Reports

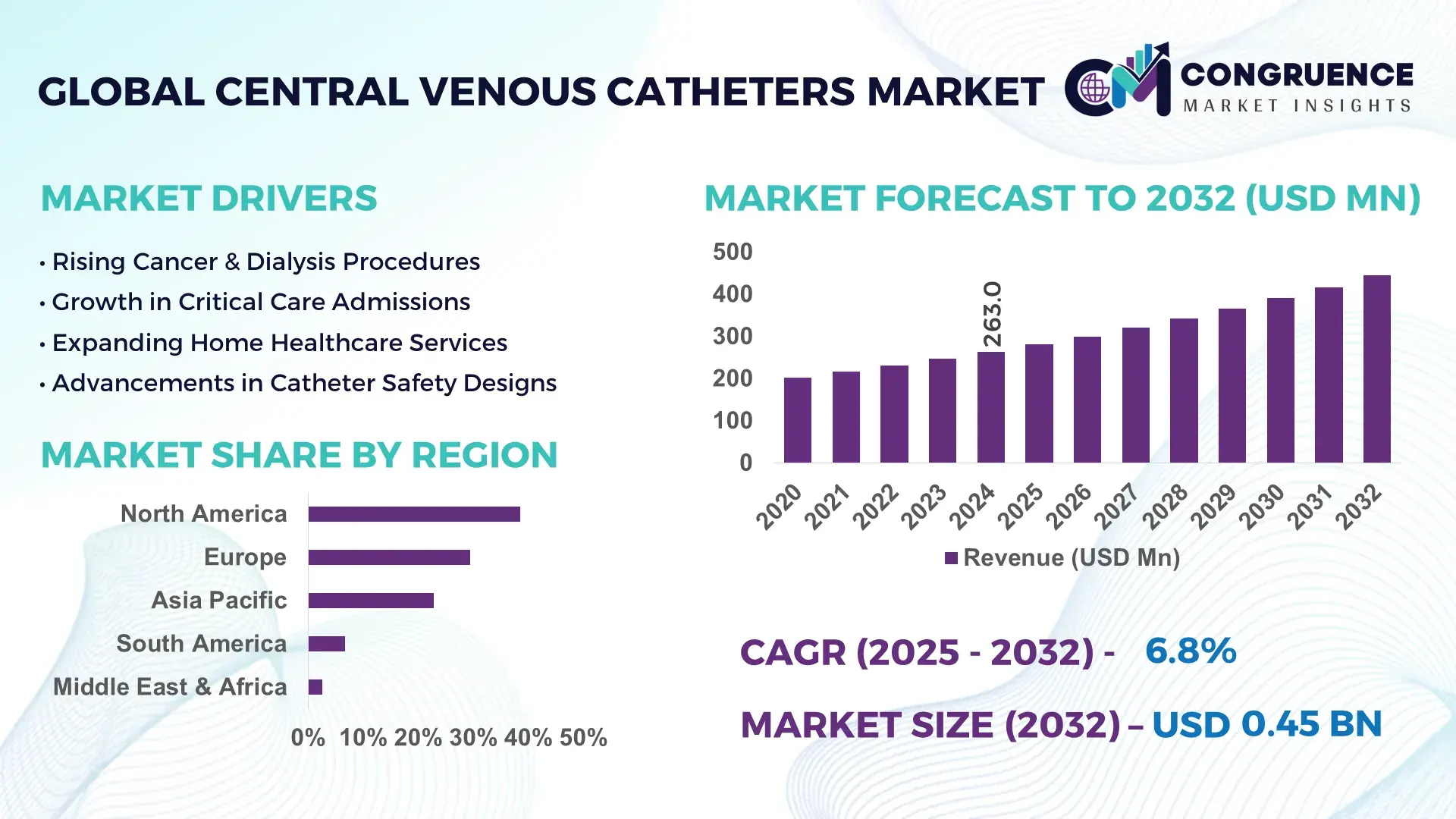

The Global Central Venous Catheters Market was valued at USD 263.0 Million in 2024 and is anticipated to reach a value of USD 445.2 Million by 2032 expanding at a CAGR of 6.80% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is primarily driven by the rising volume of critical care admissions, increasing oncology and dialysis procedures, and broader adoption of long-term vascular access devices across hospital settings.

The United States dominates the Central Venous Catheters Market in terms of industrial activity and clinical utilization. The country hosts more than 600 large acute-care hospitals equipped with advanced vascular access programs and performs over 8 million central line insertions annually across ICUs, oncology units, and dialysis centers. Investment in infection-prevention technologies remains high, with over 45% of hospitals adopting antimicrobial-impregnated catheters and ultrasound-guided insertion systems. Oncology accounts for nearly 38% of total CVC usage, followed by critical care at 34%. Domestic manufacturing capacity supports large-scale production of multilumen and power-injectable catheters, while continued R&D spending has accelerated adoption of integrated tip-location and pressure-sensing technologies, strengthening the country’s leadership in advanced catheter solutions.

Market Size & Growth: USD 263.0 Million in 2024, projected to reach USD 445.2 Million by 2032, expanding at a CAGR of 6.80%, driven by increased critical care and oncology procedures.

Top Growth Drivers: ICU catheter utilization (+41%), oncology infusion demand (+36%), ultrasound-guided placement adoption (+48%).

Short-Term Forecast: By 2028, catheter-related complication rates are expected to decline by approximately 18% due to improved coatings and placement technologies.

Emerging Technologies: Antimicrobial-coated catheters, ECG-based tip confirmation systems, and pressure-enabled safety valves.

Regional Leaders: North America (USD 165.0 Million by 2032 – high ICU adoption), Europe (USD 128.0 Million – regulatory-driven safety upgrades), Asia-Pacific (USD 92.0 Million – expanding hospital capacity).

Consumer/End-User Trends: Hospitals account for over 72% of usage, with oncology units showing the fastest procedural growth.

Pilot or Case Example: In 2024, a hospital network reduced central line-associated infections by 27% after deploying antimicrobial multilumen catheters.

Competitive Landscape: Leading player holds ~21% share, followed by 3–5 global manufacturers each below 12%.

Regulatory & ESG Impact: Infection control mandates and patient safety standards driving device upgrades.

Investment & Funding Patterns: Over USD 180 Million invested globally in catheter innovation and safety enhancement programs.

Innovation & Future Outlook: Integration of smart sensors and AI-guided placement tools shaping next-generation catheter systems.

The Central Venous Catheters Market is primarily supported by hospitals and oncology centers, which together account for over 70% of device usage. Recent innovations in antimicrobial materials and real-time tip verification are improving patient safety, while stricter infection-control regulations and expanding ICU capacity in emerging regions are reinforcing long-term demand and technology upgrades.

The Central Venous Catheters Market holds strategic importance within global healthcare infrastructure due to its critical role in intensive care, oncology treatment, parenteral nutrition, and long-term drug administration. As healthcare systems face rising patient acuity and longer hospital stays, reliable central venous access has become essential for treatment continuity and patient safety. Advanced catheter technologies are increasingly embedded into broader hospital strategies focused on infection reduction, workflow efficiency, and cost containment.

From a technology standpoint, antimicrobial-coated catheters deliver nearly 30% lower infection incidence compared to conventional polyurethane catheters, establishing a clear performance benchmark. North America dominates procedure volume due to high ICU density, while Europe leads in adoption of safety-enhanced catheters, with nearly 52% of hospitals using advanced tip-confirmation systems. In Asia-Pacific, rapid hospital expansion is accelerating catheter demand, particularly in tertiary care centers.

Looking ahead, by 2027, AI-assisted catheter placement tools are expected to reduce insertion-related complications by approximately 22%, improving first-attempt success rates and clinician efficiency. From an ESG perspective, healthcare providers are committing to 25–30% reductions in hospital-acquired infections by 2030, positioning advanced CVCs as a compliance enabler. In 2024, a U.S.-based hospital network achieved a 19% reduction in central line complications through standardized ultrasound-guided insertion protocols. Overall, the Central Venous Catheters Market is evolving into a pillar of clinical resilience, regulatory compliance, and sustainable healthcare delivery.

The Central Venous Catheters Market is shaped by rising hospitalization rates, increasing prevalence of chronic diseases, and growing reliance on invasive monitoring and infusion therapies. Demand is closely linked to ICU admissions, oncology treatments, and dialysis procedures, all of which require stable and long-term vascular access. Technological advancements such as antimicrobial coatings, multi-lumen configurations, and imaging-assisted placement are influencing purchasing decisions across hospitals. Regulatory focus on infection prevention and patient safety continues to drive replacement cycles and product upgrades. Meanwhile, emerging markets are contributing incremental volume growth due to healthcare infrastructure expansion and improved access to advanced medical devices.

The increasing prevalence of cancer, renal failure, and cardiovascular diseases has significantly raised the demand for long-term venous access solutions. Oncology patients account for nearly 40% of long-term CVC placements, while dialysis and critical care represent an additional 45%. ICU expansion and higher survival rates are extending catheter dwell times, increasing overall device utilization. Hospitals are also standardizing central line usage protocols, which has increased procedural volumes by over 30% in large tertiary facilities. These factors collectively reinforce sustained demand for advanced catheter systems.

Despite technological improvements, catheter-related bloodstream infections remain a concern, accounting for up to 15% of ICU-acquired infections globally. Treatment costs, extended hospital stays, and regulatory penalties associated with such infections can limit device adoption or delay procurement decisions. In addition, improper insertion techniques contribute to mechanical complications in approximately 12–14% of cases, emphasizing the need for skilled personnel and training, which can restrain market expansion in resource-limited settings.

Next-generation antimicrobial and antithrombogenic coatings offer opportunities to significantly reduce complication rates. Adoption of power-injectable and sensor-enabled catheters is increasing, with pilot programs showing up to 25% improvement in placement accuracy. Emerging economies upgrading tertiary hospitals represent additional growth avenues, as centralized procurement and public health investments expand access to advanced vascular access devices.

High manufacturing costs associated with advanced materials and integrated technologies raise procurement expenses for hospitals. Compliance with evolving sterilization, biocompatibility, and safety standards requires continuous design validation and testing, increasing development timelines. Smaller healthcare facilities often face budget constraints, limiting adoption of premium catheter solutions despite clinical benefits.

Expansion of Antimicrobial-Coated Catheters: Adoption of antimicrobial-coated CVCs has increased by over 42% in tertiary hospitals, contributing to infection reductions of nearly 20% per 1,000 catheter days.

Growth in Ultrasound-Guided Placement: More than 65% of ICUs now rely on ultrasound-assisted insertion, improving first-attempt success rates by 28% and reducing mechanical complications.

Rising Demand for Multi-Lumen Catheters: Multi-lumen CVCs account for approximately 58% of procedures, supporting simultaneous drug infusion, monitoring, and nutrition delivery in critical care settings.

Integration of Tip-Confirmation Technologies: ECG-based tip location systems are being adopted in 37% of large hospitals, reducing malposition rates by 24% and minimizing the need for confirmatory imaging.

The Central Venous Catheters Market is segmented by type, application, and end-user insights, reflecting diverse clinical requirements, procedural complexity, and care settings. Product segmentation highlights variations in lumen configuration, coating technology, and duration of use, which directly influence clinical outcomes and procurement decisions. Application-based segmentation is driven by the intensity of care and therapy duration, with critical care and oncology accounting for a substantial proportion of catheter utilization due to frequent infusions and monitoring needs. End-user segmentation further differentiates demand patterns across hospitals, ambulatory settings, and specialty care centers, shaped by infrastructure availability, procedural volume, and infection-control protocols. Across segments, adoption is increasingly influenced by safety-enhanced designs, ultrasound-guided placement compatibility, and antimicrobial features, aligning device selection with regulatory compliance and patient safety objectives.

Non-tunneled central venous catheters represent the leading product type, accounting for approximately 44% of total adoption, driven by their widespread use in acute and emergency care settings where short-term vascular access is required. These catheters are commonly deployed in intensive care units for hemodynamic monitoring and rapid medication delivery. In comparison, peripherally inserted central catheters (PICCs) account for nearly 28% of usage, favored for medium- to long-term therapies due to lower insertion-related complications and suitability for outpatient care. However, adoption of tunneled catheters is rising fastest, expanding at an estimated 7.4% CAGR, supported by growing demand for long-term oncology and dialysis access where reduced infection risk is critical. Implantable ports also show steady growth, particularly in chemotherapy applications, offering improved patient mobility and lower maintenance requirements. Collectively, PICCs, tunneled catheters, and implantable ports contribute around 56% of overall demand, reflecting a gradual shift toward longer-dwell solutions.

Critical care remains the dominant application segment, accounting for approximately 37% of total Central Venous Catheters utilization, as ICUs require continuous infusion, pressure monitoring, and rapid vascular access for unstable patients. Oncology follows with nearly 31% adoption, supported by the increasing number of chemotherapy cycles and long-term infusion therapies. Dialysis and renal care applications are expanding fastest, with an estimated 7.9% CAGR, driven by rising chronic kidney disease prevalence and interim catheter use before permanent access creation. Other applications—including parenteral nutrition, blood transfusion, and emergency medicine—collectively account for around 32% of demand, reflecting broad clinical reliance on central access devices. In 2024, more than 43% of hospitals globally reported increased use of long-dwell catheters for oncology and nutrition therapies, while 39% of critical care units adopted standardized central line bundles to optimize catheter utilization.

Hospitals are the leading end-user segment, representing approximately 69% of total Central Venous Catheters usage, due to high procedural volumes, availability of trained clinicians, and concentration of critical and oncology care services. In comparison, ambulatory surgical centers account for about 17% of adoption, primarily supporting short-duration procedures and day-care infusions. Specialty clinics, including oncology and dialysis centers, are the fastest-growing end-user group, expanding at an estimated 8.3% CAGR, as care delivery increasingly shifts toward outpatient and specialized treatment models. Home healthcare and long-term care facilities collectively contribute nearly 14%, reflecting growing acceptance of PICCs and implantable ports for extended therapies. In 2024, over 41% of oncology clinics reported increased reliance on long-term central access devices to support outpatient chemotherapy, while 36% of ambulatory centers expanded catheter-based infusion services.

North America accounted for the largest market share at 38.5% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2025 and 2032.

Regional performance varies significantly based on healthcare infrastructure maturity, procedural volumes, regulatory stringency, and adoption of advanced vascular access technologies. North America leads in installed base and procedural intensity, driven by high ICU bed density and chronic disease prevalence. Europe follows with strong institutional adoption and standardized clinical protocols across public healthcare systems. Asia-Pacific shows accelerated momentum due to rising hospital capacity, increasing cancer and renal disease burden, and expanding domestic manufacturing of medical devices. South America and the Middle East & Africa together represent under 15% of global demand but show improving penetration supported by healthcare investment programs, medical tourism, and gradual technology upgrades. Across all regions, infection prevention compliance, ultrasound-guided insertion practices, and antimicrobial catheter adoption are increasingly shaping procurement and utilization patterns.

The region accounted for approximately 38.5% of global Central Venous Catheters usage in 2024, reflecting high procedural density and advanced care delivery. Demand is primarily driven by hospitals, oncology centers, and dialysis clinics, with over 62% of insertions linked to critical care and cancer treatment. Regulatory frameworks emphasize patient safety and infection prevention, accelerating adoption of antimicrobial-coated and ultrasound-compatible catheters. Digital integration, such as electronic line-tracking systems, is increasingly used to monitor dwell time and reduce complications. Local manufacturers and multinational players have expanded production of safety-engineered catheters, while healthcare providers increasingly prefer multi-lumen designs for complex therapies. Regional consumer behavior shows higher institutional adoption, with nearly 48% of hospitals standardizing central line bundles across all ICUs to improve outcomes and compliance.

Europe holds nearly 29.4% of the global market, supported by strong uptake in Germany, the UK, and France, which together account for over 56% of regional usage. Public healthcare systems emphasize standardized vascular access protocols, supporting consistent demand across tertiary hospitals. Regulatory oversight and sustainability initiatives encourage reduced complication rates and extended device lifecycles. Adoption of emerging technologies, including pressure-rated PICCs and power-injectable catheters, is increasing, particularly in oncology and radiology departments. Regional manufacturers focus on biocompatible materials and recyclable packaging to align with sustainability goals. Consumer behavior reflects high clinician preference for guideline-compliant devices, with more than 45% of facilities prioritizing catheters designed for long-term use and lower infection risk.

Asia-Pacific ranks third by volume but leads in growth momentum, accounting for approximately 22.8% of global demand in 2024. China, India, and Japan collectively contribute over 64% of regional consumption, driven by rising hospitalization rates and expanding oncology care. Infrastructure expansion includes new tertiary hospitals and localized manufacturing hubs producing cost-efficient catheters. Innovation clusters increasingly focus on ultrasound-guided insertion tools and antimicrobial surface technologies. Regional manufacturers are scaling capacity to meet domestic demand and export needs. Consumer behavior indicates rapid adoption in high-volume public hospitals, with over 40% of new ICU beds in major urban centers equipped to support central line procedures.

South America represents approximately 6.7% of global demand, with Brazil and Argentina accounting for nearly 61% of regional usage. Growth is supported by expanding hospital networks and gradual modernization of intensive care units. Government healthcare programs prioritize access to essential medical devices, including vascular access products, while trade policies support imports of advanced catheters. Infrastructure improvements in urban hospitals are increasing procedure volumes. Regional players focus on affordable catheter solutions tailored for public healthcare systems. Consumer behavior reflects demand concentrated in large metropolitan hospitals, where adoption rates are nearly 2× higher than in rural facilities.

The Middle East & Africa region accounts for roughly 2.6% of global usage, with UAE and South Africa emerging as key growth markets. Demand is driven by hospital expansion, private healthcare investment, and medical tourism initiatives. Technological modernization includes adoption of ultrasound-guided insertion and infection-control protocols in tertiary centers. Regional trade partnerships support steady device supply, while regulatory frameworks increasingly emphasize quality standards. Local distributors collaborate with international manufacturers to expand access. Consumer behavior varies widely, with higher adoption in private hospitals, where utilization rates are nearly 35% higher than in public facilities.

United States – 34.2% Market share: High procedural volume, advanced ICU infrastructure, and strong regulatory emphasis on patient safety.

China – 16.8% Market share: Large hospital base, expanding domestic manufacturing, and rising oncology and critical care demand.

The Central Venous Catheters Market is characterized by a moderately concentrated competitive environment with a mix of global medical technology leaders and specialized vascular access device manufacturers. A typical industry analysis indicates 10–15 prominent competitors actively competing across product innovation, geographic reach, and clinical adoption, while the top 10 companies collectively hold approximately 61 % of global market presence—highlighting a balanced competitive landscape with room for both established and emerging players.

Leading firms differentiate through strategic product launches, regulatory clearances, and enhanced clinical safety features, particularly focusing on antimicrobial coatings, heparin-bonded catheters, and smart integration features that address infection control and procedural efficiency. Between 2023 and 2024, major companies introduced over 60 new models with features like infection-reducing chlorhexidine protection, kink-resistant bodies, and high-flow hemodialysis access functionality.

Innovation trends show increased adoption of advanced polymer composites, integrated pressure or placement sensors, and ultrasound-guided insertion enhancements, driving competitive differentiation. Commercial strategies include portfolio expansion into pediatric-specific catheters, AI-assisted placement tools, and broader vascular access system integration across hospitals and outpatient care settings.

The nature of the market combines features of both consolidation and fragmentation: global medtech leaders maintain strong distribution channels and R&D investment, while regional manufacturers compete on niche products and localized service models. Continuous strategic initiatives—including acquisitions, enhanced manufacturing capacity, and digital support tools—enable companies to capture clinical demand across intensive care, oncology, and chronic therapy applications, reinforcing a dynamic, innovation-driven competitive structure.

Becton, Dickinson and Company (BD)

Cook Medical

AngioDynamics

Vygon Ltd.

Smiths Medical

Kimal Healthcare

Comed B.V.

The Central Venous Catheters Market is undergoing significant technological evolution, driven by clinical demands for enhanced safety, precision, and patient outcomes. Central venous catheter technologies now widely incorporate antimicrobial surfaces and biofilm-resistant materials, aimed at cutting the incidence of catheter-related bloodstream infections, which have historically posed a serious clinical challenge. Recent industry developments reveal that over 60 % of new catheter models introduced between 2023 and 2024 include coatings or surface treatments targeting infection control, reflecting a priority in design for patient safety and regulatory compliance.

Advanced polymer composites, such as flexible polyurethane and silicone blends, are increasingly used to improve catheter durability and reduce vascular irritation, broadening the scope for long-term use in chronic therapies like chemotherapy and dialysis. Manufacturers are also integrating smart sensor technology into catheter systems, enabling real-time monitoring of venous pressure, temperature, and fluid flow. These sensor-enhanced devices support clinicians with immediate feedback, improving placement accuracy and reducing misplacement complications that occur in a meaningful subset of procedures.

Ultrasound-guided insertion support systems and enhanced imaging compatibility further augment procedural precision. For instance, new vascular access ultrasound platforms with integrated needle tracking and tip confirmation systems improve clinician efficiency and accuracy during catheter placement, reducing complication rates and procedural time.

Miniaturization and AI-assisted placement tools are also emerging, with a notable portion of healthcare facilities piloting algorithms that support decision-making during catheter insertion. Telemetry integration and device interoperability with electronic health records are additional trends enhancing workflow efficiency. Collectively, these technological advances extend beyond core catheter hardware to include ancillary systems, procedural support tools, and data-guided clinical insights, marking a transition toward smarter, safer, and more integrated vascular access solutions.

In January 2025, Teleflex Incorporated was awarded a contract from Vizient, Inc. for the supply of its central venous access catheters, including the Arrow™ portfolio, expanding access to Teleflex products across more than 65% of U.S. acute care providers and academic medical centers. Source: www.teleflex.com

In December 2024, Teleflex Incorporated expanded its Pressure Injectable Arrowg+ard Blue Plus™ CVC portfolio across Europe, Middle East, and Africa, introducing a new maximal sterile barrier procedure kit designed to support clinicians with all components needed for central catheter placement and help reduce central line-associated bloodstream infections. Source: www.teleflex.com

In 2024, BD launched the SiteRite 9 advanced ultrasound system to support central venous catheter placement with enhanced needle tracking and tip confirmation features aimed at improving clinician efficiency.

In 2023–2024, Cook Medical’s Spectrum Turbo-Jet catheter for high-flow hemodialysis was adopted in 280,000+ placements across nephrology centers, offering significantly higher blood flow rates and procedural efficiency.

The scope of the Central Venous Catheters Market Report covers a comprehensive examination of product types, clinical applications, technological evolution, and geographic consumption patterns critical for healthcare professionals and strategic planners in the medical device sector. It includes in-depth coverage of product variations, such as non-tunneled catheters, tunneled catheters, peripherally inserted central catheters (PICCs), and specialized high-flow or antimicrobial-coated designs that address diverse clinical needs from intensive care to chronic therapy. Segment insights detail how each type contributes to treatment protocols across acute and long-term patient care.

Geographically, the scope spans major markets including North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, analyzing regional penetration, infrastructure readiness, and usage patterns. North America is prominent in advanced catheter deployment and procedural innovation, while emerging markets in Asia-Pacific and Latin America show rising demand driven by expanding healthcare access and clinical capacity.

The report also integrates application-based focus areas, categorizing usage across hospitals, ambulatory surgical centers, oncology clinics, and dialysis facilities. It examines technological trends such as smart catheter sensors, advanced imaging support systems, and digital procedural guidance tools that increasingly shape clinician choices. Policy and regulatory landscapes, including infection control standards and device approval frameworks, are assessed to help decision-makers align product development and market entry strategies. Emerging niche segments—like pediatric and minimally invasive catheter designs—are highlighted for their clinical relevance and growth potential. The report concludes with competitive benchmarking, profiling leading vendors and innovation pipelines essential for vendors, investors, and healthcare executives navigating the complex, evolving CVC market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 263.0 Million |

| Market Revenue (2032) | USD 445.2 Million |

| CAGR (2025–2032) | 6.80% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Teleflex Incorporated, B. Braun Melsungen AG, Medtronic plc, Becton, Dickinson and Company (BD), Cook Medical, AngioDynamics, Vygon Ltd., Smiths Medical, Kimal Healthcare, Comed B.V. |

| Customization & Pricing | Available on Request (10% Customization Free) |