Reports

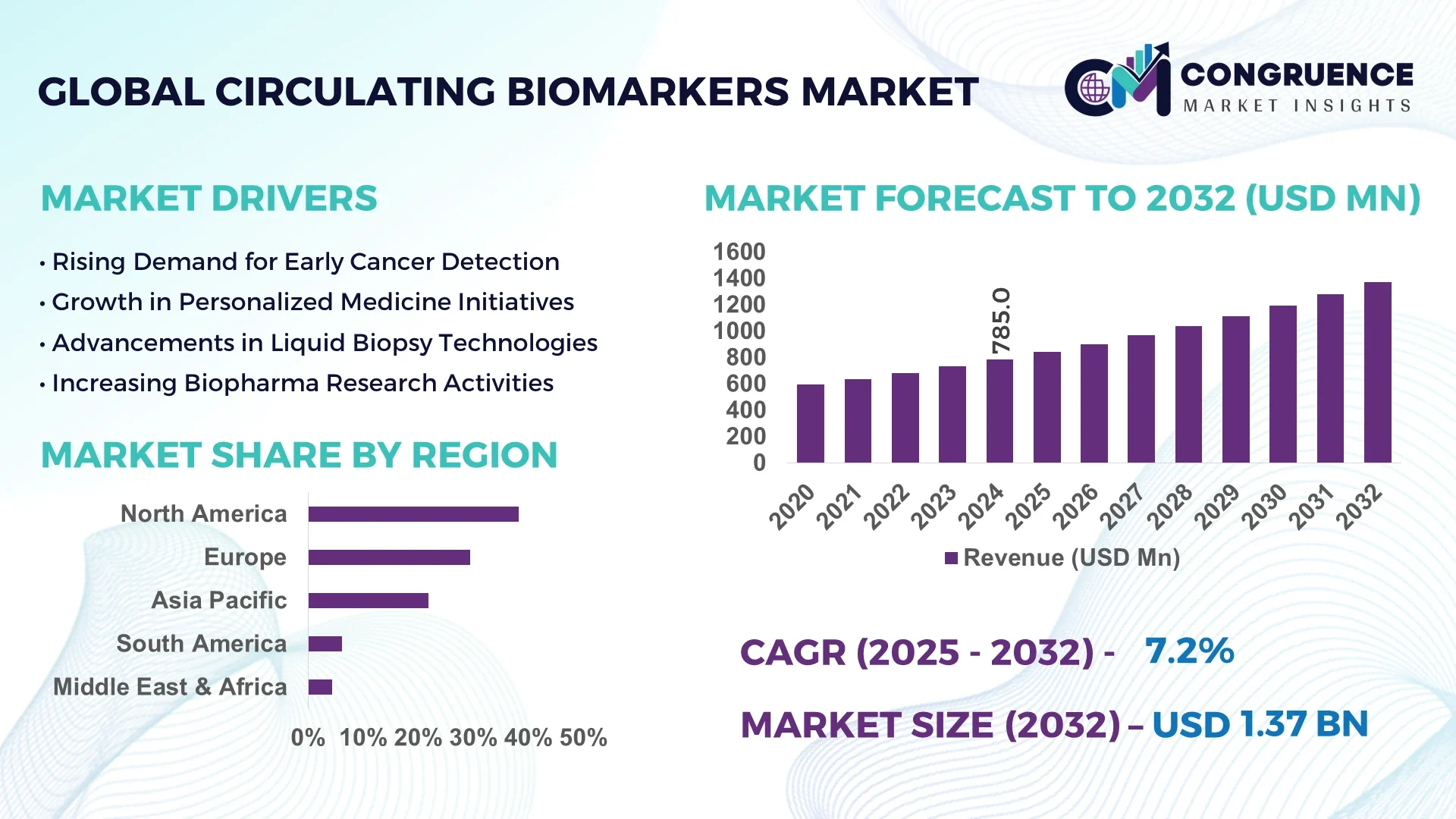

The Global Circulating Biomarkers Market was valued at USD 785.0 Million in 2024 and is anticipated to reach a value of USD 1,369.1 Million by 2032 expanding at a CAGR of 7.2% between 2025 and 2032. Growth is primarily driven by rapid advancements in liquid biopsy technologies, the rise in personalized medicine, and increased demand for non-invasive diagnostic solutions.

The United States holds a dominant position in the global circulating biomarkers market, supported by its advanced biomedical infrastructure, strong investment inflows, and extensive clinical application in oncology and cardiovascular disease monitoring. The country’s research ecosystem includes over 400 active biomarker discovery projects and more than USD 2.5 billion in annual R&D funding across public and private sectors. Additionally, the integration of AI-based bioinformatics platforms has accelerated the identification and validation of new biomarkers, enhancing precision diagnostics and early disease detection capabilities across major healthcare institutions.

Market Size & Growth: The market stood at USD 785.0 Million in 2024 and is projected to reach USD 1,369.1 Million by 2032, growing at a CAGR of 7.2%. Expansion is driven by rising adoption of liquid biopsy and molecular diagnostics.

Top Growth Drivers: Increasing oncology diagnostic applications (38%), enhanced assay efficiency (32%), and adoption in cardiovascular disease management (27%).

Short-Term Forecast: By 2028, diagnostic turnaround times are expected to improve by 35%, supported by automation and AI-driven data analysis.

Emerging Technologies: Advancements in exosome profiling, next-generation sequencing (NGS), and AI-integrated biomarker validation are reshaping diagnostic accuracy.

Regional Leaders: North America projected at USD 540.0 Million by 2032, Europe at USD 400.0 Million, and Asia Pacific at USD 320.0 Million—each driven by unique adoption in oncology and clinical trials.

Consumer/End-User Trends: Hospitals and clinical laboratories account for 60% adoption, followed by research institutes with rising use in clinical genomics and translational studies.

Pilot or Case Example: In 2024, a clinical pilot in Japan achieved 42% improvement in early cancer detection accuracy through multi-analyte liquid biopsy integration.

Competitive Landscape: Qiagen leads with approximately 12% market share, followed by Thermo Fisher Scientific, Roche Diagnostics, Bio-Rad Laboratories, and Illumina.

Regulatory & ESG Impact: Implementation of FDA and EMA biomarker validation frameworks has improved compliance, while laboratories aim for 25% waste reduction by 2030.

Investment & Funding Patterns: Global investments exceeded USD 1.4 billion in 2024, with rising venture capital funding in early-stage oncology biomarker startups.

Innovation & Future Outlook: AI-driven bioinformatics and digital pathology integration are expected to advance precision diagnostics and treatment personalization globally.

The Circulating Biomarkers Market continues to evolve across oncology, neurology, and cardiology sectors, influenced by emerging high-throughput technologies, expanding precision medicine initiatives, and favorable reimbursement policies. Regional demand is strongest in North America and Western Europe, with Asia Pacific showing high growth due to healthcare modernization and government-funded R&D programs.

The Circulating Biomarkers Market is strategically vital to the next generation of precision medicine, diagnostics, and therapeutic monitoring. As healthcare systems worldwide shift toward value-based care, circulating biomarkers provide non-invasive, cost-effective, and rapid diagnostic insights. Integration of multi-omic approaches has improved data correlation accuracy by 42% compared to conventional assays, leading to more precise disease profiling and prognosis.

North America dominates in diagnostic volume, while Europe leads in technology adoption, with approximately 48% of clinical laboratories utilizing biomarker-based liquid biopsy tests. By 2027, AI-driven diagnostic algorithms are expected to reduce detection time by 30% and improve analytical sensitivity by 25%. Firms are aligning strategies toward ESG compliance by achieving a 20% reduction in laboratory waste and transitioning to eco-friendly reagents by 2030.

In 2024, a U.S.-based research consortium demonstrated a 36% improvement in biomarker data reproducibility using machine learning-based normalization frameworks. The next two years will witness a surge in companion diagnostic applications, reinforcing the market’s role in treatment optimization and early disease intervention. Moving forward, the Circulating Biomarkers Market stands as a pillar of clinical innovation, resilience, and sustainable healthcare transformation.

The Circulating Biomarkers Market is characterized by increasing R&D investments, expanding diagnostic applications, and growing integration of digital health technologies. Advances in genomics, proteomics, and microfluidics are enabling faster and more precise detection of disease-specific biomarkers. Rising incidence of chronic diseases and the shift toward personalized medicine continue to reshape demand patterns. Emerging economies are also investing in large-scale screening programs and digital pathology infrastructure to improve population health outcomes.

Technological innovations such as next-generation sequencing and microfluidic biochips have transformed biomarker discovery and validation workflows. These platforms enable detection of rare circulating nucleic acids and proteins with high sensitivity. Adoption of multiplex assay technologies has enhanced throughput by 45%, allowing faster clinical translation. This continuous improvement supports broader diagnostic coverage across oncology, neurology, and infectious disease applications.

The Circulating Biomarkers Market faces challenges due to inconsistent international regulatory frameworks governing biomarker validation, data interoperability, and clinical approval processes. Stringent requirements for assay reproducibility and diagnostic accuracy increase testing timelines and operational costs. Limited standardization across laboratories and varying approval criteria in regions such as the EU and Asia create additional barriers to commercialization and clinical deployment.

The expansion of personalized medicine offers significant opportunities for circulating biomarkers, enabling real-time disease monitoring and tailored treatment strategies. With over 1,200 active clinical trials using circulating biomarkers, adoption in oncology and cardiovascular therapy is increasing rapidly. The rise in multi-omic data integration creates new possibilities for precision diagnostics and early detection programs, particularly in high-prevalence disease areas.

Despite technological progress, data interoperability and infrastructure limitations continue to hinder market scalability. Many clinical centers lack advanced informatics tools for managing large biomarker datasets. Integration between hospital information systems and analytical platforms remains fragmented, reducing workflow efficiency by approximately 20%. Overcoming these challenges requires unified digital frameworks and standardized data-sharing protocols.

Expansion of Liquid Biopsy Platforms: The adoption of liquid biopsy-based assays increased by 41% in 2024, driven by their ability to detect multiple cancer types using minimal sample volume. Hospitals and oncology centers are investing in automated systems that reduce processing time by 30%, improving patient turnaround and diagnostic precision.

Rise in AI-Powered Data Analytics: The application of artificial intelligence in biomarker analysis grew by 37%, enhancing predictive modeling accuracy and early disease detection. Automated machine learning systems now handle over 60% of genomic data interpretation tasks in leading research institutions.

Integration of Exosome and EV Profiling: Research advancements have pushed exosome-based biomarker profiling adoption up by 28%, enabling detection of complex neurodegenerative and metabolic disorders. The development of nano-scale separation techniques has improved biomarker purity and reproducibility by 22%.

Growth in Clinical Trial Applications: Circulating biomarkers are now incorporated in 46% of ongoing precision medicine trials worldwide. Their use has led to a 35% improvement in patient stratification efficiency and a 25% reduction in trial duration, reinforcing their critical role in personalized therapy development.

The Circulating Biomarkers Market demonstrates strong diversification across type, application, and end-user categories, reflecting the broad scope of clinical and research utilization. Key segmentation areas include circulating tumor cells (CTCs), cell-free DNA (cfDNA), circulating RNA, exosomes, and other molecular markers. Applications span oncology diagnostics, cardiovascular disease monitoring, neurological disorder analysis, and prenatal testing. End-users encompass hospitals, diagnostic laboratories, research institutions, and biopharmaceutical companies. Each segment exhibits unique adoption dynamics driven by technological integration, regulatory validation, and precision medicine initiatives. Growing demand for minimally invasive diagnostic tools and personalized healthcare solutions continues to shape the global segmentation landscape, with distinct regional patterns in clinical adoption and R&D investments.

Among all circulating biomarker types, cell-free DNA (cfDNA) dominates the market, accounting for approximately 38% of total adoption. This leadership stems from cfDNA’s ability to detect tumor-specific mutations and genomic alterations with high accuracy in oncology and prenatal testing. Circulating tumor cells (CTCs) follow with around 27% market adoption, driven by advances in microfluidic isolation and immunomagnetic capture technologies. However, exosome-based biomarkers represent the fastest-growing segment, projected to expand at an estimated 8.4% CAGR, fueled by their robust stability, non-invasive accessibility, and potential in early neurodegenerative disease detection. Other categories such as circulating RNA and proteomic biomarkers collectively contribute about 35%, maintaining relevance in multi-analyte assays and inflammation studies.

Oncology diagnostics lead the Circulating Biomarkers Market, representing approximately 46% of total application share, attributed to the global rise in cancer screening programs and increased use of liquid biopsy for tumor profiling. Cardiovascular disease monitoring follows at 23%, supported by biomarker panels capable of detecting myocardial injury and heart failure progression. However, neurological disorder diagnostics show the fastest growth, projected to expand at an estimated 8.8% CAGR, propelled by increased focus on Alzheimer’s and Parkinson’s biomarker validation studies. Remaining applications—such as prenatal testing and infectious disease screening—account for a combined 31%, emphasizing growing adoption in early-stage and population health diagnostics. In 2024, approximately 42% of hospitals worldwide reported piloting circulating biomarker-based assays for early cancer detection and therapy response monitoring. Additionally, over 35% of biotech firms integrated these biomarkers into precision medicine pipelines to improve clinical outcome prediction models.

Hospitals and clinical laboratories dominate the end-user landscape, accounting for roughly 52% of total adoption, due to their extensive use in routine diagnostics, patient monitoring, and clinical validation programs. Research and academic institutions hold around 28%, leveraging biomarker platforms for translational research, validation studies, and therapeutic discovery. Meanwhile, biopharmaceutical companies represent the fastest-growing end-user group, anticipated to grow at an estimated 8.6% CAGR, driven by increased incorporation of circulating biomarkers in drug development and clinical trials. Other end-users, including diagnostic kit manufacturers and contract research organizations, contribute a combined 20%, reflecting steady engagement in biomarker innovation and technology standardization. In 2024, nearly 45% of biopharma enterprises globally reported deploying circulating biomarker-based systems to support companion diagnostics and treatment personalization efforts. Furthermore, 37% of hospitals implemented automated biomarker testing workflows to enhance clinical throughput and diagnostic precision.

North America accounted for the largest market share at 38.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.6% between 2025 and 2032.

North America’s dominance is attributed to its advanced healthcare infrastructure, rising demand for precision diagnostics, and extensive investment in oncology biomarker research. Europe followed with a 29.5% share, driven by stringent regulatory standards and early adoption of liquid biopsy technologies. The Asia-Pacific region, holding 21.8% of the market, is experiencing rapid adoption due to expanding biotech industries in China and India. South America and the Middle East & Africa collectively accounted for 10.5%, supported by gradual improvements in diagnostic healthcare spending and clinical research initiatives.

North America holds approximately 38.2% of the global circulating biomarkers market in 2024. The market’s growth is propelled by strong demand from the healthcare, pharmaceutical, and biotechnology sectors, particularly for non-invasive cancer diagnostics and liquid biopsy tests. Supportive initiatives by the U.S. FDA for biomarker-based clinical trials and precision medicine programs have further enhanced market penetration. Technological advancements such as AI-integrated genomic analysis and cloud-based bioinformatics platforms are reshaping diagnostics workflows. Local players like Guardant Health Inc. are expanding their product portfolios to strengthen clinical utility and accessibility. Consumer behavior shows high enterprise adoption among hospitals and diagnostic labs, driven by the region’s emphasis on personalized and preventive healthcare.

Europe accounts for around 29.5% of the global circulating biomarkers market in 2024. The market benefits from strong adoption across Germany, the United Kingdom, and France, where healthcare modernization and patient-centric policies prevail. Regulatory authorities like the European Medicines Agency (EMA) have established frameworks supporting biomarker validation for clinical and pharmaceutical use. There is a rising focus on digital pathology and multi-omics integration to enhance biomarker interpretation accuracy. Local players such as QIAGEN N.V. are expanding biomarker assay portfolios to align with evolving clinical needs. Regional consumer behavior reflects a preference for explainable and compliant diagnostic tools, with regulatory pressure stimulating the shift toward transparent biomarker solutions.

Asia-Pacific represented 21.8% of the global circulating biomarkers market in 2024 and is witnessing the fastest growth globally. The region’s growth is led by China, India, and Japan, driven by escalating investments in genomics and expanding access to affordable diagnostics. Rapid advancements in biotech manufacturing, AI-driven clinical data analytics, and public–private partnerships are strengthening regional infrastructure. China’s large patient population and India’s rising clinical trial participation are further boosting market demand. Local players such as GenScript Biotech Corporation are focusing on developing cost-effective biomarker platforms. Consumer behavior in this region reflects high engagement with digital health tools and mobile-based diagnostic applications, especially in urban centers.

South America holds nearly 6.2% of the global circulating biomarkers market in 2024, with Brazil and Argentina being the primary contributors. The regional market is driven by increased government healthcare investments, establishment of molecular diagnostic laboratories, and partnerships with global biotech firms. Trade policies encouraging medical device imports and clinical research collaborations have boosted access to biomarker technologies. Local biotechnology companies in Brazil are actively working toward expanding diagnostic assay production capacity. Consumer behavior trends indicate that growth is tied to increased localization of healthcare solutions, reflecting linguistic and cultural adaptability in service delivery and patient engagement.

The Middle East & Africa accounted for approximately 4.3% of the global circulating biomarkers market in 2024. Demand is primarily concentrated in UAE, Saudi Arabia, and South Africa, where healthcare modernization and diversification efforts are underway. Key growth sectors include oncology diagnostics, pharmaceutical R&D, and clinical genomics. National initiatives promoting healthcare innovation, such as the UAE Vision 2031, are fostering local research collaborations. Companies like Bioline Global FZ are contributing to expanding biomarker testing infrastructure. Consumer behavior in this region reflects a rising acceptance of precision medicine and telehealth diagnostics, supported by digital transformation efforts in healthcare ecosystems.

United States – 35.4% Market Share: Dominance due to advanced clinical infrastructure, high R&D funding, and rapid regulatory approvals for liquid biopsy products.

China – 18.6% Market Share: Strong manufacturing capacity, expanding biotech sector, and growing patient population driving biomarker-based diagnostics adoption.

The circulating biomarkers market operates within a moderately consolidated environment, featuring over 60 active competitors globally and a combined top-5 company share of approximately 45%. Market leaders maintain strong positioning through vertical integration of assay platforms, reagent supply, and bioinformatics services. Strategic initiatives have included 25+ partnerships and acquisitions announced between 2022-2024, and more than 70 new product launches focused on liquid biopsy, extracellular vesicles, and AI-driven analytics. Innovation trends show significant investment in multi-omic marker panels, machine-learning interpretation tools, and decentralized testing formats—virtually every top player has introduced a next-generation workflow or consumable. While incumbent diagnostics firms leverage existing distribution networks and regulatory experience, biotech challengers are gaining traction with cost-effective platforms. Competitive pressure is highest in North America, where reimbursement pathways favour early adopters, and emerging players are gaining share in Asia-Pacific via local manufacturing collaborations. Decision-makers should note that market entry and scale-up are increasingly driven by robust clinical validation and global regulatory alignment rather than simple assay novelty.

Roche Diagnostics (F. Hoffmann-La Roche Ltd.)

Menarini Silicon Biosystems SpA

Bio-Rad Laboratories, Inc.

Foundation Medicine, Inc.

Illumina Inc.

Guardant Health Inc.

Current technologies in the circulating biomarkers market emphasize high-sensitivity detection of cell-free DNA (cfDNA), circulating tumour cells (CTCs) and extracellular vesicles (EVs). For example, cfDNA platforms have improved variant detection at allele frequencies below 0.1 % while sample volumes continue to decrease to <10 mL blood. The integration of next-generation sequencing (NGS) with enriched workflows allows simultaneous mutation, methylation and fragmentation analyses – boosting biomarker signal detection across early-stage disease populations. Emerging technologies include AI-powered bioinformatics pipelines that interpret multi-parametric data (genomic, epigenomic, proteomic) and reduce time-to-result from days to hours. Point-of-care microfluidic platforms leveraging vertical flow assays are achieving limits of detection previously restricted to central labs. In addition, multiplex immunoassays are now capable of quantifying tens of protein markers alongside nucleic acid markers from the same sample. Institutional adoption of cloud-native reporting systems and decentralized laboratory networks is accelerating global rollout of circulating biomarker services. From a strategic standpoint, decision-makers must account for supply-chain readiness (reagents, single-use chips, cloud licenses), regulatory clearance paths for assays (IVD vs RUO) and data-security frameworks for multi-omic patient data. The technology roadmap indicates that over the next 3-5 years the value-chain will shift toward integrated kits combining sample-prep, detection and analytics into end-user-friendly platforms, enhancing scalability and lowering cost per test.

In September 2023, Roche France, Foundation Medicine and the Institute Gustave Roussy announced a partnership to deploy the FoundationOne®Liquid CDx blood-based genomic profiling test for cancer patients in France, aiming to establish in-house liquid biopsy capabilities at the institute. Source: www.foundationmedicine.com

In February 2024, Myriad Genetics, Inc. acquired select assets from Intermountain Health’s precision genomics lab, enabling the expansion of its liquid biopsy and hereditary cancer testing portfolio within clinical networks. Source: www.myriad.com

In November 2024, Foundation Medicine launched a grants programme aimed at addressing biomarker testing disparities in breast and prostate cancer, enabling genomics-driven biomarker adoption across underserved provider networks. Source: www.foundationmedicine.com

In July 2024, Menarini Silicon Biosystems published trial results showing its CELLSEARCH® circulating tumour cell (CTC) assay detected metastatic breast cancer relapse significantly earlier than imaging, expanding its clinical application. Source: www.siliconbiosystems.com

The scope of this report encompasses a comprehensive analysis of the circulating biomarkers market across typologies (cfDNA, CTCs, EVs, circulating RNA, proteomic markers), key applications (oncology diagnostics, cardiovascular disease monitoring, neurological disorder screening, prenatal testing), and end-users (hospitals, diagnostic laboratories, research institutes, biopharmaceutical companies). Geographically, the report covers North America, Europe, Asia-Pacific, Latin America and Middle East & Africa, offering volume, regional share and adoption trends. It also includes emerging niche segments such as multi-cancer early detection (MCED), point-of-care biomarker testing, and integration of AI/machine-learning analytics. The analysis extends to workflow components — sample collection, assay development, instrumentation, data analytics — and traces the technology value-chain from innovation through commercialization.

The report further evaluates market entry barriers, reimbursement landscapes, regulatory frameworks, and strategic initiatives such as partnerships, M&A and funding rounds. This breadth provides decision-makers with actionable insight into investment priorities, competitive positioning and technology road-mapping for the circulating biomarkers domain.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 785.0 Million |

| Market Revenue (2032) | USD 1,369.1 Million |

| CAGR (2025–2032) | 7.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technological Advancements, Segmentation Analysis, Regional Insights, Competitive Landscape, and Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Qiagen N.V., Thermo Fisher Scientific, Inc., Guardant Health, Inc., Roche Diagnostics (F. Hoffmann-La Roche Ltd.), Menarini Silicon Biosystems SpA, Bio-Rad Laboratories, Inc., Foundation Medicine, Inc., Illumina Inc., Guardant Health Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |