 |

USD 8210.63 Million |

|

CAGR (2025 - 2032) |

7.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Nidec Corporation , Maxon Motor AG , Johnson Electric, Bosch Mobility , Siemens, TECO Electric & Machinery Co., Allied Motion Technologies, Toshiba Electronic Devices & Storage Corporation, Delta Electronics, MinebeaMitsumi Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |