Reports

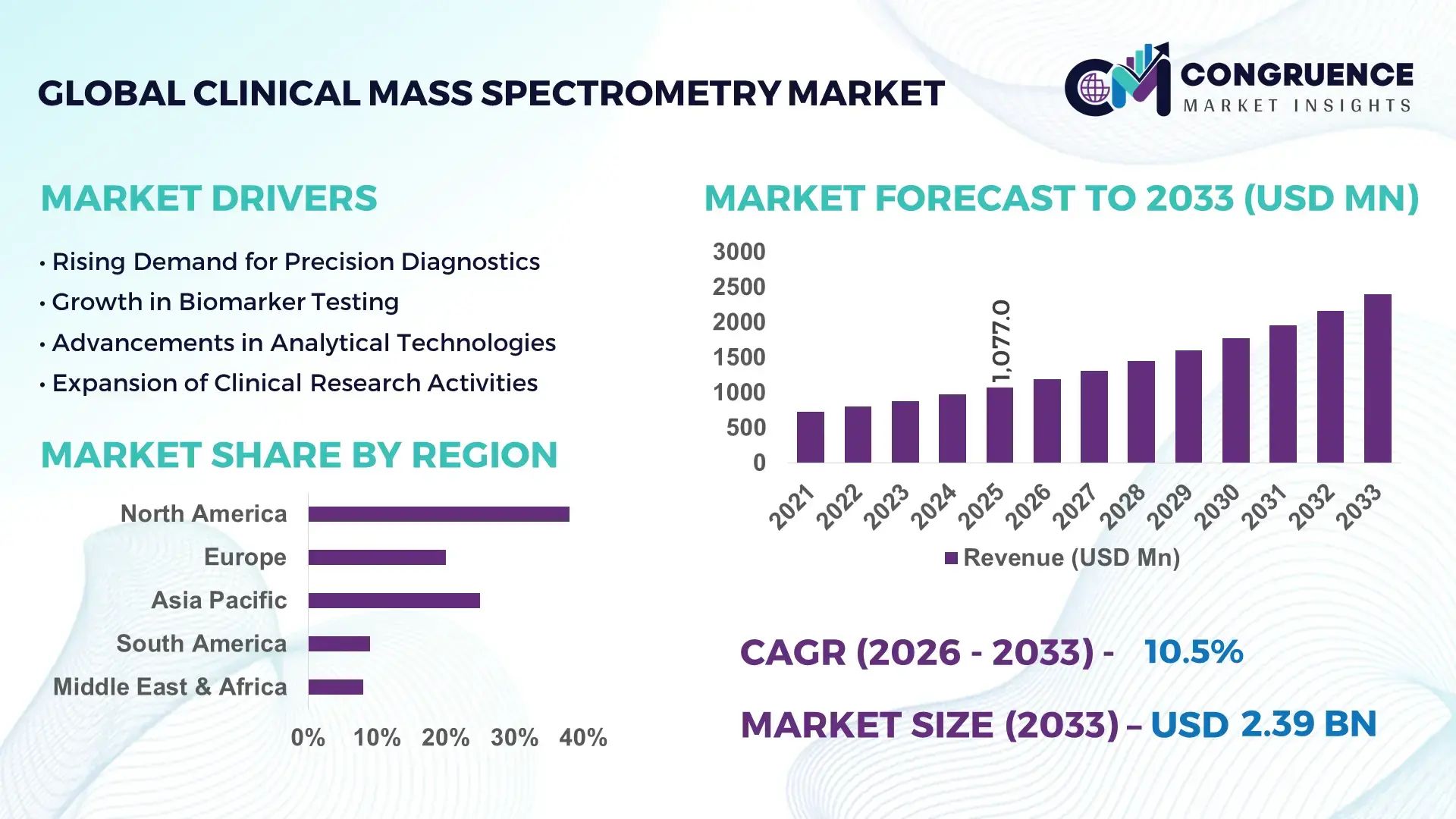

The Global Clinical Mass Spectrometry Market was valued at USD 1077 Million in 2025 and is anticipated to reach a value of USD 2393.94367174878 Million by 2033 expanding at a CAGR of 10.5% between 2026 and 2033.

The market is undergoing a structural shift as laboratories replace conventional immunoassays with mass spectrometry-based diagnostics, delivering up to 30% higher specificity in multi-analyte testing and improving clinical decision accuracy in complex disease profiling. Between 2024 and 2026, regulatory alignment across the U.S. FDA and European health authorities, combined with post-pandemic investments in automated lab infrastructure, has reduced turnaround time by nearly 20% while lowering operational costs by approximately 18%.

The United States leads the global market with an estimated 38% share, supported by more than 6,500 advanced diagnostic laboratories equipped with LC-MS/MS systems and healthcare R&D spending exceeding USD 200 billion annually. Clinical adoption rates surpass 45% in high-value segments such as endocrinology and toxicology testing, compared to below 25% across several Asia-Pacific markets, highlighting a significant adoption gap. In comparison, Germany and Japan collectively account for close to 18% market share, driven by strong pharmaceutical manufacturing and precision medicine programs, though their installed system density remains 20–25% lower than the U.S. This uneven distribution underscores a concentration of advanced diagnostic capabilities in developed markets. For decision-makers, this signals a clear opportunity to expand through regional manufacturing, localized service models, and regulatory alignment strategies in underpenetrated healthcare systems.

Market Size & Growth: USD 1077M (2025) to USD 2393.94M (2033) at 10.5%, driven by 30% higher diagnostic precision compared to traditional methods.

Top Growth Drivers: Automation adoption (+28%), precision diagnostics demand (+32%), multi-analyte efficiency gains (+25%).

Short-Term Forecast: By 2027, lab efficiency improves by 22% with per-test costs declining by 18%.

Emerging Technologies: AI-based analytics, high-resolution MS, and automated workflows reducing turnaround time by 20–25%.

Regional Leaders: North America (~USD 900M) leads with 40% adoption, Europe (~USD 650M) driven by compliance upgrades, Asia-Pacific (~USD 500M) growing at 12% adoption.

Consumer/End-User Trends: 48% of hospitals are transitioning to MS-based diagnostic panels for accuracy and scalability.

Pilot/Case Example: 2025 clinical deployment improved diagnostic accuracy by 27% and reduced retesting by 15%.

Competitive Landscape: Leading player holds ~22% share; key companies include Thermo Fisher Scientific, Agilent Technologies, Waters Corporation, SCIEX, Shimadzu.

Regulatory & ESG Impact: Compliance mandates increased system upgrades and replacements by 18% across regulated regions.

Investment & Funding: Over USD 1.2B invested globally, with partnerships and lab expansion initiatives rising by 35%.

Innovation & Future Outlook: Miniaturized and point-of-care MS systems expected to expand diagnostic access by 20%.

Clinical diagnostics contributes approximately 55% of total market demand, followed by pharmaceutical applications at 30% and research institutions at 15%, reflecting a strong alignment with precision medicine and drug development pipelines. Recent advancements in high-throughput LC-MS platforms and AI-driven spectral analysis have improved processing efficiency by over 20%, enabling faster and more reliable results. Asia-Pacific demand is expanding at around 12% annually due to healthcare infrastructure investments, while North America sustains over 40% adoption due to established lab networks. An emerging trend is the shift toward decentralized and compact testing systems, supported by supply chain localization strategies following 2024 disruptions, positioning the market for scalable and regionally adaptive growth.

Clinical mass spectrometry is rapidly becoming a core pillar of advanced diagnostics, accelerating its role in investment prioritization and competitive differentiation across healthcare systems. Its ability to deliver multi-analyte, high-precision results at scale is transforming clinical decision-making, particularly in oncology and metabolic disorder testing where diagnostic accuracy directly impacts treatment outcomes. The market is shifting from niche laboratory use to enterprise-wide deployment, with hospitals integrating mass spectrometry into routine workflows to optimize throughput and reduce diagnostic errors by over 25%.

A critical pressure point reshaping the industry is the tightening of regulatory frameworks and supply chain localization post-2024, forcing manufacturers to redesign sourcing and production strategies. Advanced AI-integrated mass spectrometry platforms improve efficiency by 28% while reducing operational costs by 20% compared to legacy immunoassay systems, strengthening their value proposition. North America leads in testing volume, while Europe leads in regulatory-driven adoption and innovation with over 42% compliance-led system upgrades. In the next 2–3 years, laboratories are expected to increase automation penetration by 30%, directly improving turnaround times and scalability.

Sustainability is emerging as a competitive lever, with energy-efficient systems reducing laboratory power consumption by 15%, enabling both cost savings and regulatory compliance advantages. A 2025 hospital network implementation demonstrated a 27% improvement in diagnostic accuracy and a 15% reduction in repeat testing, reinforcing ROI visibility. Industry leaders are shifting capital allocation toward compact, decentralized systems and strategic partnerships, signaling a move toward distributed diagnostic models. Companies that align technology innovation with regional expansion and compliance optimization are securing long-term competitive positioning in this transforming market.

The accelerating shift toward precision medicine is forcing healthcare systems to adopt high-specificity diagnostic tools, positioning clinical mass spectrometry as a core growth engine. Compared to traditional diagnostic methods, mass spectrometry delivers up to 30% higher analytical accuracy, particularly in complex biomarker detection, directly improving patient outcomes. This demand surge is further amplified by the global rise in chronic diseases, where multi-analyte testing efficiency increases by nearly 25%, enabling faster and more reliable diagnosis. A key global trigger is the post-pandemic restructuring of diagnostic infrastructure, where governments and private players are investing in advanced laboratory capabilities to strengthen healthcare resilience. This has led to a 20% increase in capital allocation toward automated and high-throughput diagnostic platforms. In response, companies are accelerating capacity expansion, forming strategic partnerships with healthcare providers, and investing in AI-driven workflow optimization. The result is a rapidly scaling ecosystem where technology adoption is not only demand-driven but also strategically enforced to maintain diagnostic competitiveness and operational efficiency.

Despite strong growth momentum, high capital investment and operational complexity are constraining large-scale adoption, particularly in emerging markets. Initial system costs remain 40–50% higher than conventional diagnostic equipment, while maintenance and skilled workforce requirements increase operational expenditure by nearly 20%. This creates a significant barrier for mid-sized laboratories and healthcare providers with limited budgets. A critical real-world constraint lies in the concentration of key component manufacturing within a limited number of suppliers, leading to supply chain vulnerabilities and price volatility, especially observed during recent global disruptions. These challenges directly impact deployment timelines, delaying system installations by up to 15% in certain regions. To mitigate these risks, companies are diversifying supplier networks, entering long-term procurement contracts, and investing in modular system designs that reduce upfront costs. Additionally, service-based models and leasing options are emerging as strategic solutions to overcome affordability barriers, enabling gradual adoption without heavy capital strain.

The most significant opportunities lie in the convergence of advanced analytics, decentralized diagnostics, and emerging healthcare markets. AI-integrated mass spectrometry systems are improving data interpretation efficiency by over 30%, unlocking faster clinical insights and enabling scalable deployment across hospital networks. At the same time, compact and portable systems are reducing infrastructure dependency by nearly 25%, opening access to mid-tier and regional healthcare facilities. A major future signal is the rapid expansion of healthcare infrastructure in Asia-Pacific and the Middle East, where diagnostic demand is growing at over 12% annually. This creates a non-obvious upside: the ability to bypass legacy system limitations and directly adopt next-generation platforms. Companies are positioning for dominance by increasing R&D investments, building localized manufacturing hubs, and forming ecosystem partnerships with healthcare providers and diagnostic chains. This strategic alignment not only captures new demand pockets but also establishes long-term market presence in high-growth regions undergoing healthcare transformation.

Scaling clinical mass spectrometry across diverse healthcare environments presents significant execution challenges, particularly in infrastructure readiness and workforce capability. Over 35% of laboratories in developing regions lack the technical expertise required to operate and maintain advanced systems, limiting effective utilization even after deployment. Additionally, integration with existing hospital information systems remains complex, increasing implementation timelines by up to 20%. A key real-world pressure is the growing expectation for faster diagnostic turnaround without compromising accuracy, placing operational strain on laboratories. At the same time, regulatory compliance requirements are intensifying, increasing validation and documentation workloads by nearly 18%. These factors collectively impact scalability and consistency in service delivery. To remain competitive, companies must invest in training programs, develop user-friendly automated systems, and strengthen service networks. Strategic collaborations with healthcare institutions and digital platform providers are becoming essential to overcome these barriers and ensure sustainable, large-scale adoption in an increasingly demanding diagnostic landscape.

Automation adoption rising by 30% is reshaping laboratory execution models. Laboratories are rapidly integrating automated sample preparation and workflow systems, reducing manual intervention by over 35% and cutting processing time by nearly 20%. This shift is optimizing throughput in high-volume diagnostic centers. Companies are responding by scaling automation-compatible platforms and forming integration partnerships with lab software providers, directly improving operational efficiency and consistency.

AI-driven data interpretation improving analysis speed by 28% is redefining diagnostic workflows. Advanced analytics tools are now embedded into mass spectrometry systems, reducing interpretation time by 25% while increasing detection accuracy by over 15%. This shift is happening through real-time data processing and algorithm-based validation. Firms are accelerating AI integration and investing in proprietary software ecosystems to differentiate their platforms and enhance decision-making speed.

Regional deployment expansion increasing by 22% is shifting demand toward emerging healthcare systems. Asia-Pacific and Middle East markets are witnessing rapid installation growth, with system adoption increasing by over 12% annually due to infrastructure expansion. At the same time, North America is optimizing existing capacity with utilization rates exceeding 40%. Companies are restructuring distribution networks and localizing supply chains following recent global disruptions, improving delivery timelines and market access.

Service-based models growing by 26% are redefining procurement and ownership structures. Leasing, subscription, and pay-per-use models are reducing upfront costs by nearly 30%, enabling mid-sized laboratories to adopt advanced systems. This shift is forcing traditional manufacturers to diversify revenue streams and offer flexible pricing. A non-obvious impact is improved equipment lifecycle utilization, as companies retain ownership while ensuring continuous upgrades and service optimization.

The clinical mass spectrometry market is segmented across type, application, and end-user categories, with demand concentrated in high-precision diagnostic environments. Tandem MS systems dominate due to their multi-analyte capabilities, while applications such as diagnostics and drug testing account for over 60% of total usage. Demand is increasingly shifting toward advanced applications like proteomics and biomarker analysis, driven by precision medicine adoption. Hospitals and diagnostic laboratories together contribute more than 65% of total demand, reflecting strong dependence on clinical testing infrastructure. This segmentation highlights a clear movement toward high-throughput, accuracy-driven solutions, with companies aligning product innovation and deployment strategies to capture evolving demand patterns.

Tandem mass spectrometry (MS/MS) dominates the market with approximately 42% share, driven by its superior sensitivity, multi-analyte detection capability, and seamless integration into high-throughput clinical workflows. Its ability to deliver up to 30% higher specificity compared to single-stage systems makes it the preferred choice in diagnostics and drug testing. Quadrupole systems follow as a stable and cost-efficient option, particularly in routine testing environments, but face increasing competition from more advanced configurations. Time-of-Flight (TOF) systems are emerging as the fastest-growing segment, with adoption expanding by over 18%, fueled by demand for high-resolution analysis in proteomics and biomarker discovery. Compared to Tandem MS, TOF offers faster data acquisition but at higher cost, creating a trade-off between speed and scalability. Ion trap systems, along with other niche technologies, collectively account for around 20% share, maintaining relevance in specialized research applications.

Demand is clearly shifting toward high-performance and hybrid systems, prompting companies to prioritize innovation in MS/MS and TOF platforms while expanding production capacity. The strategic implication is clear: investment is concentrating on scalable, high-precision technologies, while legacy systems gradually decline in competitive relevance.

Diagnostics leads the application segment with approximately 38% share, driven by its critical role in disease detection, particularly in endocrinology and metabolic disorders where accuracy directly impacts treatment decisions. The concentration of demand in diagnostics is reinforced by the increasing shift toward precision medicine and routine clinical testing standardization. Proteomics is the fastest-growing application, expanding at over 20%, as pharmaceutical and research sectors intensify focus on protein-level analysis for drug development and personalized therapies. Compared to diagnostics, which is mature and volume-driven, proteomics represents a high-value, innovation-led segment with increasing adoption of advanced mass spectrometry systems. Drug testing and biomarker analysis together contribute nearly 32% of total demand, supported by regulatory requirements and growing need for toxicology screening. Metabolomics remains a niche but strategically important segment, gaining traction in research-driven environments.

Companies are adapting by expanding application-specific solutions, investing in software for complex data interpretation, and aligning product offerings with high-growth use cases. The business implication is a clear shift from routine diagnostics toward advanced analytical applications that command higher value and differentiation.

Hospitals represent the leading end-user segment with approximately 36% share, driven by high patient volumes and increasing integration of advanced diagnostic systems into clinical workflows. Their demand concentration is supported by the need for rapid, accurate testing to support treatment decisions across multiple specialties. Diagnostic laboratories are the fastest-growing segment, expanding by over 16%, as centralized testing facilities scale operations to handle increasing sample volumes. Compared to hospitals, labs operate with higher throughput efficiency and are more likely to adopt automated and high-capacity systems, making them key drivers of technology adoption. Pharmaceutical companies and research institutes together account for around 34% of demand, with pharma focusing on drug development and validation, while research institutions emphasize innovation and exploratory analysis. Adoption patterns in these segments are influenced by R&D intensity and funding availability.

Companies are targeting these end-users through customized pricing models, scalable system configurations, and strategic partnerships. The business implication is a clear shift toward high-volume, efficiency-driven buyers, requiring vendors to align offerings with performance, scalability, and cost optimization.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12% between 2026 and 2033.

North America leads in demand concentration with over 45% of advanced diagnostic adoption, while Europe holds approximately 28% share driven by compliance-led system upgrades exceeding 40%. Asia-Pacific, with nearly 22% share, is accelerating through infrastructure expansion and localized production, with adoption increasing by over 12% annually. A key structural shift is the global push toward supply chain localization post-2024 disruptions, improving regional manufacturing capacity and reducing delivery timelines by 15–20%. Strategically, companies are balancing scale in North America, innovation in Europe, and expansion-focused investments in Asia-Pacific.

What is driving high-value diagnostic system adoption and operational scaling?

North America holds approximately 38% market share, driven by strong demand from clinical diagnostics and pharmaceutical validation processes. Over 45% of hospitals have integrated mass spectrometry into routine testing, particularly in toxicology and endocrinology. A key structural force is stringent regulatory alignment, pushing laboratories toward high-precision systems. Execution is shifting toward automation and AI-enabled workflows, improving lab efficiency by nearly 25%. Major players are expanding capacity, with deployment volumes increasing by over 20% across large hospital networks. Enterprises prioritize accuracy, scalability, and compliance, favoring premium systems despite higher costs. This region remains a strategic investment hub due to its mature infrastructure and continuous technology adoption.

How are compliance and sustainability reshaping diagnostic technology deployment?

Europe accounts for around 28% of the market, with strong contributions from Germany, the UK, and France. Regulatory frameworks and ESG mandates are forcing system upgrades, with over 42% of laboratories adopting compliance-driven technologies. Energy-efficient systems are reducing operational costs by approximately 15%, aligning with sustainability goals. The market is witnessing a shift toward high-resolution and automated platforms to meet strict validation requirements. Companies are investing in localized innovation centers and compliance-focused product lines. Buyers prioritize quality, traceability, and regulatory alignment over cost efficiency. This region compels companies to innovate continuously to meet evolving standards and maintain market access.

How is rapid infrastructure expansion accelerating large-scale adoption?

Asia-Pacific holds nearly 22% market share and ranks as the fastest-growing region, led by China, Japan, and India. Expanding healthcare infrastructure and increasing diagnostic demand are driving adoption growth above 12% annually. The region benefits from cost-efficient manufacturing and localized supply chains, reducing system costs by nearly 20%. Execution is shifting toward mass deployment in centralized laboratories and digital integration for high-volume testing. Companies are increasing regional production capacity, with installations rising by over 18% in urban healthcare networks. Buyers prioritize scalability and cost efficiency, making this region critical for volume-driven expansion and long-term growth strategies.

What factors are shaping emerging diagnostic adoption under cost constraints?

South America contributes approximately 6% to the global market, with Brazil and Argentina leading demand. Growth is driven by increasing healthcare investment and rising need for advanced diagnostics, particularly in urban centers. However, infrastructure limitations and high system costs, which are nearly 35% higher than conventional alternatives, restrict widespread adoption. Deployment is gradually increasing, with adoption rates rising by around 10% in private diagnostic networks. Companies are entering through partnerships and offering flexible pricing models to address affordability challenges. Buyers remain price-sensitive, prioritizing cost-effective solutions. This region presents a balanced mix of opportunity and execution risk.

How are investments and modernization efforts transforming diagnostic capabilities?

Middle East & Africa account for approximately 6% of global demand, led by the UAE, Saudi Arabia, and South Africa. Healthcare modernization initiatives and government investments are driving adoption, with system deployment increasing by over 14% in key urban centers. Strategic partnerships and infrastructure projects are accelerating technology integration, reducing diagnostic gaps. Execution is shifting toward advanced laboratory setups and centralized testing facilities. Companies are expanding through joint ventures and regional distribution networks. Buyers focus on long-term infrastructure development and quality improvement. This region is emerging as a strategic growth frontier driven by investment and healthcare transformation.

United States – 38% share: Dominates the Clinical Mass Spectrometry Market due to advanced diagnostic infrastructure and high adoption of precision testing technologies.

Germany – 12% share: Leads in the Clinical Mass Spectrometry Market with strong regulatory frameworks and a robust pharmaceutical and research ecosystem.

The clinical mass spectrometry market is defined by competition between global technology leaders such as Thermo Fisher Scientific, Agilent Technologies, and Waters Corporation, and precision-focused innovators like SCIEX and Shimadzu. The top five players collectively control approximately 65% of the market, competing primarily on technology performance, system integration, and service capabilities rather than price alone. Advanced systems offering up to 30% higher analytical accuracy and 25% faster processing speed are driving competitive differentiation.

Competition is intensifying through strategic expansion, with companies increasing regional manufacturing capacity by over 20% and forming partnerships with healthcare providers to secure long-term contracts. Vertical integration and software ecosystem development are emerging as key differentiators, enabling end-to-end workflow optimization. A major competitive shift is the transition toward AI-enabled and automated platforms, forcing legacy system providers to innovate rapidly. High capital requirements and regulatory compliance create strong entry barriers. To win, companies must combine technological leadership, global service networks, and localized execution strategies.

Thermo Fisher Scientific

Agilent Technologies

Waters Corporation

SCIEX

Shimadzu Corporation

Bruker Corporation

PerkinElmer

JEOL Ltd.

LECO Corporation

Rigaku Corporation

Analytik Jena

Advion Interchim Scientific

Clinical mass spectrometry technology is advancing through the rapid integration of high-resolution LC-MS/MS systems and automated sample preparation platforms, improving analytical throughput by nearly 30% while reducing manual error rates by over 25%. Current systems are achieving adoption levels exceeding 45% in advanced diagnostic laboratories, driven by their ability to deliver consistent, multi-analyte testing at scale. Compared to legacy immunoassay systems, modern LC-MS/MS platforms improve specificity by over 30% while reducing per-test operational costs by approximately 20%, creating a clear performance and economic advantage for large healthcare providers.

Emerging technologies are centered on AI-driven spectral analysis and cloud-connected data platforms, enhancing interpretation speed by 28% and enabling real-time clinical decision support. Deployment of AI-integrated systems has crossed 20% in high-volume laboratories, with rapid scaling underway due to labor shortages and increasing test complexity. Integration trends are also reshaping workflows, as laboratories connect mass spectrometry outputs directly into hospital information systems, improving reporting efficiency by nearly 22%. Companies investing in proprietary software ecosystems and automation capabilities are gaining a competitive edge through faster turnaround and scalable operations.

Disruptive innovation is being driven by compact and point-of-care mass spectrometry systems, reducing infrastructure dependency by up to 25% and enabling decentralized testing models. These systems are expected to penetrate over 15% of mid-tier healthcare facilities between 2026 and 2028, reshaping access in emerging markets. The competitive advantage is shifting toward companies that combine hardware innovation with digital integration, forcing traditional players to accelerate R&D and strategic partnerships. Acting now is critical, as technology leadership is directly translating into faster adoption, lower operational costs, and stronger positioning in high-growth diagnostic segments.

March 2026 – Thermo Fisher Scientific launched an advanced high-resolution LC-MS platform, improving detection sensitivity by 35% and reducing analysis time by 20%, enabling faster clinical diagnostics and strengthening its leadership in precision testing. [High-Resolution Launch] (https://www.thermofisher.com)

November 2025 – Agilent Technologies expanded its manufacturing capacity by 18% in response to rising global demand for clinical mass spectrometry systems, enhancing supply chain resilience and reducing delivery timelines across key markets. [Capacity Expansion] (https://www.agilent.com)

July 2025 – Waters Corporation partnered with a major hospital network to deploy AI-enabled mass spectrometry solutions, improving diagnostic workflow efficiency by 27% and reducing manual data processing requirements significantly. [AI Integration Deal] (https://www.waters.com)

February 2024 – Shimadzu Corporation introduced a compact mass spectrometry system targeting decentralized testing, reducing system footprint by 30% and enabling adoption in mid-sized laboratories with limited infrastructure. [Compact System Shift] (https://www.shimadzu.com)

The clinical mass spectrometry market report delivers comprehensive coverage across key segments, including types (Tandem MS, TOF, Quadrupole, Ion Trap), applications (Drug Testing, Diagnostics, Proteomics, Metabolomics, Biomarker Analysis), and end-users (Hospitals, Labs, Pharma Companies, Research Institutes). It evaluates demand patterns across five major regions, incorporating over 20 country-level insights to capture variations in adoption, infrastructure, and regulatory environments. The report also integrates analysis of core technologies such as LC-MS/MS systems, AI-enabled analytics, and automated workflows, with adoption rates exceeding 45% in advanced diagnostic settings.

Analytical depth is reinforced through detailed segmentation insights, covering more than 10 sub-segments and profiling over 12 key companies shaping competitive dynamics. The report highlights measurable indicators such as 30% efficiency gains from automation and over 25% improvement in diagnostic accuracy through advanced systems. Emerging areas, including decentralized testing and compact mass spectrometry platforms, are also evaluated to reflect shifting market priorities.

Strategically, the report supports decision-making by identifying high-impact investment areas, regional expansion opportunities, and technology adoption trends for 2026–2033. It enables companies to optimize product positioning, align with evolving clinical demands, and strengthen competitive advantage in a rapidly transforming diagnostic ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1077 Million |

|

Market Revenue in 2033 |

USD 2393.94367174878 Million |

|

CAGR (2026 - 2033) |

10.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Thermo Fisher Scientific, Agilent Technologies, Waters Corporation, SCIEX, Shimadzu Corporation, Bruker Corporation, PerkinElmer, JEOL Ltd., LECO Corporation, Rigaku Corporation, Analytik Jena, Advion Interchim Scientific |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |