Reports

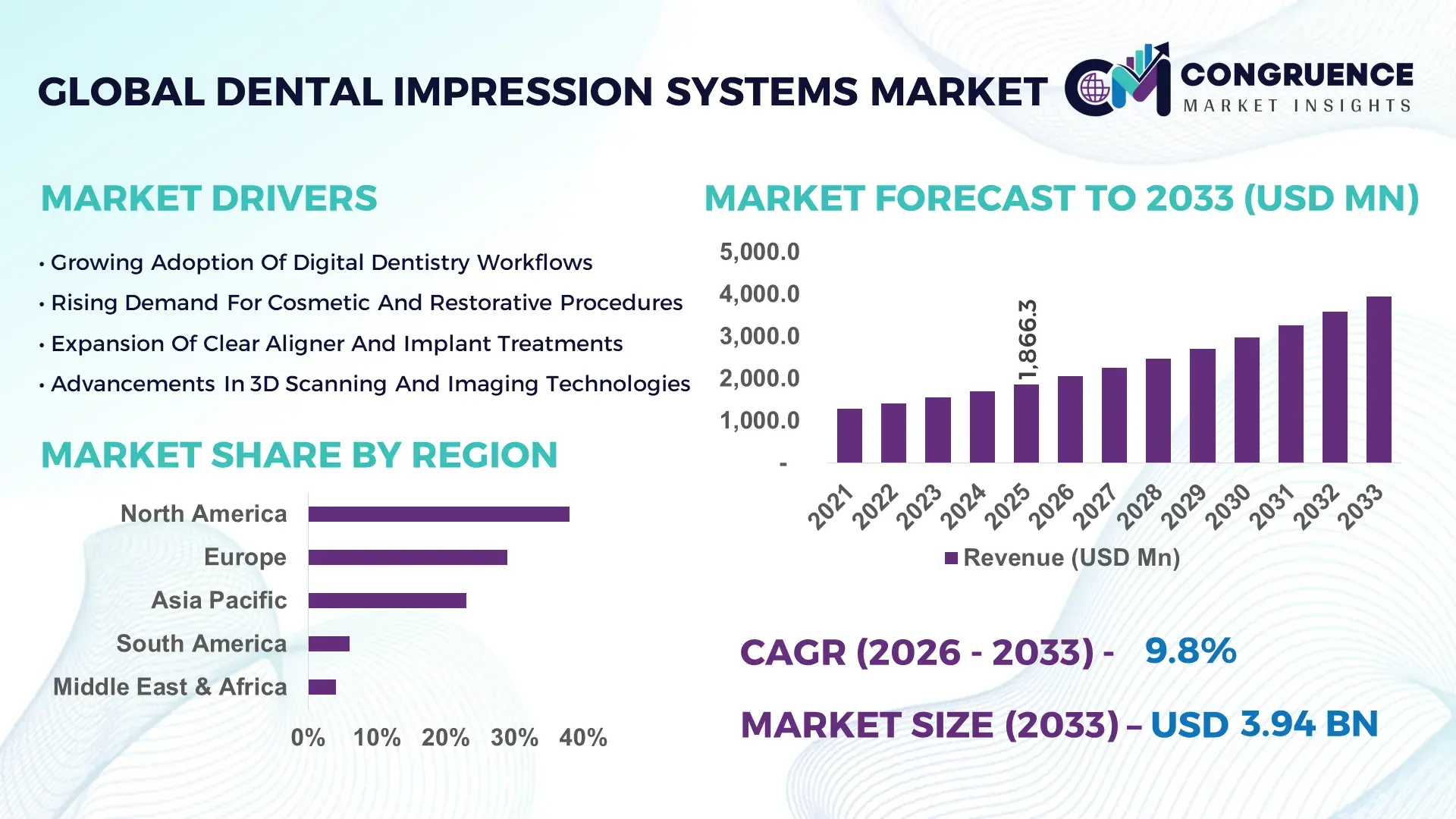

The Global Dental Impression Systems Market was valued at USD 1,866.3 Million in 2025 and is anticipated to reach a value of USD 3,942.8 Million by 2033 expanding at a CAGR of 9.8% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by the rapid adoption of digital dentistry workflows and chairside CAD/CAM integration across restorative procedures.

In the United States, which leads advanced dental technology deployment, more than 202,000 licensed dentists operate across private practices and dental service organizations, with over 47% of clinics equipped with intraoral scanning systems in 2025. Annual investment in dental digitalization exceeded USD 850 million, focusing on high-precision optical scanners and AI-driven impression software. Over 62% of orthodontic laboratories utilize digital impression systems for aligner production, while implantology applications account for nearly 38% of digital workflow usage. Continuous upgrades in 3D imaging accuracy below 20 microns and integration with cloud-based case management platforms reinforce the country’s strong manufacturing and clinical adoption ecosystem.

Market Size & Growth: Valued at USD 1,866.3 Million in 2025 and projected to reach USD 3,942.8 Million by 2033 at 9.8% CAGR, supported by digital dentistry transformation.

Top Growth Drivers: 48% digital workflow adoption increase; 35% faster prosthetic turnaround; 27% rise in cosmetic dentistry procedures.

Short-Term Forecast: By 2028, AI-integrated scanning systems are expected to reduce impression errors by 22%.

Emerging Technologies: AI-driven margin detection, cloud-based CAD integration, and high-resolution 3D optical scanning.

Regional Leaders: North America projected at USD 1,210 Million by 2033; Europe USD 1,060 Million; Asia-Pacific USD 960 Million, driven by orthodontic expansion.

Consumer/End-User Trends: Over 54% of patients prefer digital impressions for improved comfort and reduced chair time.

Pilot Example: In 2024, a large dental chain improved prosthetic accuracy by 18% using AI-assisted intraoral scanners.

Competitive Landscape: Leading player holds approximately 21% share; followed by 3–5 multinational dental equipment manufacturers.

Regulatory & ESG Impact: Increased compliance with sterilization and digital record mandates affecting 60% of new installations.

Investment Patterns: More than USD 1.2 Billion invested globally in dental tech innovation between 2023–2025.

Innovation & Outlook: Integrated digital ecosystems combining scanning, milling, and cloud collaboration are reshaping clinical efficiency.

Dental Impression Systems are widely deployed in restorative dentistry (42%), orthodontics (31%), and implantology (18%), with growing penetration in cosmetic and pediatric dentistry. Recent innovations include wireless handheld scanners, powder-free optical imaging, and AI-powered bite registration tools. Regulatory emphasis on infection control and digital documentation compliance further accelerates system upgrades across developed and emerging dental markets.

The Dental Impression Systems Market holds strategic importance within the broader digital dentistry ecosystem as clinics transition from traditional elastomeric materials to fully digital impression workflows. AI-assisted intraoral scanning delivers 24% faster image capture compared to conventional silicone impressions while reducing remakes by nearly 20%. North America dominates in procedural volume, while Asia-Pacific leads in adoption momentum with over 41% of new dental clinics installing digital scanning units in 2025.

By 2028, AI-driven occlusal analysis and automated margin detection are expected to improve prosthetic fit accuracy by 25%, enhancing patient satisfaction and reducing chairside adjustments. Firms are committing to ESG targets such as 30% reduction in disposable material waste by 2030 through elimination of physical impression trays. In 2024, a European dental network achieved a 19% reduction in turnaround time through cloud-based case collaboration platforms integrated with advanced scanners.

With increasing interoperability between scanning devices and CAD/CAM milling units, the Dental Impression Systems Market is positioned as a core pillar of clinical efficiency, regulatory compliance, and sustainable digital transformation across global dental practices.

The Dental Impression Systems Market is shaped by accelerated digitalization, rising cosmetic dentistry demand, and expanding orthodontic treatments worldwide. Over 3.5 billion individuals globally are affected by oral diseases, stimulating restorative and prosthetic procedures that require high-precision impressions. Traditional impression materials are gradually declining as digital intraoral scanners offer up to 30% faster procedure times and enhanced patient comfort. Dental service organizations account for approximately 36% of large-scale system purchases, reflecting centralized procurement trends. Technological advancements such as real-time 3D rendering and integrated patient record systems improve workflow coordination. However, disparities in reimbursement frameworks and high capital costs continue influencing adoption rates across smaller clinics and developing economies.

Digital dentistry adoption has increased by over 45% in the past five years, significantly driving the Dental Impression Systems market. Intraoral scanning reduces patient discomfort by 32% compared to traditional impression materials. Approximately 58% of restorative procedures in developed markets now utilize digital impressions. Orthodontic aligner demand has expanded by 29%, directly increasing scanner utilization. Cloud-based case sharing shortens laboratory turnaround by 18%, enhancing productivity. Growing aesthetic dentistry procedures, particularly veneers and crowns, account for 34% of digital impression applications. Enhanced imaging resolution below 20 microns further supports precision-driven clinical outcomes, making digital systems an indispensable solution in modern dental practices.

The upfront cost of advanced intraoral scanners ranges between USD 20,000 and USD 45,000 per unit, posing barriers for small and independent practices. Maintenance contracts and software subscription models add 8–12% annual operational expenditure. In developing regions, only 22% of dental clinics have access to digital scanning infrastructure. Limited reimbursement coverage for digital procedures in certain healthcare systems slows investment decisions. Training requirements also impact adoption, as over 30% of practitioners report initial workflow integration challenges. These financial and operational constraints moderate penetration in price-sensitive markets despite long-term efficiency gains.

Global orthodontic case volumes increased by 26% between 2022 and 2025, creating substantial demand for precise digital impressions. Implant procedures account for nearly 14 million cases annually, with digital impression usage improving implant alignment accuracy by 21%. Emerging markets in Asia and Latin America are expanding dental infrastructure, with new clinic openings growing at 9% annually. Teledentistry platforms integrated with digital impression files improve case consultations by 17%. AI-driven predictive modeling enhances treatment planning efficiency by 23%, creating new monetization pathways for advanced Dental Impression Systems providers.

Interoperability constraints between scanners and CAD/CAM systems affect approximately 28% of multi-brand clinical setups. Proprietary software ecosystems restrict seamless data exchange, increasing integration costs by 12–15%. Cybersecurity concerns around cloud-based storage impact nearly 19% of digital dental workflows. Regulatory approvals for advanced AI-assisted tools also extend product commercialization timelines by up to 18 months in certain jurisdictions. Addressing compatibility standards and data protection compliance remains critical to sustaining adoption momentum.

• Accelerated Adoption of AI-Enhanced Intraoral Scanners: Over 52% of newly installed Dental Impression Systems in 2025 feature AI-driven margin detection. Clinics reported a 21% reduction in impression remakes and a 17% improvement in prosthetic fit accuracy, strengthening workflow reliability and patient satisfaction metrics.

• Integration with Chairside CAD/CAM Milling: Approximately 46% of digital impression users now connect scanners directly with in-house milling units. This integration reduces crown fabrication time by 28% and lowers laboratory outsourcing costs by 19%, boosting operational efficiency in high-volume clinics.

• Growth of Wireless and Portable Systems: Wireless scanner adoption increased by 33% between 2023 and 2025, enabling enhanced maneuverability and reducing setup time by 14%. Lightweight handheld devices below 250 grams improve ergonomics and procedural comfort for clinicians.

• Expansion in Emerging Dental Markets: Asia-Pacific clinic digitalization rates rose by 37% in urban centers, while Latin American adoption expanded by 24%. Government-backed dental modernization initiatives improved digital infrastructure coverage by 18%, driving equipment procurement growth.

The Dental Impression Systems Market is segmented by type into traditional impression materials and digital impression systems, with digital systems representing the majority of new installations. Applications span restorative dentistry, orthodontics, implantology, and cosmetic procedures. End-users include dental clinics, dental laboratories, and academic institutions. Digital systems dominate high-value clinical workflows, particularly in prosthetic fabrication and orthodontic aligner production. Regional adoption varies significantly, with developed markets emphasizing full digital integration and emerging markets maintaining hybrid usage models. Growing patient demand for comfort and faster procedures further shapes segmentation dynamics across clinical specialties.

Digital Dental Impression Systems account for approximately 64% of total adoption, supported by improved scanning precision and workflow automation. Traditional elastomeric materials represent 36%, primarily in smaller or cost-sensitive practices. Digital systems demonstrate the fastest expansion at 10.6% CAGR, driven by AI-enabled scanning and cloud collaboration tools. Within digital systems, powder-free optical scanners represent 42% of installations, while laser-based systems hold 22%. Emerging hybrid systems integrating 3D imaging and bite analysis are gaining traction and are expected to surpass 30% penetration by 2033.

Restorative dentistry leads with 44% share of Dental Impression Systems utilization, followed by orthodontics at 31% and implantology at 18%. Cosmetic dentistry is the fastest-growing application at 11.2% CAGR, driven by increased veneer and smile enhancement procedures. Over 39% of clinics globally reported piloting advanced Dental Impression Systems for aesthetic case planning in 2025. Orthodontic aligner treatments increased by 27%, supporting higher scanner demand.

Dental clinics represent 61% of total Dental Impression Systems usage, reflecting direct patient interaction and chairside workflow integration. Dental laboratories account for 27%, primarily for prosthetic modeling and aligner fabrication. Academic and research institutions contribute 12%, supporting training and clinical validation programs. Dental clinics remain the fastest-growing segment at 10.9% CAGR due to digital workflow transformation. Approximately 42% of US-based clinics reported transitioning to fully digital impression processes by 2025.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.4% between 2026 and 2033.

North America recorded over 82,000 digital intraoral scanner installations across dental clinics and laboratories, supported by more than 200,000 practicing dentists and a 47% penetration rate of chairside CAD/CAM systems. Europe held approximately 29% share in 2025, with Germany, the UK, and France collectively representing over 61% of regional demand. Asia-Pacific captured 23% share, driven by more than 18,500 new dental clinic openings between 2023 and 2025, particularly in China and India. South America contributed 6%, with Brazil accounting for nearly 54% of regional digital impression purchases. Middle East & Africa represented 4%, supported by private dental chains expanding at 9% annually. Globally, digital impression systems account for 64% of new equipment investments, while traditional materials continue to serve 36% of practices in cost-sensitive markets.

How Is Advanced Digital Dentistry Infrastructure Driving Market Expansion?

North America Dental Impression Systems Market holds 38% of global volume demand, supported by high digital dentistry penetration and structured reimbursement frameworks. Over 47% of dental clinics operate intraoral scanners, and nearly 52% of restorative procedures utilize digital impressions. Key industries driving demand include dental service organizations, orthodontic aligner manufacturers, and prosthetic laboratories. Regulatory oversight from federal and state health authorities mandates stringent infection control and electronic documentation standards, encouraging digital system adoption.

Technological advancements such as AI-assisted margin detection and cloud-based CAD integration have improved prosthetic accuracy by 21%. A leading regional manufacturer expanded its AI-powered scanner portfolio in 2024, reporting a 19% reduction in impression remakes across pilot clinics. Consumer behavior reflects strong acceptance of digital workflows, with over 54% of patients preferring powder-free scanning for comfort and reduced chair time.

Why Is Regulatory-Driven Digital Transformation Accelerating Adoption?

Europe Dental Impression Systems Market accounts for approximately 29% of global installations. Germany, the UK, and France collectively contribute over 61% of regional equipment demand. Regulatory emphasis on patient data protection and digital documentation has influenced more than 48% of clinics to upgrade to integrated digital impression systems. Sustainability initiatives promoting reduced material waste have accelerated the shift from elastomeric materials to reusable digital scanners.

Adoption of AI-enabled scanning software increased by 34% between 2023 and 2025. A prominent European dental technology provider introduced cloud-synchronized scanner platforms that enhanced laboratory collaboration efficiency by 17%. Consumer behavior indicates strong preference for minimally invasive procedures, with cosmetic dentistry procedures rising by 26% across Western Europe, driving increased scanner utilization.

What Factors Are Powering Rapid Digital Dental Infrastructure Growth?

Asia-Pacific Dental Impression Systems Market ranks second in global volume and demonstrates the fastest expansion trajectory. China, India, and Japan represent more than 68% of regional installations. Over 18,500 new dental clinics were established between 2023 and 2025, and digital scanner adoption in urban centers reached 39%. Infrastructure modernization programs have increased dental equipment imports by 28%.

Regional manufacturing hubs have expanded 3D optical scanner assembly capacity by 22%, supporting cost-effective deployment. A regional dental equipment company launched a lightweight wireless scanner in 2024, improving workflow efficiency by 16% in pilot hospitals. Consumer behavior reflects growing demand for orthodontic aligners, with case volumes rising 31% across metropolitan areas.

How Are Expanding Private Dental Networks Supporting Market Penetration?

South America Dental Impression Systems Market holds approximately 6% of global demand, with Brazil accounting for 54% of regional installations and Argentina contributing 18%. Expansion of private dental chains at 8% annual growth has increased procurement of digital scanning systems. Infrastructure investments in urban healthcare facilities improved equipment availability by 21% between 2023 and 2025.

Government trade agreements reduced import tariffs on medical devices by up to 6%, improving affordability. A regional distributor reported a 14% increase in scanner sales following localized training programs. Consumer demand is influenced by aesthetic dentistry trends, with veneer and aligner treatments increasing 23% across major cities.

Is Healthcare Modernization Enhancing Digital Dentistry Adoption?

Middle East & Africa Dental Impression Systems Market represents around 4% of global installations, led by the UAE and South Africa, which together account for 63% of regional demand. Healthcare modernization initiatives increased private dental clinic capacity by 19% between 2022 and 2025. Technological adoption includes AI-integrated scanning and cloud collaboration platforms, improving prosthetic accuracy by 15%.

Trade partnerships have reduced equipment procurement lead times by 11%. A regional dental technology supplier expanded training centers in 2024, supporting 1,200 clinicians in digital workflow integration. Consumer behavior shows rising preference for premium cosmetic dentistry services, with procedure volumes increasing 18% in metropolitan hubs.

United States – 34% share: Dental Impression Systems Market leadership supported by advanced digital dentistry infrastructure and over 47% clinic-level scanner penetration.

Germany – 12% share: Strong manufacturing base and high adoption of AI-enabled Dental Impression Systems in restorative and orthodontic procedures.

The Dental Impression Systems Market exhibits a moderately consolidated structure, with the top five companies accounting for approximately 58% of global installations. More than 35 active manufacturers operate across digital scanning, impression materials, and CAD/CAM integration solutions. Market leaders focus on AI-driven software upgrades, ergonomic scanner design, and seamless interoperability with laboratory systems.

Strategic initiatives between 2023 and 2025 included over 18 product launches emphasizing powder-free optical scanning and wireless connectivity. Partnerships between scanner manufacturers and aligner companies increased by 22%, enhancing integrated treatment planning workflows. Mergers and acquisitions activity rose by 15%, particularly in software integration and cloud-based dental collaboration platforms.

Competitive differentiation centers on imaging precision below 20 microns, battery life exceeding 60 minutes, and real-time 3D rendering speeds under 30 seconds. R&D investment accounts for nearly 9% of annual operational budgets among leading players, reinforcing innovation intensity within the global Dental Impression Systems Market.

Planmeca Oy

Carestream Dental LLC

Medit Corp.

Straumann Group

GC Corporation

Ivoclar Vivadent AG

Henry Schein, Inc.

Shining 3D Tech Co., Ltd.

Midmark Corporation

Zirkonzahn GmbH

Vatech Co., Ltd.

Technological innovation in the Dental Impression Systems Market is centered on AI-powered imaging, high-resolution 3D optical scanning, and integrated digital workflow ecosystems. Modern intraoral scanners achieve accuracy levels below 20 microns, enabling precise crown and bridge fabrication. Real-time 3D rendering capabilities have reduced scanning time to under 45 seconds per arch, improving chairside productivity by 24%.

AI-driven margin detection and occlusal analysis tools enhance treatment planning accuracy by 21% and reduce remakes by nearly 18%. Wireless scanners weighing less than 250 grams improve ergonomics and reduce operator fatigue by 14%. Cloud-based case management platforms facilitate instant laboratory collaboration, cutting turnaround time by 17%.

Interoperability with CAD/CAM milling systems allows chairside fabrication within 60 minutes for single crowns. Advanced software encryption protocols ensure compliance with digital health data regulations, addressing cybersecurity concerns affecting 19% of digital practices. Emerging technologies include augmented reality visualization for prosthetic alignment and machine-learning algorithms predicting restoration adjustments. Investment in R&D exceeds 9% of operational expenditure among leading manufacturers, reinforcing rapid innovation cycles in the Dental Impression Systems Market.

• In March 2025, Dentsply Sirona introduced an enhanced version of its Primescan intraoral scanner with AI-powered scan intelligence, improving scanning speed by 20% and reducing data processing time by 15%, strengthening chairside digital workflow efficiency. Source: www.dentsplysirona.com

• In January 2025, 3Shape announced an update to its TRIOS software platform integrating automated margin line detection, resulting in up to 18% fewer remakes in pilot clinics and improved laboratory communication accuracy. Source: www.3shape.com

• In September 2024, Align Technology expanded its iTero scanner portfolio with upgraded imaging algorithms that enhanced restorative case visualization accuracy by 22%, supporting advanced orthodontic and implant workflows. Source: www.aligntech.com

• In July 2024, Planmeca launched a new wireless intraoral scanner featuring a 45-minute continuous scanning battery life and improved ergonomic design, reducing operator fatigue by 14% in clinical trials. Source: www.planmeca.com

The Dental Impression Systems Market Report comprehensively analyzes digital and traditional impression technologies across restorative dentistry, orthodontics, implantology, and cosmetic applications. The scope includes detailed segmentation by type, application, and end-user, covering digital intraoral scanners, elastomeric materials, and hybrid solutions. It evaluates usage patterns across dental clinics (61%), laboratories (27%), and academic institutions (12%), offering data-driven insights into equipment penetration rates and workflow transformation trends.

Geographically, the report covers North America (38% share), Europe (29%), Asia-Pacific (23%), South America (6%), and Middle East & Africa (4%), providing installation volumes, regulatory environments, and technology adoption statistics. It assesses over 35 active competitors, highlighting innovation metrics such as scanning precision below 20 microns and chairside fabrication within 60 minutes.

The scope further includes analysis of digital integration trends, AI-enabled margin detection, cloud-based collaboration systems, and cybersecurity considerations. It addresses procurement patterns, clinical workflow optimization, and patient preference trends, offering actionable intelligence for manufacturers, distributors, investors, and healthcare decision-makers seeking to capitalize on the evolving global Dental Impression Systems Market landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1,866.3 Million |

|

Market Revenue in 2033 |

USD 3,942.8 Million |

|

CAGR (2026 - 2033) |

9.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

3Shape A/S, Dentsply Sirona, Align Technology, Inc., Planmeca Oy, Carestream Dental LLC, Medit Corp., Straumann Group, GC Corporation, Ivoclar Vivadent AG, Henry Schein, Inc., Shining 3D Tech Co., Ltd., Midmark Corporation, Zirkonzahn GmbH, Vatech Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |