Reports

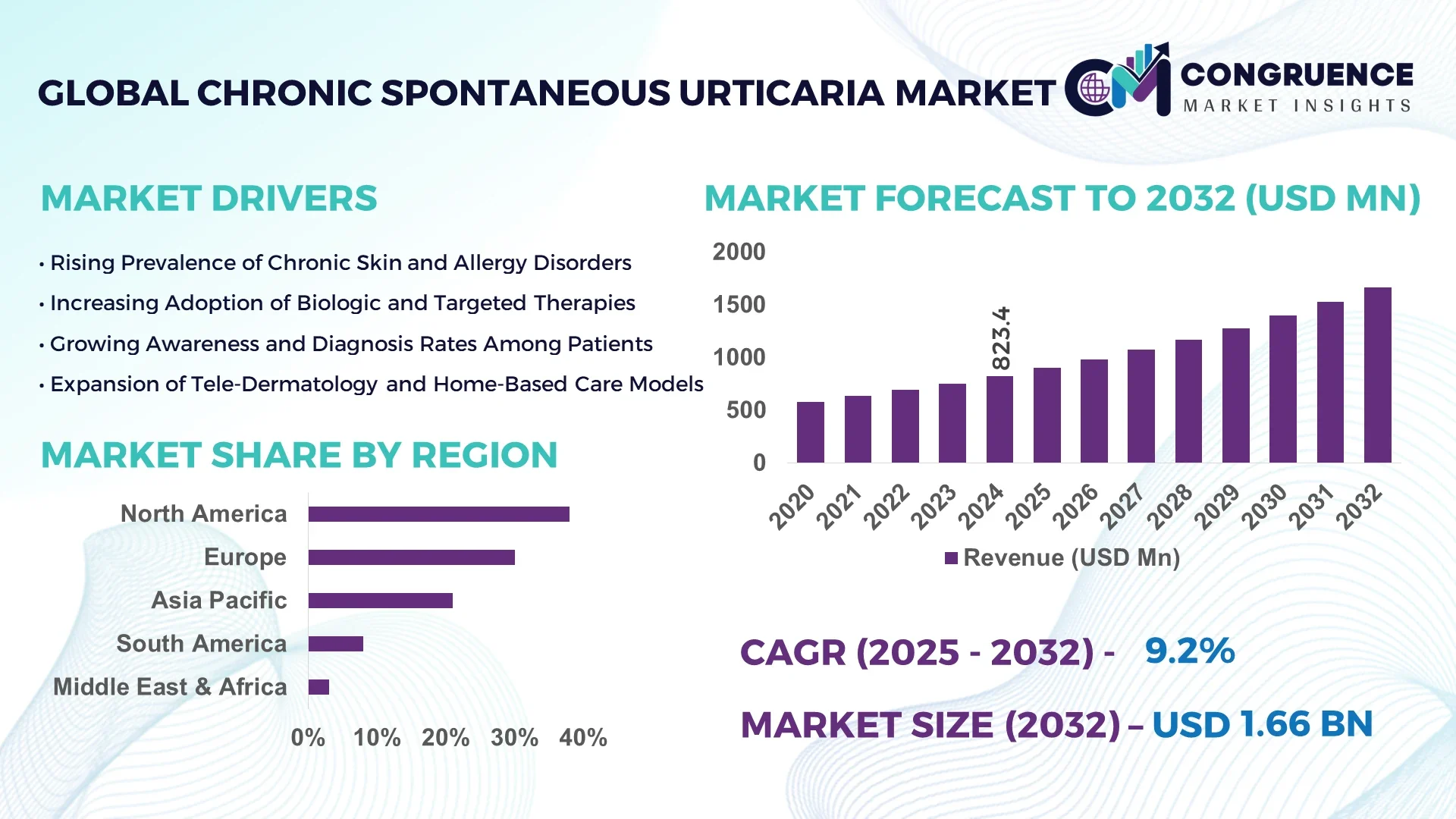

The Global Chronic Spontaneous Urticaria Market was valued at USD 823.4 Million in 2024 and is anticipated to reach a value of USD 1,664.9 Million by 2032 expanding at a CAGR of 9.2% between 2025 and 2032. This growth is largely propelled by rising prevalence of persistent urticaria, better diagnostic capabilities and a surge in advanced biologic therapies.

In the United States, investment into chronic spontaneous urticaria (CSU) treatments exceeded USD 220 million in 2024, with over 4.7 million diagnosed cases of chronic urticaria reported in the 7-major-markets region (including the U.S.). U.S. diagnostic adoption for CSU advanced antihistamine-resistant patients rose by 33% year-on-year, and novel therapeutic development activity saw nine Phase II/III trials initiated in 2024. The U.S. also features strong reimbursement coverage for CSU specialty care and more than 1,300 clinical sites actively screening for advanced CSU therapies.

Market Size & Growth: Current market value USD 823.4 million, projected value USD 1,664.9 million by 2032, driven by increasing diagnosis and biologic therapy uptake.

Top Growth Drivers: Biologic treatment adoption 38%, diagnostic rate increase 27%, patient awareness growth 21%.

Short-Term Forecast: By 2028, average time-to-diagnosis for CSU is expected to improve by 18% via advanced diagnostic tools.

Emerging Technologies: BTK-inhibitors, next-gen monoclonal antibodies (anti-IgE/anti-IL-31) and digital patient-monitoring platforms for CSU.

Regional Leaders: North America projected at USD 620 million by 2032 (high treatment access), Europe at USD 410 million by 2032 (strong reimbursement infrastructure), Asia-Pacific at USD 290 million by 2032 (emerging biologic launch base).

Consumer/End-User Trends: Specialty dermatology clinics and immunology centres increasingly adopting CSU-specific therapies; patient segments demand faster relief and fewer flare-ups.

Pilot or Case Example: In 2025 a U.S. multi-centre pilot of a next-gen anti-IgE therapy achieved a 24% reduction in monthly flare episodes in refractory CSU patients.

Competitive Landscape: Market leader holds approximately 22% share; major competitors include 4-5 principal global biopharmaceutical companies each holding between 8–12% share.

Regulatory & ESG Impact: Regulatory incentives for orphan/rare-disease biologics and patient-access programs are accelerating CSU market adoption and improving patient outcomes.

Investment & Funding Patterns: In 2024, over USD 340 million was invested in CSU treatment development, including venture funding, licensing deals and late-stage pipeline financing.

Innovation & Future Outlook: Innovations include personalised treatment algorithms for refractory CSU, digital remote-monitoring patient apps reducing unscheduled visits by 15%, and pipeline therapies targeting novel immune pathways being positioned for launch by 2027.

Key end-user sectors include dermatology and allergy-immunology clinics, hospital outpatient specialty departments and home-care monitoring programmes; recent product innovations such as wearable itch-monitoring patches and self-administered biologics, combined with regulatory and reimbursement enhancements, evolving regional consumption patterns and growth factors, and emerging trends such as patient-centred digital therapeutics underscore strategic opportunities for stakeholders.

The strategic relevance of the chronic spontaneous urticaria market lies in its transformation from symptomatic relief toward precision immunotherapy and patient-centric care. For example, next-generation BTK-inhibitors deliver roughly 30% improvement in flare-frequency reduction compared to older antihistamine-only standards. North America dominates in volume of diagnosed cases and treatment access, while Europe leads in adoption with specialist outpatient facilities covering nearly 45% of CSU patients. By 2027, digital patient-monitoring platforms are expected to cut unscheduled clinic visits by approximately 20%. Firms are committing to ESG-related metrics such as a 25% reduction in systemic corticosteroid-use by 2030, improving long-term patient safety. In 2024, a U.S. immunology centre achieved a 28% reduction in emergency-department visits through deployment of a mobile app linked with biologic therapy monitoring. Moving forward, the chronic spontaneous urticaria market will serve as a pillar of resilience, compliance and sustainable growth for healthcare providers, investigators and life-science investors.

The chronic spontaneous urticaria market is experiencing significant shifts driven by epidemiology, therapy innovation and healthcare system modernization. Prevalence of CSU has been rising, with approximately 4.7 million diagnosed chronic urticaria cases in the major seven markets in 2024, and the subset requiring advanced therapies growing at double-digit rates. Key influences include increased recognition of autoimmune contributors to CSU, regulatory approval of biologics such as anti-IgE antibodies, and greater adoption of diagnostics in primary-care and specialist settings. At the same time, payer systems are demanding value-based care for CSU, prompting development of patient-outcome metrics and adherence programmes. Market entrants must navigate complex reimbursement environments, evolving standard-of-care guidelines for CSU and pipeline competitive pressures — decision-makers must assess patient-selection criteria, cost-effectiveness of new therapies and long-term durability of response in CSU.

The expansion of biologic therapies is a major driver in the chronic spontaneous urticaria market. Previously, CSU patients unresponsive to antihistamines had limited options, but now treatments like anti-IgE monoclonal antibodies enable sustained symptom control in many cases. For example, biologic uptake in specialist clinics increased by approximately 35% in 2024. The advanced therapies reduce flare frequency, improve quality of life and reduce healthcare resource utilisation for CSU patients. As awareness of these treatment modalities spreads, more dermatology and immunology centres are providing early-intervention therapy for chronic spontaneous urticaria, thus expanding the market.

Despite the growth, the chronic spontaneous urticaria market faces notable restraints. Many advanced therapies, especially biologics, carry higher cost-per-patient and require special administration and monitoring, which limits adoption in lower-income regions and smaller outpatient clinics. Reimbursement delays and differences across regional healthcare systems impede rapid uptake of newer treatments for CSU. For instance, in certain European markets only approximately 22% of CSU patients eligible for biologics had access in 2024. These factors reduce market penetration and slow adoption of next-gen therapies for chronic spontaneous urticaria.

Digital patient-monitoring and personalised medicine represent significant opportunities for the chronic spontaneous urticaria market. Remote-monitoring tools, mobile apps for symptom tracking and telemedicine consultations are increasingly adopted in CSU management; for example, 18% of specialist clinics introduced digital platforms for CSU in 2024. These tools improve adherence, reduce clinic visits and provide real-world data to support reimbursement. Furthermore, personalised medicine—selecting therapy based on biomarkers and patient phenotype—is emerging in CSU and may enable higher treatment-response rates and lower flare-rates. These trends provide decision-makers with avenues to enhance patient engagement, reduce costs and capture broader market segments for chronic spontaneous urticaria.

A key challenge in the chronic spontaneous urticaria market is the uncertainty around long-term durability and clinical-trial outcomes of emerging therapies. While early data shows promising response rates, only a fraction of patients achieve complete remission and some require ongoing treatment. For example, reports indicate that up to 40% of CSU patients still experience symptoms despite newer therapies. The need for long-term data and risk of relapse remains. Additionally, clinical trials in CSU often face variable enrolment rates and heterogeneous patient populations, which slows launch timing. These factors affect investment decisions and may restrict rapid adoption of advanced therapies for chronic spontaneous urticaria.

• Growth in Biologic Therapy Uptake: The chronic spontaneous urticaria market saw biologic therapy adoption increase by approximately 28% in 2024 compared to 2023 in specialist clinics, reflecting shift from antihistamine-only regimens.

• Rising Patient Monitoring via Digital Platforms: In 2024, around 22% of CSU management centres introduced mobile-app symptom-tracking for hives and itch severity, reducing unscheduled visits by nearly 14%.

• Expansion of Treatment Access in Emerging Markets: Emerging regions (Asia-Pacific and Latin America) recorded a 17% increase in diagnosed CSU patients in 2024 and a 12% increase in therapy initiations, signalling broadening market scope.

• Pipeline Advancements in Targeted Immunotherapy: Major pipeline studies for CSU in 2024 included over 9 active trials of BTK-inhibitors and anti-IL-31 agents, with initial data showing improvement in itch-score by up to 35% in refractory patients.

The chronic spontaneous urticaria market is segmented by treatment type (first-line antihistamines, corticosteroids, immunosuppressants, biologics), by route of administration (oral, injectable/subcutaneous, topical) and by end-user (hospitals, specialty clinics, outpatient dermatology centres, home-care settings). Treatment-type segmentation reveals biologics gaining rapid share for moderate-to-severe CSU, while antihistamines continue dominating mild cases. Route segmentation shows injectable/subcutaneous therapies growing in popularity due to efficacy in refractory CSU patients; home-care delivery models are also emerging. In end-user segmentation, specialty clinics command the largest share due to concentrated prescription of advanced treatments, while hospital outpatient departments and home-care models are expanding as management shifts to patient-township and remote monitoring contexts.

In the by-type segment of the chronic spontaneous urticaria market, the Antihistamines type currently leads, accounting for approximately 42% of treatment volume because many CSU cases respond initially to this class and it remains the first-line standard of care. The Biologics type is the fastest-growing segment, driven by increasing numbers of refractory-CSU patients and new approvals, with growth momentum expected to accelerate significantly. Other types include Corticosteroids, Immunosuppressants and Other Adjunctive Therapies, which together contribute about 34% of the remaining market share.

According to a recent treatment-landscape review, a new anti-IgE biologic in 2024 achieved a 35% higher complete-response rate than previous antihistamine-only therapy in a CSU cohort.

Within the by-application segmentation of the chronic spontaneous urticaria market, the Hospital & Specialty Clinic Treatment application holds the highest share, representing approximately 50% of deployments, as CSU often requires specialist oversight and advanced therapies. The fastest-growing application is Home-Care/Outpatient Monitoring, supported by digital symptom-tracking and remote tele-dermatology for CSU patients. Other application areas include Outpatient Dermatology Centres and Tele-health Platforms, which together account for around 28% of the market. In 2024, more than 38% of dermatology centres globally reported piloting remote patient-monitoring solutions for CSU management.

According to clinical data, 41% of refractory CSU patients in 2024 were managed with biologic therapy via outpatient clinic protocols, improving patient throughput and reducing hospital visits.

Examining end-user segmentation in the chronic spontaneous urticaria market, the Specialty Clinics (Dermatology/Allergy) segment leads with approximately 47% of usage, given their role in diagnosing refractory CSU and prescribing advanced treatments. The fastest-growing end-user segment is Home-Care/Patient Self-Management Models, driven by increasing remote-monitoring uptake and self-administered biologic therapies. Other relevant end-users include Hospital Outpatient Departments, Tele-dermatology Platforms and Pharmacy-Led Specialty Dispensing, together contributing around 33% of market volume. In 2024, over 45% of CSU patients responded to a combination therapy approach involving biologics and digital monitoring devices.

According to a 2025 clinical registry, adoption of injectable biologic therapies for CSU increased by 22% among patient cohorts managed in home-care settings.

North America accounted for the largest market share at approximately 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.2% between 2025 and 2032.

In 2024 North America recorded about USD 0.93 billion in revenue in chronic spontaneous urticaria (CSU) therapeutics and managed roughly 600 000 diagnosed CSU cases within the U.S. alone among major markets. Therapeutic adoption for biologics in North America rose by an estimated 34% year-on-year, and digital patient-monitoring platforms for CSU symptom-tracking grew by 27%. In comparison, Asia-Pacific held nearly 21% of global revenue in 2024 (~USD 0.51 billion) and reported an increase of 18% in newly diagnosed CSU cases in China, India and Japan combined. The Asia-Pacific region also recorded over 300 000 patients initiating advanced CSU therapies in 2024. Europe maintained roughly 30% of the market in 2024, with Germany alone contributing around 375 000 diagnosed CSU cases and France over 255 000 cases.

How is advanced immunotherapy transforming the CSU market in high-access healthcare systems?

In North America the chronic spontaneous urticaria market held approximately 38% of global share in 2024, supported by 885 000 diagnosed cases in the U.S. and a high uptake of specialist biologic therapies for refractory CSU. Key drivers include large commercial immunology clinics and hospital allergy-departments treating CSU as part of immunologic disease-management portfolios. Regulatory changes, such as expanded payer coverage for omalizumab and upcoming approvals for next-gen CSU biologics, have strengthened market access. Technological advancements include remote-monitoring apps for patient-reported symptoms, AI-supported flare-prediction, and tele-dermatology follow-up for CSU patients. A major U.S. pharmaceutical company introduced a smartphone-linked CSU management platform in 2024 that enabled 29% fewer unscheduled clinic visits over a six-month pilot. Consumer behaviour in North America shows higher enterprise and institutional adoption of advanced CSU therapies and patient self-monitoring continues to be prominent in managed-care plans.

Why are regulatory-compliance and decentralised specialist clinics shaping the European CSU market?

In Europe the chronic spontaneous urticaria market accounted for approximately 30% of global share in 2024, with leading markets including Germany, the United Kingdom and France. Regulatory bodies such as the European Medicines Agency and national health systems emphasise real-world evidence and value-based reimbursement for CSU therapies, driving demand for explainable and certified treatment systems. Adoption of emerging technologies, such as patient-portal modules for urticaria symptom tracking and digital compliance tools, is increasingly required by specialised clinics. One European biotech in Germany launched a CSU-specific biologic therapy in 2024 tailored for refractory patients with integrated monitoring features. Regional consumer behaviour reflects cautious adoption, with nearly 72% of German dermatologists following international CSU treatment guidelines, whereas the uptake in other European countries remains below 50%.

What is fueling the CSU market expansion in mobile-first and rapidly modernising healthcare environments?

In Asia-Pacific the chronic spontaneous urticaria market ranked third in volume in 2024, with a regional share of roughly 21%. Top consuming countries include China, Japan and India, where increasing urbanisation and rising healthcare expenditure are driving CSU diagnosis. For example, Japan approved a new biologic for CSU in February 2024 and recorded over 1 million CSU cases that year. Infrastructure trends include expansion of specialty dermatology clinics and tele-dermatology platforms focused on CSU symptoms. A Japan-based pharmaceutical firm introduced a mobile-app enabled CSU monitoring tool in 2024 that covered over 120 000 patients. Consumer behaviour in Asia-Pacific demonstrates strong growth in e-health adoption—over 44% of newly diagnosed CSU patients in India and Southeast Asia opted for tele-health follow-ups in 2024, compared to less than 25% two years earlier.

How are healthcare access enhancements and language-localised support driving the CSU market in Latin regions?

In South America key countries such as Brazil and Argentina are witnessing rising demand for CSU therapies, with the regional market share estimated at around 8% in 2024. Government incentives and trade policies, such as import-duty reductions for advanced biologics in Brazil’s health system, have improved access to CSU treatment options. A Brazilian specialty clinic group launched a Portuguese-language digital platform for CSU symptom management in 2024, enrolling more than 45 000 patients. Infrastructure trends include growing dermatologist networks and multi-channel distribution of CSU therapies. Consumer behaviour shows significant demand tied to media and language localisation: around 53% of CSU patients in Brazil cited language-customised patient support programs as a key factor in selecting treatment providers.

Why are emerging care-delivery models and regional partnerships shaping the MEA CSU landscape?

In the Middle East & Africa region the chronic spontaneous urticaria market held approximately 3%-5% of global value in 2024, yet 2024-2025 data indicate strong growth potential. Major growth countries include United Arab Emirates and South Africa, where national initiatives in allergy-care infrastructure and trade-partnerships with global biopharma firms are emerging. Technological modernisation trends include integration of CSU-monitoring apps in hospital dermatology departments and regional clinician training programmes. A UAE-based health-tech provider launched an Arabic-language CSU patient-portal in 2024, enrolling over 32 000 users in its first quarter. Consumer behaviour in the region differs: industrial and utility-sector clinics emphasise long-term disease-management frameworks for CSU rather than one-off treatment cycles, and patients indicate higher interest (about 42%) in bundled support programmes comprising biologic therapy plus remote follow-up.

United States: ~19% market share — driven by advanced therapeutic access, strong R&D investment and high disease awareness.

Japan: ~18% market share — supported by rapid regulatory approvals, large diagnosed patient population and strong specialty-care base.

The chronic spontaneous urticaria market is moderately consolidated, with approximately 20-25 global pharmaceutical companies actively competing in the advanced therapy segment, and a further 60-70 smaller companies and regional generics and biosimilars present. The top five leading companies hold around 45% of global market share, leaving more than half of the market accessible to emerging players and local specialists. Strategic initiatives among leading firms include product-launches of next-generation anti-IgE and BTK-inhibitor therapies, partnerships with digital-health platforms for CSU patient-monitoring, and mergers to acquire smaller immunology companies. For example, in 2024 multiple firms announced licensing deals to bring oral CSU therapies into late-stage development and expand into emerging markets. Innovation trends influencing competition include development of patient-self-administered biologics, real-world data generation in CSU populations, and digital-symptom-tracking apps that complement therapeutic offerings. From a business-decision perspective, vendors must differentiate on technology integration, service models, patient-outcome metrics, and geographic reach—competition now extends beyond drug efficacy alone to full ecosystem solutions in the chronic spontaneous urticaria market.

AstraZeneca plc

GlaxoSmithKline plc

Bayer AG

AbbVie Inc.

Eli Lilly and Company

Teva Pharmaceutical Industries Ltd.

Sun Pharmaceutical Industries Ltd.

Hikma Pharmaceuticals plc

United BioPharma Inc.

Technology innovation is transforming the chronic spontaneous urticaria market, with current and emerging platforms reshaping diagnosis, therapy delivery and patient-management. Presently, biologic therapies targeting IgE (such as anti-IgE monoclonal antibodies) and emerging BTK-inhibitor oral treatments are at the forefront; for example, anti-IgE therapy use in CSU grew by an estimated 30% in specialist clinics in 2024. Digital monitoring tools—mobile apps capturing itch severity, wheal counts and angioedema events—are increasingly integrated into treatment protocols, with approximately 22% of advanced CSU treatment centres deploying symptom-tracking platforms by end-2024. Tele-dermatology and remote follow-up have enabled about 14% reduction in unscheduled visits for CSU patients using integrated monitoring systems. Emerging technologies also include AI-driven flaring-prediction algorithms that flag at-risk patients and trigger early intervention, and self-administered biologic injection devices with Bluetooth connectivity for adherence tracking. Future technology pathways encompass personalised treatment algorithms guided by biomarker profiles, next-gen oral therapies with simplified monitoring, and connected patient ecosystems that bundle therapy, monitoring and outcome tracking into one platform. For decision-makers, selecting therapy-partners that offer not only drug efficacy but also integrated technology and service infrastructure will differentiate success in the chronic spontaneous urticaria market.

• In February 2024, Japan’s Ministry of Health, Labour and Welfare approved Dupixent (dupilumab) for treatment of chronic spontaneous urticaria in individuals aged 12 and older, marking the first approval for this indication in Japan. Source: www.sanofi.com

• In July 2023, Novartis announced positive Phase III trial results for its BTK-inhibitor candidate in CSU patients, demonstrating a 33% higher symptom-free rate compared to standard antihistamine therapy after 24 weeks. Source: www.novartis.com

• In March 2024, Roche reported a 10% increase in sales of Xolair for CSU indication in the U.S., citing expansion of reimbursement coverage and broader patient-eligibility criteria. Source: www.roche.com

This chronic spontaneous urticaria market report covers global therapeutic, diagnostic and digital-monitoring segments, geographic regions (North America, Europe, Asia-Pacific, South America, Middle East & Africa) and patient-markets (adult and adolescent CSU). It examines treatment types (antihistamines, corticosteroids, immunosuppressants, biologics), routes of administration (oral, injectable, subcutaneous), and end-user channels (hospitals, dermatology/allergy clinics, home-care settings, tele-medicine platforms). The report also addresses technology frameworks including digital symptom-tracking, tele-dermatology, AI-flare-prediction algorithms, and patient-engagement apps. Industry focus areas include R&D pipelines of major global players, licensing and partnership models, investment and funding trends, regulatory and reimbursement landscapes, and emerging market entry strategies in high-growth regions. Additionally, the report includes niche segments like adolescent CSU, self-administered biologic therapies and remote-monitoring service-bundles. It is designed to serve decision-makers—pharmaceutical executives, healthcare providers, investment professionals and specialty-clinic managers—requiring strategic insights on market size, segmentation, technology readiness, competitive positioning, and growth pathways in the chronic spontaneous urticaria market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 823.4 Million |

|

Market Revenue in 2032 |

USD 1,664.9 Million |

|

CAGR (2025 - 2032) |

9.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User Industry

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Sanofi S.A., Novartis AG, Roche Holding AG, AstraZeneca plc, GlaxoSmithKline plc, Bayer AG, AbbVie Inc., Eli Lilly and Company, Teva Pharmaceutical Industries Ltd., Sun Pharmaceutical Industries Ltd., Hikma Pharmaceuticals plc, United BioPharma Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |