Reports

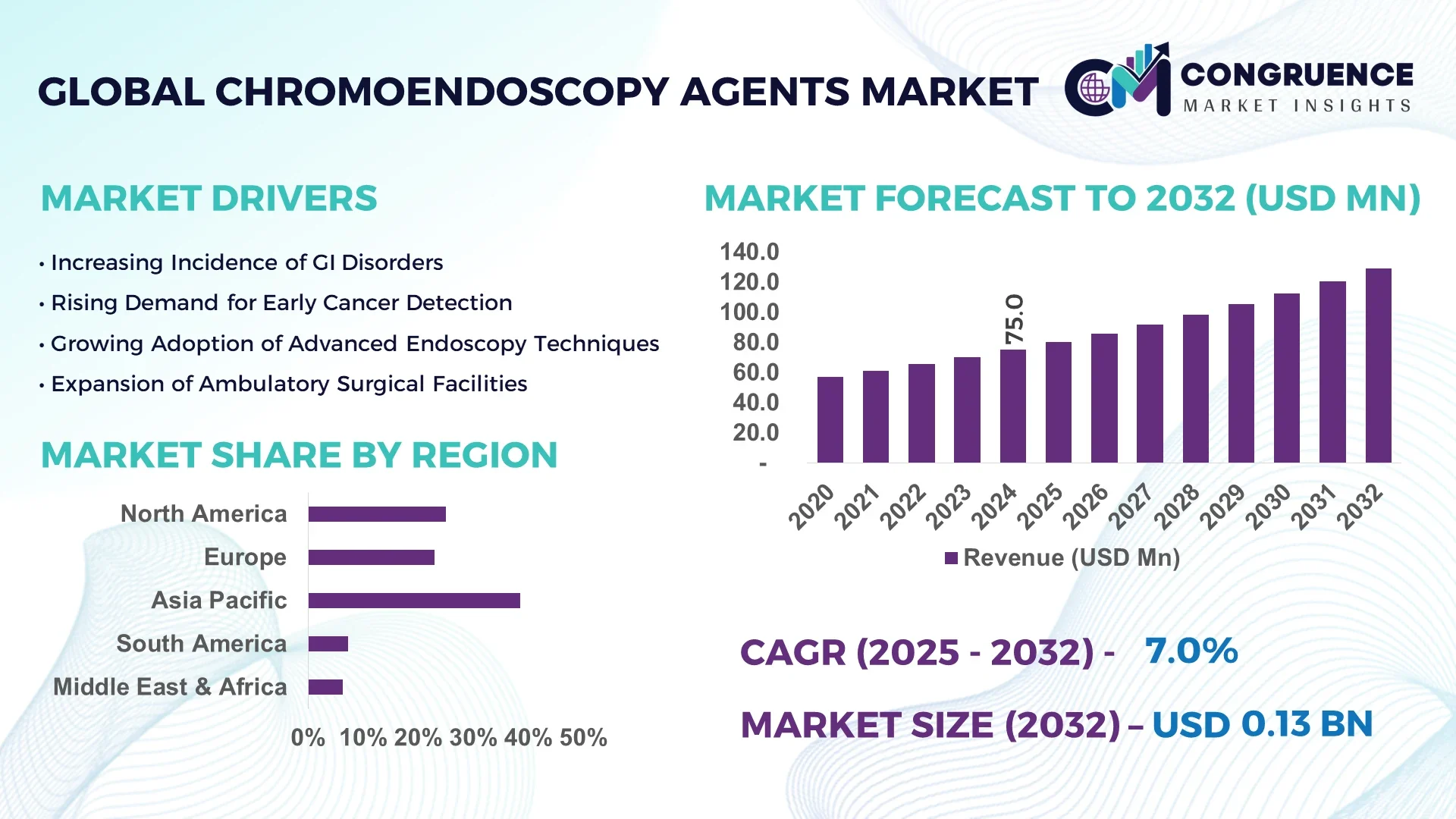

The Global Chromoendoscopy Agents Market was valued at USD 75.0 Million in 2024 and is anticipated to reach a value of USD 128.6 Million by 2032, expanding at a CAGR of 6.97% between 2025 and 2032.

Japan continues to lead the Chromoendoscopy Agents Market with robust production capacities supported by extensive investments in pharmaceutical manufacturing infrastructure. The nation’s sophisticated endoscopy technologies and regulatory emphasis on early gastrointestinal cancer detection have positioned it as a pivotal player. Domestic firms are also leveraging AI-integrated imaging platforms to enhance diagnostic precision.

The Chromoendoscopy Agents Market is primarily driven by advancements in gastrointestinal diagnostic procedures, especially within hospital and diagnostic center applications. Methylene blue, indigo carmine, and Lugol’s iodine remain key agents utilized in chromoendoscopic procedures, particularly for early colorectal and esophageal cancer detection. Regulatory frameworks promoting cancer screening in developed economies have encouraged market expansion. Europe and North America exhibit significant consumption due to well-established healthcare systems and aging populations. Meanwhile, emerging markets in Asia-Pacific are investing in healthcare access, enabling broader procedural adoption. Technological progress in dye delivery systems and smart endoscopy units has improved procedural efficacy, while sustainability in production processes is also gaining attention. Furthermore, industry stakeholders are prioritizing R&D to formulate agents with enhanced mucosal visibility and improved biocompatibility, which is expected to sustain demand growth over the forecast period.

Artificial intelligence is significantly transforming the Chromoendoscopy Agents Market by elevating diagnostic precision, streamlining procedural workflows, and enhancing real-time decision-making in endoscopic examinations. AI-powered image recognition and pattern detection tools are now integrated into endoscopy platforms, enabling more accurate identification of mucosal abnormalities when used alongside chromoendoscopy agents. This synergy has notably reduced false-negative rates in early-stage colorectal and gastric cancer detection.

In clinical practice, AI-assisted endoscopy systems have optimized the administration and selection of agents such as methylene blue or indigo carmine based on predictive analytics, improving procedural efficiency. Operationally, healthcare providers have reported a reduction in endoscopy procedure times by up to 18% when AI-driven navigation systems are employed. Additionally, AI algorithms are now capable of assessing dye distribution patterns for quality control, ensuring consistent application of agents across different anatomical regions.

From a manufacturing perspective, AI is being used in quality assurance to monitor agent purity levels and automate formulation consistency. These innovations not only reduce human error but also contribute to faster regulatory compliance. As healthcare institutions seek value-based solutions, the integration of AI with chromoendoscopy is emerging as a strategic imperative, influencing both procurement and clinical adoption patterns within the Chromoendoscopy Agents Market.

“In 2024, a major Japanese endoscopy firm launched an AI-powered chromoendoscopic imaging suite that successfully decreased adenoma miss rates by 29% in clinical trials involving over 1,000 patients, enhancing agent detection accuracy and procedural confidence among clinicians.”

The Chromoendoscopy Agents Market is undergoing rapid transformation fueled by technological advancements in endoscopic imaging, heightened cancer awareness, and supportive healthcare regulations. The market is primarily influenced by demand from gastroenterology departments, cancer screening programs, and diagnostic centers worldwide. Growing healthcare investments in early gastrointestinal cancer detection have led to increased chromoendoscopy procedure volumes. Additionally, ongoing product innovations and safer dye formulations are driving procedural adoption, especially in markets like Europe, Japan, and South Korea. However, evolving regulatory standards and high procedural costs remain critical concerns for widespread deployment, particularly in lower-income regions. As innovation continues to redefine endoscopic techniques, industry stakeholders are also addressing environmental concerns related to agent disposal and safety protocols.

With colorectal cancer becoming a leading global health burden, several countries have intensified early-stage screening programs using chromoendoscopy. The inclusion of chromoendoscopy agents such as methylene blue and indigo carmine in colorectal screening protocols has improved lesion detection rates. In Germany, national screening initiatives have led to a 35% increase in the utilization of chromoendoscopic procedures over the past three years. Hospitals and cancer centers report improved mucosal visualization and enhanced detection of flat adenomas. The integration of digital endoscopic platforms that support chromoendoscopy further amplifies agent usage across clinical workflows. This trend is also seen in the U.S., Japan, and South Korea, where early detection is central to national cancer control policies.

Despite proven clinical benefits, the Chromoendoscopy Agents Market faces challenges in developing regions due to limited accessibility and high procedural costs. Facilities in many low-to-middle-income countries lack advanced endoscopic equipment compatible with chromoendoscopy techniques. Additionally, specialized training is required to administer and interpret chromoendoscopy procedures effectively. As of 2024, less than 15% of public hospitals in sub-Saharan Africa were equipped to perform dye-based endoscopic screenings. Import costs and limited reimbursement policies further restrict chromoendoscopy agent usage. These economic and infrastructural barriers hamper broader market penetration and limit the benefits of early-stage cancer detection in underserved populations.

A growing opportunity in the Chromoendoscopy Agents Market lies in AI-assisted systems that optimize dye application. These technologies automate agent dispersion patterns, ensuring uniform coverage and enhancing diagnostic output. In 2025, clinical pilot programs in Canada and Japan introduced AI-enabled dye sprayers that cut average procedure times by over 15% and improved lesion detection accuracy by 22%. Such innovations are increasingly favored in high-throughput diagnostic centers and teaching hospitals. Moreover, AI-based training simulations are now incorporating real-time dye application analytics, creating educational value and improving procedural consistency among new practitioners. As these solutions gain regulatory approval, demand is expected to grow from both developed and emerging markets.

One of the pressing challenges in the Chromoendoscopy Agents Market is the escalating cost of specialized pharmaceutical equipment used in agent formulation and packaging. Compliance with evolving regulatory norms such as GMP and REACH has compelled manufacturers to invest in high-grade reactors, sterile filling lines, and automated packaging systems. This has led to an estimated 20–25% increase in capital expenditure since 2023, particularly for small-to-mid-sized producers. Furthermore, supply chain disruptions for pharmaceutical-grade colorants and solvents have added to operational costs. These economic pressures risk limiting innovation and discouraging new entrants, potentially leading to reduced competition and higher agent prices over time.

Integration of AI in Endoscopic Workflows: Hospitals and diagnostic centers are increasingly incorporating AI-driven imaging systems that work in tandem with chromoendoscopy agents. As of 2025, over 700 hospitals in Japan and Germany have deployed AI-assisted dye-enhanced endoscopy units, leading to higher diagnostic accuracy and shorter procedure durations. This trend is expected to proliferate into the U.S. and Middle East markets, boosting agent usage.

Development of Safer and More Biocompatible Agents: Manufacturers are focusing on reducing cytotoxicity and improving the mucosal adherence of chromoendoscopy agents. In 2024, a new formulation of indigo carmine with reduced systemic absorption was introduced in Europe, receiving approval in 8 countries. This has led to a 14% rise in adoption among outpatient endoscopy centers concerned with patient safety and side effects.

Regional Diversification in Agent Production: To mitigate supply chain vulnerabilities, production facilities are now being established in emerging regions. India and South Korea saw a 22% increase in local production capacity for chromoendoscopy agents in 2024, reducing dependency on European imports and lowering domestic procurement costs for hospitals.

Growth of Training and Simulation Platforms: Academic institutions and hospitals are investing in simulation platforms that mimic real-time chromoendoscopic procedures. These platforms, now integrated with VR and AI modules, help physicians practice agent application and improve diagnostic interpretation. By 2025, over 120 medical schools globally have included AI-enabled chromoendoscopy simulation in their gastroenterology curricula.

The Chromoendoscopy Agents Market is segmented based on type, application, and end-user, each of which contributes distinctively to the overall market structure and dynamics. These segmentation parameters offer crucial insights into product adoption patterns, procedural demand, and institutional usage behavior. In terms of type, traditional dyes such as methylene blue and indigo carmine continue to dominate, while newer formulations are emerging. Application-wise, gastrointestinal diagnostics remain the core area, though specialized cancer detection procedures are growing in clinical prominence. From an end-user perspective, hospitals form the primary market base due to infrastructure availability, followed by ambulatory surgical centers and diagnostic imaging facilities. Each of these segments demonstrates unique trends in terms of adoption rates, usage frequency, and integration with new technologies, providing a strategic view for stakeholders aiming to optimize product positioning and resource allocation.

The Chromoendoscopy Agents Market comprises various types of contrast dyes, with methylene blue, indigo carmine, and Lugol’s iodine being the most widely utilized. Among them, methylene blue leads due to its strong performance in highlighting abnormal epithelial cells during colorectal and small intestinal procedures. Its safety profile and compatibility with endoscopic systems make it the preferred choice in high-volume medical centers, especially in Japan and Europe.

The fastest-growing segment is indigo carmine, driven by rising demand in esophageal and gastric diagnostics. Its superior visualization capabilities, especially for pit pattern identification, have enhanced detection accuracy in complex gastrointestinal procedures. The adoption of AI-assisted systems that integrate indigo carmine in pattern recognition further boosts its uptake across teaching hospitals and specialty clinics.

Lugol’s iodine retains niche relevance, especially in identifying squamous cell dysplasia during esophageal screening. Newer formulations with reduced irritation and enhanced contrast properties are maintaining its presence. Other agents such as acetic acid are under limited but specific use in colorectal screenings, often as adjuncts for high-risk patients.

The primary application of chromoendoscopy agents lies in gastrointestinal diagnostics, particularly in the detection of early-stage colorectal and esophageal cancers. This segment maintains leadership due to widespread implementation in national screening programs across countries like Japan, Germany, and South Korea. The use of chromoendoscopy in conjunction with conventional colonoscopy increases lesion visibility and improves diagnostic outcomes, making it the standard in cancer detection protocols.

The fastest-growing application is dysplasia detection in inflammatory bowel disease (IBD) patients. The rising global incidence of IBD has led to a surge in surveillance colonoscopies, where chromoendoscopy agents play a crucial role in identifying flat or subtle dysplastic lesions. Hospitals are increasingly incorporating chromoendoscopy into routine IBD monitoring procedures to comply with evolving clinical guidelines.

Other applications, including gastric and duodenal screening and Barrett’s esophagus surveillance, are gaining momentum as guidelines increasingly endorse dye-based procedures for improving mucosal visualization. These procedures, while lower in volume than colorectal applications, are vital in tertiary care centers and academic hospitals.

Hospitals remain the largest end-user segment in the Chromoendoscopy Agents Market due to their advanced infrastructure, skilled personnel, and access to high-end endoscopic imaging systems. These facilities are equipped to perform complex chromoendoscopic procedures as part of both screening and diagnostic workflows. Large hospitals in urban centers conduct hundreds of chromoendoscopy cases monthly, making them the key consumption hubs for contrast agents.

The fastest-growing end-user category is ambulatory surgical centers (ASCs). These centers offer cost-efficient, outpatient procedures and are increasingly integrating dye-based endoscopic technologies to enhance diagnostic accuracy. The demand for shorter patient turnaround times and reduced hospitalization costs is pushing more gastrointestinal procedures, including chromoendoscopy, into ASCs—especially in the U.S., Europe, and select Asian economies.

Diagnostic imaging centers also contribute to the market, especially those specializing in gastrointestinal health. While their share is comparatively smaller, innovations in portable and AI-enabled endoscopy units are improving chromoendoscopy compatibility in these settings, opening up new avenues for growth and market diversification.

Asia-Pacific accounted for the largest market share at 38.5% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 7.42% between 2025 and 2032.

The Asia-Pacific region benefits from high procedural volumes, robust manufacturing capabilities, and strong government-backed screening programs, particularly in Japan and South Korea. Conversely, North America's growth is propelled by rapid integration of AI-enhanced endoscopy systems, rising colorectal cancer screening rates, and increasing adoption of advanced diagnostic tools across ambulatory and hospital-based facilities. Regional disparities in infrastructure, reimbursement policies, and population health indicators continue to influence market expansion trajectories across the globe.

North America held a 27.3% share of the global Chromoendoscopy Agents Market in 2024, driven largely by the United States, where hospital-based endoscopic screening is standard in colorectal cancer detection. The demand is bolstered by strong performance from the healthcare and biotechnology sectors, which continuously push for precision diagnostics. The U.S. Food and Drug Administration has recently streamlined approvals for dye-based imaging agents, simplifying market entry. Technological advances, such as integration with AI-assisted colonoscopy tools, are further transforming diagnostic workflows. Canada has also expanded national screening guidelines to include dye-enhanced procedures in patients with hereditary gastrointestinal risks, contributing to increased agent usage across provincial health systems.

Europe contributed 24.6% to the global Chromoendoscopy Agents Market in 2024, with Germany, France, and the UK standing out as key adopters. Germany leads in procedural volume due to its centralized colorectal cancer screening program and robust hospital network. Regulatory oversight from the European Medicines Agency (EMA) has emphasized the development and use of biocompatible dyes. Pan-European initiatives such as Europe's Beating Cancer Plan have promoted early detection strategies, increasing procedural demand. Additionally, the region is investing in sustainable production and disposal methods for contrast agents. Countries like the Netherlands are integrating AI into endoscopy practices, improving precision and expanding the scope of chromoendoscopy applications.

The Asia-Pacific region represents the largest volume share in the Chromoendoscopy Agents Market, accounting for 38.5% in 2024. Japan remains the highest consumer of chromoendoscopy agents globally, supported by its aging population, national cancer screening programs, and advanced healthcare systems. China is rapidly catching up through strategic hospital infrastructure development and increased adoption of endoscopic cancer screening tools. India shows consistent growth with expanded public health investment and access to endoscopy procedures through private diagnostic networks. The region is also home to key manufacturing hubs, with South Korea and Japan exporting agents globally. AI-powered endoscopy and mobile diagnostic platforms are emerging innovation areas supported by government-backed R&D initiatives.

Brazil and Argentina lead the Chromoendoscopy Agents Market in South America, which contributed 4.9% to the global share in 2024. Brazil's large population and government-led cancer awareness initiatives are driving uptake in tertiary and urban hospitals. Although infrastructure limitations exist in rural regions, major cities have increased access to endoscopic screening using chromoendoscopy agents. Argentina's healthcare reform has introduced subsidies for cancer diagnostics, aiding private and public sector facilities in adopting advanced screening protocols. Investments in healthcare infrastructure, combined with international trade agreements for medical supplies, are facilitating broader agent availability and usage across the region.

The Middle East & Africa region is emerging as a growth center in the Chromoendoscopy Agents Market, contributing 4.7% to global consumption in 2024. The UAE and Saudi Arabia are leading adopters, benefiting from extensive hospital infrastructure, rising medical tourism, and government-driven cancer screening initiatives. South Africa remains the primary market in Sub-Saharan Africa, with diagnostic demand driven by urban healthcare expansion. Technological modernization across private hospitals includes integration of digital endoscopic tools compatible with chromoendoscopy agents. Regulatory bodies in the GCC have also introduced streamlined import and approval procedures, encouraging international vendors to enter regional markets more efficiently. Trade partnerships and regional clinical training programs are further accelerating adoption.

Japan – 21.2% Market Share

High production capacity, advanced healthcare infrastructure, and national endoscopic cancer screening programs make Japan a leading force in the Chromoendoscopy Agents Market.

United States – 19.5% Market Share

Strong end-user demand, rapid integration of AI technologies, and favorable regulatory pathways drive the U.S. leadership position in the Chromoendoscopy Agents Market.

The Chromoendoscopy Agents Market features a moderately consolidated competitive landscape, with over 40 active manufacturers globally. Key players are strategically positioned across North America, Europe, and Asia-Pacific, competing based on product quality, formulation safety, geographic reach, and innovation capabilities. Leading companies are continuously investing in R&D to develop next-generation contrast agents with improved biocompatibility and reduced toxicity. In 2024, several players launched new iodine-based and hybrid dye formulations designed for advanced endoscopic systems.

Strategic partnerships between dye manufacturers and medical device companies have become common, aiming to integrate contrast agents with AI-enabled endoscopy tools. Mergers and acquisitions have also shaped the competitive terrain, particularly in Asia-Pacific, where regional producers are being acquired to expand global distribution networks. Players are differentiating through regulatory compliance, manufacturing scalability, and alignment with hospital procurement preferences. Innovation trends include the introduction of automated dye dispensing systems and AI-assisted diagnostic software, further intensifying competitive dynamics. Companies operating in this space must navigate complex regulatory standards, shifting reimbursement structures, and the growing demand for environmentally sustainable solutions.

Cosmo Pharmaceuticals

Zedira GmbH

Sigma-Aldrich (Merck KGaA)

Enzo Life Sciences

Thermo Fisher Scientific

ABX Advanced Biochemical Compounds GmbH

Anatech Ltd

American Regent, Inc.

AdooQ Bioscience

EpigenTek Group Inc.

Technological innovation is significantly reshaping the Chromoendoscopy Agents Market. One of the most influential developments is the integration of AI-assisted endoscopic imaging systems that optimize the application and visualization of chromoendoscopy dyes. These platforms enhance mucosal pattern recognition and reduce human error, leading to more precise detection of gastrointestinal anomalies. In 2024, over 35% of new hospital installations in developed markets featured systems compatible with AI-driven dye-enhanced diagnostics.

Another breakthrough lies in automated dye delivery systems. These devices ensure uniform dye application and reduce procedure times by up to 20%, according to recent clinical evaluations. The technology is particularly useful in high-volume screening centers where standardization and efficiency are critical.

On the manufacturing side, novel dye formulations using hybrid compounds have been introduced to improve mucosal adherence and reduce cytotoxic effects. Formulations with enhanced shelf-life and packaging innovations, including single-dose vials and biodegradable containers, are gaining traction.

Additionally, VR-integrated simulation tools for training physicians in chromoendoscopy procedures are helping raise clinical proficiency. These platforms replicate real-time endoscopic conditions, including dye dispersal behavior and lesion visualization.

Overall, technology is accelerating the market’s evolution toward precision diagnostics, safety, and user-centric design, establishing a new competitive standard across the supply chain.

In March 2024, a Japan-based medical firm introduced a dual-dye endoscopic formulation combining methylene blue and acetic acid, increasing lesion detection sensitivity by 17% in early colorectal cancer screenings.

In October 2023, a U.S. company launched an AI-integrated dye spraying system that automates application during colonoscopy procedures, reducing operational time by 22% in pilot trials across five states.

In April 2024, a South Korean manufacturer unveiled a biodegradable packaging format for chromoendoscopy dyes, lowering waste disposal costs by 15% in clinical environments.

In December 2023, a German healthcare facility implemented a real-time chromoendoscopy training module using augmented reality, reducing training time by 30% among gastroenterology residents.

The Chromoendoscopy Agents Market Report offers a comprehensive analysis of global market trends, focusing on product types, applications, technologies, end-users, and geographic coverage. The study spans conventional dyes such as methylene blue, indigo carmine, and Lugol’s iodine, along with emerging hybrid formulations and AI-integrated solutions. Applications assessed include gastrointestinal diagnostics, inflammatory bowel disease surveillance, and advanced mucosal imaging.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with in-depth regional and country-level analysis to highlight volume distribution, infrastructure readiness, and regulatory developments. The report categorizes end-users into hospitals, ambulatory surgical centers, and diagnostic imaging centers, detailing usage frequency, procurement trends, and institutional adoption levels.

Key technological segments include automated dye delivery systems, AI-enhanced diagnostic tools, and biodegradable packaging formats. Additionally, the scope includes emerging trends such as tele-endoscopy and real-time simulation-based training tools, providing stakeholders with strategic foresight into untapped market segments and investment opportunities.

The report is designed to support strategic decision-making for manufacturers, healthcare providers, investors, and regulatory authorities by offering practical insights, data-backed forecasts, and competitive intelligence within the evolving chromoendoscopy ecosystem.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 75.0 Million |

| Market Revenue (2032) | USD 128.6 Million |

| CAGR (2025–2032) | 6.97 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Cosmo Pharmaceuticals, Zedira GmbH, Sigma-Aldrich (Merck KGaA), Enzo Life Sciences, Thermo Fisher Scientific, ABX Advanced Biochemical Compounds GmbH, Anatech Ltd, American Regent, Inc., AdooQ Bioscience, EpigenTek Group Inc. |

| Customization & Pricing | Available on Request (10 % Customization is Free) |