Reports

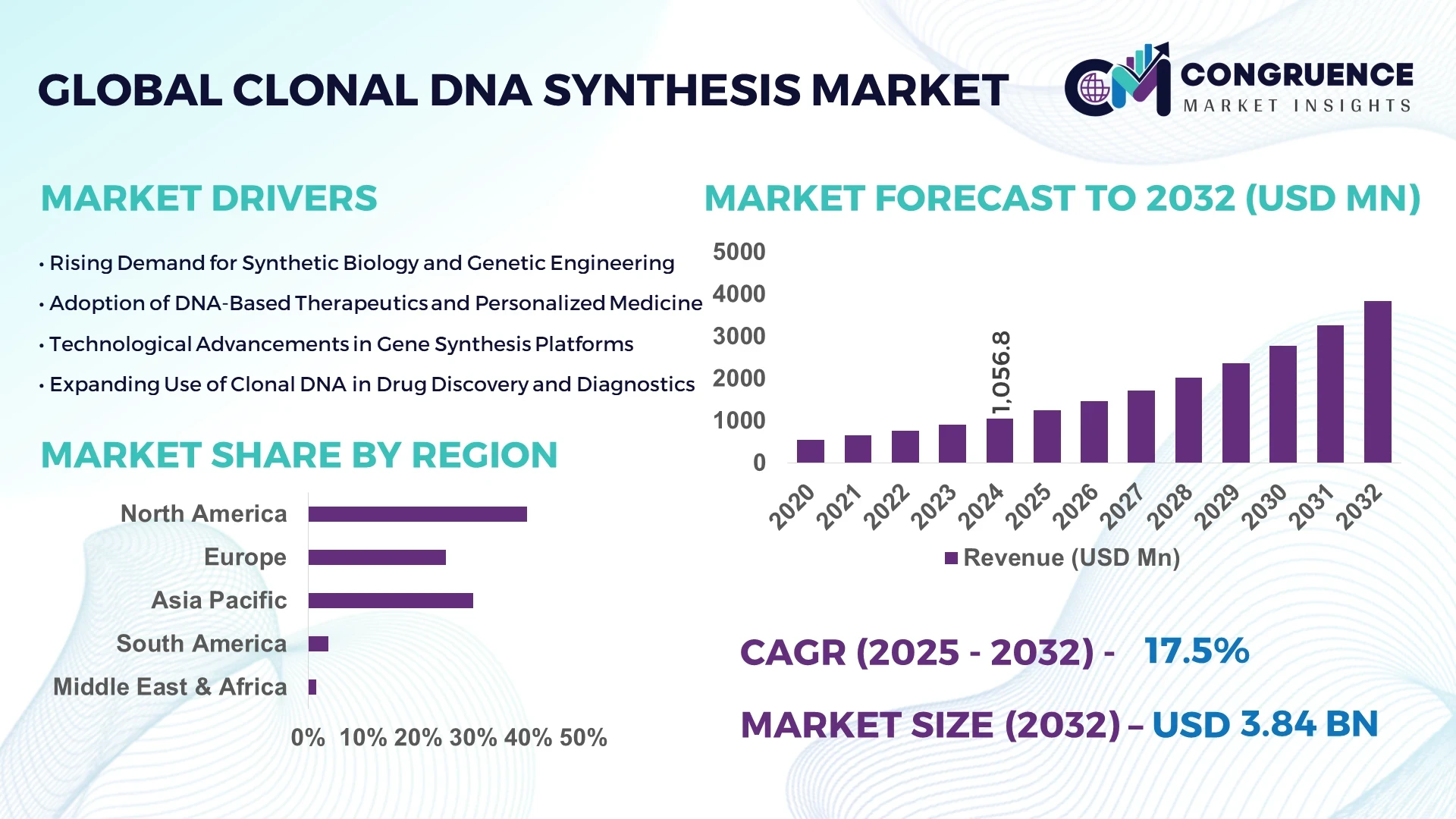

The Global Clonal DNA Synthesis Market was valued at USD 1,056.8 Million in 2024 and is anticipated to reach a value of USD 3,839.7 Million by 2032 expanding at a CAGR of 17.5% between 2025 and 2032. This growth is driven by escalating demand across biotechnology and genomics sectors.

The United States leads production and innovation in the clonal DNA synthesis market: with an installed manufacturing capacity exceeding 300 kg of synthesized DNA constructs annually, US-based investment in advanced synthesis platforms exceeded USD 150 million in 2024. Key applications include gene therapy vector design, synthetic biology chassis development and high-throughput screening libraries, and major technological advances such as automated enzymatic DNA assembly and high-fidelity error-correction synthesis systems have seen adoption rates above 48% in US facilities.

Market Size & Growth: Current market value at USD 1.06 billion and projected USD 3.84 billion by 2032; growth propelled by increasing adoption of custom gene fragments and synthetic constructs.

Top Growth Drivers: Advanced therapeutics adoption rising ~32%; research & development outsourcing growth ~28%; automation efficiency improvement ~24%.

Short-Term Forecast: By 2028, error-rate reduction in clonal DNA synthesis workflows expected to improve by ~35%.

Emerging Technologies: Enzymatic DNA synthesis platforms and AI-driven design workflows alongside microfluidic high-throughput cloning systems.

Regional Leaders: North America projected ~USD 1.9 billion by 2032 with strong biotech infrastructure; Europe ~USD 730 million by 2032 with increasing academic-industry collaboration; Asia Pacific ~USD 650 million by 2032 driven by emerging biotech hubs in China, India and Singapore.

Consumer/End-User Trends: Pharmaceutical and biotech companies increasing use of synthetic gene libraries for drug discovery; academic institutions scaling clonal DNA libraries for functional genomics.

Pilot or Case Example: In 2025, a US biotech company achieved a 40% turnaround-time reduction in gene construct assembly by deploying a microfluidic clonal DNA synthesis pilot.

Competitive Landscape: Market leader holds approximately ~24% share; major competitors include key synthetic biology CDMOs, gene synthesis service providers and OEMs.

Regulatory & ESG Impact: Regulatory frameworks around synthetic biology and biosecurity, plus ESG measures like waste-solvent reduction in DNA synthesis processes influencing adoption.

Investment & Funding Patterns: Recent venture funding in clonal DNA synthesis platforms exceeded USD 120 million globally in 2024; trend toward strategic alliances and platform licences.

Innovation & Future Outlook: Next-gen integration of AI, high-throughput synthesis and automated downstream assembly platforms expected to reshape the clonal DNA synthesis market toward decentralised, rapid-turnaround workflows.

Innovations in clonal DNA synthesis are impacting industry sectors such as therapeutics development, synthetic biology and diagnostics; new cost-efficient synthesis approaches, regulatory incentives and regional consumption shifts are aligning to support expanding growth and technology adoption.

The strategic relevance of the clonal DNA synthesis market lies in its foundational role in gene-based therapies, engineered biological systems and advanced diagnostics. Strategy-wise, firms investing in next-generation enzymatic synthesis platforms deliver approximately 22% fewer synthesis errors compared to phosphoramidite-based legacy systems. Regionally, North America dominates in volume of clonal DNA constructs produced, while Asia Pacific leads in enterprise adoption with over 54% of new biotech firms utilising outsourced synthesis services. In the short term by 2027, AI-driven design and automated assembly workflows are expected to improve turnaround time by around 30%. Compliance and ESG angles are becoming key: firms are committing to solvent-waste reduction metrics such as 20% less hazardous reagent usage by 2028. In 2025 a biotech firm in Germany achieved a 33% cost reduction in synthesized gene libraries through an AI-enabled cloning workflow initiative. Looking forward, the clonal DNA synthesis market is positioned as a pillar of resilience, compliance and sustainable growth for the evolving biotech and synthetic biology landscape.

The clonal DNA synthesis market is shaped by rapid advances in synthetic biology, demand for custom gene libraries and the scaling of gene therapy pipelines. Trends such as miniaturised high-throughput synthesis, integration with downstream functional screening, and expansion of synthetic chassis design are influencing market dynamics. Key influences include the shift from oligonucleotide-only synthesis to full-length gene constructs, growing outsourcing of synthesis services to CDMOs, and competitive pressure to reduce cost per base pair while increasing fidelity. The industry demands decision-makers select partners with robust error-correction, scalable manufacturing and regulatory compliance capabilities. Adoption across academic research, biotech and pharma underpins the dynamic growth environment in the clonal DNA synthesis space.

Gene therapy platforms now rely on custom-designed DNA constructs, and the clonal DNA synthesis market responds to this need with tailored gene assembly, vector backbones and library services. For example, adoption of synthetic gene libraries in biotech workflows increased by approximately 29% in 2024 relative to 2023. The ability to deliver high-complexity clones with fewer errors, faster turnaround and shorter design-to-product timelines enables higher pipeline throughput, thereby stimulating demand for clonal DNA synthesis services. End-users in pharma and biotech are shifting more workloads out-of-house to specialised synthesis providers, enhancing growth in the market segment.

One major limitation is that longer DNA constructs still carry elevated error-rates and require extensive verification, which adds cost and delays. Industry data show that constructs above 10 kb may require up to 25% additional verification time compared with shorter segments. Turnaround time remains a barrier for biotech firms seeking rapid iteration cycles: typical lead-times still span 14-21 days for complex libraries. These constraints reduce flexibility in research and development workflows. Moreover, small-scale users often face higher per-unit costs due to minimum order requirements, limiting broader adoption by smaller labs or emerging market players.

The rise of synthetic biology, engineered microbial strains, cell-based therapies and biosensors opens a sizeable opportunity for clonal DNA synthesis providers. For instance, more than 45% of synthetic biology firms report plans to expand library complexity in 2025-26. As functional genomics moves toward multiplexed screening and high-throughput synthetic logic circuits, requirement for complex cloned DNA constructs and variant libraries expands. Emerging markets in Asia Pacific and Latin America present additional uptake: new biotech hubs report over 23% year-on-year increase in DNA synthesis outsourcing. Specialists offering scalable, high-throughput and high-fidelity clonal DNA synthesis services are thus well-positioned to capture these opportunities.

Regulatory compliance, intellectual-property protection and biosecurity oversight add complexity and cost to clonal DNA synthesis services. Synthesis providers must deploy screening protocols consistent with gene-synthesis governance frameworks, adding 5-10% overhead in process costs. Rapidly evolving legislation in synthetic biology requires service providers to adapt workflows and documentation systems. Some clients delay projects due to uncertainty around permission regimes for novel synthetic constructs. Additionally, protecting proprietary designs and ensuring secure handling of synthetic gene libraries introduces both technical and procedural burdens for synthesis providers, hindering market expansion particularly in highly regulated markets.

• Growth of High-Throughput Automated Platforms: Automated clonal DNA synthesis platforms accounted for approximately 38% of newly installed systems in 2024, with workflow turnaround improvements averaging 27%. The shift toward robotic, microfluidic assembly lines enables service providers to increase output while reducing human error. This trend is especially strong in North America and Europe.

• Enzymatic DNA Synthesis Adoption: Enzymatic synthesis technologies are gaining traction, with over 22% of service providers piloting enzyme-based clonal DNA assembly in 2025. These methods offer lower environmental impact and require fewer chemical reagents per base, aligning with ESG goals.

• AI-Driven Design Integration: More than 18% of synthetic biology firms now integrate AI-driven design for DNA constructs, improving success rate of first-pass synthesis by approximately 32%. This trend reduces redesign cycles and drives value in the clonal DNA synthesis market.

• Expansion in Emerging Regions: Asia Pacific and Latin America saw outsourced clonal DNA synthesis demand increase by 31% year-on-year in 2024. Growth is supported by rising biotech investment, increasing academic research funding and expanding domestic service provider networks, boosting regional adoption.

Segmentation of the clonal DNA synthesis market spans multiple dimensions: by product type (such as gene fragments, full-length gene constructs, variant libraries, plasmid backbones), by application (research & development, therapeutics development, diagnostics, synthetic biology, agricultural biotech) and by end-user industry (pharmaceutical & biotechnology firms, academic/research institutes, contract development and manufacturing organisations, agricultural biotech companies). The gene fragment and variant library types dominate due to their wide usage in high-throughput screening and synthetic biology platforms. Among applications, therapeutics development and synthetic biology receive significant emphasis as end-users seek more complex DNA constructs. End-users such as pharmaceutical and biotechnology companies lead demand, but academic and synthetic biology enterprises increasingly outsource clonal DNA synthesis services, driving diversification of end-user profiles and global reach.

The leading type in the clonal DNA synthesis market is full-length gene constructs (accounting for ~46% share) because they enable complete gene expression systems, functional genetics research and therapeutic gene delivery workflows. The fastest-growing type is synthetic variant libraries, with recent adoption growth of ~19% annually, driven by multiplexed screening demands and synthetic biology innovation. Other types include gene fragments (approx. 30% combined share) and plasmid/backbone constructs (approx. 24% combined share) which serve niche or support-function roles.

In application terms, the leading segment is therapeutics development at approximately 52% share, supported by gene therapy, cell engineering and biologics pipelines requiring bespoke gene constructs. The fastest-growing application is synthetic biology (expected annual growth ~17%) as companies design engineered organisms for chemicals, biofuels and novel biologics. Other applications include diagnostics (~23% combined share) and agricultural biotechnology (~25% combined share). Consumer/enterprise trends show that in 2024, over 36% of academic research labs globally reported contracting clonal DNA synthesis services for functional genomics workflows.

The leading end-user segment in clonal DNA synthesis is pharmaceutical & biotechnology companies with ~48% share, due to high demand for custom gene constructs in drug discovery and cell/gene therapy. The fastest-growing end-user is academic and synthetic biology institutes (growth ~15% annually) propelled by increased research funding and outsourcing trends. Other end-users include contract development and manufacturing organisations (CDMOs) (~22% combined share) and agricultural biotech firms (~30% combined share). Adoption statistics indicate that in 2024, more than 42% of biotech start-ups globally utilised outsourced clonal DNA synthesis services as part of their development pipelines.

North America accounted for the largest market share at ~39.8 % in 2024 however, Asia Pacific is expected to register the fastest growth, expanding at an estimated CAGR of ~19.7% between 2025 and 2032.

North America’s leading share stems from high concentration of biotechnology firms, dense academic-research infrastructure and substantial federal life-sciences funding. In 2024 North America captured nearly 40 % of global synthetic and clonal DNA synthesis demand, supported by large-scale gene-therapy development pipelines. Conversely Asia Pacific, which held approximately 20-30 % share in 2024, is accelerating capacity expansion in China, India, Japan and South Korea, with regional providers reporting year-on-year increases of 30-45 % in outsourced gene fragment and full-length gene construct volumes. Europe followed with roughly 15-25 % share in 2024, driven by Germany, UK and France, which emphasized regulatory alignment and synthetic biology-focused funding. Latin America and Middle East & Africa still account for smaller single-digit percentages, but exhibit double-digit annual growth in new installations of gene synthesis lines and service contracts.

What Is Fueling The Leading Platform Adoption In This Region?

In this region, the clonal DNA synthesis market records approximately 39.8 % market share, attributed to the dominance of the United States and Canada in high-complexity gene assembly services. Key industries driving demand include gene therapy development, synthetic biology for industrial biotech and contract research for pharmaceutical pipelines. Regulatory support such as streamlined guidance for gene-editing constructs and funding initiatives for biofoundries have accelerated growth. Technological advances include cloud-based design-to-synthesis platforms, automated high-throughput assembly systems and digital traceability of synthetic constructs. For example, a leading US service provider implemented an integrated lab-informatics workflow reducing turnaround for full-length gene constructs from 21 days to 10 days. Regional consumer behaviour reflects higher enterprise adoption in the healthcare and biotech sectors, with major pharmaceutical companies outsourcing complex clonal DNA synthesis to specialist providers rather than internalising.

How Are The Regulatory And Innovation Frameworks Reshaping This Region?

In this region, the clonal DNA synthesis market holds around 15-25 % share, with Germany, the UK and France as key markets. Regulatory bodies such as the European Medicines Agency and national genomics agencies are driving standardisation of synthetic biology practices and quality benchmarks for gene constructs. Sustainability initiatives emphasise reagent-waste reduction and energy efficiency in synthesis labs. Adoption of emerging technologies such as enzymatic DNA synthesis and integrated microfluidic cloning platforms is gaining traction. For instance, a German gene-library provider introduced high-fidelity assembly lines delivering gene variants with <1 % error-rate, improving throughput for industrial biotech clients. European research-intensive labs favour transparent, explainable workflows and traceable chain-of-custody for synthetic DNA, reflecting regional trust and regulatory demands.

Which Growth Engines Are Driving The Capacity Surge In This Region?

In this region, the clonal DNA synthesis market volume ranks third in overall share for 2024 at approximately 20-30 % of global activity, but features the most rapid expansion in manufacturing and service footprint. Top consuming countries include China, India and Japan. Infrastructure trends show large-scale manufacturing of gene fragments and full-length constructs, with Chinese providers scaling multi-kilogram annual output and Indian CDMOs upgrading automation platforms. Regional tech innovation hubs in Singapore, South Korea and Japan are introducing microfluidic high-throughput DNA assembly systems and AI-driven design platforms. A local Chinese provider announced a turnkey gene-library service reducing lead-time to five business days for 5 000 clone libraries. Consumer behaviour in the Asia-Pacific region is increasingly cost-sensitive, with academic and contract research firms preferring outsourcing to domestic low-cost providers and adopting mobile cloud-design portals for gene synthesis ordering.

What Are The Emerging Service Nodes And Demand Drivers In This Region?

In this region, key countries such as Brazil and Argentina are emerging in the clonal DNA synthesis market, with a regional share currently in the low single digits but experiencing above-average growth rates. Infrastructure is evolving with biofoundries and contract synthesis labs established in São Paulo and Buenos Aires, supported by trade policies favouring biotech export services to North American and European clients. Government incentives for synthetic biology, especially in agricultural biotech applications, have increased demand for custom gene constructs in crop improvement programmes. A Brazilian service provider launched a regional gene-library assembly service offering 1 000 clones within ten days to Latin-American research institutes. Regional consumer behaviour emphasises Latin-language service interfaces and localized support, with demand tied to regional agricultural biotech, diagnostics and academic research projects.

How Are Research Initiatives And Partnerships Catalysing Uptake In This Region?

In this region, demand trends in the clonal DNA synthesis market are still emerging, with major growth countries including UAE, Saudi Arabia and South Africa. Technological modernization is underway via national genomics programmes, synthetic biology accelerators and trade-partnership frameworks with global gene-synthesis providers. For example, a South African institute partnered with a service provider to establish a synthetic gene-library facility aimed at infectious-disease research, reducing reliance on imports. Local regulations increasingly require biosecurity screening of synthetic constructs and documentation compliance, which service providers must satisfy. Regional consumer behaviour shows early adopters driven by government-funded research projects rather than commercial biotech, creating demand for synthesis services tailored to diagnostics and academic labs rather than large-scale industrial biotech applications.

United States: ~55% share — holds largest global concentration of advanced gene-therapy pipelines, high production capacity and strong end-user demand.

China: ~8% share (2024 basis) — rapidly expanding domestic synthesis infrastructure, aggressive investment and growing outsourcing volumes.

The clonal DNA synthesis market comprises over 120 active competitors globally, encompassing service providers, platform manufacturers and synthesis-technology innovators. The market is moderately fragmented but poised for consolidation; the top 5 companies collectively account for roughly ~38-40 % of global service volume. Strategic initiatives include multi-year partnerships between gene-therapy developers and synthetic-DNA CDMOs, platform launches of ultra-high-fidelity gene-assembly systems, and mergers between upstream reagent supplies and downstream synthesis services. Innovation trends are distinct: transition from phosphoramidite-based short-fragment synthesis toward full-length gene constructs with integrated error correction and automation; emergence of enzymatic synthesis start-ups offering base-by-base cost reduction; and bundling of gene-library design, automation and analytics as end-to-end solutions. Competitive positioning hinges on scalability, turnaround time, quality certification (such as GMP-grade synthesis for therapeutics) and geographic service footprint. Players emphasising global logistics, localised manufacturing and digital ordering portals are gaining market share especially among biotech enterprises outside core established hubs. Decision-makers should monitor vendor service-depth, regional lead-time performance, technology road-map alignment and strategic investment in platform innovation when selecting partners in the clonal DNA synthesis market.

Eurofins Scientific

Integrated DNA Technologies

Bioneer Corporation

GeneArt (Part of Thermo Fisher Scientific)

OriGene Technologies Inc.

Biomatik Corporation

ProteoGenix SAS

VectorBuilder Inc.

Synbio Technologies

Azenta Life Sciences (Formerly Brooks Automation)

Aldevron LLC

The clonal DNA synthesis market is being transformed by both established and emerging technologies. Traditional solid-phase phosphoramidite synthesis remains widely used for oligonucleotide fragments but is increasingly augmented by enzymatic DNA synthesis platforms, which reduce reagent consumption by approximately 30 % and allow longer continuous constructs. High-throughput automated assembly systems now enable multiplexed cloning of hundreds to thousands of gene variants in a single workflow, supporting library size expansion by over 40 % per annum in advanced service environments. Cloud-based design portals integrated with synthesis machines allow end-users to submit sequence constructs and receive real-time tracking, shortening lead-times by roughly 25 %. Microfluidic lab-on-chip systems are moving toward in-house synthesis solutions, enabling biotech firms to deploy mini gene-printers in-house rather than outsource; some designs claim 50 % footprint reduction compared with standard equipment. Error-correction technologies (such as enzymatic mismatch repair, next-generation sequencing verification) are now delivering error-rates under 0.5 % for full-length gene constructs, improving success-first-pass rates by more than 30 %. Another emerging trend is the integration of AI-driven sequence optimisation (codon usage, GC-content balancing, off-target minimisation) which reportedly raises first-pass synthesis success by approximately 32 %. The necessity for GMP-grade synthesis in therapeutic applications has pushed providers to adopt ISO 17025 certification, traceable chain-of-custody and robust biosecurity screening. As decision-makers evaluate synthesis partners, factors such as platform scalability, automation level, turnaround time, error-rate performance and IP-safe workflows are critical in selecting vendors aligned with growth-oriented synthetic biology and therapeutic programmes.

• In March 2024, Twist Bioscience announced expansion of its high-throughput gene-library synthesis facility in San Francisco, enabling delivery of up to 10 000 custom constructs per week and reducing lead-time by 20%. Source: www.twistbioscience.com

• In September 2023, GenScript Biotech opened a new automated gene-assembly line in Suzhou, China, capable of producing 5 kg of full-length gene constructs annually and supporting domestic biotech firms with local turnaround of under five days. Source: www.genscript.com

• In November 2024, Eurofins Scientific introduced a GMP-grade clonal DNA synthesis service with integrated quality-control analytics and chain-of-custody reporting tailored for gene-therapy developers, covering constructs up to 8 kb. Source: www.eurofins.com

• In June 2024, Thermo Fisher Scientific launched its cloud-connected gene-synthesis ordering portal which integrates AI-design and offers real-time assembly monitoring, reducing project-planning time by approximately 30%. Source: www.thermofisher.com

The scope of the clonal DNA synthesis market report encompasses a global examination of product types (including full-length gene constructs, gene fragments, variant libraries, plasmid back-bones), application areas (therapeutics development, synthetic biology, diagnostics, agriculture biotech, academic research) and end-user industries (pharmaceutical & biotechnology companies, academic/research institutes, contract development and manufacturing organisations (CDMOs), agricultural biotech firms and others). Geographic coverage spans North America, Europe, Asia-Pacific, South America and Middle East & Africa, with detailed country-level profiles for leading markets such as the United States, China, Germany, UK, India and Brazil. Technology segments analysed include solid-phase chemical synthesis, enzymatic synthesis, automated high-throughput assembly, microfluidic platforms and AI-driven design workflows. Market dynamics such as production capacity, service-model evolution, regional outsourcing trends, regulatory frameworks, biosecurity compliance and ESG-driven process innovations are addressed. The report further examines emerging niche segments, for example on-site synthesis-printers, decentralised biofoundries, custom variant-library services for synthetic biology and climate-smart agriculture gene applications. Strategic insights for decision-makers cover technological readiness, vendor assessments, investment patterns, competitive landscape and growth-opportunity mapping across region-specific demand patterns and service provider ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1,056.8 Million |

|

Market Revenue in 2032 |

USD 3,839.7 Million |

|

CAGR (2025 - 2032) |

17.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Thermo Fisher Scientific, Twist Bioscience, GenScript Biotech, Eurofins Scientific, Integrated DNA Technologies, Bioneer Corporation, GeneArt (Part of Thermo Fisher Scientific), OriGene Technologies Inc., Biomatik Corporation, ProteoGenix SAS, VectorBuilder Inc., Synbio Technologies, Azenta Life Sciences (Formerly Brooks Automation), Aldevron LLC |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |