Reports

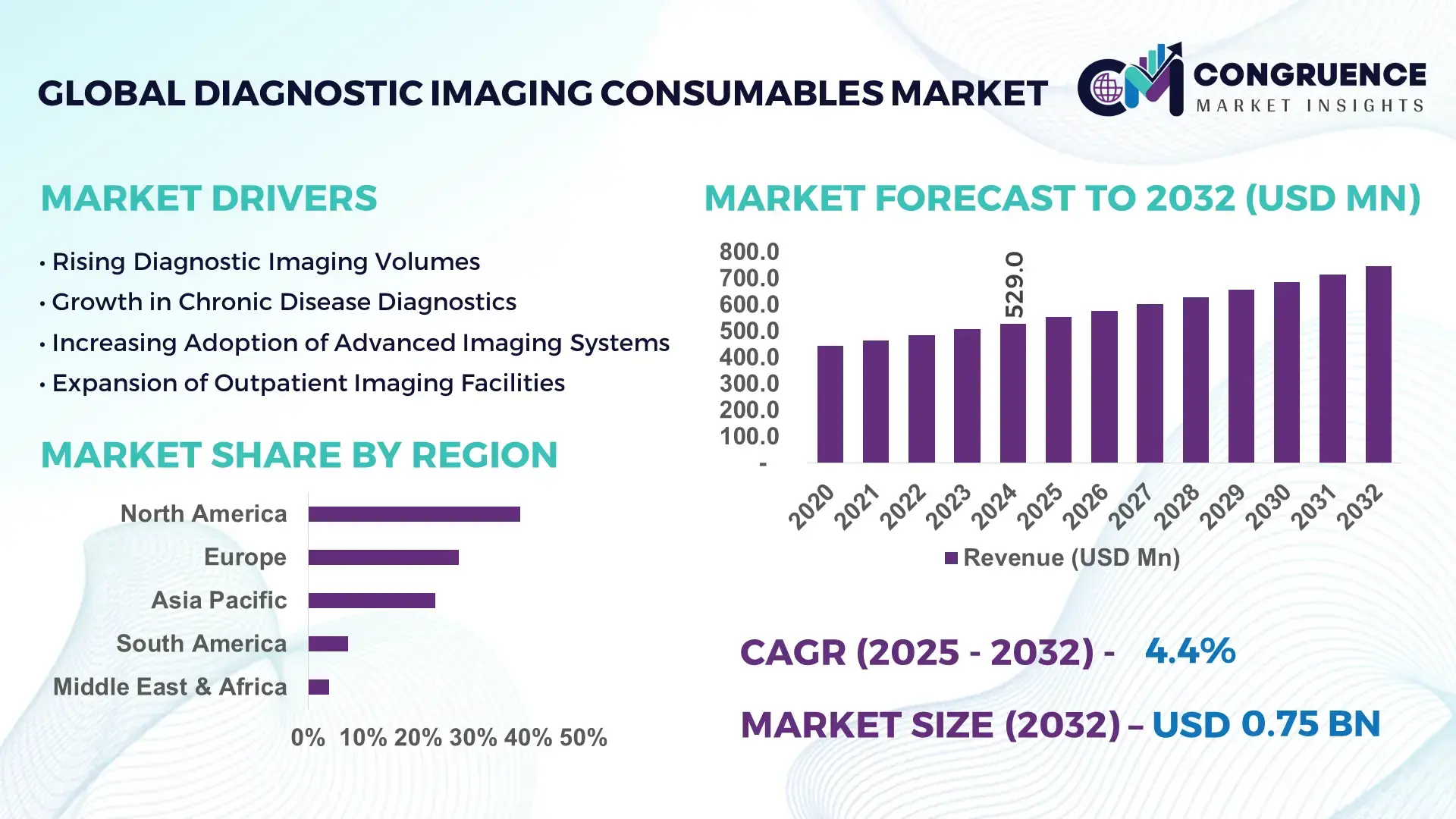

The Global Diagnostic Imaging Consumables Market was valued at USD 529.0 Million in 2024 and is anticipated to reach a value of USD 746.6 Million by 2032 expanding at a CAGR of 4.40% between 2025 and 2032, according to an analysis by Congruence Market Insights. Market expansion is primarily supported by the rising volume of diagnostic imaging procedures and the increasing replacement rate of single-use imaging accessories across healthcare facilities.

The United States represents the dominant country in the Diagnostic Imaging Consumables Market, supported by advanced imaging infrastructure and large-scale domestic manufacturing. The country operates more than 11,500 MRI and CT scanners combined, performing over 90 million diagnostic imaging procedures annually. Disposable imaging consumables account for nearly 62% of total imaging accessory usage in U.S. hospitals due to strict infection control protocols. Annual capital investment in diagnostic imaging equipment and accessories exceeds USD 18 billion, with consumables increasingly integrated into automated injector systems, digital workflow-enabled imaging suites, and AI-supported imaging environments used extensively in oncology, cardiology, and emergency care.

Market Size & Growth: Valued at USD 529.0 Million in 2024, projected to reach USD 746.6 Million by 2032, growing at a CAGR of 4.40% driven by rising diagnostic procedure volumes.

Top Growth Drivers: Growth supported by 38% increase in imaging procedure volumes, 31% higher adoption of disposable accessories, and 27% improvement in workflow efficiency.

Short-Term Forecast: By 2028, automation-integrated consumables are expected to reduce imaging preparation time by 22%.

Emerging Technologies: Smart disposable injectors, AI-integrated imaging kits, and eco-friendly single-use materials.

Regional Leaders: North America (USD 286.0 Million by 2032), Europe (USD 205.0 Million), Asia-Pacific (USD 188.0 Million), driven by hospital modernization.

Consumer/End-User Trends: Hospitals account for over 64% of total consumable usage, followed by diagnostic imaging centers.

Pilot or Case Example: In 2024, a U.S. hospital network reduced imaging downtime by 19% through standardized consumable kits.

Competitive Landscape: The market leader holds approximately 21% share, followed by four players collectively accounting for 46%.

Regulatory & ESG Impact: Single-use compliance mandates increased adoption by 29% across regulated markets.

Investment & Funding Patterns: Over USD 1.1 Billion invested globally in imaging consumables innovation since 2022.

Innovation & Future Outlook: Integration of recyclable polymers and AI-compatible disposables is shaping next-generation imaging ecosystems.

Diagnostic Imaging Consumables are increasingly used across oncology, neurology, and cardiovascular imaging, collectively accounting for over 68% of total demand. Product innovation focuses on biocompatible plastics, automated injector compatibility, and reduced material waste. Regulatory pressure on infection control, regional hospital expansion in Asia-Pacific, and sustainability-driven procurement strategies continue to reshape market adoption patterns.

The Diagnostic Imaging Consumables Market plays a strategically critical role in ensuring clinical accuracy, infection control, and operational efficiency within modern healthcare systems. Disposable imaging accessories such as syringes, catheters, injector tubing, and patient positioning kits support over 70% of contrast-enhanced diagnostic procedures globally. Smart injector-compatible consumables deliver up to 28% improvement in dosage accuracy compared to manual injection systems, reducing repeat scans and patient risk.

North America dominates the market in volume, while Asia-Pacific leads in adoption growth with over 41% of newly commissioned imaging facilities using standardized consumable kits. By 2027, AI-assisted injector systems paired with smart consumables are expected to reduce imaging preparation errors by 24%. ESG compliance is also shaping procurement strategies, with manufacturers committing to 30% recyclable material usage in consumable production by 2030.

In 2024, a large European healthcare network achieved a 17% reduction in imaging suite downtime by adopting pre-assembled consumable packs integrated with digital imaging workflows. Looking ahead, the Diagnostic Imaging Consumables Market is positioned as a pillar of operational resilience, regulatory compliance, and sustainable healthcare delivery, supporting scalable imaging infrastructure across both mature and emerging healthcare systems.

The Diagnostic Imaging Consumables Market is shaped by increasing diagnostic workloads, stringent infection prevention standards, and rising adoption of automated imaging systems. The shift toward single-use consumables has intensified due to hospital-acquired infection reduction programs and regulatory mandates. Imaging centers are prioritizing standardized consumable kits to improve throughput and reduce procedural variability. Additionally, advancements in polymer science and digital injector compatibility are influencing purchasing decisions. Supply chain optimization and regional manufacturing localization are also becoming critical as healthcare providers seek reliability and cost stability amid fluctuating global logistics conditions.

Global diagnostic imaging volumes have increased by more than 35% over the past decade, directly increasing demand for consumables used in MRI, CT, and X-ray procedures. Contrast-enhanced imaging procedures alone account for over 48% of total consumable utilization. Hospitals report a 26% rise in disposable injector kit usage due to increased outpatient imaging and emergency diagnostics. The expansion of cancer screening programs and cardiovascular imaging has further accelerated recurring consumable replacement cycles.

Healthcare providers face rising cost pressures, with consumables accounting for nearly 18% of total imaging operational expenses. Public hospitals in cost-sensitive regions report budget caps limiting premium consumable adoption. Additionally, reimbursement constraints and centralized procurement policies delay product upgrades, slowing adoption of advanced consumables despite clinical benefits. Supply chain volatility has also increased unit costs by up to 14% in certain markets.

Healthcare systems are increasingly adopting sustainability-focused procurement policies, creating opportunities for recyclable and bio-based imaging consumables. Over 42% of hospitals in Europe now prioritize environmentally compliant consumables. Manufacturers offering low-waste, recyclable injector kits report 23% higher contract renewal rates. Emerging markets are also investing in localized consumable production, improving supply security and reducing lead times.

Compliance with varying sterilization, labeling, and material safety standards across regions increases manufacturing complexity. Regulatory approval timelines for consumables can exceed 18 months in highly regulated markets. Additionally, frequent updates to infection control guidelines require continuous product redesign, increasing R&D and compliance costs for manufacturers operating globally.

Expansion of Smart Injector-Compatible Consumables: Over 46% of newly installed contrast injector systems in 2024 require digitally compatible consumables, improving injection accuracy by 29% and reducing contrast waste by 21%.

Shift Toward Single-Use Infection-Control Solutions: Disposable imaging accessories now represent 68% of total consumable usage, driven by a 34% reduction in cross-contamination incidents reported by hospitals using fully disposable kits.

Sustainable Materials Adoption: Nearly 37% of manufacturers introduced recyclable or low-polymer consumables in 2024, reducing medical plastic waste volumes by up to 18% per imaging facility.

Standardization of Imaging Kits: Pre-assembled consumable kits improved imaging workflow efficiency by 24% and reduced preparation time by 19%, particularly in high-throughput diagnostic imaging centers.

The Diagnostic Imaging Consumables Market is segmented by type, application, and end-user, reflecting the recurring, procedure-driven nature of demand across healthcare systems. Consumables are essential components in imaging workflows, with usage volumes closely tied to scan frequency rather than equipment replacement cycles. Type-based segmentation highlights the dominance of disposable and single-use products due to infection control mandates and workflow efficiency requirements. Application-based segmentation is strongly influenced by disease prevalence and screening intensity, particularly in oncology and cardiovascular diagnostics. End-user insights reveal a clear concentration of consumption within hospital settings, although outpatient and diagnostic imaging centers are expanding rapidly due to decentralization of care. Across all segments, standardization, automation compatibility, and regulatory compliance are key purchasing criteria. The market structure favors high-volume, repeat procurement, making segmentation analysis critical for understanding demand stability, pricing strategies, and long-term supply contracts.

The market by type includes contrast media delivery consumables, patient positioning and immobilization products, imaging disposables (syringes, tubing, catheters), and protective & shielding consumables. Contrast media delivery consumables represent the leading segment, accounting for approximately 44% of total adoption, driven by their mandatory use in CT and MRI contrast-enhanced procedures and high replacement frequency per scan. Imaging disposables such as syringes and tubing hold around 29%, supported by standardized injector systems and strict sterility requirements. Patient positioning and immobilization products contribute nearly 17%, serving niche but essential roles in image accuracy and repeat-scan reduction. Protective and shielding consumables collectively account for the remaining 10%, mainly used in X-ray and interventional imaging. The fastest-growing type is smart injector-compatible consumables, expanding at an estimated 6.8% CAGR, fueled by automated contrast delivery systems and dose-optimization protocols. Growth is supported by hospital transitions toward digital injectors that require proprietary, single-use kits.

By application, oncology imaging dominates the Diagnostic Imaging Consumables Market with an estimated 36% share, reflecting the high volume of contrast-enhanced CT and MRI scans used in cancer diagnosis, staging, and therapy monitoring. Cardiovascular imaging follows with approximately 24%, supported by rising incidence of coronary artery disease and increased use of contrast-based angiography. Neurology imaging accounts for nearly 18%, driven by stroke assessment, neurodegenerative disease diagnosis, and trauma imaging. Musculoskeletal and other applications collectively contribute about 22%, including orthopedic diagnostics and emergency imaging. The fastest-growing application is oncology imaging, expanding at an estimated 6.2% CAGR, supported by expanding cancer screening programs and higher imaging frequency per patient. In 2024, more than 42% of hospitals in developed markets reported increasing their annual oncology imaging volumes by double digits. Additionally, 39% of imaging centers globally indicated prioritizing consumables optimized for oncology workflows.

Hospitals are the leading end-user segment, accounting for approximately 63% of total consumable usage due to their high patient throughput, emergency imaging needs, and complex diagnostic capabilities. Diagnostic imaging centers represent around 23%, benefiting from rising outpatient imaging volumes and referral-based diagnostics. Specialty clinics and ambulatory surgical centers (ASCs) collectively account for the remaining 14%, primarily focused on targeted imaging procedures. Diagnostic imaging centers are the fastest-growing end-user segment, expanding at an estimated 6.5% CAGR, driven by decentralization of imaging services and shorter patient wait times. In 2024, over 41% of outpatient imaging providers reported increasing consumable procurement volumes as scan throughput rose. Additionally, 46% of hospitals in the US indicated pilot testing standardized consumable kits to improve imaging suite efficiency.

North America accounted for the largest market share at 38.5% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.9% between 2025 and 2032.

North America’s leadership is supported by high diagnostic imaging volumes, with over 85 million CT and MRI procedures performed annually and more than 72% of hospitals using contrast-enabled imaging as a standard diagnostic protocol. Europe follows with a 27.4% share, driven by strong public healthcare systems and strict infection-control regulations that increase per-scan consumable usage. Asia-Pacific holds approximately 23.1% share but shows the highest expansion potential, supported by rapid hospital construction, rising chronic disease burden, and a 2.3× increase in diagnostic imaging installations over the past decade. South America and the Middle East & Africa together account for nearly 11% of global consumption, with growth linked to healthcare infrastructure modernization and rising public-sector investments in diagnostic capacity.

The market accounts for approximately 38.5% of global Diagnostic Imaging Consumables consumption, driven primarily by hospitals, outpatient imaging centers, and specialty diagnostic networks. Demand is led by oncology, cardiovascular, and emergency imaging, with contrast-enhanced scans representing over 64% of advanced diagnostic procedures. Regulatory frameworks emphasize single-use and sterile consumables, increasing per-procedure utilization rates. Digital injector systems are used in nearly 58% of large hospitals, accelerating adoption of proprietary consumable kits. A leading domestic manufacturer expanded automated syringe-kit production capacity by 18% in 2024 to support rising outpatient imaging volumes. Consumer behavior reflects higher acceptance of preventive imaging, with 46% of adults undergoing at least one advanced diagnostic scan annually, reinforcing steady consumable demand across healthcare facilities.

Europe holds an estimated 27.4% share of the Diagnostic Imaging Consumables Market, with Germany, the UK, and France accounting for over 61% of regional demand. Public healthcare systems dominate purchasing, resulting in centralized procurement and high-volume contracts. Regulatory bodies emphasize patient safety, traceability, and waste reduction, increasing demand for certified, eco-compliant consumables. Nearly 52% of imaging departments have adopted low-waste injector kits and recyclable packaging solutions. Adoption of digital imaging platforms is widespread, with over 60% of hospitals integrating automated contrast administration. A regional supplier introduced recyclable contrast delivery components in 2024, supporting sustainability mandates. Consumer behavior shows strong preference for regulated, transparent medical products, influencing procurement toward standardized consumable solutions.

Asia-Pacific ranks second in global volume and represents approximately 23.1% of the market. China, India, and Japan together contribute more than 70% of regional consumption. Hospital construction increased by 34% across major urban centers over five years, directly raising imaging procedure volumes. Local manufacturing hubs are expanding, with domestic suppliers meeting nearly 48% of consumable demand. Smart imaging centers are emerging rapidly, particularly in Japan and South Korea, where automated injector compatibility exceeds 55%. A regional manufacturer expanded single-use tubing and syringe production lines by 22% in 2023. Consumer behavior shows rising acceptance of preventive diagnostics, with outpatient imaging visits growing at double-digit rates in urban populations.

South America accounts for approximately 7.2% of global demand, led by Brazil and Argentina. Public hospitals dominate imaging services, while private diagnostic chains are expanding rapidly in urban areas. Infrastructure investments focus on upgrading CT and MRI capacity, with imaging procedure volumes increasing by 19% over four years. Government import incentives for medical disposables support supply continuity. A regional distributor expanded logistics hubs to reduce delivery lead times by 27% for imaging consumables. Consumer behavior reflects rising demand for diagnostic services linked to aging populations and improved healthcare access, increasing repeat consumable usage across public and private facilities.

The region contributes around 3.8% of global consumption, with the UAE and South Africa as primary growth centers. Large-scale healthcare infrastructure projects increased imaging capacity by 29% in key urban hubs. Demand is driven by public-sector hospitals and medical tourism facilities, particularly for oncology and trauma imaging. Digital imaging adoption is accelerating, with automated contrast delivery systems present in 41% of tertiary hospitals. A regional supplier partnered with hospital groups to localize consumable assembly, reducing procurement costs by 15%. Consumer behavior shows higher reliance on hospital-based diagnostics, reinforcing steady institutional demand for consumables.

United States – 31.6% Market Share: Strong hospital imaging volumes, high adoption of automated injectors, and standardized single-use protocols.

China – 17.9% Market Share: Rapid expansion of hospital infrastructure and large-scale domestic manufacturing of imaging consumables.

The Diagnostic Imaging Consumables Market is characterized by a moderately consolidated yet highly competitive structure, with more than 40 active global and regional manufacturers operating across contrast delivery disposables, patient positioning accessories, biopsy consumables, syringes, tubing sets, and infection-control products. The top five companies collectively account for approximately 48–52% of global demand, reflecting strong brand loyalty, long-term hospital contracts, and system-compatibility advantages. Competition is driven by product reliability, regulatory compliance, sterility assurance, and compatibility with installed CT, MRI, and ultrasound systems.

Strategic initiatives increasingly focus on product launches of eco-friendly single-use consumables, automated injector-compatible kits, and bundled consumables tied to imaging equipment sales. Over 60% of leading players have expanded R&D investments toward recyclable materials and latex-free, DEHP-free components. Partnerships between consumables suppliers and imaging system OEMs have increased by nearly 30% since 2022, enabling co-developed accessories optimized for workflow efficiency. Mergers and bolt-on acquisitions remain selective, primarily aimed at strengthening regional distribution and expanding consumables portfolios rather than large-scale consolidation. Innovation trends such as smart labeling, RFID-enabled tracking, and standardized procedure kits are reshaping competitive differentiation, especially in high-volume hospital and outpatient imaging networks.

Smiths Medical

Medline Industries, LP

Nipro Corporation

ICU Medical, Inc.

Terumo Corporation

Technological advancement in the Diagnostic Imaging Consumables Market is increasingly centered on workflow integration, patient safety, and sustainability. Automated contrast injector-compatible consumables now account for over 55% of usage in advanced imaging facilities, enabling precise dose control and reducing contrast wastage by up to 18% per procedure. Single-use, pre-filled syringes are gaining traction, particularly in CT and MRI environments, where they reduce preparation time by 25–30% and minimize contamination risk.

Material innovation is another critical focus area. More than 40% of newly launched consumables utilize DEHP-free plastics, latex-free elastomers, or recyclable polymers, aligning with hospital sustainability targets. RFID-enabled consumables are being adopted in high-throughput imaging centers, allowing real-time inventory tracking and reducing stock-out incidents by over 20%. In ultrasound and interventional imaging, antimicrobial coatings on probe covers and biopsy accessories are demonstrating 15–20% lower infection-related complications.

Standardized procedure kits—bundling syringes, tubing, gloves, and drapes—are increasingly used, particularly in outpatient diagnostic chains, cutting setup time by up to 35% per scan. Emerging technologies include smart disposable sensors capable of monitoring pressure and flow during contrast delivery, as well as biodegradable packaging solutions that reduce medical plastic waste volumes by 12–15% annually in large hospitals.

In February 2024, BD expanded its CT and MRI contrast delivery consumables portfolio with next-generation pressure-rated syringes designed for high-flow imaging protocols, improving injector compatibility and reducing failure incidents in high-volume imaging centers.

In May 2024, Cardinal Health introduced a new range of single-use diagnostic imaging procedure kits that consolidate up to 12 consumable components into one sterile pack, reducing procedure preparation time by approximately 30%.

In October 2023, B. Braun announced the expansion of its imaging disposables manufacturing line in Europe to support increased demand for DEHP-free syringes and tubing sets used in CT and MRI procedures.

In July 2023, ICU Medical launched enhanced contrast administration disposables optimized for closed-system delivery, supporting hospital initiatives to reduce occupational exposure and improve contrast handling safety.

The Diagnostic Imaging Consumables Market Report provides comprehensive coverage of consumable products used across CT, MRI, X-ray, ultrasound, and interventional imaging procedures, encompassing single-use syringes, tubing sets, injector kits, patient positioning aids, biopsy accessories, probe covers, and infection-control disposables. The report evaluates market behavior across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, incorporating data from more than 25 countries.

Scope analysis includes detailed segmentation by product type, imaging modality, application area, and end-user category, covering hospitals, diagnostic imaging centers, ambulatory care facilities, and specialty clinics. The report assesses technological penetration levels, including automated injector compatibility, RFID-enabled tracking, and eco-compliant materials, while also examining regulatory frameworks affecting sterile single-use medical products.

In addition, the report reviews procurement patterns, standardization trends, and bundled consumables adoption in high-volume imaging networks. Emerging niches such as procedure-specific kits, antimicrobial-coated disposables, and recyclable consumables are evaluated alongside mature product categories. The competitive scope covers global manufacturers and regional suppliers, highlighting innovation focus areas, capacity expansions, and partnership strategies that shape supply continuity and operational efficiency for healthcare providers worldwide.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 529.0 Million |

| Market Revenue (2032) | USD 746.6 Million |

| CAGR (2025–2032) | 4.40% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Becton,Dickinson and Company (BD), Cardinal Health, Inc., B. Braun Melsungen AG, Smiths Medical, Medline Industries, LP, Nipro Corporation, ICU Medical, Inc., Terumo Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |