Reports

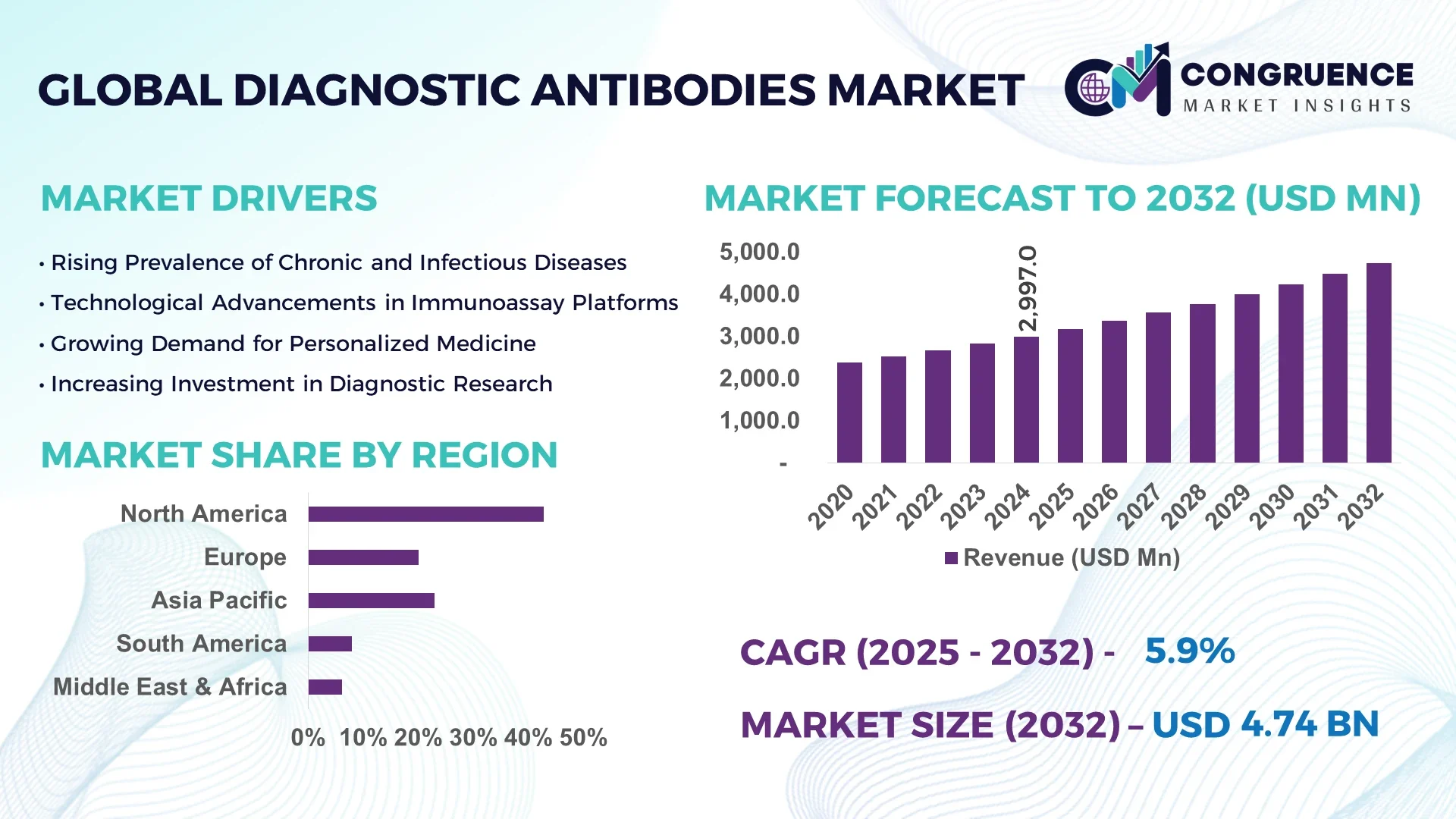

The Global Diagnostic Antibodies Market was valued at USD 2,997.0 million in 2024 and is anticipated to reach a value of USD 4,740.8 million by 2032, expanding at a CAGR of 5.9% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

North America, particularly the United States, dominates the diagnostic antibodies market. This leadership is attributed to advanced healthcare infrastructure, a strong regulatory framework, and a high prevalence of chronic diseases. The presence of key market players, robust R&D activities, and favorable reimbursement policies further contribute to market growth. Additionally, increasing adoption of personalized medicine and point-of-care testing drives market expansion in this region.

The diagnostic antibodies market is experiencing significant growth due to advancements in biotechnology and immunoassay techniques. The rise of companion diagnostics, which aid in tailoring treatments to individual patients, is also propelling the market forward. Furthermore, the integration of artificial intelligence and machine learning is enhancing diagnostic accuracy and efficiency, leading to improved patient outcomes. The market is also benefiting from the rapid adoption of point-of-care testing and the emergence of infectious diseases, which necessitate quick and accurate diagnostic solutions.

Artificial Intelligence (AI) is revolutionizing the diagnostic antibodies market by enhancing the precision, speed, and efficiency of diagnostic processes. AI algorithms can analyze vast datasets to identify patterns and correlations that may not be apparent to human researchers. This capability is particularly beneficial in the development and optimization of diagnostic antibodies, where understanding complex biological interactions is crucial.

One significant application of AI is in the prediction of antibody-antigen interactions. By leveraging machine learning models trained on extensive datasets of known interactions, researchers can predict the binding affinity of new antibodies, thereby streamlining the development process. This predictive capability reduces the reliance on time-consuming and costly laboratory experiments.

AI is also instrumental in the personalization of diagnostics. By analyzing individual patient data, AI can help in designing diagnostic antibodies tailored to detect specific biomarkers unique to a patient's condition. This personalization enhances the accuracy of diagnostics and enables early detection of diseases.

Furthermore, AI-driven automation in laboratories is increasing throughput and reducing human error. Automated systems can handle repetitive tasks such as sample preparation and data analysis, freeing up researchers to focus on more complex aspects of diagnostic development.

In summary, AI is transforming the diagnostic antibodies market by improving the accuracy and efficiency of diagnostics, enabling personalized medicine, and accelerating the development of new diagnostic tools.

“In November 2024, Antiverse, a Cardiff-based biotech company, announced a partnership with Japan's Nxera to apply AI-designed antibodies in drug development. Antiverse utilizes AI to design antibodies that can attach to difficult targets in the body, moving from traditional trial-and-error methods to more precise drug design. This approach aims to reduce the time and cost associated with bringing new drugs to market, which traditionally can take up to 15 years and cost between $1 to $2 billion. By analyzing vast datasets, AI allows for faster identification of targets, prediction of molecular behaviors, and optimization of clinical trials, potentially reducing late-stage failures.”

The increasing emphasis on personalized medicine is a significant driver of the diagnostic antibodies market. Personalized medicine involves tailoring medical treatment to the individual characteristics of each patient, which requires precise diagnostic tools to identify specific biomarkers. Diagnostic antibodies play a crucial role in detecting these biomarkers, enabling healthcare providers to select the most effective treatments. The growing prevalence of chronic diseases and the need for early detection and targeted therapy are fueling the demand for diagnostic antibodies in personalized medicine.

The development of diagnostic antibodies is a complex and expensive process, involving extensive research, clinical trials, and regulatory approvals. These high costs can be a significant barrier, particularly for small and medium-sized enterprises. Additionally, the need for specialized equipment and skilled personnel further adds to the expenses. These financial challenges can limit the entry of new players into the market and slow down the development of innovative diagnostic solutions.

The integration of AI and machine learning presents substantial opportunities in the diagnostic antibodies market. These technologies can enhance the accuracy and efficiency of diagnostic processes by analyzing large datasets to identify patterns and predict outcomes. AI can accelerate the development of diagnostic antibodies by predicting antibody-antigen interactions and optimizing antibody design. Furthermore, machine learning algorithms can assist in personalizing diagnostics based on individual patient data, leading to more effective treatments. The adoption of AI and machine learning is expected to drive innovation and growth in the diagnostic antibodies market.

The diagnostic antibodies market faces challenges related to regulatory and ethical considerations. The development and use of diagnostic antibodies must comply with stringent regulatory standards to ensure safety and efficacy. Navigating these regulatory pathways can be time-consuming and costly. Additionally, ethical concerns regarding patient data privacy and the use of AI in diagnostics need to be addressed. Ensuring compliance with regulations and addressing ethical issues are critical for the successful development and adoption of diagnostic antibodies.

Advancements in Nanotechnology: The integration of nanotechnology in diagnostic antibodies is enhancing the sensitivity and specificity of diagnostic tests. Nanoparticles can be engineered to bind selectively to specific biomarkers, improving the detection of diseases at early stages. This advancement is particularly beneficial in cancer diagnostics, where early detection is crucial for effective treatment.

Development of Multiplex Assays: There is a growing trend towards the development of multiplex assays that can detect multiple biomarkers simultaneously. These assays increase the efficiency of diagnostics by providing comprehensive information from a single test. The use of diagnostic antibodies in multiplex assays is expanding their applications in various disease areas, including infectious diseases and autoimmune disorders.

Point-of-Care Testing (POCT): The demand for rapid and decentralized diagnostic solutions is driving the adoption of point-of-care testing. Diagnostic antibodies are integral to POCT devices, enabling real-time testing at the bedside or in remote settings. This trend is improving patient management and healthcare delivery efficiency, particularly in resource-limited settings.

Automation and Digitalization: The automation and digitalization of diagnostic processes are enhancing the throughput and reliability of diagnostic tests. Automated systems utilizing diagnostic antibodies are reducing human error and increasing the consistency of test results. Digital platforms are also facilitating the integration of diagnostic data into electronic health records, improving patient care and data analysis capabilities.

The Diagnostic Antibodies Market is segmented based on type, application, and end-user, each offering unique insights into growth opportunities and market behavior. This segmentation provides a granular understanding of where the market is headed and which segments are outperforming others. Each category plays a critical role in shaping market dynamics, as diagnostic antibodies continue to be essential tools in medical diagnostics, especially with the rise of personalized healthcare and real-time disease detection. While certain segments dominate in terms of revenue, others are emerging rapidly, propelled by technological innovation, disease prevalence, and evolving healthcare infrastructure across different regions.

The Diagnostic Antibodies Market includes monoclonal antibodies, polyclonal antibodies, and others. Among these, monoclonal antibodies hold the largest market share due to their high specificity, consistency, and reproducibility in diagnostic applications. These antibodies are extensively used in diagnostics for cancer, infectious diseases, and autoimmune conditions. Monoclonal antibodies enable precise detection of biomarkers, which makes them ideal for use in clinical laboratories and imaging techniques.

On the other hand, polyclonal antibodies are witnessing the fastest growth rate, particularly in developing countries. Their cost-effectiveness and ease of production make them suitable for rapid test kits and emerging disease diagnostics. These antibodies are widely used in ELISA, immunohistochemistry, and Western blot assays, where broader antigen recognition is beneficial.

The “others” category includes recombinant antibodies and hybrid antibodies. Although currently niche, these are gaining traction due to ongoing innovations in antibody engineering and recombinant DNA technology, offering a balance between monoclonal specificity and polyclonal sensitivity.

Key application areas of diagnostic antibodies include oncology, infectious diseases, cardiology, autoimmune disorders, and others. Oncology is the leading segment owing to the global rise in cancer prevalence and the critical role antibodies play in tumor marker detection and therapeutic monitoring. The demand for early cancer detection and monitoring is consistently driving the use of diagnostic antibodies in both clinical and research settings.

Infectious diseases represent the fastest-growing segment, primarily fueled by the increasing occurrence of pandemics, outbreaks, and antimicrobial resistance. Antibody-based diagnostics offer high sensitivity and specificity, making them essential for detecting pathogens like SARS-CoV-2, HIV, Hepatitis, and Dengue in low-resource and high-volume testing environments.

Other applications like cardiology and autoimmune disorders continue to gain traction, especially with increased investment in biomarker discovery and point-of-care diagnostic solutions. The integration of antibodies in these domains improves diagnostic accuracy and enables timely clinical intervention, further enhancing patient outcomes.

The major end users in the Diagnostic Antibodies Market include hospitals & clinics, diagnostic laboratories, academic & research institutes, and others. Hospitals and clinics account for the largest market share, primarily due to their role in providing comprehensive diagnostics for in-patient and emergency care. These facilities utilize diagnostic antibodies for routine testing and advanced imaging, ensuring fast and accurate diagnostics essential for patient management.

Diagnostic laboratories are emerging as the fastest-growing end-user segment, particularly driven by the increasing demand for centralized laboratory services and reference lab collaborations. These facilities focus heavily on high-throughput and automation-based testing, often integrating AI tools to manage large volumes of antibody-based tests efficiently.

Academic and research institutes play a significant role in early-stage innovation, assay development, and clinical validation of new antibodies. While they represent a smaller share in terms of revenue, their contributions are essential for market innovation.

The “others” category includes home testing services and veterinary labs, which are expanding rapidly as the awareness around preventive healthcare and zoonotic disease diagnostics continues to grow.

North America accounted for the largest market share at 42.8% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

This regional variation reflects differences in healthcare infrastructure, disease prevalence, R&D investments, and access to diagnostics. North America's dominance is supported by its strong biotechnology ecosystem and early adoption of innovative diagnostic solutions. Meanwhile, Asia-Pacific’s growth is driven by increasing healthcare expenditure, rising awareness of early disease detection, and growing investment in diagnostic research. Europe, South America, and the Middle East & Africa are also witnessing consistent advancements and infrastructure development contributing to market expansion.

Precision Diagnostics Fueling Market Dominance

North America remains the largest contributor to the global diagnostic antibodies market, with the United States alone accounting for over 35% of the global revenue share in 2024. The region benefits from a strong network of diagnostic laboratories, advanced healthcare facilities, and continuous innovation in antibody-based technologies. High incidence rates of chronic illnesses such as cancer, diabetes, and cardiovascular diseases increase the demand for early and accurate diagnostics. The U.S. Food and Drug Administration's active role in approving innovative antibody-based diagnostic tests has also supported market momentum. Canada, with its expanding biotech sector and investment in infectious disease diagnostics, is showing promising growth.

Integration of AI and Point-of-Care Diagnostics in Western Europe

Europe represents a significant portion of the market, accounting for approximately 27.6% of the global revenue in 2024. Germany, France, and the U.K. lead the regional market owing to advanced healthcare systems and a high concentration of diagnostic equipment manufacturers. The region is at the forefront of integrating AI in antibody-based diagnostic platforms, especially in oncology and neurodegenerative disease screening. There is also increased demand for decentralized, rapid testing solutions across hospitals and clinics. Eastern European countries are also experiencing moderate growth due to investments in healthcare digitization and improved laboratory infrastructures.

Rising Healthcare Infrastructure and Investment in Diagnostics

Asia-Pacific is the fastest-growing region in the diagnostic antibodies market, with countries like China, India, and Japan driving the momentum. The region accounted for nearly 18.5% of the market share in 2024 and is experiencing significant expansion due to rising healthcare awareness, increasing burden of infectious and chronic diseases, and growing urbanization. In China, government-led initiatives for healthcare reform and innovation in biotech have fueled growth in diagnostics. India is seeing increased demand for rapid testing kits and personalized diagnostics, especially in rural areas. Japan maintains a strong R&D ecosystem focused on precision medicine and next-generation diagnostics.

Expanded Access to Diagnostic Services in Emerging Economies

South America accounted for about 6.1% of the global diagnostic antibodies market share in 2024. Brazil leads the regional market due to its extensive network of public health laboratories and rising government focus on disease surveillance and immunodiagnostics. The increasing prevalence of infectious diseases such as Zika, Dengue, and Chikungunya is prompting the need for effective antibody-based testing. Argentina and Chile are also expanding access to diagnostic technologies, particularly in underserved communities. Private-public partnerships are helping bridge gaps in diagnostic coverage, further supporting market penetration.

Growing Demand for Infectious Disease Diagnostics in Developing Regions

The Middle East & Africa region held around 5.0% of the global market in 2024. While still emerging, the market is gaining traction due to rising healthcare investments, especially in the Gulf Cooperation Council (GCC) countries. The growing need for accurate diagnostics in areas impacted by infectious diseases such as malaria, tuberculosis, and HIV is a significant market driver. South Africa and Saudi Arabia are the most prominent markets in the region, benefiting from growing urban healthcare networks and increased collaboration with international biotech companies. Diagnostic antibody usage is steadily rising as healthcare infrastructure becomes more sophisticated across urban and semi-urban areas.

United States – USD 870.5 Million, leading due to advanced diagnostics infrastructure, high chronic disease burden, and continuous R&D in antibody-based technologies.

China – USD 510.2 Million, rising rapidly due to government investment in healthcare, expansion of diagnostic labs, and increased prevalence of infectious diseases.

The global Diagnostic Antibodies Market is marked by intense competition with companies racing to develop highly specific and sensitive antibody-based diagnostics. Market leaders are actively investing in expanding their product portfolios and leveraging strategic collaborations to maintain a competitive edge. Innovation in monoclonal and polyclonal antibody production, along with enhanced validation protocols, is enabling firms to deliver precise diagnostic solutions across multiple therapeutic areas. Growth is especially evident in infectious disease diagnostics, oncology markers, and autoimmune disease panels. Furthermore, several companies are focusing on integrating diagnostic antibodies with point-of-care technologies, improving access to testing in both clinical and non-clinical settings. The market is also witnessing a shift toward multiplex testing formats and digital immunoassays, which support faster, more accurate results. Companies are emphasizing regulatory compliance, automated manufacturing, and high-throughput screening methods to meet rising global demand and ensure product quality. As a result, the industry is transitioning toward innovation-driven and patient-centric diagnostics solutions.

Abbott Laboratories

Thermo Fisher Scientific

Danaher Corporation

Bio-Rad Laboratories

Siemens Healthineers

F. Hoffmann-La Roche Ltd.

Agilent Technologies, Inc.

Abcam plc

Boehringer Ingelheim International GmbH

Aytu BioScience, Inc.

Technology is at the core of advancements in the Diagnostic Antibodies Market. The integration of next-generation sequencing (NGS), digital PCR, and flow cytometry has revolutionized the way antibodies are produced, validated, and applied. These innovations have dramatically improved specificity, sensitivity, and reproducibility, allowing for earlier and more accurate diagnosis of diseases such as cancer, HIV, hepatitis, and autoimmune disorders. Robotic automation in laboratory workflows has significantly enhanced throughput and reduced time-to-results in diagnostic antibody development.

Artificial Intelligence (AI) and machine learning algorithms are accelerating antibody discovery and epitope mapping. AI is being used to predict optimal antibody-antigen interactions and eliminate low-affinity candidates early in the pipeline. Bioinformatics tools are further supporting target identification and validation. Point-of-care testing (POCT) is another technological frontier. Handheld devices using antibody-based biosensors are enabling rapid diagnostics in non-laboratory settings, with growing adoption in rural clinics and emergency departments. Additionally, microfluidic devices combined with antibody assays are improving sample processing efficiency and reducing reagent consumption.

Miniaturized, high-throughput platforms that allow for simultaneous detection of multiple biomarkers are seeing increasing demand in clinical diagnostics. These advancements are enhancing the applicability of diagnostic antibodies in precision medicine, enabling stratified treatment strategies based on biomarker profiles. The diagnostic industry is rapidly moving toward digitized, decentralized, and real-time testing enabled by cutting-edge antibody-based technologies.

In January 2023, Creative Diagnostics launched over 1,000 new antibody targets, including various conjugated formats, expanding its monoclonal antibody capabilities for global diagnostics customers.

In May 2023, Versiti introduced a novel Anti-Von Willebrand Factor (VWF) Antibody Assay to assist clinicians in identifying patients suspected of acquired von Willebrand Disease (aVWD), enhancing autoimmune diagnostic capabilities.

In June 2023, EUROIMMUN released the 'UNIQO 160' automated IIFT system, streamlining the diagnosis of autoimmune disorders through improved throughput and standardization.

In March 2023, Trinity Biotech unveiled the Autoimmune Panel Plus, a comprehensive diagnostic tool offering higher sensitivity and accuracy for detecting a broad range of autoimmune diseases.

The Diagnostic Antibodies Market Report provides a detailed exploration of industry trends, product innovation, and market performance across geographies and segments. The report offers a granular analysis of diagnostic antibody types including monoclonal and polyclonal antibodies, and how these are being adopted in applications such as infectious disease testing, cancer detection, and autoimmune disease diagnostics. It evaluates market dynamics influenced by growing healthcare awareness, increasing disease prevalence, and demand for faster diagnostic results.

The scope includes assessment of end-users such as hospitals, diagnostic laboratories, and research institutions, with insights into purchasing behaviors and regional demand patterns. Emerging technologies like AI-assisted antibody development, high-throughput screening, and POCT integration are also evaluated. The competitive landscape is mapped by profiling major players, recent mergers and product launches, and innovation pipelines.

In addition to current trends, the report highlights growth potential across developing regions and identifies key opportunities linked to decentralized testing and personalized medicine. It serves as a critical tool for decision-makers seeking actionable insights into technological innovations, regulatory considerations, and future prospects of the global Diagnostic Antibodies Market.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Diagnostic Antibodies Market |

| Market Revenue (2024) | USD 2,997.0 Million |

| Market Revenue (2032) | USD 4,740.8 Million |

| CAGR (2025–2032) | 5.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Abbott Laboratories, Thermo Fisher Scientific, Danaher Corporation, Bio-Rad Laboratories, Siemens Healthineers, F. Hoffmann-La Roche Ltd., Agilent Technologies, Inc., Abcam plc, Boehringer Ingelheim International GmbH, Aytu BioScience, Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |