Reports

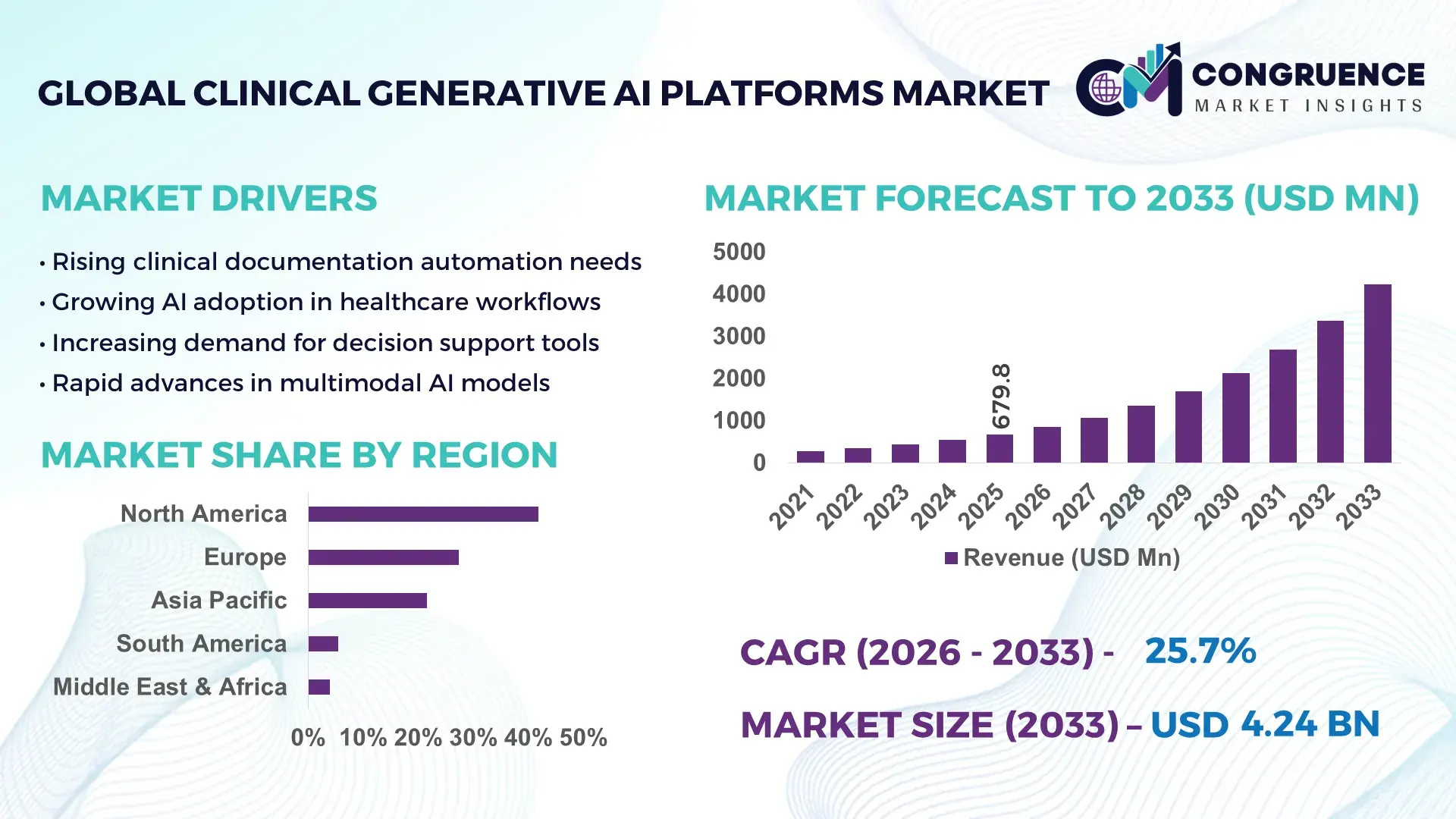

The Global Clinical Generative AI Platforms Market was valued at USD 679.8 Million in 2025 and is anticipated to reach a value of USD 4,237.0 Million by 2033 expanding at a CAGR of 25.7% between 2026 and 2033, according to an analysis by Congruence Market Insights. This expansion is driven by accelerated adoption of AI-powered clinical decision support, automated documentation, and real-time diagnostic assistance across healthcare delivery systems.

The United States represents the most advanced ecosystem for Clinical Generative AI Platforms, supported by large-scale healthcare digitization and AI infrastructure maturity. Over 72% of major U.S. hospital networks have deployed or piloted generative AI solutions for clinical documentation, triage, or decision support. Annual investment in healthcare AI platforms exceeded USD 6.8 billion, with clinical AI accounting for a substantial portion. More than 60 AI-native healthcare platforms are actively deployed across U.S. clinical environments, supporting applications such as radiology reporting, discharge summaries, and patient interaction automation. Adoption among large provider systems exceeds 44%, while nearly 38% of clinicians report daily interaction with generative AI tools embedded in EHR workflows.

Market Size & Growth: Valued at USD 679.8 Million in 2025, projected to reach USD 4,237.0 Million by 2033 at a CAGR of 25.7%, supported by AI-driven clinical productivity gains.

Top Growth Drivers: Clinical workflow automation (41%), AI-assisted diagnostics adoption (34%), clinician efficiency improvement (29%).

Short-Term Forecast: By 2028, clinical documentation time per physician is expected to decline by 32%.

Emerging Technologies: Multimodal foundation models, generative clinical copilots, synthetic medical data generation.

Regional Leaders: North America (USD 1,680 Million by 2033; EHR-integrated AI), Europe (USD 1,210 Million; compliance-driven adoption), Asia Pacific (USD 980 Million; hospital digitization).

Consumer/End-User Trends: Hospitals and integrated delivery networks represent over 46% of deployments.

Pilot or Case Example: In 2024, a national hospital pilot reduced clinical note completion delays by 38%.

Competitive Landscape: Microsoft–Nuance (~19%), followed by Epic, Google Health, Oracle Health, and IBM.

Regulatory & ESG Impact: Expansion of AI governance frameworks and clinical safety mandates.

Investment & Funding Patterns: Over USD 9.5 billion invested globally since 2022 in clinical GenAI platforms.

Innovation & Future Outlook: Growth in AI-native clinical operating systems and embedded care copilots.

Clinical generative AI platforms serve hospitals (48%), outpatient clinics (27%), and life science organizations (25%). Innovations in multimodal clinical reasoning, regulatory-aligned model validation, and secure deployment frameworks are reshaping adoption. North America leads institutional deployment, while Asia Pacific shows rapid clinician onboarding. Future momentum will be driven by real-time decision intelligence, regulatory harmonization, and scalable AI infrastructure.

The Clinical Generative AI Platforms Market is strategically redefining healthcare operations by embedding intelligence directly into clinical workflows. These platforms enable real-time documentation, diagnostic synthesis, and decision augmentation, reducing clinician cognitive load while improving care consistency. Multimodal foundation models deliver up to 36% improvement in diagnostic summarization accuracy compared to rule-based clinical decision systems, enabling faster and more reliable care delivery.

From a regional standpoint, North America dominates in deployment volume, while Europe leads in enterprise-grade adoption with nearly 52% of large healthcare organizations actively using regulated clinical AI platforms. By 2027, generative clinical copilots are expected to improve clinician productivity by 30%, particularly in documentation-intensive specialties such as primary care and radiology. ESG considerations are becoming central, with firms committing to 25% reductions in clinician overtime hours and 20% lower burnout indices by 2030 through AI-enabled workflow optimization.

A measurable micro-scenario emerged in 2024, when a U.S. academic hospital system deployed a generative AI documentation assistant, achieving a 34% reduction in physician after-hours charting within six months. Looking forward, the Clinical Generative AI Platforms Market is positioned as a critical pillar for healthcare system resilience, regulatory-aligned innovation, and sustainable digital transformation.

The Clinical Generative AI Platforms Market dynamics are shaped by clinician shortages, rising documentation burdens, and the need for real-time clinical intelligence. Healthcare systems are increasingly shifting from fragmented AI tools to unified generative platforms embedded within EHR environments. Advances in multimodal data processing, including text, imaging, and structured records, are expanding clinical use cases. However, regulatory oversight, data privacy constraints, and model validation requirements continue to influence deployment strategies. Overall, the Clinical Generative AI Platforms Market is evolving toward secure, explainable, and workflow-native AI solutions.

Clinicians spend nearly 40% of their working hours on documentation and administrative tasks, limiting patient-facing care. Clinical generative AI platforms automate note generation, discharge summaries, and order recommendations, reducing documentation time by 30–45%. Hospitals deploying these platforms report faster patient throughput and improved clinician satisfaction scores. Growing demand for scalable productivity solutions amid workforce shortages continues to drive platform adoption across inpatient and outpatient settings.

Clinical AI platforms must comply with strict data privacy, safety, and transparency standards. Over 58% of healthcare organizations report delays in AI deployment due to governance reviews and model validation requirements. Concerns around hallucinated outputs and liability exposure necessitate extensive testing, slowing implementation timelines and increasing compliance costs.

More than 80% of hospitals globally use EHR systems, creating a large addressable base for embedded generative AI platforms. Native integration enables real-time clinical assistance, reducing context switching and improving adoption. Opportunities are emerging in specialty-specific copilots, population health analytics, and AI-assisted care coordination across value-based care models.

Deploying clinical-grade generative AI requires specialized AI engineering, clinical informatics expertise, and secure compute infrastructure. Nearly 46% of healthcare providers cite shortages in AI-skilled personnel as a deployment barrier. Infrastructure costs, interoperability complexity, and change management further challenge large-scale rollouts.

Rapid Expansion of Clinical Documentation Copilots: Over 62% of new platform deployments focus on AI-assisted documentation, reducing physician note completion times by 35% and improving record consistency.

Growth of Multimodal Clinical Reasoning Models: Platforms combining text, imaging, and structured data have improved diagnostic correlation accuracy by 29%, supporting complex clinical decision-making.

Enterprise-Grade Governance and Explainability: Approximately 54% of healthcare organizations now require built-in explainability and audit logs, increasing trust and regulatory alignment.

Shift Toward AI-Native Clinical Operating Systems: More than 40% of large providers are transitioning from point AI tools to unified generative platforms, enabling scalable, system-wide intelligence deployment.

The Clinical Generative AI Platforms Market is segmented by type, application, and end-user, reflecting how generative intelligence is embedded across clinical workflows, care delivery models, and healthcare institutions. By type, platforms vary based on underlying model architecture and data modality integration, ranging from text-centric systems to multimodal and specialty-trained clinical models. Application segmentation highlights where value is being captured, particularly in documentation automation, clinical decision support, diagnostics, and patient engagement. End-user segmentation reveals adoption differences between hospitals, outpatient providers, life sciences organizations, and payers. Across all segments, adoption is strongly influenced by interoperability with EHR systems, regulatory readiness, and the ability to demonstrate measurable improvements in clinical efficiency, safety, and care quality.

Text-based large language models optimized for clinical workflows represent the leading product type, accounting for approximately 46% of total platform adoption. These systems are widely used for clinical documentation, discharge summaries, referral letters, and clinical note synthesis due to their ease of deployment and strong alignment with existing text-heavy EHR environments. Multimodal clinical generative AI platforms—capable of processing text, medical images, lab data, and structured patient records—hold around 32% of adoption, driven by their ability to support complex diagnostic and decision-making tasks. However, multimodal platforms are the fastest-growing type, expanding at an estimated 29.4% CAGR, as hospitals increasingly seek unified AI systems that reduce fragmentation across radiology, pathology, and clinical notes.

Specialty-trained generative models focused on domains such as oncology, cardiology, or radiology contribute the remaining 22% combined share, serving high-acuity and research-intensive use cases. While smaller in scale, these models offer higher clinical specificity and are increasingly embedded into enterprise platforms as modular capabilities.

• In 2025, a national academic medical network deployed a multimodal clinical generative AI system integrating radiology images and physician notes, reducing diagnostic review time by 27% across more than 200,000 patient cases.

Clinical documentation and workflow automation is the leading application segment, representing approximately 44% of overall platform usage, as healthcare organizations prioritize reducing administrative burden and clinician burnout. Clinical decision support applications account for around 28%, leveraging generative AI to summarize patient histories, flag risks, and assist treatment planning. Diagnostic and imaging support applications contribute about 18%, while patient engagement and virtual clinical assistance collectively represent the remaining 10%.

Among these, patient engagement and virtual assistance is the fastest-growing application, expanding at an estimated 31.2% CAGR, supported by rising demand for AI-powered triage, symptom assessment, and post-discharge follow-up. In 2025, over 42% of hospitals in the US reported piloting generative AI systems that combine clinical notes with imaging or lab data to support physician decision-making, while nearly 39% of healthcare enterprises globally indicated active trials of generative AI for patient-facing clinical interactions.

• In 2025, a public healthcare authority implemented generative AI-powered diagnostic support tools across more than 150 hospitals, improving early disease detection workflows for over 2 million patients.

Hospitals and integrated delivery networks are the leading end-user segment, accounting for approximately 48% of total adoption, due to their complex clinical workflows, high documentation volumes, and capacity to invest in enterprise-grade AI platforms. Outpatient clinics and physician groups represent around 27%, increasingly adopting generative AI to streamline visits and manage chronic care. Life sciences organizations and payers collectively account for the remaining 25%, using clinical generative AI for trial design, real-world evidence analysis, and utilization management.

Outpatient clinics are the fastest-growing end-user segment, expanding at an estimated 28.6% CAGR, driven by the need for scalable clinical support tools without large administrative teams. In 2025, over 38% of multi-specialty clinics reported piloting generative AI for visit documentation, while 42% of hospitals were testing AI platforms that combine radiology scans with structured patient records to enhance diagnostic workflows.

• In 2024, a national primary care network deployed a generative AI clinical assistant across 500 clinics, achieving a 33% reduction in physician documentation time within the first year.

North America accounted for the largest market share at 41.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 30.6% between 2026 and 2033.

Regional performance in the Clinical Generative AI Platforms Market varies significantly based on healthcare digitization maturity, regulatory frameworks, AI infrastructure readiness, and clinician adoption rates. Europe followed North America with a 27.3% share, supported by structured healthcare systems and strong compliance-driven AI deployment. Asia-Pacific held approximately 21.6%, but shows the highest momentum due to rapid hospital digitization, rising patient volumes, and government-backed AI programs. South America and the Middle East & Africa together accounted for nearly 9.3%, with adoption concentrated in urban healthcare networks and national digital health initiatives. Across regions, hospitals remain the primary adopters, representing over 45% of deployments globally, while outpatient and telehealth-driven platforms are expanding fastest in emerging economies.

The region commands approximately 41.8% of the global Clinical Generative AI Platforms Market share, driven by advanced healthcare IT infrastructure and early AI adoption. Demand is primarily fueled by hospitals, integrated delivery networks, and academic medical centers, which together account for over 62% of regional deployments. Regulatory frameworks supporting AI-enabled clinical decision tools and data interoperability standards have accelerated adoption. Technological trends include deep EHR integration, multimodal AI for diagnostics, and real-time clinical documentation tools. More than 70% of large hospitals have piloted or deployed generative AI systems for physician documentation. Local players are actively enhancing clinician-focused AI assistants to reduce administrative workloads. Consumer behavior reflects higher enterprise adoption, particularly in healthcare systems focused on productivity, patient safety, and clinician burnout reduction.

Europe holds close to 27.3% of the global market share, with Germany, the UK, and France collectively contributing over 58% of regional adoption. The market is shaped by strong regulatory oversight, encouraging explainable and auditable AI models for clinical use. Healthcare providers increasingly prioritize transparency, data privacy, and validation, influencing platform design. Adoption of generative AI is strongest in public hospitals and research institutions, accounting for nearly 54% of deployments. Emerging technologies such as federated learning and privacy-preserving AI are gaining traction. Regional players are focusing on clinically validated language models aligned with regulatory expectations. Consumer behavior in Europe reflects higher demand for compliant, interpretable AI systems that align with strict governance requirements.

Asia-Pacific ranks as the fastest-growing region, representing approximately 21.6% of global market volume. China, India, and Japan together account for over 65% of regional consumption, driven by large patient populations and rapid hospital digitization. Infrastructure investments in smart hospitals and national AI health platforms are accelerating adoption. More than 48% of tertiary hospitals in major urban centers have initiated generative AI pilots for diagnostics and documentation. Regional innovation hubs are advancing multilingual clinical models to address language diversity. Local players are deploying mobile-first AI clinical assistants to support high outpatient volumes. Consumer behavior highlights growth driven by mobile health platforms, telemedicine, and AI-enabled clinical triage tools.

South America accounts for approximately 5.4% of the global market, with Brazil and Argentina contributing nearly 61% of regional adoption. Market growth is supported by gradual healthcare digitalization and government-backed health IT modernization programs. Infrastructure development in urban hospitals and private healthcare networks is driving early-stage AI deployment. Public-private partnerships are encouraging the use of generative AI for clinical documentation and patient communication. Local healthcare technology firms are integrating language-adaptive AI models to support multilingual clinical environments. Consumer behavior in the region shows demand linked to language localization, telehealth expansion, and improved access to specialist-level clinical insights.

The Middle East & Africa region represents approximately 3.9% of the global market, with the UAE and South Africa accounting for over 47% of regional demand. Adoption is driven by healthcare modernization programs, smart hospital initiatives, and national AI strategies. Technological trends include cloud-based clinical AI platforms and multilingual support systems. Governments are actively encouraging digital health investments through innovation-friendly regulations and cross-border partnerships. Regional healthcare groups are deploying generative AI to enhance clinical documentation and patient engagement. Consumer behavior reflects growing acceptance of AI-assisted care in urban centers, with demand focused on efficiency, accessibility, and digital-first healthcare services.

United States – 34.6% Market Share: Strong hospital digitization, advanced AI infrastructure, and high enterprise healthcare adoption.

China – 14.2% Market Share: Large-scale hospital networks, government-backed AI health initiatives, and high patient volumes driving deployment.

The Clinical Generative AI Platforms Market is moderately fragmented with a significant number of active competitors spanning technology giants, healthcare IT specialists, and innovative startups. Overall, there are 40+ globally active competitors developing clinical-grade generative AI solutions tailored for clinical documentation, decision support, diagnostic assistance, and patient engagement workflows. The combined share of the top 5 companies in this market is approximately 38–42%, indicating both the presence of leading players and meaningful competitive opportunities for emerging vendors. Strategic initiatives shaping competition include partnerships, platform integrations with EHR systems, and specialized product launches that embed generative AI deeply into clinical workflows. For example, major EHR vendors are embedding native generative AI assistants to automate clinical note creation and summary generation, while specialized startups are securing funding rounds and expanding product capabilities to address specific clinical use cases at scale. Healthcare providers increasingly choose solutions with interoperability, explainability, and compliance capabilities, making regulatory alignment and data governance critical competitive differentiators. Innovation trends include multimodal AI models capable of synthesizing text, imaging, and structured health data in real time, and AI copilots designed to function within clinical treatment pathways. Overall, competition is dynamic, with ongoing mergers, strategic alliances, and product expansions influencing market structure and vendor positioning in this evolving ecosystem.

IBM Watson Health

Oracle Health

Salesforce Health Cloud

Rad AI

Heidi Health

Honey Health

Abridge

OpenEvidence

Cognizant Healthcare AI

Philips HealthSuite AI

Counterforce Health

Technology in the Clinical Generative AI Platforms Market is rapidly progressing, with developments that directly improve clinical decision-making, documentation efficiency, and patient experience. Generative AI architectures now leverage multimodal model frameworks that can process text, medical imaging, structured records, and lab results in unified workflows. This allows clinicians to receive synthesized insights from diverse data types rather than isolated outputs. Adoption of retrieval-augmented generation frameworks enhances the relevance and clinical context of AI recommendations by retrieving and integrating historical patient data into generative outputs.

Ambient clinical intelligence systems—powered by advanced speech recognition, natural language understanding, and context-aware processing—are increasingly embedded in electronic health record (EHR) systems to automate documentation and reduce manual note-taking burdens. Text-to-code and AI-driven coding assistants streamline billing and compliance tasks. Semantic indexing and mega-structure platforms organize vast clinical datasets across diseases, enabling efficient data retrieval and clinical reasoning at scale with high accuracy measures exceeding 95% in complex cases.

Cloud-native AI microservices and API-driven model orchestration frameworks facilitate integration across healthcare IT stacks, enabling rapid deployment, scaling, and governance controls. Explainable AI modules and real-time audit logging are being incorporated to meet stringent clinical validation and regulatory requirements, while federated learning and privacy-preserving AI enable model improvement across institutions without moving sensitive patient data. These technological trends are reshaping how clinical workflows interact with generative AI, emphasizing interoperability, security, and actionable insights for frontline providers.

• In March 2025, Microsoft introduced the Dragon Copilot AI assistant designed to support clinical documentation and smart dictation within healthcare settings, featuring multilingual ambient note generation and task automation to reduce clinician administrative burden. Source: www.theverge.com

• In February 2025, Pittsburgh-based healthcare AI startup Abridge raised USD 250 million in funding to enhance its clinical documentation AI capabilities, expanding deployment across ~100 healthcare systems in the U.S. Source: www.reuters.com

• In December 2025, Bristol Myers Squibb, in collaboration with Accenture, launched Mosaic, a generative AI-powered medical content hub in Mumbai that accelerates physician education and patient-centric content generation. Source: www.timesofindia.indiatimes.com

• In January 2026, Variant Bio unveiled Inference, an agentic AI platform for drug discovery that processes genomic data and secured multi-year research collaborations with major pharmaceutical partners potentially exceeding USD 120 million in milestone payments. Source: www.reuters.com

The Clinical Generative AI Platforms Market Report provides a comprehensive analysis of the global landscape, articulating segmentation across product types, clinical applications, and end-user groups relevant to healthcare decision-makers. It examines platform types including text-centric language models, multimodal clinical AI systems, and specialty-trained solutions, detailing their technical capabilities, integration models, and deployment contexts. Application focus areas include clinical documentation automation, clinical decision support, diagnostic augmentation, patient engagement tools, and virtual care copilots, highlighting adoption patterns across acute care, outpatient, and specialized clinical environments. The report also outlines end-user adoption by hospitals, clinics, life sciences organizations, and payer systems, reflecting variations in clinical workflows, IT infrastructure, and budget allocation.

Geographically, the report analyzes regional markets including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering insights into differing adoption drivers, regulatory environments, and digital health maturity levels. It further explores emerging technology domains such as AI-native EHR integration, semantic search engines for clinical data, federated learning approaches, model governance frameworks, and explainable AI modules tailored to healthcare compliance. Strategic initiatives such as partnerships, platform enhancements, and AI ecosystem development are covered, providing decision-makers with actionable intelligence on competitive positioning and future-proofing strategies. By encompassing both macro-level market trends and fine-grained technological advancements, the report equips stakeholders with the breadth and depth of insights needed to evaluate investment, implementation, and innovation strategies in the evolving clinical generative AI landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 679.8 Million |

| Market Revenue (2033) | USD 4,237.0 Million |

| CAGR (2026–2033) | 25.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Microsoft Healthcare, Epic Systems, Google Cloud AI, IBM Watson Health, Oracle Health, Salesforce Health Cloud, Rad AI, Heidi Health, Honey Health, Abridge, OpenEvidence, Cognizant Healthcare AI, Philips HealthSuite AI, Counterforce Health |

| Customization & Pricing | Available on Request (10% Customization Free) |