Reports

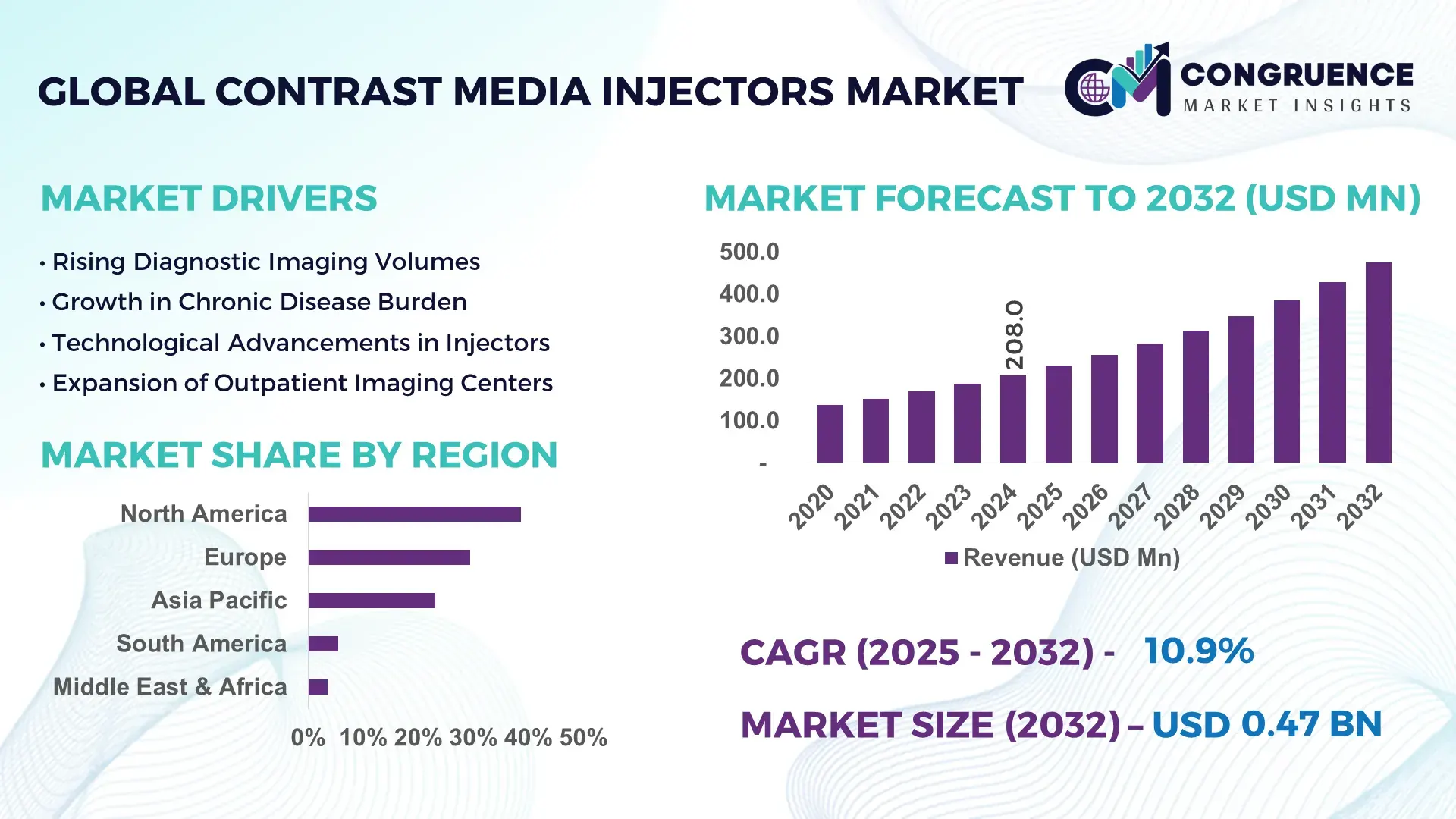

The Global Contrast Media Injectors Market was valued at USD 208.0 Million in 2024 and is anticipated to reach a value of USD 474.9 Million by 2032 expanding at a CAGR of 10.87% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is primarily driven by the rising volume of diagnostic imaging procedures and increasing adoption of automated, high-precision injection systems in hospitals and imaging centers.

The United States represents the dominant country in the Contrast Media Injectors Market, supported by advanced diagnostic infrastructure and high imaging utilization rates. The country performs over 90 million CT scans and 40 million MRI scans annually, creating sustained demand for injector systems across radiology departments. Investment in medical imaging equipment exceeds USD 20 billion annually, with a significant portion allocated to workflow automation and patient safety technologies. Dual-head and syringe-less injectors are increasingly deployed, reducing contrast waste by nearly 15–20% per procedure. Adoption is highest in tertiary hospitals and outpatient imaging centers, which together account for more than 70% of injector installations, supported by continuous upgrades to comply with evolving safety and dosing accuracy standards.

Market Size & Growth: Valued at USD 208.0 million in 2024, projected to reach USD 474.9 million by 2032 at a CAGR of 10.87%, driven by rising diagnostic imaging volumes.

Top Growth Drivers: CT scan utilization (64%), automation-driven workflow efficiency (48%), patient safety compliance adoption (39%).

Short-Term Forecast: By 2028, automated injectors are expected to reduce contrast media wastage by approximately 22%.

Emerging Technologies: Syringe-less injectors, AI-enabled dose optimization, pressure-monitoring smart injectors.

Regional Leaders: North America (USD 182.4 million by 2032; outpatient imaging growth), Europe (USD 146.7 million; regulatory-driven upgrades), Asia-Pacific (USD 109.2 million; infrastructure expansion).

Consumer/End-User Trends: Hospitals account for over 58% of installations, while imaging centers show faster adoption rates.

Pilot or Case Example: In 2023, a multi-hospital network reduced injector-related scan delays by 31% through smart injector deployment.

Competitive Landscape: Market leader holds ~28% share, followed by Bayer, Bracco, Guerbet, Nemoto, and Ulrich Medical.

Regulatory & ESG Impact: Stricter contrast dosing safety norms and waste reduction mandates shaping procurement decisions.

Investment & Funding Patterns: Over USD 1.1 billion invested globally since 2021 in imaging workflow automation technologies.

Innovation & Future Outlook: Integration with PACS, RIS, and AI diagnostics platforms defining next-generation injector systems.

The Contrast Media Injectors Market is shaped by CT injectors (46%), MRI injectors (34%), and angiography injectors (20%). Technological innovation, stricter patient safety protocols, and hospital digitization programs are driving regional consumption, with Asia-Pacific emerging as the fastest-expanding installation base.

The Contrast Media Injectors Market plays a strategic role in modern diagnostic imaging by enabling precise, repeatable, and safe contrast delivery across CT, MRI, and angiography procedures. Healthcare providers increasingly view injector systems as workflow-critical assets rather than auxiliary devices, particularly as imaging volumes rise and diagnostic turnaround times shorten. Syringe-less injector technology delivers up to 25% reduction in preparation time compared to traditional dual-syringe systems, improving scanner utilization and patient throughput.

Regionally, North America dominates in procedural volume, while Europe leads in adoption, with approximately 62% of imaging facilities using automated injectors integrated with digital imaging systems. In Asia-Pacific, hospital infrastructure expansion is accelerating uptake, particularly in China and India, where diagnostic imaging installations grow rapidly.

In the short term, by 2027, AI-enabled dose optimization is expected to reduce contrast-related adverse events by 18%, supporting safer imaging practices. ESG considerations are also influencing procurement, with manufacturers committing to 30% reduction in disposable plastic components by 2030 through recyclable injector consumables.

A measurable micro-scenario emerged in 2024, when a U.S.-based hospital group achieved a 27% improvement in scan room efficiency by integrating smart injectors with RIS and PACS platforms. Looking forward, the Contrast Media Injectors Market is positioned as a critical enabler of diagnostic accuracy, operational resilience, and sustainable healthcare delivery.

The Contrast Media Injectors Market is influenced by rising diagnostic imaging demand, hospital automation, and evolving patient safety regulations. Increasing prevalence of chronic diseases has led to higher CT and MRI utilization, directly increasing injector deployment. Technological advancements such as pressure-controlled injection, real-time monitoring, and digital connectivity are reshaping purchasing criteria. At the same time, capital budget constraints and lifecycle costs influence procurement decisions. Market dynamics also reflect a shift toward outpatient imaging centers, which now perform nearly 45% of diagnostic scans globally, driving demand for compact, high-throughput injector systems.

Global imaging procedure volumes continue to rise, with CT scan utilization increasing by over 7% annually in major healthcare systems. Contrast-enhanced studies account for nearly 65% of CT procedures, directly boosting injector demand. Automated injectors improve scan consistency and reduce manual errors, leading to improved diagnostic quality. Hospitals report up to 20% reduction in repeat scans after adopting advanced injector systems, reinforcing their role in efficient radiology workflows.

Advanced injector systems require significant upfront investment, with full-system installations often exceeding USD 35,000 per unit. Annual maintenance, calibration, and consumable costs further strain budgets, particularly for smaller imaging centers. In emerging markets, cost sensitivity limits adoption, while refurbished injector availability slows replacement cycles in mature regions.

Outpatient imaging centers are expanding rapidly, performing nearly 40–45% of contrast-based scans. These facilities prioritize compact, automated injectors with fast setup and minimal downtime. Demand for scalable injector platforms tailored to high-throughput outpatient workflows presents strong growth opportunities, especially in urban and semi-urban regions.

Injectors must meet stringent safety and accuracy standards related to pressure limits, dosing precision, and cross-contamination prevention. Compliance testing increases product development timelines and certification costs. Frequent regulatory updates require ongoing design modifications, adding complexity for manufacturers and delaying market entry for new systems.

Shift Toward Syringe-less Injector Systems: Over 42% of new installations now use syringe-less technology, reducing contrast waste by 15–20% and lowering setup time by 30% per procedure.

Integration with Imaging IT Systems: Approximately 55% of hospitals deploy injectors integrated with PACS and RIS platforms, enabling automated protocol selection and improving scan consistency by 18%.

Growth in Dual-Head CT Injectors: Dual-head injectors are used in nearly 60% of contrast-enhanced CT procedures, allowing saline flushing and improving image clarity while reducing contrast volume by 12%.

Emphasis on Patient Safety Monitoring: Smart pressure-sensing injectors have reduced extravasation incidents by 25%, strengthening patient safety outcomes in high-volume imaging environments.

The Contrast Media Injectors Market is segmented by type, application, and end-user, reflecting varied clinical workflows, imaging modalities, and healthcare delivery models. By type, differentiation is driven by injector configuration, automation level, and compatibility with imaging systems such as CT, MRI, and angiography. Applications are closely linked to diagnostic imaging volumes and procedural complexity, with contrast-enhanced CT and MRI scans forming the backbone of demand. End-user segmentation highlights differences in procurement behavior, utilization intensity, and technology adoption between hospitals, diagnostic imaging centers, and specialty clinics. Across segments, decision-making is increasingly influenced by patient safety standards, workflow efficiency, and digital integration with hospital information systems. Adoption patterns also show a shift toward high-throughput, automated solutions that minimize contrast wastage and procedural variability, while emerging outpatient settings are reshaping volume distribution and equipment preferences.

The market by type includes CT contrast media injectors, MRI contrast media injectors, angiography injectors, and combination or multi-modality injectors. CT injectors represent the leading segment, accounting for approximately 46% of total installations, supported by the high global volume of contrast-enhanced CT procedures and the widespread use of dual-head injector systems that enable saline flushing and dose precision. MRI injectors follow with around 34% share, driven by increasing neurological, musculoskeletal, and oncology imaging requirements, where controlled injection rates are critical for image consistency. Angiography injectors, while smaller in volume, are gaining importance in interventional cardiology and vascular procedures, supported by rising minimally invasive interventions. This segment is the fastest-growing, expanding at an estimated 11.8% CAGR, driven by increasing catheter-based procedures and demand for high-pressure, precision-controlled injectors. Combination and multi-modality injectors address niche requirements in hybrid imaging environments and account for a combined 20% share, offering flexibility for facilities seeking to optimize equipment utilization.

By application, the market is segmented into computed tomography (CT), magnetic resonance imaging (MRI), angiography, and other contrast-enhanced diagnostic procedures. CT imaging is the dominant application, accounting for nearly 58% of overall usage, due to its role as the first-line diagnostic tool in trauma, oncology staging, and cardiovascular assessment. MRI applications contribute approximately 27%, reflecting growing demand for contrast-enhanced neurological and soft-tissue imaging. Angiography is the fastest-growing application, expanding at an estimated 12.3% CAGR, supported by rising interventional cardiology and neurovascular procedures. Other applications, including fluoroscopy-based studies and hybrid imaging, collectively represent a combined 15% share, serving specialized diagnostic needs. Consumer and adoption trends reinforce this segmentation. In 2024, approximately 42% of hospitals in the United States reported upgrading contrast injector systems specifically to support higher CT scan throughput. Additionally, over 35% of imaging centers globally indicated active testing of automated injector protocols to reduce scan preparation time and improve patient throughput.

End-user segmentation comprises hospitals, diagnostic imaging centers, ambulatory surgical centers (ASCs), and specialty clinics. Hospitals dominate the market with an estimated 61% share, reflecting high patient volumes, complex diagnostic requirements, and continuous investment in imaging infrastructure. Large tertiary hospitals typically operate multiple injector systems per imaging modality, driving higher utilization rates. Diagnostic imaging centers represent the fastest-growing end-user segment, expanding at approximately 10.9% CAGR, fueled by the global shift toward outpatient diagnostics and decentralized imaging services. These centers prioritize compact, high-throughput injectors that minimize downtime and operational complexity. ASCs and specialty clinics collectively account for a combined 18% share, primarily supporting orthopedic, cardiovascular, and oncology-focused imaging. Adoption trends show that in 2024, over 38% of outpatient imaging centers globally reported transitioning from manual or semi-automated injectors to fully automated systems. Additionally, nearly 45% of hospitals in developed markets indicated active integration of injector systems with RIS and PACS platforms to improve workflow automation.

North America accounted for the largest market share at 38.6% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.1% between 2025 and 2032.

The global Contrast Media Injectors Market shows clear regional divergence driven by healthcare infrastructure maturity, diagnostic imaging volumes, and capital investment intensity. North America leads due to high penetration of advanced CT and MRI systems, with over 92 imaging scanners per million population and strong replacement demand for automated injectors. Europe follows with 29.4% share, supported by standardized imaging protocols and public healthcare spending across Germany, the UK, and France. Asia-Pacific, holding 23.1% share in 2024, ranks third in size but first in growth momentum, supported by double-digit expansion in diagnostic centers and over 18% annual increases in CT scan volumes across China and India. South America and the Middle East & Africa together account for 8.9%, driven by selective infrastructure upgrades, public–private partnerships, and rising chronic disease diagnostics. Regional adoption is increasingly shaped by digital injector integration, patient safety mandates, and outpatient imaging expansion.

The market in this region accounts for approximately 38.6% of global demand, driven primarily by hospitals and large diagnostic imaging networks. CT and MRI procedures collectively represent over 70% of injector utilization, supported by strong demand from oncology, cardiology, and trauma diagnostics. Government-backed healthcare expenditure exceeds USD 4.5 trillion annually, supporting continuous equipment upgrades. Regulatory emphasis on patient safety and contrast dose accuracy has accelerated adoption of dual-head and smart injectors with error-reduction features. Technological trends include injector integration with RIS and PACS systems, now implemented in over 45% of large hospitals. A leading local player has expanded automated injector installations across multi-hospital networks, reducing scan preparation time by 22%. Consumer behavior reflects high acceptance of contrast-enhanced imaging, with outpatient diagnostic visits growing by 11% year-on-year.

Europe holds around 29.4% market share, with Germany, the UK, and France contributing nearly 58% of regional demand. Strong regulatory oversight from medical device authorities has driven adoption of injectors with traceability, digital logging, and dose monitoring. Public healthcare systems conduct over 210 million imaging procedures annually, supporting stable injector demand. Sustainability initiatives encourage longer device life cycles and reduced contrast wastage, influencing procurement criteria. Emerging technologies such as pressure-adaptive injectors and software-based workflow optimization are now used in over 35% of tertiary hospitals. A regional manufacturer has focused on MRI-compatible injector platforms, expanding installations across university hospitals. Consumer behavior is influenced by compliance-driven procurement, with hospitals prioritizing transparent performance data and safety certifications.

Asia-Pacific represents 23.1% of the global market and ranks as the fastest-growing region by volume expansion. China, India, and Japan together account for over 72% of regional consumption, supported by rapid hospital construction and imaging center growth. The region adds more than 6,000 new CT and MRI scanners annually, creating sustained demand for injector systems. Manufacturing localization and cost-optimized injector models are gaining traction, particularly in China and India. Innovation hubs in Japan and South Korea are advancing compact, AI-assisted injectors. A regional player has scaled domestic production to supply over 12,000 injector units annually. Consumer behavior reflects rising outpatient diagnostics, with urban imaging visits increasing by 15% per year.

South America accounts for approximately 5.4% of global demand, led by Brazil and Argentina. Public healthcare infrastructure upgrades and private diagnostic chain expansion are key growth drivers. Over 65% of injector demand originates from metropolitan hospitals and private imaging centers. Government incentives supporting medical equipment imports and localized assembly have improved accessibility. Digital injector adoption remains selective but is increasing in tertiary hospitals. A regional distributor has partnered with hospital groups to standardize injector platforms across 120+ imaging sites. Consumer behavior shows rising preference for private diagnostics, with insured outpatient imaging volumes growing by 9% annually.

This region contributes around 3.5% of global market volume, with the UAE and South Africa representing nearly 48% of regional demand. Growth is supported by hospital expansion programs, particularly in urban centers. Diagnostic imaging demand is rising alongside chronic disease prevalence, with CT scan volumes increasing by 14% year-on-year in Gulf countries. Technological modernization includes adoption of automated injectors in flagship hospitals and medical cities. Regulatory frameworks increasingly mandate device safety and performance documentation. A regional healthcare group has upgraded injector systems across 30 hospitals to support high-throughput imaging. Consumer behavior reflects growing trust in advanced diagnostics, particularly in private healthcare facilities.

United States – 32.1% Market Share: Strong diagnostic imaging density, high hospital capital expenditure, and widespread adoption of automated injector technologies.

Germany – 11.4% Market Share: Robust public healthcare infrastructure, high imaging procedure volumes, and strict compliance-driven equipment procurement.

The Market Competition Landscape in the Contrast Media Injectors Market is moderately concentrated, with a combination of established global manufacturers and specialized medical device firms competing across multiple segments and technologies. There are 20+ active competitors globally, spanning innovative injector system developers, consumables suppliers, and integrated imaging platform providers. The market is characterized by ongoing strategic initiatives such as product launches, partnerships, acquisitions, and technology collaborations, aimed at enhancing clinical performance, workflow automation, and integration with hospital information systems. The top five companies collectively account for an estimated ~45% of total injector installations, reflecting a landscape where leading players maintain strong footholds while a diverse set of regional firms capture niche opportunities. Companies are investing in dual-head injector systems, syringeless technology, real-time pressure monitoring, and touch-enabled interfaces to differentiate offerings and address clinical demand for precision and safety. Notable mergers, such as Medtronic’s acquisition of a startup focused on automated injector technologies, underscore competitive efforts to broaden portfolios and accelerate innovation. Strategic partnerships—such as collaborations between Bayer and Siemens Healthineers for integrated imaging and injection solutions—further demonstrate the emphasis on value-added bundled offerings. Innovation trends influencing the competitive environment include AI-enabled dosing algorithms, modular systems for hybrid imaging, and enhanced consumable logistics that together shape competitive advantage and influence procurement decisions among hospitals and imaging networks.

Guerbet LLC

Ulrich GmbH & Co. KG

Nemoto Kyorindo Co., Ltd.

Siemens Healthineers

Medtronic plc

ANITA Medical Systems Pvt. Ltd.

Lantheus Medical Imaging

Technological innovation in the Contrast Media Injectors Market is rapidly transforming operational efficiency, clinical precision, and integration within diagnostic imaging workflows. Automated injector systems remain at the forefront, with advanced dual-head injectors that can simultaneously deliver contrast media and saline flushing, reducing preparation time and improving imaging quality for CT and MRI procedures. Approximately 36% of new injector models introduced recently feature automated delivery capabilities, programmable injection protocols, and real-time monitoring of contrast flow parameters, enhancing reproducibility and reducing manual variation in contrast administration.

Syringeless injector technology is another pivotal trend, eliminating manual syringe preparation and significantly reducing contamination risk, plastic waste, and setup time. Around 15% of newly installed injectors incorporate syringeless designs, which streamline workflows in high-throughput hospital imaging departments.

AI and machine learning integration is expanding beyond basic automation to include predictive dosage optimization and adaptive injection profiles tailored to patient physiology. These systems leverage algorithmic insights to fine-tune contrast delivery, improving diagnostic clarity while reducing contrast waste and potential adverse reactions. Integration with hospital electronic systems and imaging IT platforms—such as PACS (Picture Archiving and Communication Systems) and RIS (Radiology Information Systems)—enables seamless data exchanges that support workflow automation and documentation consistency across imaging suites.

Pressure monitoring and enhanced safety protocols feature prominently in next-generation injectors, with real-time pressure feedback and automated safety cutoffs built into roughly 25% of upgraded systems, supporting more secure use in interventional and high-pressure imaging contexts.

Modular and multi-modal injectors that support CT, MRI, and angiography in a single platform are gaining traction, enabling facilities to optimize capital equipment utilization. These innovations are reshaping procurement strategies for radiology departments, incentivizing the adoption of systems capable of handling diverse clinical demands. Continuous investment in digital connectivity, ergonomic design, and consumables optimization underscores the technology trajectory in the contrast media injector landscape.

In December 2024, Bracco Diagnostics Inc. received FDA 510(k) clearance for the Bracco-branded Max 3™ Rapid Exchange and Syringeless Injector for MRI procedures, designed to streamline workflow by allowing direct injection from original contrast media vials, reduce disposable plastic waste, and improve operational efficiency in radiology suites. Source: www.bracco.com

In November 2023, Bracco Imaging and ulrich GmbH & Co. KG announced a long-term strategic partnership to bring a Bracco-branded state-of-the-art MR injector to the U.S., with a 510(k) premarket notification submitted to the FDA, aimed at enhancing diagnostic imaging quality and expanding the injector portfolio. Source: www.bracco.com

In Q1 2024, Ulrich Medical achieved above-average sales growth of 18% in Europe, with France showing a 90% increase in CT and MRI injector sales, driven by regulatory approvals allowing multi-patient syringe-free injectors. Source: www.ulrichmedical.com

In November 2024, Bayer received U.S. FDA 510(k) clearance for its MEDRAD Centargo CT Injection System, a multi-patient automated injector designed to improve workflow efficiency in CT suites with features such as rapid setup and flexible contrast/saline delivery, supporting high-volume imaging operations

The scope of the Contrast Media Injectors Market Report encompasses a comprehensive analysis of product systems, injector typologies, clinical applications, and end-user environments globally. The report details segmentation by injector systems and consumables, covering single-head, dual-head, and syringeless injectors, and examines how these categories meet diverse clinical needs across CT, MRI, angiography, and hybrid imaging procedures. It also assesses the operational deployment contexts in hospitals, diagnostic imaging centers, ambulatory surgical centers, and specialty radiology clinics to illuminate purchasing behavior and utilization patterns. Regionally, the report provides a detailed view of North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting infrastructure trends, regulatory landscapes, and the impact of diagnostic imaging volumes on injector adoption. Technology focus areas include digital integration with imaging IT ecosystems, advancements in automated and AI-assisted contrast delivery, and the rise of modular and multi-modal systems that support scalable imaging workflows. Competitive analysis evaluates product launches, strategic partnerships, and innovation trajectories among key market participants. The report also identifies niche segments such as pressure-controlled injectors for high-intensity procedures and consumable optimization tools that reduce waste and streamline logistics. Together, these elements equip decision-makers with actionable insights into market structure, technology evolution, and growth opportunities in contrast media injectors.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 208.0 Million |

| Market Revenue (2032) | USD 474.9 Million |

| CAGR (2025–2032) | 10.87% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Bayer AG; Bracco Diagnostics Inc.; GE Healthcare; Guerbet Group; Ulrich GmbH & Co. KG; Nemoto Kyorindo Co., Ltd.; Siemens Healthineers; Medtron AG; ANITA Medical Systems Pvt. Ltd.; Lantheus Medical Imaging |

| Customization & Pricing | Available on Request (10% Customization Free) |