Reports

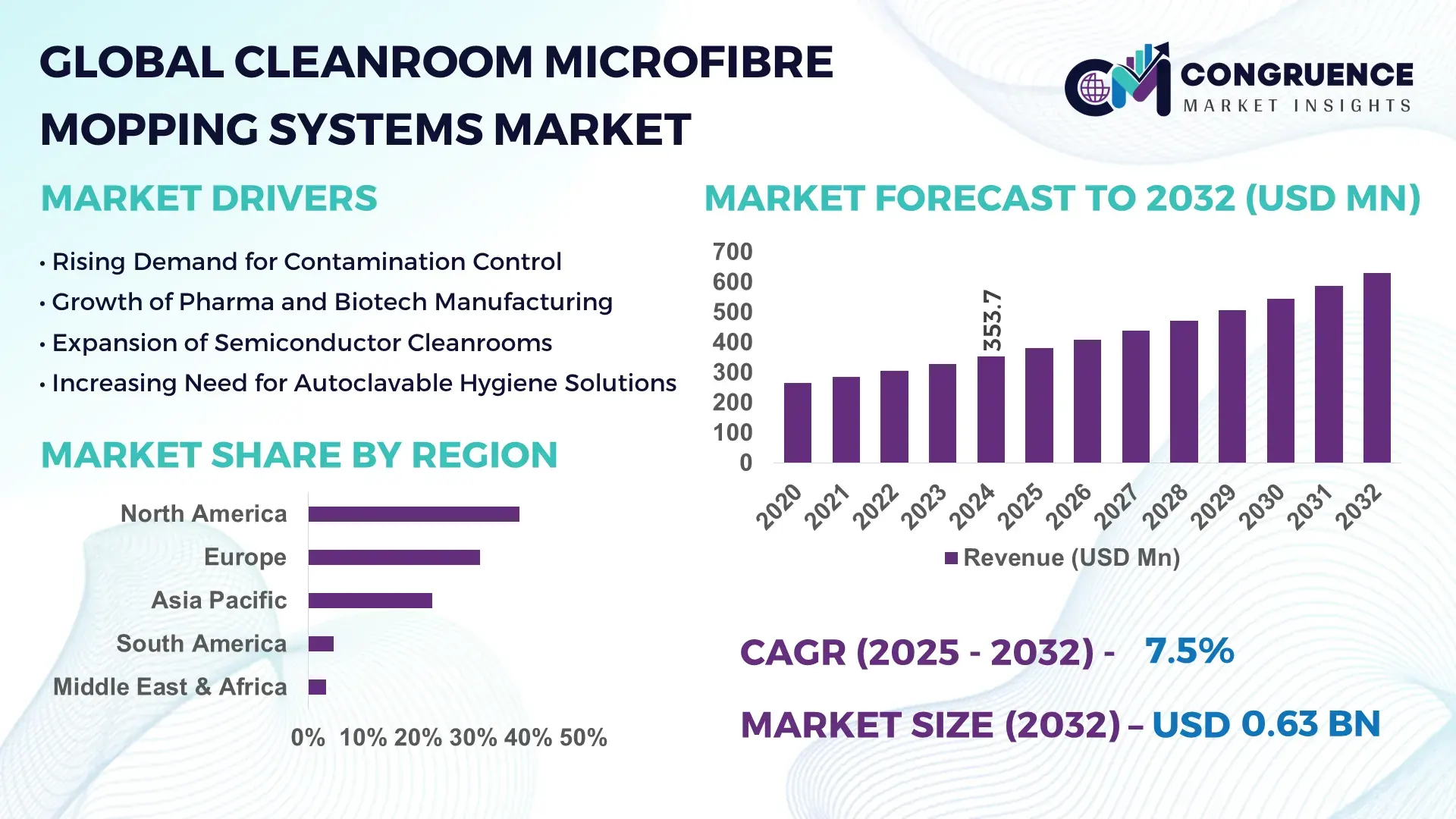

The Global Cleanroom Microfibre Mopping Systems Market was valued at USD 353.7 Million in 2024 and is anticipated to reach a value of USD 630.8 Million by 2032 expanding at a CAGR of 7.5% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is primarily driven by rising demand for contamination-controlled cleaning solutions across pharmaceutical, semiconductor, and high-precision manufacturing environments.

In the United States—one of the world’s most advanced cleanroom equipment hubs—investments in cleanroom infrastructure exceeded USD 4.2 billion in 2024, with over 38,000 active ISO-certified cleanroom facilities. Advanced microfibre systems are increasingly deployed across biotechnology and nanotechnology labs, where particle-capture efficiency above 95% is required. The country’s strong regulatory environment and rapid expansion of biologics manufacturing continue to boost demand for next-generation mopping systems with improved surface contact, enhanced lint-free performance, and high durability under repeated sterilization cycles.

Market Size & Growth: Valued at USD 353.7 million in 2024 and projected to reach USD 630.8 million by 2032, growing at 7.5% due to rising demand for sterile, low-lint cleaning technologies.

Top Growth Drivers: 41% increase in cleanroom construction, 32% rise in GMP-compliant cleaning protocols, and 27% improvement in microfibre efficiency are accelerating adoption.

Short-Term Forecast: By 2028, workflow efficiency in controlled environments is expected to improve by 22% through advanced microfibre designs and ergonomic mop handle systems.

Emerging Technologies: Multi-layered microfibre composites and autoclavable polymer-reinforced frames are gaining traction.

Regional Leaders: By 2032, North America is projected to reach USD 210 million, Europe USD 165 million, and Asia-Pacific USD 198 million with strong adoption in pharmaceuticals and electronics.

Consumer/End-User Trends: Pharma and semiconductor facilities continue to dominate usage, with over 58% adoption in critical environments in 2024.

Pilot or Case Example: In 2024, a leading biologics manufacturer implemented microfibre mopping automation, achieving a 29% reduction in particle contamination.

Competitive Landscape: A global market leader holds approximately 18% share, followed by 4–5 established players focusing on sterile cleaning innovations.

Regulatory & ESG Impact: Enhancements in ISO 14644 compliance and sustainability requirements are accelerating the shift toward reusable, long-life microfibre systems.

Investment & Funding Patterns: Over USD 620 million was invested in cleanroom infrastructure upgrades and sterile consumables between 2022 and 2024.

Innovation & Future Outlook: Antimicrobial microfibre coatings, IoT-enabled cleaning validation, and fully sterile interchangeable mop heads are expected to shape future market demand.

Cleanroom Microfibre Mopping Systems are increasingly used across pharmaceutical, semiconductor, and healthcare cleanrooms, contributing over 65% of total demand, driven by advances in microfibre absorption capacity, electrostatic particle capture, and compatibility with stringent ISO classifications. Rapid innovation in ergonomic mop frames and low-shedding textiles continues to enhance market expansion globally.

The Cleanroom Microfibre Mopping Systems Market plays a pivotal role in ensuring contamination control across highly regulated sectors such as pharmaceuticals, semiconductors, aerospace, and biotechnology. Modern microfibre systems offer superior particulate retention, with advanced split-fibre structures delivering up to 40% higher capture efficiency compared to traditional non-woven mop systems. Europe dominates in volume due to its strong pharmaceutical manufacturing base, while Asia-Pacific leads in adoption with over 62% of new cleanroom facilities integrating advanced microfibre systems. By 2027, automation-enabled mopping technologies are expected to reduce manual cleaning time by 28%, directly enhancing operational uptime.

New process-driven models are emerging where technology upgrades outperform legacy systems. For instance, electrostatic microfibre innovations deliver 35% better residue removal versus older cotton-based alternatives. ESG commitments are equally shaping purchasing decisions, with major pharmaceutical firms targeting a 30% reduction in single-use cleaning materials by 2030. In 2024, a major semiconductor manufacturer in Taiwan achieved a 21% reduction in cross-contamination incidents through the deployment of precision-engineered microfibre mop heads.

As cleanroom specifications become more stringent, companies increasingly adopt validated mopping systems that meet ISO 14644 and GMP standards. By 2028, AI-enabled cleaning validation tools integrated into microfibre systems are expected to reduce compliance reporting time by 25%. Overall, the Cleanroom Microfibre Mopping Systems Market stands as a key enabler of resilient, compliant, and sustainable controlled-environment operations worldwide.

The Cleanroom Microfibre Mopping Systems Market is shaped by evolving regulatory mandates, rapid cleanroom expansion, and the rising need for high-efficiency contamination control tools. The surge in biologics and semiconductor production is accelerating demand for microfibre solutions that offer superior particle capture, chemical resistance, and autoclave durability. Continuous innovation in textile engineering, including multi-layer fibre structuring and reduced-lint materials, enhances adoption across controlled environments. At the same time, stringent GMP, FDA, and ISO 14644 standards are prompting end-users to shift from traditional cotton and sponge mops to validated microfibre systems. These market forces collectively reinforce steady growth, supported by increased global investments in sterile manufacturing infrastructure.

The rapid expansion of global pharmaceutical and semiconductor production is significantly driving demand for advanced Cleanroom Microfibre Mopping Systems. With more than 72% of new cleanroom facilities in 2024 designed for ISO 5–ISO 7 operations, the need for ultralow-lint, high-absorption microfibre systems has intensified. Semiconductor fabs require particulate contamination below 100 particles/ft³, making microfibre mops essential for maintaining wafer integrity. In pharmaceuticals, sterile injectables and biologics manufacturing increased by 18% in 2023–2024, creating strong demand for GMP-compliant cleaning tools. Modern microfibre systems provide up to 40% better particle retention and 30% longer lifespan compared to conventional systems, enabling firms to meet regulatory standards while improving operational efficiency. These factors collectively reinforce strong market momentum.

The Cleanroom Microfibre Mopping Systems Market faces constraints primarily due to the higher cost of sterile-grade microfibre systems, driven by rigorous manufacturing standards and material specifications. Sterile microfibre mop heads are subjected to gamma irradiation or steam sterilization compatibility testing, increasing production complexity and cost. Price differentials can exceed 45% compared to standard non-cleanroom mops, creating budget challenges for smaller facilities. Additionally, the requirement for frequent validation, documentation, and controlled storage adds overhead expenses. Replacement cycles for high-grade mop heads—often every 20 to 25 cleaning cycles in ISO 5 environments—further contribute to operating costs. These cumulative expenses may slow adoption, especially in emerging markets with limited capital investment capacity.

The rapid expansion of cleanroom infrastructure worldwide presents a substantial opportunity for the Cleanroom Microfibre Mopping Systems Market. Over 4,500 new cleanroom construction projects were announced globally between 2022 and 2024, with Asia-Pacific accounting for nearly 48% of them. These new facilities increasingly demand advanced microfibre mopping solutions capable of achieving up to 99% particle removal efficiency. The rise of biologics, mRNA manufacturing, precision electronics, and medical device production further expands the addressable market. Manufacturers are introducing autoclavable, ergonomic, and polymer-reinforced mops to meet diverse cleanroom requirements. As more companies adopt sustainable cleaning protocols, reusable microfibre systems with extended lifespans—up to 60 wash cycles—are gaining traction, creating new revenue streams for suppliers.

Regulatory stringency poses significant challenges for Cleanroom Microfibre Mopping Systems manufacturers, who must ensure compliance with ISO 14644, GMP, and aseptic processing standards. Validating microfibre mop heads for consistent fibre integrity, particulate shedding, sterilization compatibility, and chemical resistance requires intensive R&D and quality assurance. Testing costs can rise by over 30% when meeting ISO 4–ISO 5 cleanroom requirements. Additionally, operators must maintain strict documentation related to batch traceability, usage cycles, and contamination control outcomes. Small-scale manufacturers often struggle to meet these criteria, limiting market entry. End-users face challenges in training personnel to properly handle sterile microfibre systems, leading to variability in cleaning outcomes and reduced efficiency.

• Expansion of Modular Cleanroom Adoption: Modular cleanrooms grew by 55% globally in 2024, driving significant demand for compatible microfibre mopping systems. As modular facilities reduce construction timelines by 45% and improve operational flexibility, demand for agile cleaning systems with fast-swappable mop heads has increased.

• Rising Use of Antimicrobial Microfibre Technologies: Over 38% of newly purchased mop heads in 2024 integrated antimicrobial fibres that reduce microbial presence by up to 92%. These materials support pharmaceutical and biotech cleanrooms where biological contamination control is critical.

• Growth of Autoclavable and Reusable Mopping Systems: Reusable microfibre mops capable of withstanding 50–70 autoclave cycles saw a 33% surge in demand. This trend is fueled by sustainability goals and a push toward reducing single-use waste within controlled environments.

• Data-Driven Cleaning Validation Adoption: Facilities increasingly use data-logging tools integrated with cleaning systems, improving compliance documentation accuracy by 28%. This shift supports automated validation workflows in high-precision manufacturing sectors.

The Cleanroom Microfibre Mopping Systems Market is segmented by type, application, and end-user categories, each contributing uniquely to market expansion. Type segmentation includes flat mops, strip mops, bucket systems, and specialized autoclavable tools, each serving different cleanroom classifications. Application segments span pharmaceuticals, semiconductors, biotechnology, healthcare, and medical devices. End-user segmentation reflects adoption patterns across manufacturing plants, laboratories, hospitals, and research institutions. Pharmaceuticals and semiconductors remain dominant adopters due to strict contamination control protocols, while biotechnology exhibits rapid adoption driven by advanced biologics production. Overall, segmentation demonstrates varied technology sophistication and evolving regional usage trends.

Flat microfibre mops lead the Cleanroom Microfibre Mopping Systems Market, accounting for approximately 46% share due to their superior surface coverage and particle-capture efficiency. Strip mop systems follow with about 28% share, commonly used in larger cleanroom corridors and controlled manufacturing spaces. Autoclavable microfibre mops represent the fastest-growing segment, expected to expand at 8.9% CAGR owing to increasing adoption in high-sterility environments requiring up to 70 heat-sterilization cycles. Specialty mop systems—including polymer-reinforced frames and electrostatic microfibre textiles—collectively contribute 26% of the market, serving niche applications in ISO 4–ISO 7 cleanrooms.

Pharmaceutical manufacturing dominates the application segment, holding 44% of total adoption due to stringent GMP and ISO 14644 requirements. Semiconductor fabrication follows with 31%, driven by ultra-low contamination thresholds in chip production lines. Biotechnology and healthcare applications are accelerating, with biotech expected to record an 8.1% CAGR as facilities shift to high-efficiency microfibre cleaning tools. Medical device manufacturing and research laboratories contribute a combined 25% share. In 2024, over 38% of global enterprises reported piloting Cleanroom Microfibre Mopping Systems to enhance contamination control. Consumer adoption of sterile cleaning techniques is also rising, with 42% of hospitals in the United States integrating advanced microfibre systems.

Pharmaceutical and biotechnology companies represent the leading end-user segment, accounting for 47% of global Cleanroom Microfibre Mopping Systems adoption due to strict sterile production protocols. Semiconductor and electronics manufacturers follow with 29%, driven by precision cleaning requirements in wafer processing. The fastest-growing end-user group is healthcare facilities, expected to record a 7.8% CAGR as hospitals adopt sterile reusable microfibre systems for infection control. Research laboratories, aerospace facilities, and medical device manufacturers together contribute 24% of demand. In 2024, more than 38% of organizations worldwide piloted advanced cleanroom mopping systems, with adoption rates in biotech labs exceeding 52%.

North America accounted for the largest market share at 38.4% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2025 and 2032.

In 2024, North America recorded over USD 135 million in cleanroom microfibre mopping systems procurement across pharmaceuticals, semiconductors, and biotechnology sectors. Europe followed with an approximate 31.2% share valued near USD 110 million, supported by high adoption in Germany, France, and the UK. Asia-Pacific’s cleanroom deployments surpassed USD 80 million in 2024, led by China and Japan, while South America and Middle East & Africa together accounted for more than USD 27 million. This regional diversity emphasizes strong demand for contamination control tools where over 65% of global controlled environments now specify microfibre cleaning in GMP protocols. A rising number of labs and manufacturing hubs use validated microfibre systems that capture over 98% of particulate contaminants, underscoring growing requirements for high-performance cleaning tools in critical environments.

How is North America driving efficiency standards in controlled environment cleaning?

North America holds about 38.4% share of the global cleanroom microfibre mopping systems market, driven by extensive usage in pharmaceutical, semiconductor fabs, medical device, and aerospace cleanrooms. Key industries include high-sterility drug manufacturing and advanced electronics production, where contamination control is critical. Notable regulatory changes like updated GMP guidelines and ISO 14644 revisions have spurred adoption of microfibre systems designed for low-shedding and high absorption. Technological advancements such as polymer-reinforced frames, ergonomic handles, and autoclavable microfibre heads have improved cleaning precision and eliminated cross-contamination risks. A prominent local supplier expanded its ULPA-grade microfibre portfolio in 2024 to cater to next-gen biologics labs requiring over 99.9% particulate capture. Regional behavioral trends show stronger enterprise adoption among healthcare providers and large OEMs with automated cleanroom protocols, reinforcing quality standards and operational consistency.

Is Europe prioritizing regulatory-aligned microfibre cleaning solutions for sterile environments?

Europe accounts for approximately 31.2% of the cleanroom microfibre mopping systems market, led by Germany, the UK, and France. Regulatory bodies emphasize stringent contamination control in pharmaceuticals, biotech, and medical devices, prompting increased investment in advanced microfibre solutions that meet ISO 14644 and EU GMP Annex 1 guidelines. Sustainability initiatives are influencing product design, with a shift toward reusable microfibre heads that withstand high-temperature sterilization cycles and minimize waste. Emerging technologies such as low-lint, electrostatic microfibre textiles and digital process validation tools are gaining traction. A European provider has introduced hybrid microfibre mop heads with antimicrobial treatments to reduce bioload concerns in ISO 5 labs. Regional consumer behavior reflects a preference for explainable, compliance-ready cleaning systems and strong interest in validated cleaning protocols supported by documentation and traceability.

What is fueling Asia-Pacific’s accelerated cleanroom microfibre adoption?

Asia-Pacific represents a significant share of global cleanroom microfibre mopping systems demand, with China, India, and Japan leading consumption in 2024. Regional growth is propelled by massive cleanroom construction projects across semiconductor fabs and vaccine production facilities. Infrastructure investments are high, with over 600 new GMP-certified cleanrooms commissioned in the past two years, driven by strong manufacturing expansions. Local manufacturers are innovating with low-shedding microfibre yarns and moisture-optimized fibres to meet stringent cleanroom standards. For instance, a major microfibre supplier in China expanded capacity by more than 45% in 2024 to support domestic biotech and electronics sectors. Technology trends include AI-enhanced contamination mapping and mobile app–integrated cleaning validation, aligning with Asia-Pacific’s growth driven by e-commerce and mobile AI apps. Consumer behavior favors cost-effective solutions without compromising on performance, boosting demand for high-efficiency reusable microfibre systems.

How is South America integrating microfibre cleaning solutions across controlled environments?

South America accounted for roughly 4–5% of the cleanroom microfibre mopping systems market in 2024, with Brazil and Argentina as key contributors. Growth is supported by expanding cleanroom operations in pharmaceuticals, food safety labs, and aerospace testing facilities. Infrastructure trends show increased investment in contamination control training and validated cleaning processes. Government incentives for local medical device manufacturing and trade policies favoring technology upgrades have led regional labs to adopt advanced microfibre systems. A local player in Brazil rolled out autoclavable, low-lint microfibre mop heads tailored to medical and testing environments. Regional consumer behavior reflects increasing demand tied to media, language localization, and regional regulatory compliance, pushing firms to choose validated cleaning systems for controlled-environment reliability.

Is technological modernization driving microfibre cleaning adoption in emerging markets?

Middle East & Africa comprise about 3–4% of the global cleanroom microfibre mopping systems market, with UAE, South Africa, and select North African countries leading adoption. Demand correlates with modernization of pharmaceutical, oil & gas, and advanced manufacturing sectors requiring contamination control solutions. Technological modernization includes deployment of autoclavable frames, low-shedding microfibre textiles, and validated cleaning workflows in newly launched cleanrooms. Local regulations and trade partnerships are enhancing access to advanced cleaning technologies, helping facilities align with international GMP and ISO standards. A regional supplier has initiated educational programs on microfibre cleaning best practices to support infrastructure development. Consumer behavior shows cautious yet increasing adoption of validated, high-performance cleaning tools, particularly where quality assurance and documentation are prioritized in regulated production environments.

United States – ~38.4% market share - The United States leads due to extensive cleanroom infrastructure investment, high adoption of sterile cleaning protocols, and strong demand from pharmaceuticals and semiconductor sectors.

China – ~22.6% market share - China’s dominance stems from rapid expansion of biotech, semiconductor fabrication facilities, and large-scale cleanroom construction supporting domestic manufacturing growth.

The Cleanroom Microfibre Mopping Systems market is moderately competitive with a mix of global and regional players. The market structure shows both consolidation among Tier-1 suppliers and fragmentation across local manufacturers serving specific industrial applications. An estimated 32–40 active companies provide microfibre mop heads, frames, buckets, and sterilizable cleaning kits tailored for controlled environments. The top 5 companies collectively hold around 42% of global volume, with strong presence in North America and Europe. Leading vendors differentiate through product innovation such as polymer-reinforced handles, autoclavable microfibre textiles, and integrated cleaning validation tools. Strategic initiatives include partnerships with cleanroom consultants, adoption of antimicrobial fibre technologies, and expansion of distribution networks in Asia-Pacific and Latin America. New product launches in 2024 emphasized ergonomic design, reduced particle shedding, and compatibility with ISO 14644 cleaning standards, catering to semiconductors, pharmaceuticals, and biotech end-users. Innovation trends such as multi-layer microfibre constructions, IoT-linked contamination mapping, and reusable hygiene systems are shaping competitive positioning. Market participants are also investing in sustainability by developing reusable mop heads with high durability cycles and reduced disposal waste, aligning with corporate ESG goals that encourage efficient resource use in cleanroom operations. Overall, the competitive landscape reflects a balance between technological advancement and regional adaptation to varying cleanroom demands.

Texwipe

Cleanroom Depot

Contec, Inc.

SAAF International

Vikan A/S

Chemtex Specialty U.S.A.

Micronova Cleanroom Technology

GVS Filter Technology

Steris plc

Hollingsworth & Vose

ITW Texwipe

Swish Maintenance Ltd.

Cleanroom Microfibre Mopping Systems technology is evolving rapidly, driven by innovations in fibre engineering, decontamination science, and automated validation protocols tailored for critical environments. Microfibre textiles used in these systems are engineered with ultra-fine fibres—often less than 1 denier thickness—to maximize surface area and enhance particulate capture efficiency while maintaining low lint and low particulate shedding characteristics. Advanced multi-layer fibre structures incorporate varied yarn densities and electrostatic properties to trap both hydrophilic and hydrophobic contaminants across ISO 4–ISO 8 cleanrooms. Precision weaving and split-fibre technologies provide consistent performance, helping achieve over 98% particle retention in controlled environments.

Sterilization compatibility remains a core technological requirement for cleanroom microfibre systems. To meet this need, manufacturers have developed autoclavable and radiation-tolerant microfibre materials capable of retaining structural integrity and performance after repeated sterilization cycles, often exceeding 50 autoclave exposures. Polymer-reinforced handles and frames made from high-grade polypropylene or stainless steel facilitate repeated sterilization without deformation or corrosion. These systems also reduce cross-contamination risks and extend usable life cycles, contributing to operational cost efficiency.

Emerging innovations include antimicrobial microfibre treatments that inhibit microbial growth on mop surfaces, significantly reducing bioload in pharmaceutical and biotech environments. These treatments leverage embedded silver ions or other antimicrobial agents that maintain efficacy even after numerous wash cycles. In addition, electrostatic microfibre technologies improve fine particulate capture, addressing challenges where traditional wet mopping cannot reach sub-micron contaminants.

Digital integration is another trend shaping this market. Cleanroom facilities increasingly adopt data-driven cleaning validation systems that pair microfibre mopping tools with sensors and software for real-time documentation, traceability, and compliance reporting. These systems can log parameters such as surface coverage, contamination levels pre- and post-cleaning, and operator actions, ensuring adherence to GMP and ISO standards. By automating validation workflows and reducing manual documentation, these innovations improve audit readiness and operational transparency.

Furthermore, bespoke microfibre mopping configurations—optimized for specific industries such as semiconductors, medical devices, and pharmaceutical manufacturing—are enabling custom cleaning protocols. For example, semiconductor fabs often require low-ionic and low-pyrogenic microfibre heads to prevent wafer contamination, while pharmaceutical applications focus on sterility and chemical compatibility.

These technological advancements are increasing the value proposition of cleanroom microfibre mopping systems for facility engineers, quality assurance teams, and compliance officers in controlled environments, facilitating enhanced contamination control, improved workflow efficiency, and strengthened regulatory alignment.

• In August 2024, Contec, Inc. expanded its cleanroom microfibre mopping portfolio to include autoclavable, low-particulate mop heads with enhanced durability for ISO Class 5 and above, improving contaminant capture performance in pharmaceutical and semiconductor cleanrooms. Source: www.contecinc.com

• In April 2024, Ecolab introduced a next-generation microfibre cleaning kit integrating antimicrobial fibre technology, increasing microbial reduction efficiency by over 90% in controlled environments. Source: www.ecolab.com

• In December 2023, Kimberly-Clark Professional launched improved cleanroom microfibre pads with optimized weave density, reducing lint and particle shedding by 35% during critical cleaning cycles in high-purity zones. Source: www.kimberly-clark.com

• In June 2023, Texwipe unveiled an advanced electrostatic microfibre mop system designed for high-precision electronics cleanrooms, offering enhanced fine particulate removal and reduced chemical usage. Source: www.texwipe.com

The Cleanroom Microfibre Mopping Systems Market Report provides a comprehensive analysis of product types, applications, end-user industries, and regional demand dynamics in contamination-controlled environments. It examines flat and strip microfibre systems, autoclavable tools, bucket and wringer combinations, and specialized low-dust products engineered for ISO 4–ISO 8 cleanrooms used in pharmaceuticals, biotech, medical device manufacturing, semiconductors, aerospace, and research laboratories. Technological focus areas include advanced fibre engineering, polymer-reinforced components, antimicrobial treatments, and digital cleaning validation protocols that enhance compliance documentation and operational transparency. The report also addresses regional variations in adoption patterns, with detailed assessments of infrastructure growth, regulatory environments, and cleanroom construction trends across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, providing insights for strategic planning. In addition, it evaluates competitive landscapes, key vendor profiles, strategic initiatives such as partnerships and product innovations, and emerging opportunities within controlled environments seeking high-efficiency, low-contamination cleaning solutions. Overall, the scope delivers actionable intelligence tailored for decision-makers to understand market direction, technological influence, and future growth pathways in cleanroom cleaning systems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 353.7 Million |

|

Market Revenue in 2032 |

USD 630.8 Million |

|

CAGR (2025 - 2032) |

7.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Ecolab Cleanroom Solutions, Kimberly-Clark Professional, MicroCare, Texwipe, Cleanroom Depot, Contec, Inc., SAAF International, Vikan A/S, Chemtex Specialty U.S.A., Micronova Cleanroom Technology, GVS Filter Technology, Steris plc, Hollingsworth & Vose, ITW Texwipe, Swish Maintenance Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |