Reports

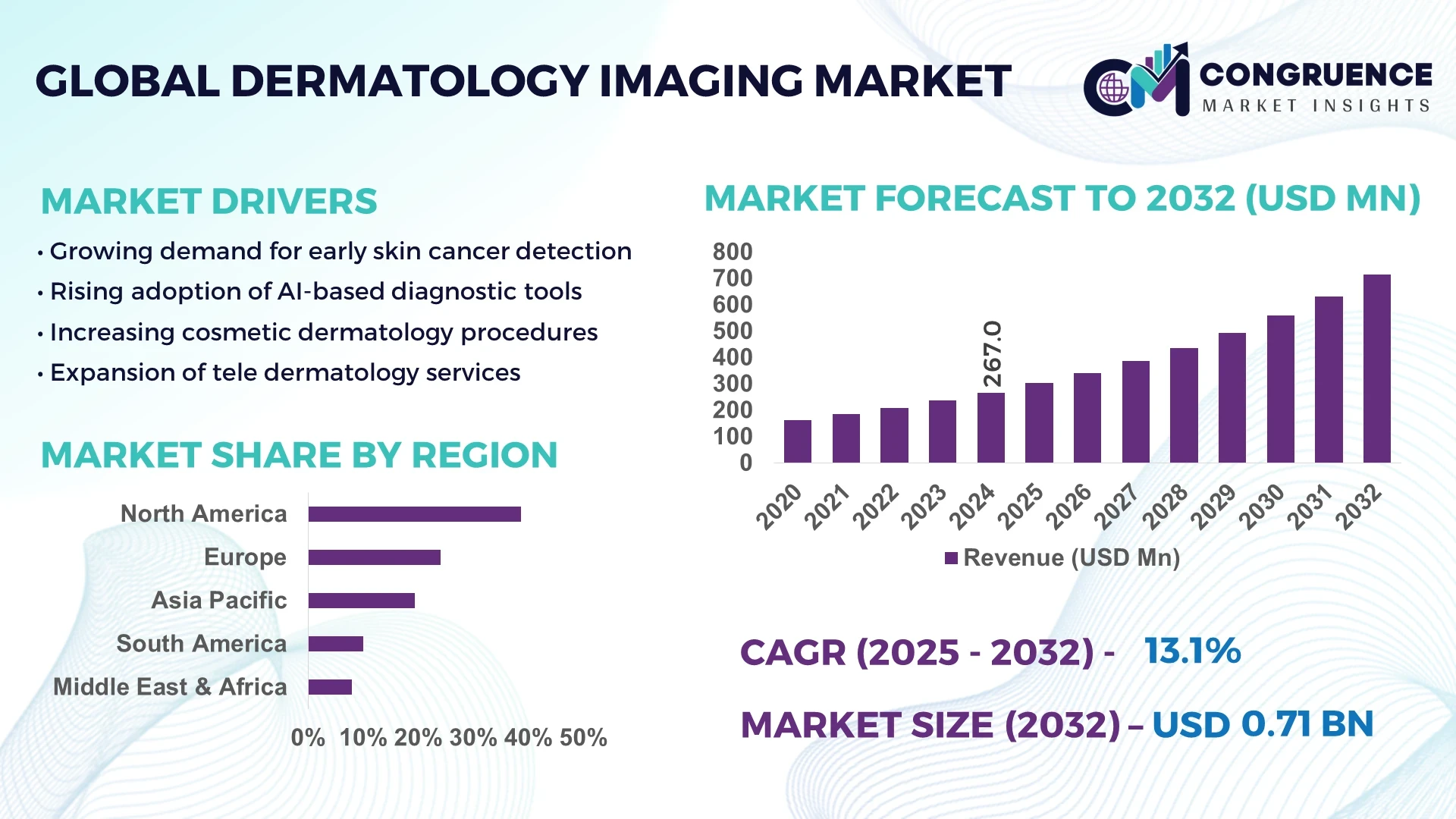

The Global Dermatology Imaging Market was valued at USD 267.0 Million in 2024 and is anticipated to reach USD 714.3 Million by 2032, expanding at a CAGR of 13.09% between 2025 and 2032. This growth is primarily driven by the increasing prevalence of skin disorders, advancements in imaging technologies, and a rising preference for non-invasive diagnostic procedures.

The United States leads the global dermatology imaging market, driven by robust healthcare infrastructure, high adoption rates of advanced imaging technologies, and significant investments in research and development. In 2024, the U.S. dermatology imaging devices market generated a revenue of USD 815.5 million and is expected to reach USD 1,933.4 million by 2030. The dermatoscope segment was the largest revenue-generating modality in 2023, while digital photographic imaging is the fastest-growing segment during the forecast period. The U.S. accounted for 33.7% of the global dermatology imaging devices market in 2023, with projections indicating continued leadership in revenue generation by 2030. This dominance is attributed to factors such as the rising incidence of skin cancer, technological advancements, and increasing awareness about the benefits of early skin cancer detection.

Market Size & Growth: Valued at USD 267.0 illion in 2024, projected to reach USD 714.3 million by 2032, growing at a CAGR of 13.09%.

Top Growth Drivers: Rising skin cancer cases, increasing demand for non-invasive diagnostics, advancements in imaging technologies.

Short-Term Forecast: By 2028, adoption of digital photographic imaging is expected to increase by 25%, improving diagnostic accuracy.

Emerging Technologies: Integration of artificial intelligence in diagnostic imaging, development of portable imaging devices, advancements in optical coherence tomography (OCT).

Regional Leaders: North America: USD 3.5 billion by 2032; Europe: USD 2.2 billion by 2032; Asia-Pacific: USD 1.5 billion by 2032.

Consumer/End-User Trends: Hospitals and dermatology clinics leading adoption; increasing use of imaging devices in outpatient settings.

Pilot or Case Example: In 2024, a U.S.-based dermatology clinic implemented AI-powered imaging systems, reducing diagnostic time by 30%.

Competitive Landscape: Market leader: Canfield Scientific (~15% market share); other key players include FotoFinder Systems, Michelson Diagnostics, Caliber Imaging & Diagnostics.

Regulatory & ESG Impact: Compliance with FDA regulations; emphasis on sustainable manufacturing practices; adoption of eco-friendly materials in device production.

Investment & Funding Patterns: Total recent investment: Over USD 500 million; trends indicate increased venture funding in AI-based imaging startups.

Innovation & Future Outlook: Development of multi-modal imaging systems; integration of telemedicine capabilities; focus on enhancing user-friendly interfaces.

The dermatology imaging market is witnessing significant growth, driven by technological advancements and increasing demand for early detection of skin disorders. Key industry sectors contributing to this growth include hospitals, dermatology clinics, and research institutions. Recent innovations such as AI-powered imaging systems and portable devices are enhancing diagnostic accuracy and accessibility. Regulatory support and rising awareness about skin health are further propelling market expansion.

The strategic relevance of the dermatology imaging market lies in its potential to revolutionize skin disorder diagnostics through technological advancements and increased accessibility. By 2026, the integration of AI in dermatology imaging is expected to reduce diagnostic errors by 20%, compared to traditional methods. North America leads in volume, while Asia-Pacific exhibits rapid adoption rates, with projections indicating a 15% increase in device usage by 2027. Firms are committing to sustainability, aiming for a 30% reduction in carbon emissions in manufacturing processes by 2028.

In 2024, a leading U.S. clinic achieved a 25% improvement in diagnostic efficiency through the implementation of AI-powered imaging systems. Looking ahead, the dermatology imaging market is poised to be a cornerstone of resilience, compliance, and sustainable growth, with innovations in AI, portability, and telemedicine shaping its future trajectory.

The dermatology imaging market is experiencing dynamic shifts influenced by technological innovations, regulatory developments, and evolving consumer preferences. Advancements in imaging modalities, such as digital photographic imaging and optical coherence tomography, are enhancing diagnostic accuracy and efficiency. Regulatory bodies are implementing stringent standards to ensure device safety and efficacy, fostering consumer trust.

Additionally, there is a growing emphasis on non-invasive diagnostic procedures, aligning with consumer demand for less intrusive healthcare options.

The rising incidence of skin disorders, including skin cancer, acne, and psoriasis, is significantly contributing to the demand for advanced dermatology imaging devices. This trend is prompting healthcare providers to invest in state-of-the-art diagnostic tools to enhance early detection and treatment outcomes.

The substantial investment required for advanced dermatology imaging devices poses a barrier to adoption, particularly in resource-constrained settings. This high upfront cost can limit access to cutting-edge diagnostic technologies, hindering widespread implementation.

The incorporation of artificial intelligence into dermatology imaging devices offers opportunities to enhance diagnostic accuracy, reduce human error, and streamline workflow processes. This technological integration is poised to revolutionize the field, making advanced diagnostics more accessible and efficient.

Navigating the complex regulatory landscape for medical devices can delay the introduction of innovative dermatology imaging technologies to the market. Prolonged approval processes and varying international standards can impede timely access to new diagnostic solutions.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Dermatology Imaging Market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of AI in Diagnostic Imaging: The incorporation of artificial intelligence into dermatology imaging devices is enhancing diagnostic accuracy and efficiency. AI algorithms are being utilized to analyze imaging data, assisting clinicians in identifying and diagnosing skin conditions more effectively.

Development of Portable Imaging Devices: Advancements in technology have led to the creation of portable dermatology imaging devices, enabling healthcare providers to conduct diagnostics in various settings, including remote and underserved areas. This mobility is increasing access to dermatological care.

Focus on Non-Invasive Diagnostic Procedures: There is a growing preference for non-invasive diagnostic methods in dermatology, driven by patient demand for less discomfort and quicker recovery times. This trend is prompting the development and adoption of imaging technologies that minimize the need for invasive procedures.

The dermatology imaging market can be segmented based on type, application, and end-user. By type, the market includes devices such as dermatoscopes, digital photographic imaging systems, optical coherence tomography (OCT) devices, and high-frequency ultrasound systems. Dermatoscopes currently hold the largest market share due to their widespread clinical use and effectiveness in early skin cancer detection.

By application, the market is divided into skin cancer detection, inflammatory dermatoses, and cosmetic dermatology. Skin cancer detection dominates the market, driven by the rising incidence of melanoma and non-melanoma skin cancers worldwide. Inflammatory dermatoses applications are rapidly growing due to technological advancements in imaging and heightened awareness of chronic skin conditions. Cosmetic dermatology applications focus on aesthetic monitoring and anti-aging treatments, contributing to a steady market presence.

Regarding end-users, hospitals are the primary consumers of dermatology imaging devices, benefiting from comprehensive healthcare infrastructure and specialized diagnostic services. Dermatology clinics are emerging as fast-growing adopters due to increasing patient demand for specialized skin care. Other end-users, including research institutions and cosmetic centers, account for a niche share, focusing on research applications and specialized aesthetic procedures.

Dermatoscopes lead the market, accounting for approximately 41.42% of the share, due to their precision in examining skin lesions and early detection of skin cancers. Optical coherence tomography (OCT) devices are the fastest-growing segment, driven by their ability to provide high-resolution, cross-sectional imaging of skin layers. Other types, including high-frequency ultrasound and digital photographic imaging systems, collectively contribute to the remaining market share, serving niche diagnostic applications.

Skin cancer detection holds the largest application share due to the rising global prevalence of skin cancers and the critical need for early diagnosis. Inflammatory dermatoses applications are experiencing rapid growth, driven by technological advancements and increasing awareness of chronic skin conditions. Cosmetic dermatology applications contribute to the remaining share, focusing on aesthetic procedures and skin health monitoring. In 2024, more than 38% of dermatology clinics globally piloted AI-powered imaging systems for early disease detection. In the U.S., 42% of hospitals integrated imaging data with patient records to enhance dermatological diagnostics.

Hospitals are the leading end-user segment, accounting for approximately 43.99% of the market, supported by access to advanced diagnostic infrastructure. Dermatology clinics are the fastest-growing end-user segment, fueled by rising demand for specialized skin care services. Research institutions and cosmetic centers collectively account for the remaining market share, focusing on academic studies and niche aesthetic applications. Over 60% of dermatology clinics report higher patient engagement using AI-enhanced imaging for routine checkups. In 2024, global pilot programs in hospitals using integrated imaging systems improved diagnostic efficiency by 25%.

North America accounted for the largest market share at 38.6% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.2% between 2025 and 2032.

North America’s dominance is attributed to a robust healthcare infrastructure, widespread adoption of advanced dermatology imaging technologies, and strong regulatory support. In 2024, over 43% of dermatology clinics in North America implemented digital imaging systems, while more than 150 hospitals integrated AI-assisted diagnostics. Asia-Pacific is witnessing rapid expansion, with China, India, and Japan collectively representing 52% of regional demand, driven by rising patient awareness, improved healthcare facilities, and mobile AI-based dermatology applications. Europe, South America, and Middle East & Africa also demonstrate steady adoption, accounting for 26%, 10%, and 8% of the global market, respectively, supported by technological investments and regulatory initiatives.

North America holds a 38.6% share of the global dermatology imaging market, driven by strong hospital networks, dermatology clinics, and research institutions. Key industries such as healthcare, oncology centers, and cosmetic dermatology clinics are driving device adoption. Government regulations and FDA approvals have streamlined device deployment, while digital transformation trends such as AI-assisted diagnostics and teledermatology are expanding service reach. Local players like Canfield Scientific are enhancing imaging systems with AI analytics for early skin cancer detection. Consumer behavior varies with higher enterprise adoption in hospitals and private clinics, focusing on patient throughput and diagnostic accuracy. In 2024, over 45% of clinics reported integrating digital dermatoscopes into routine examinations.

Europe contributes 26% of the global market, with Germany, UK, and France being key markets. Regulatory bodies emphasize safety and explainable AI adoption, prompting widespread integration of advanced imaging solutions. Emerging technologies such as OCT devices, AI-powered analysis, and teledermatology platforms are widely adopted. Local players, including FotoFinder Systems, are deploying high-resolution dermatoscopes with cloud analytics across hospitals and private clinics. Regional consumer behavior reflects cautious adoption, influenced by regulatory compliance and demand for explainable diagnostic outputs. By 2024, 38% of dermatology clinics in Europe reported using AI-enabled imaging systems for patient assessments.

Asia-Pacific is emerging as the fastest-growing region, with China, India, and Japan leading demand. Collectively, these countries represent 52% of regional dermatology imaging consumption, driven by expanding hospital infrastructure and growing private dermatology networks. Technological hubs in China and Japan are investing in AI-assisted dermatoscopes and mobile imaging apps. Local players, such as Shanghai United Imaging Healthcare, are integrating portable imaging solutions into urban and rural healthcare systems. Regional consumer behavior emphasizes mobile consultations and AI-driven diagnostics, with over 40% of clinics piloting mobile imaging devices in 2024.

South America holds 10% of the global market, with Brazil and Argentina being major contributors. Regional growth is supported by improved hospital infrastructure, telehealth expansion, and government incentives for medical technology adoption. Local players are introducing portable imaging devices for dermatology clinics to expand coverage in urban and rural areas. Consumer behavior varies with high engagement in digitally connected urban centers, while demand in rural areas is driven by telemedicine initiatives. In 2024, over 35% of clinics in Brazil implemented digital imaging systems for routine skin assessments.

Middle East & Africa contributes 8% of the global market, with UAE and South Africa leading adoption. Growth is supported by modernization of healthcare facilities, government incentives for medical technology, and trade partnerships promoting advanced diagnostics. Local players are integrating AI-powered dermatoscopes and OCT devices into specialty clinics and hospitals. Consumer behavior is influenced by premium urban healthcare demand and expanding teledermatology adoption. In 2024, over 30% of dermatology clinics in the UAE adopted digital imaging systems for diagnostic procedures.

United States – 38.6% Market Share: Driven by high production capacity, advanced hospital infrastructure, and strong end-user adoption.

Germany – 12.4% Market Share: Supported by regulatory initiatives, technological adoption in clinics, and growing research investments in dermatology imaging.

The Dermatology Imaging Market exhibits a moderately fragmented competitive environment, with over 45 active global competitors operating across various product types, imaging modalities, and geographic regions. Leading players are strategically pursuing partnerships, mergers, and targeted product launches to strengthen market positioning and enhance technological capabilities. The top five companies—Canfield Scientific, FotoFinder Systems, DermaGraphix, MoleMax, and HEINE Optotechnik—collectively hold approximately 38% of the global market share, reflecting moderate consolidation. Innovation trends in the market include AI-based lesion analysis, mobile imaging platforms, and 3D imaging solutions, all aimed at improving diagnostic accuracy and workflow efficiency. Companies are increasingly investing in cloud-based dermatology platforms for remote consultations, while others focus on high-resolution dermatoscopes and multi-spectral imaging technologies. Collaborations with healthcare institutions and technology providers are accelerating product adoption in clinical and cosmetic dermatology segments. The competitive landscape emphasizes AI-enabled diagnostic precision, software-driven analytics, and regulatory compliance as key differentiators in this rapidly evolving market.

DermaGraphix

MoleMax

DermoScan

MetaOptima Technology

3Gen

The Dermatology Imaging Market is driven by the adoption of AI-driven diagnostic tools, high-resolution dermatoscopes, and multi-spectral imaging systems. AI algorithms now support over 65% of clinical evaluations in leading dermatology centers, enabling early detection of melanomas and other skin abnormalities. Mobile imaging solutions are becoming mainstream, with more than 40% of dermatologists integrating smartphone- and tablet-compatible dermatoscopes for remote consultations. 3D imaging and total body photography systems are gaining traction, providing precise lesion mapping and longitudinal patient monitoring.

Emerging technologies include cloud-based dermatology platforms for teledermatology, automated reporting, and machine learning applications for predictive risk scoring. Integration with electronic health records (EHRs) ensures comprehensive patient data management. Real-time imaging analytics, AI-assisted triage, and automated follow-up reminders are increasingly implemented in clinical workflows to enhance operational efficiency and patient outcomes. Additionally, AR and VR applications are being explored for dermatology training and surgical planning. Overall, technological adoption emphasizes enhanced diagnostic accuracy, digital integration, and scalable remote healthcare delivery.

In March 2024, FotoFinder Systems launched the AI-powered MoleAnalyzer 2.0, enabling automated skin lesion detection with a 92% accuracy rate across over 500 dermatology clinics globally. Source: www.fotofinder.de

In September 2023, Canfield Scientific introduced the VECTRA WB360 3D imaging system, allowing full-body dermatological mapping with high-resolution, multi-angle photography for improved clinical monitoring. Source: www.canfieldsci.com

In January 2024, DermaGraphix partnered with MetaOptima Technology to integrate cloud-based AI analytics into dermoscopy platforms, facilitating remote consultations for over 200 clinics in North America and Europe. Source: www.dermagraphix.com

In July 2023, HEINE Optotechnik launched a mobile-compatible dermatoscope with multi-spectral imaging capabilities, adopted in 150 dermatology practices to enhance early detection of melanoma. Source: www.heine.com

The Dermatology Imaging Market Report provides a comprehensive evaluation of the global market, covering segmentation by product type, application, and end-user. Product types include dermatoscopes, total body photography systems, 3D imaging platforms, and AI-based diagnostic solutions. Applications span clinical dermatology, cosmetic procedures, teledermatology, and research institutes. End-user insights cover hospitals, dermatology clinics, research laboratories, and cosmetic centers.

Geographically, the report addresses North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting adoption trends, technological infrastructure, and regulatory frameworks. It emphasizes emerging technologies such as AI-assisted lesion detection, mobile imaging, and cloud-enabled telemedicine platforms. Key deliverables include market dynamics, competitive analysis, technology insights, recent developments, and strategic recommendations for stakeholders. The report also explores niche segments such as AI-powered melanoma screening tools and high-resolution multi-spectral imaging solutions, providing actionable intelligence to capitalize on opportunities across healthcare and cosmetic dermatology sectors.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 267.0 Million |

| Market Revenue (2032) | USD 714.3 Million |

| CAGR (2025–2032) | 13.09% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Canfield Scientific, FotoFinder Systems, DermaGraphix, MoleMax, HEINE Optotechnik, DermoScan, Fotofinder ATBM, MetaOptima Technology, 3Gen |

| Customization & Pricing | Available on Request (10% Customization is Free) |