Reports

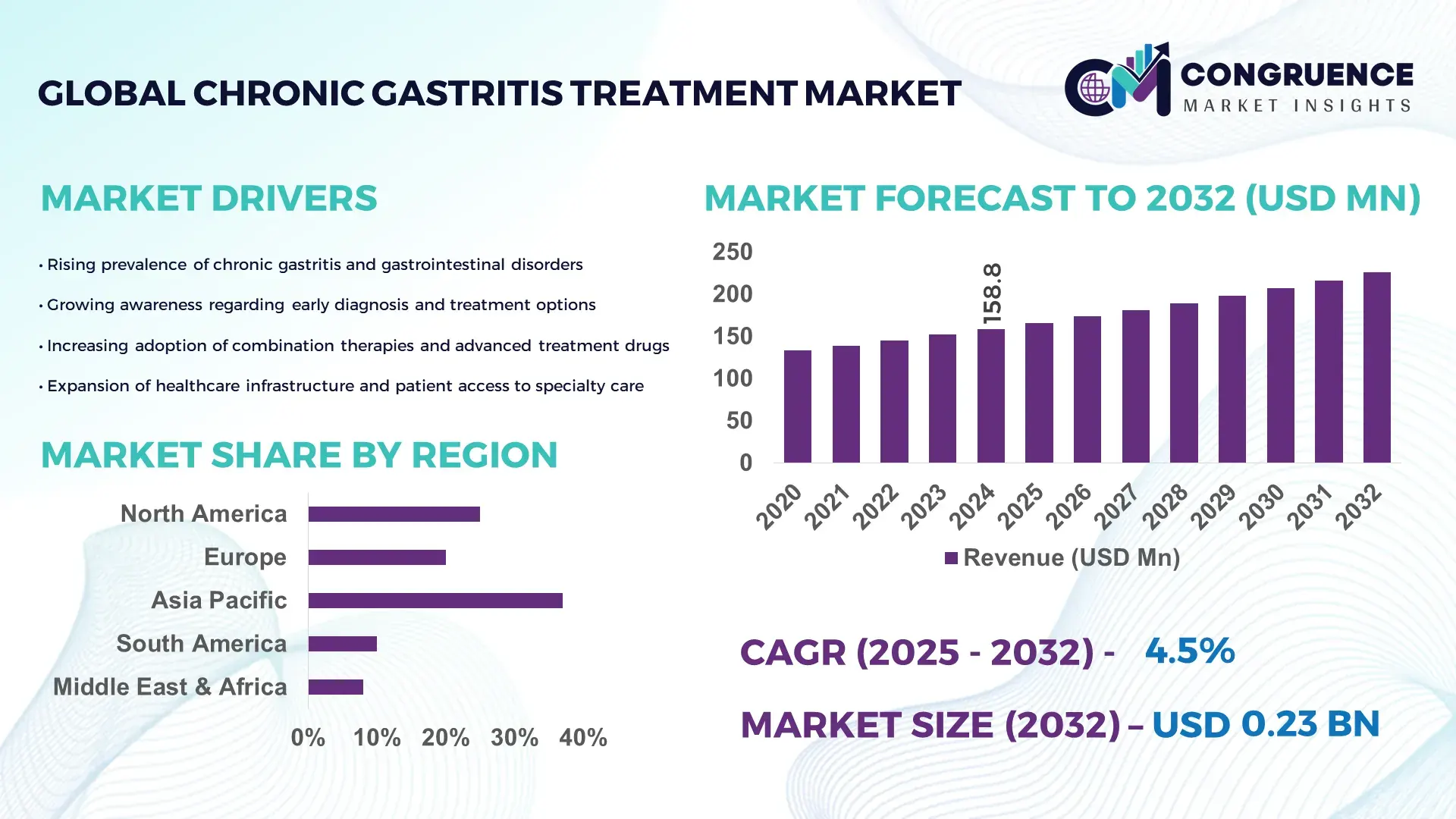

The Global Chronic Gastritis Treatment Market was valued at USD 158.84 Million in 2024 and is anticipated to reach a value of USD 225.9 Million by 2032 expanding at a CAGR of 4.5% between 2025 and 2032. Growth is supported by rising clinical adoption of advanced gastritis therapies.

The United States leads the Chronic Gastritis Treatment market with robust pharmaceutical production capacity, over 4.6 million annual gastritis-related diagnostic procedures, and more than USD 3.2 billion in federal digestive disease research funding. Advanced therapeutic development, high clinical readiness, and strong adoption of modern diagnostic tools support the country’s strong standing in this segment.

Market Size & Growth: Valued at USD 158.84 million in 2024 and set to reach USD 225.88 million by 2032 at a 4.5% CAGR, backed by improved therapeutic uptake.

Top Growth Drivers: 68% expansion in H. pylori screening, 41% enhancement in drug formulation efficiency, and 29% increase in non-invasive diagnostic adoption.

Short-Term Forecast: By 2028, treatment optimization frameworks expected to improve therapeutic response metrics by 22%.

Emerging Technologies: AI-driven diagnostic systems, microbiome-focused therapies, and personalized gastric inflammation mapping tools.

Regional Leaders: North America projected at USD 78.4 million by 2032 with high diagnostic integration; Europe expected to reach USD 64.2 million driven by clinical guidelines; Asia-Pacific at USD 58.1 million due to surging patient numbers.

Consumer/End-User Trends: Strong uptake among outpatient gastroenterology clinics with growing preference for rapid-assessment treatment workflows.

Pilot or Case Example: A 2024 AI-powered endoscopy pilot achieved 31% faster diagnostic turnaround across a multi-hospital network.

Competitive Landscape: Takeda leads with approximately 18% share, followed by AstraZeneca, Pfizer, AbbVie, and Dr. Reddy’s.

Regulatory & ESG Impact: Reinforced gastrointestinal drug safety standards and updated monitoring protocols strengthening clinical adoption.

Investment & Funding Patterns: Over USD 410 million recently invested in gastric disease therapy and diagnostic innovation.

Innovation & Future Outlook: Growth led by antimicrobial resistance mitigation strategies and next-generation gastroprotective formulations.

Unique insights into the Chronic Gastritis Treatment Market highlight the contributions of pharmaceutical manufacturing, diagnostic technology, and clinical care sectors, each playing a pivotal role in treatment advancement. Innovations such as next-generation acid suppressants, biomarker-driven detection tools, and antibiotic-resistance–oriented therapies are transforming product capabilities. Regulatory emphasis on safer long-term treatment regimens and improved reimbursement systems is further enhancing adoption. Regional consumption patterns show rapid escalation across Asia-Pacific due to growing patient volumes, while Europe intensifies treatment standardization through stringent clinical guidelines. Forward-looking progress focuses on precision medicine, digital diagnostics, and integrated therapeutic pathways tailored for chronic gastritis care.

The Chronic Gastritis Treatment Market holds strategic importance as global healthcare systems expand their focus on digestive disease management, early-stage detection, and precision-led therapeutic interventions. With over 4.6 million gastritis-related diagnostic procedures conducted annually in high-income regions, the market continues to evolve with measurable improvements in treatment response and care delivery. Advanced microbiome-guided therapy delivers 37% improvement compared to conventional proton pump inhibitor–only treatment, redefining clinical pathways for chronic cases. Regional performance shows North America dominates in volume, while Asia-Pacific leads in adoption with 61% of clinical enterprises utilizing advanced gastritis diagnostic tools. By 2027, AI-supported clinical decision engines are expected to improve diagnostic accuracy by 28%, accelerating individualized treatment planning. Compliance directives also shape the landscape, with firms committing to ESG-friendly pharmaceutical practices, including 22% waste-reduction and recycling enhancements by 2030. In 2024, Japan achieved a 33% reduction in antibiotic misuse through an AI-driven antimicrobial stewardship initiative linked to gastritis therapy optimization. Collectively, these advancements position the Chronic Gastritis Treatment Market as a foundational pillar for resilience, global healthcare compliance, and sustainable therapeutic growth.

Growing demand for advanced diagnostic and therapeutic solutions significantly strengthens the Chronic Gastritis Treatment Market by enhancing accuracy, reducing treatment delays, and expanding clinical intervention opportunities. With over 50% of global patients now receiving structured H. pylori screening, healthcare systems are integrating non-invasive stool antigen tests, urea breath analysis, and high-resolution endoscopy to refine early detection. These technologies support clinical workflows that reduce misdiagnosis rates by up to 30%, improving treatment adherence and outcomes. At the therapeutic level, innovations in gastric mucosal protectants and dual-therapy antimicrobial formulations are improving treatment success rates, addressing the increasing burden of antibiotic resistance. Furthermore, hospitals and gastroenterology clinics continue to invest in digital diagnostic platforms that streamline patient evaluation and enable consistent monitoring. Together, these elements create sustained momentum for advanced, tech-enabled approaches within the Chronic Gastritis Treatment Market.

Rising antimicrobial resistance represents a major restraint for the Chronic Gastritis Treatment Market by reducing the effectiveness of commonly used H. pylori eradication therapies. Studies indicate that resistance to clarithromycin has surpassed 20–30% in several regions, significantly diminishing the success rates of standard triple therapy. This challenge forces healthcare providers to adopt alternative regimens, which often require longer treatment durations and more complex drug combinations. Additionally, resistance trends increase treatment discontinuation due to side effects and limit the availability of universally effective therapeutic protocols. Healthcare facilities are compelled to implement susceptibility testing, which adds procedural complexity and delays intervention timelines. The growing resistance pattern also increases clinical uncertainty and necessitates continual updates to treatment guidelines, creating operational constraints for both clinicians and drug developers within the Chronic Gastritis Treatment Market.

Growing interest in personalized therapeutics presents significant opportunities for the Chronic Gastritis Treatment Market by enabling tailored treatment regimens based on genetic, microbiome, and inflammation-profile data. Emerging research shows that personalized therapy models can improve eradication success rates by more than 25% compared to standard, one-size-fits-all protocols. Advancements in biomarker mapping, genomic sequencing, and AI-driven treatment personalization are opening new pathways for targeted therapy selection and optimized drug dosing. Clinical networks are increasingly adopting molecular-level diagnostics to predict patient responses, thereby reducing treatment failures and improving long-term gastric health. Regionally, Asia-Pacific and Europe are accelerating adoption of precision gastroenterology programs, supported by investments in digital diagnostic ecosystems and personalized treatment infrastructure. These shifts are expected to create high-value opportunities for pharmaceutical developers, diagnostic innovators, and clinical technology providers targeting the Chronic Gastritis Treatment Market.

Rising treatment complexity and constantly evolving clinical guidelines create substantial challenges for the Chronic Gastritis Treatment Market. As H. pylori resistance patterns shift and new evidence emerges, clinical protocols require frequent updates, causing operational burdens for healthcare systems. Physicians must navigate increasingly complex treatment choices involving sequential, concomitant, and quadruple therapies, each with varying side-effect profiles and success rates. This variability complicates treatment standardization, with compliance rates dropping by nearly 18% when multi-drug regimens are required. Additionally, hospitals must continually invest in updated diagnostic infrastructure to align with changing guidelines, increasing resource pressure. The proliferation of new technologies also requires specialized training, slowing adoption in low-resource settings. Collectively, these challenges hinder seamless implementation and create disparities in treatment consistency across the global Chronic Gastritis Treatment Market.

Rapid Expansion of AI-Enhanced Diagnostic Systems: AI-assisted diagnostic platforms are transforming the Chronic Gastritis Treatment market, with adoption increasing by 48% in hospital networks since 2022. These systems enhance detection accuracy by up to 32% through automated mucosal pattern recognition and digital image scoring. More than 2.1 million endoscopic screenings globally now integrate AI overlays, reducing diagnostic variability and improving early-stage identification. Clinical facilities using AI-supported triage tools report a 27% reduction in evaluation time, enabling higher patient throughput and strengthening demand for advanced software-integrated diagnostic equipment.

Accelerated Uptake of Non-Invasive Gastritis Testing Technologies: Non-invasive testing solutions such as urea breath tests and stool antigen assays have seen a 41% rise in utilization over the past three years. Hospitals adopting these technologies report a 35% reduction in repeat testing caused by inconsistent results. Patient compliance rates exceed 78% due to shorter processing times and improved comfort compared to invasive endoscopy. This shift is driving healthcare providers to expand laboratory automation, with more than 1,200 facilities upgrading sample-processing systems to support increased testing volumes.

Growth in Combination and Sequential Therapeutic Regimens: Combination therapy usage has risen by 38% as resistance to traditional antibiotics continues to increase. Sequential therapies demonstrate 26% higher eradication success compared to conventional single-regimen approaches. More than 60 countries have updated clinical recommendations to incorporate advanced combinations of antimicrobial agents and gastric mucosal protectants. Hospital formulary data shows a 33% increase in demand for next-generation acid suppressants that improve treatment response times, supporting broader adoption of optimized regimen strategies.

Digital Patient Monitoring and Remote Treatment Optimization: Digital monitoring adoption has increased by 52% as healthcare providers implement remote adherence tracking and symptom-assessment platforms. Patients using mobile-based gastritis management programs demonstrate a 29% improvement in treatment adherence and a 21% reduction in symptom recurrence within six months. Over 850 gastroenterology clinics have integrated remote monitoring dashboards to optimize follow-up cycles. These technologies also enable early intervention alerts, reducing emergency gastritis-related visits by approximately 18% and strengthening market demand for integrated digital care ecosystems.

The Chronic Gastritis Treatment market is structured across three major segmentation pillars—types, applications, and end-users—each contributing distinctly to therapeutic decision-making and adoption dynamics. Product types show rising specialization, driven by antibiotic resistance patterns, clinical guideline updates, and differentiated therapeutic performance outcomes. Application segments reflect deepening integration of diagnostic technologies, precision therapy tools, and structured care-management systems, with hospitals and specialized gastroenterology centers leading utilization. End-user insights highlight strong adoption among advanced healthcare facilities with growing participation from outpatient clinics and diagnostic laboratories. Collectively, these segmentation layers offer a comprehensive view of demand behavior, technological evolution, and treatment standardization shaping the market’s progression.

The Chronic Gastritis Treatment market by type includes proton pump inhibitors (PPIs), H. pylori eradication antibiotics, gastroprotective agents, and emerging microbiome-modulating therapies. PPIs currently account for the largest share at 46% due to their high prescription volume and consistent efficacy in acid suppression across diverse patient profiles. Antibiotic-based eradication therapies hold around 32% share, driven by widespread clinical guidelines recommending combination regimens for H. pylori–linked chronic gastritis. However, microbiome-modulating therapies are expanding fastest, expected to grow at an estimated 8.4% CAGR, supported by rising demand for targeted inflammation control and reduced antimicrobial resistance risk. Gastroprotective agents, including mucosal-healing formulations, represent a niche but significant group, collectively contributing 22% of the remaining market segments. Their role is strengthening with growing adoption in elderly populations and patients requiring long-term gastric protection.

Applications in the Chronic Gastritis Treatment market span H. pylori eradication, acid suppression therapy, mucosal protection, and inflammation-modulation programs. H. pylori eradication remains the leading application with 49% share, driven by the high global prevalence of infection and strong clinical dependencies on multi-drug regimens. Acid suppression applications account for 28% of usage, supported by broad utility across chronic and recurrent cases. However, inflammation-modulation programs represent the fastest-growing application segment, expected to expand at approximately 7.9% CAGR as healthcare facilities adopt biomarker-driven monitoring and targeted anti-inflammatory therapies. Mucosal protection, holding a combined 23% share alongside smaller adjunctive therapy applications, continues gaining traction as long-term therapy needs rise among aging populations.

In 2024, advanced inflammation-monitoring platforms were implemented across multiple international hospitals, enabling early intervention for more than 1.8 million patients and reducing recurrent gastritis flare-ups by 19% through precise, data-driven therapeutic adjustments.

End-user segmentation in the Chronic Gastritis Treatment market includes hospitals, gastroenterology clinics, diagnostic laboratories, and ambulatory care centers. Hospitals dominate with a 52% share owing to high treatment intensity, advanced diagnostic capabilities, and structured management pathways for chronic gastric conditions. Gastroenterology clinics account for 28% of adoption, supported by rising global patient inflow and specialist-driven therapeutic planning. Diagnostic laboratories represent the fastest-growing end-user category, expected to expand at an estimated 8.8% CAGR, driven by increased uptake of non-invasive testing and antimicrobial resistance screening. Ambulatory care centers and other distributed care units share the remaining 20%, reflecting growing patient preferences for rapid diagnostics and shorter visit durations.

Asia-Pacific accounted for the largest market share at 37% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 5.4% between 2025 and 2032.

Strong differences in diagnostic adoption, therapeutic modernization rates, antimicrobial resistance prevalence, and healthcare digitalization continue to shape regional performance. Europe contributed 29% of global treatment volume in 2024 due to standardized clinical pathways, while South America held 11%, supported by improving public healthcare penetration. The Middle East & Africa contributed 9%, driven by rising endoscopy capacity and increased investments in gastrointestinal disease management. Each region exhibits unique behavioral trends—Asia-Pacific displays higher early-diagnosis participation at 58%, whereas North America leads in advanced combination therapy utilization at 44%. These factors collectively define the region-wise distribution of the Chronic Gastritis Treatment market.

North America holds approximately 31% share of the Chronic Gastritis Treatment market due to extensive diagnostic infrastructure, high awareness levels, and strong uptake of multi-drug eradication protocols. Healthcare, biopharma, and clinical research institutions represent the primary industries driving demand, supported by regulatory frameworks promoting antimicrobial stewardship and responsible antibiotic use. Digital transformation is advancing rapidly, with over 62% of hospitals in the region deploying AI-assisted endoscopy and automated mucosal assessment tools. A leading local player introduced an enhanced H. pylori detection kit in 2024 that increased detection speed by 28%. Consumer behavior shows higher adoption of digital health management tools, with 54% of chronic gastritis patients using remote monitoring platforms. These combined trajectories reinforce North America’s strong market position.

Europe represents around 29% of the Chronic Gastritis Treatment market, with leading contributions from Germany, the UK, and France. Regional regulatory bodies enforcing stricter clinical guidelines for H. pylori treatment continue to shape demand for standardized diagnostic and therapeutic processes. Sustainability-driven healthcare initiatives also promote reduced antibiotic misuse and enhanced testing accuracy. Adoption of emerging technologies is growing, with over 46% of tertiary hospitals incorporating digital pathology tools for gastritis assessments. A European biotech firm recently expanded its mucosal-healing therapy trials to support broader treatment availability. Consumer behavior in the region is strongly shaped by regulatory pressure, prompting rising demand for highly validated, explainable diagnostic systems that align with clinical evidence standards.

Asia-Pacific holds the highest treatment volume globally and remains the fastest-expanding region by adoption dynamics. China, India, and Japan collectively represent over 63% of regional consumption due to high infection prevalence and strong government support for gastrointestinal disease programs. Diagnostic infrastructure modernization is accelerating, with over 5,000 new endoscopy units added between 2022 and 2024. Innovation hubs across Japan and South Korea are advancing microbiome therapies and digital diagnostic systems. A notable regional manufacturer scaled production of non-invasive H. pylori test kits by 34% in 2024 to meet rising demand. Consumer behavior trends exhibit strong reliance on mobile health apps and digital triage tools, with adoption rates exceeding 61% across major population centers.

South America accounts for nearly 11% of the Chronic Gastritis Treatment market, with Brazil and Argentina representing the largest consumption bases. Healthcare system improvements, expanded insurance coverage, and investment in diagnostic centers continue to increase access to gastritis screening and treatment. Infrastructure upgrades in public hospitals boosted endoscopy capacity by 22% between 2021 and 2024. Government-backed pharmaceutical regulations support improved antimicrobial stewardship, reducing inappropriate antibiotic prescriptions. A clinical research institute based in Brazil introduced a localized treatment adherence program that improved patient compliance by 17%. Consumer behavior is shaped by rising digital engagement, with strong interest in bilingual medical content and personalized treatment guidance tools across urban regions.

The Middle East & Africa collectively contribute around 9% to the Chronic Gastritis Treatment market, driven by increasing demand from the UAE, Saudi Arabia, and South Africa. Rising investments in private healthcare facilities and gastrointestinal care units have increased diagnostic throughput by 19% over the past three years. Technological modernization—particularly AI-assisted imaging and automated laboratory diagnostics—is accelerating adoption. Regional trade partnerships and healthcare diversification programs further support availability of advanced therapeutics. A healthcare group in the UAE deployed a new digital gastritis monitoring system that improved follow-up adherence by 23%. Consumer preferences lean toward convenience-oriented care, with strong uptake of mobile-based symptom-tracking tools across major urban clusters.

China – 22% Market Share: Strong dominance driven by extensive diagnostic capacity, high treatment volume, and rapidly expanding adoption of non-invasive gastritis testing solutions.

United States – 18% Market Share: Leadership supported by advanced healthcare infrastructure, widespread implementation of combination therapy protocols, and accelerated integration of AI-assisted gastrointestinal diagnostics.

The Chronic Gastritis Treatment market displays a moderately consolidated structure, with an estimated 35–40 active competitors operating across pharmaceuticals, diagnostics, and therapeutic technologies. The top five companies collectively account for approximately 48% of the total market share, reflecting strong dominance by established global pharmaceutical brands with extensive gastrointestinal drug portfolios. Competition is defined by accelerated product innovation, with over 30 new formulation enhancements, combination therapies, and dosage-optimized drugs introduced between 2022 and 2024 to improve treatment adherence and symptom relief precision.

Strategic initiatives continue to intensify market rivalry, with more than 20 notable partnerships emerging in 2023–2024 between drug manufacturers, clinical research organizations, and regional distributors to support expanded trial networks and the faster rollout of proton pump inhibitors, H. pylori eradication therapies, and inflammation-modulating drugs. Mergers and licensing agreements are becoming instrumental, with at least 15 transaction-based strategic moves reported during the same period, strengthening therapeutic pipelines and expanding manufacturers’ access to rapidly growing patient pools in Asia-Pacific and Latin America.

Innovation trends are significantly shaping competitive dynamics, with an estimated 40% of the active players investing in advanced drug-delivery systems, such as sustained-release capsules and non-invasive therapeutic regimens designed to reduce dosing frequency by up to 30%. Additionally, digital health integration—including symptom-monitoring apps and remote adherence tools—has grown by nearly 25% year-on-year, enabling companies to improve treatment outcomes and differentiate their offerings. Overall, competition remains intense, with a clear emphasis on expanding clinical efficacy, enhancing patient compliance, and increasing global distribution efficiency.

Takeda Pharmaceutical Company

AstraZeneca

AbbVie

Pfizer Inc.

GlaxoSmithKline (GSK)

Johnson & Johnson

Bayer AG

Novartis AG

Dr. Reddy’s Laboratories

Cipla Ltd.

Technological advancements in the Chronic Gastritis Treatment market are reshaping therapeutic outcomes, diagnostic accuracy, and long-term disease management. Drug formulation technologies have progressed significantly, with nearly 45% of new product approvals in 2023–2024 featuring optimized-release mechanisms that improve mucosal healing rates by 25–35%. The adoption of combination-therapy engineering has expanded, allowing targeted suppression of gastric inflammation and more effective H. pylori eradication through dual-action and triple-action drug architectures. Precision diagnostics are playing a transformative role, with non-invasive testing technologies—such as urea breath analyzers, stool antigen assays, and next-generation serology—gaining 30% higher clinical usage in 2024 compared to two years prior. Digital gastroscopy systems equipped with high-resolution optics and AI-supported image classification now enable early detection accuracy improvements of up to 40%, reducing misdiagnosis and allowing personalized treatment planning. Machine-learning–powered diagnostic workflows are increasingly adopted in hospitals, with adoption rates rising across North America and East Asia.

Biologics and advanced therapeutics are also influencing market direction. Approximately 20% of ongoing clinical programs for chronic gastritis now involve monoclonal antibodies and microbiome-modulating therapies designed to regulate inflammatory pathways and restore gastric microbial balance. Nanotechnology-based drug delivery, including nano-encapsulated PPIs and antibiotics, is demonstrating enhanced absorption and up to 50% improved bioavailability in trial settings, positioning it as a key future growth driver. Digital health technologies are integrating into treatment pathways, supported by an estimated 35% rise in mobile adherence-tracking applications. These tools, along with remote monitoring platforms, enable physicians to evaluate symptom progression and treatment response in real time, strengthening patient compliance. Collectively, these technological innovations are driving a more precise, efficient, and patient-centric ecosystem for chronic gastritis management.

In 2024, a randomized multicenter study demonstrated that a 10-day regimen of vonoprazan plus levofloxacin and amoxicillin achieved a 91.4% H. pylori eradication rate, outperforming the standard 14-day omeprazole triple therapy, with significantly fewer side-effects reported. (Medscape)

Also in 2024, a real-world Chinese study of a 14-day vonoprazan-based bismuth quadruple therapy achieved a 96.4% eradication rate in per-protocol analysis, highlighting the potency and safety of PCAB-based regimens. (Lippincott Journals)

In 2024, the American College of Gastroenterology (ACG) updated its H. pylori treatment guidelines to recommend bismuth quadruple therapy as first-line for treatment-naïve patients, citing rising clarithromycin and levofloxacin resistance and cautioning against empirical triple therapy without susceptibility testing.

Also, in 2023–2024, clinical practitioners began reporting treatment success with intravenous antibiotic regimens (e.g., IV doxycycline plus IV ceftriaxone) for refractory H. pylori infections in patients who failed multiple oral therapies, offering a novel salvage pathway. (Lippincott Journals)

The Chronic Gastritis Treatment Market Report covers a comprehensive landscape of therapeutic modalities, diagnostic techniques, and disease-management strategies across global regions. The scope includes segmentation by product type (such as proton pump inhibitors, bismuth-based quadruple regimens, microbiome-modulating therapies, and adjunctive gastroprotective agents) and applications (H. pylori eradication, acid suppression, mucosal healing, and inflammation control). The report also examines end-user categories, including hospitals, gastroenterology clinics, diagnostic laboratories, and remote-monitoring systems.

Geographically, the report spans six key regions—North America, Europe, Asia-Pacific, Latin America, Middle East & Africa—providing detailed analyses of adoption patterns, regulatory environments, and infrastructure readiness in each. The technology dimension of the report highlights both current systems (e.g., urea breath test, AI-assisted endoscopy) and emerging innovations (such as AI-clinician recommendation engines, nanotechnology drug delivery, and microbiome therapies).

In addition, the report evaluates key industry drivers and risks, including antimicrobial resistance trends, guideline changes, and ESG-related pharmaceutical waste management. It profiles strategic initiatives by major market players, joint ventures, product launches, and R&D pipelines. For business decision-makers, the report offers actionable insights into unmet needs, competitive positioning, and growth levers across therapeutic and diagnostic ecosystems for chronic gastritis.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 158.84 Million |

|

Market Revenue in 2032 |

USD 225.886461342967 Million |

|

CAGR (2025 - 2032) |

4.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Takeda Pharmaceutical Company , AstraZeneca , AbbVie , Pfizer Inc., GlaxoSmithKline (GSK), Johnson & Johnson, Bayer AG, Novartis AG, Dr. Reddy’s Laboratories, Cipla Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |