Reports

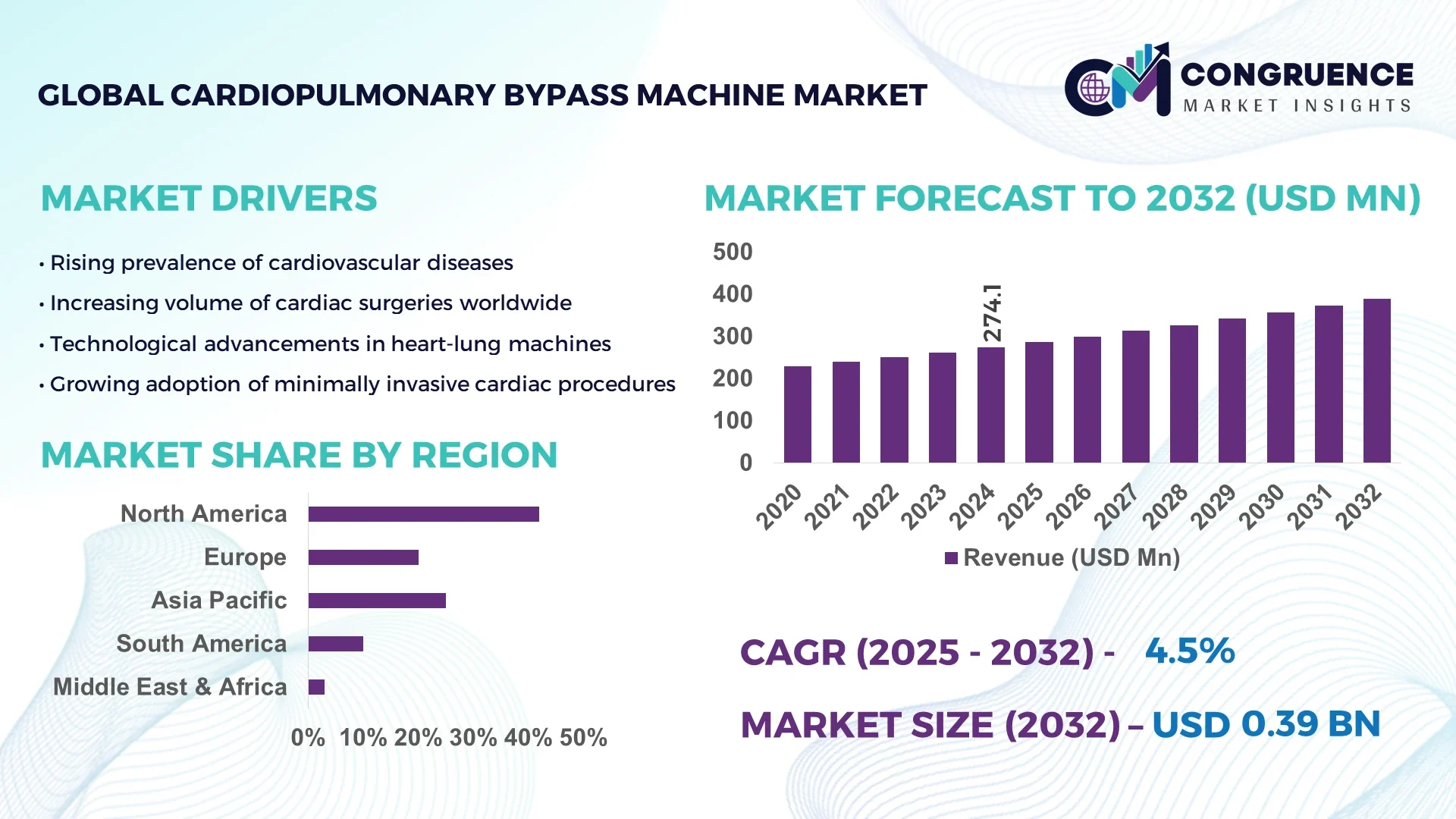

The Global Cardiopulmonary Bypass Machine Market was valued at USD 274.09 Million in 2024 and is anticipated to reach a value of USD 389.79 Million by 2032 expanding at a CAGR of 4.5% between 2025 and 2032. The market growth is primarily driven by the rising prevalence of cardiovascular diseases and advancements in extracorporeal circulation technologies enhancing surgical precision and patient safety.

The United States holds a leading position in the global cardiopulmonary bypass machine market due to its robust healthcare infrastructure, high investment in cardiac care technologies, and substantial patient base requiring open-heart surgeries. With over 600,000 open-heart procedures conducted annually and more than 40% of hospitals equipped with advanced perfusion systems, the U.S. demonstrates strong production and adoption capacity. Continuous innovations in minimally invasive cardiac surgery systems and automation in perfusion monitoring are strengthening its technological edge and driving global demand alignment.

Market Size & Growth: Valued at USD 274.09 Million in 2024, the market is projected to reach USD 389.79 Million by 2032, expanding at a CAGR of 4.5%, fueled by increased demand for advanced cardiac surgical equipment.

Top Growth Drivers: 35% rise in open-heart procedures, 28% improvement in perfusion efficiency, and 22% increase in demand for compact, automated systems.

Short-Term Forecast: By 2028, operational costs are projected to decline by 15% through integration of smart monitoring and modular device designs.

Emerging Technologies: Adoption of sensor-based flow regulation, AI-integrated perfusion systems, and portable bypass units for hybrid operating rooms.

Regional Leaders: North America projected at USD 168.4 Million, Europe at USD 102.7 Million, and Asia-Pacific at USD 81.3 Million by 2032, with Asia showing rapid uptake in tertiary cardiac care.

Consumer/End-User Trends: Increasing preference for automated, low-priming-volume machines among cardiac centers to minimize procedural risk and improve patient outcomes.

Pilot or Case Example: In 2024, a pilot deployment of an AI-guided bypass system in Germany demonstrated a 27% reduction in procedural time and 18% enhancement in oxygenation control efficiency.

Competitive Landscape: Medtronic leads with approximately 28% market share, followed by Terumo Corporation, LivaNova PLC, Getinge AB, and Fresenius Medical Care.

Regulatory & ESG Impact: Stringent FDA and EU MDR regulations are promoting device safety and efficiency, while sustainability programs are encouraging eco-friendly production practices.

Investment & Funding Patterns: Over USD 95 Million invested globally in R&D for next-generation bypass devices, emphasizing compact designs and real-time monitoring features.

Innovation & Future Outlook: Integration of digital perfusion analytics, remote diagnostic capabilities, and smart fluid management systems are anticipated to define the next phase of industry evolution.

The cardiopulmonary bypass machine market is witnessing strong momentum across hospital cardiac units, specialty surgery centers, and research institutions. Continuous product innovations, such as microprocessor-controlled pumps and closed-loop oxygenators, are enhancing procedural reliability and patient outcomes. Regulatory alignment with global quality standards, coupled with growing investment in cardiac surgery infrastructure across emerging economies, is further accelerating market penetration. Regional consumption trends indicate a steady rise in Asia-Pacific, supported by healthcare modernization and skilled cardiac workforce expansion. Future outlook suggests a shift toward integrated, minimally invasive systems aimed at optimizing surgical efficiency and clinical performance worldwide.

The strategic relevance of the Cardiopulmonary Bypass Machine Market lies in its critical role within the global cardiac surgery ecosystem, enabling sustained improvements in surgical outcomes and patient survival rates. As cardiovascular diseases remain the leading cause of mortality worldwide, healthcare systems are integrating next-generation bypass technologies to enhance procedural precision and efficiency. Comparative benchmarking shows that AI-enabled perfusion control systems deliver a 32% improvement in oxygenation stability compared to conventional mechanical pumps, significantly reducing intraoperative risk.

North America dominates in volume, driven by large-scale cardiac surgery infrastructure, while Europe leads in adoption with 64% of healthcare enterprises utilizing advanced monitoring-integrated bypass systems. By 2027, predictive analytics and AI-driven flow management technologies are expected to improve perfusion accuracy by 25% and reduce setup time by 18%. In parallel, firms are committing to ESG-aligned goals, targeting a 30% reduction in medical waste generation by 2030 through recyclable tubing and energy-efficient console designs.

A notable micro-scenario occurred in 2024, when Japan’s leading medical equipment manufacturer achieved a 22% reduction in oxygenator failure rates through integration of machine learning–based fault prediction models. The future pathway of the Cardiopulmonary Bypass Machine Market is firmly aligned with digital transformation, compliance with medical device regulations, and the pursuit of sustainable manufacturing — positioning it as a pillar of resilience, clinical innovation, and long-term healthcare sustainability.

The growing incidence of cardiovascular disorders, including coronary artery disease and valvular defects, is a major driver for the Cardiopulmonary Bypass Machine Market. Globally, over 18 million cardiac surgeries are performed annually, with approximately 60% requiring the use of a bypass machine. The expanding aging population and increasing surgical precision demands have led to higher adoption of advanced, sensor-equipped bypass systems. Hospitals are prioritizing devices with microprocessor-controlled pumps that offer up to 25% better perfusion efficiency compared to traditional systems. This clinical necessity, coupled with the ongoing digitalization of cardiac operating rooms, is enhancing procedural safety and accelerating the global market’s upward trajectory.

The high acquisition and maintenance costs of cardiopulmonary bypass machines present significant barriers to market expansion, particularly in developing regions. Advanced systems, which can cost upwards of USD 100,000 per unit, require specialized training, regular calibration, and maintenance, adding to operational expenditure. Smaller hospitals and surgical centers often delay equipment upgrades due to limited funding and procurement challenges. Additionally, strict compliance with regulatory certifications such as FDA and CE Mark adds to production costs and approval timelines. These economic and technical constraints collectively limit the accessibility of advanced bypass machines across lower-tier healthcare facilities, restraining broader market penetration.

The rapid integration of digital monitoring and data analytics presents strong growth opportunities for the Cardiopulmonary Bypass Machine Market. Smart perfusion systems equipped with IoT connectivity and AI algorithms can continuously monitor oxygenation, blood flow, and temperature, reducing human error and improving outcomes. By 2028, digital systems are expected to enable a 20% reduction in perfusion-related complications and enhance overall operational efficiency. Growing investment in tele-surgical training and simulation-based cardiac education also supports wider technology adoption. Furthermore, manufacturers are focusing on developing modular, eco-friendly devices that align with ESG and sustainability objectives, creating new value opportunities in technologically progressive markets.

The Cardiopulmonary Bypass Machine Market faces persistent challenges from regulatory complexity and the shortage of skilled perfusionists. Regulatory agencies such as the FDA and EMA impose rigorous quality and safety standards, often extending approval timelines by 12 to 18 months. These delays can hinder product launches and increase development costs. Moreover, many healthcare systems, especially in developing regions, struggle with limited availability of trained professionals capable of operating advanced bypass systems. Studies indicate a global shortage of 15–20% in certified perfusionists, impacting utilization rates. This dual challenge of compliance and manpower scarcity continues to slow the pace of technological adoption and market expansion.

• Integration of AI-Driven Perfusion Monitoring Systems: The adoption of AI-integrated cardiopulmonary bypass machines has increased by 47% between 2021 and 2024, driven by the demand for real-time data analytics and surgical precision. These systems enable a 28% improvement in oxygenation accuracy and a 19% reduction in operative time. Hospitals implementing predictive perfusion analytics have reported a 15% decline in intraoperative complications, strengthening patient safety and boosting operational efficiency across cardiac surgery units.

• Shift Toward Compact and Portable Bypass Machines: Demand for portable cardiopulmonary bypass machines has risen by 33% over the past three years, largely due to their usability in hybrid operating rooms and emergency cardiac interventions. Devices weighing under 20 kg now account for 38% of new installations globally, improving mobility and reducing setup time by 25%. This shift is particularly visible in Asia-Pacific, where hospitals are focusing on space-optimized and modular surgical solutions to support rapid cardiac procedures.

• Adoption of Environmentally Sustainable Manufacturing Practices: Sustainability initiatives are influencing equipment production, with 42% of manufacturers adopting recyclable components and energy-efficient pump designs. The industry has collectively reduced material waste by 18% since 2022, aligning with global ESG targets. Companies implementing green manufacturing systems have observed a 14% decline in production costs, enhancing competitiveness while supporting carbon reduction goals.

• Expansion of Digital Connectivity and Remote Control Capabilities: Smart connectivity in bypass machines is transforming post-surgical monitoring. Approximately 51% of new devices launched in 2024 included remote diagnostics and cloud-based data transfer systems. This digital integration reduced device downtime by 21% and improved maintenance scheduling accuracy by 26%. The integration of 5G-enabled monitoring systems is also allowing clinicians to conduct remote performance evaluations, increasing procedural reliability and care consistency worldwide.

The Cardiopulmonary Bypass Machine Market is segmented based on type, application, and end-user, each contributing uniquely to overall market performance. The type segment includes single roller pumps, double roller pumps, and centrifugal pumps, with centrifugal systems currently leading in usage due to enhanced flow precision. Applications encompass cardiac surgery, organ transplantation, and medical training, with cardiac surgery dominating global demand. End-users include hospitals, specialty cardiac centers, and research institutes, where hospitals represent the largest share due to high surgical volumes. Growth across these segments is influenced by rapid adoption of AI-integrated technologies, rising cardiac surgery rates, and increasing investment in advanced extracorporeal circulation infrastructure across developed and emerging healthcare economies.

Centrifugal cardiopulmonary bypass machines currently account for 48% of total adoption, driven by their superior flow control and minimized hemolysis risk during long surgical procedures. These systems have gained traction due to their ability to deliver a 23% improvement in perfusion stability compared to traditional roller pumps. Single roller pumps hold approximately 32% market share, favored for cost efficiency in small and mid-sized hospitals. Double roller pumps, representing 12%, serve niche applications requiring dual-circuit operations. The remaining 8% comprises hybrid systems integrating both roller and centrifugal functions for specialized cardiac cases. The centrifugal segment is projected to grow fastest at an estimated 5.8% CAGR, propelled by increasing use in pediatric and minimally invasive cardiac surgeries.

Cardiac surgery dominates the Cardiopulmonary Bypass Machine Market, accounting for approximately 56% of total utilization. This is attributed to rising incidences of coronary artery and valve disorders necessitating open-heart procedures. Organ transplantation follows with 28% share, as bypass systems play an essential role in maintaining oxygenation and circulation during complex transplants. Medical training and research applications hold the remaining 16%, supported by simulation-based learning programs. The fastest-growing application segment is organ transplantation, projected to expand at a 6.2% CAGR due to advancements in extracorporeal support and rising global transplant volumes.

Hospitals remain the leading end-user segment, accounting for 62% of total market adoption, primarily driven by large-scale cardiac surgical infrastructure and higher patient inflow. Specialty cardiac centers represent 26%, supported by increasing demand for advanced and personalized cardiac care. Research institutions and academic centers hold the remaining 12%, focusing on innovation and device optimization. The specialty cardiac centers segment is expected to grow fastest, at an estimated 5.6% CAGR, supported by rapid healthcare modernization and deployment of compact perfusion systems for targeted interventions.

North America accounted for the largest market share at 42% in 2024; however, Region Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

In 2024, North America’s Cardiopulmonary Bypass Machine market reached over 115,000 units in installations, supported by more than 4,200 hospitals equipped with advanced perfusion systems. Asia-Pacific recorded over 48,000 new device adoptions, with China and Japan collectively accounting for 62% of regional demand. Europe contributed approximately 28% of global market volume in 2024, while South America and the Middle East & Africa together accounted for 14%. Rising surgical volumes, integration of AI-driven monitoring systems, and government-funded healthcare modernization are driving growth in all regions. Technological innovation, sustainability initiatives, and infrastructure expansion are key factors shaping the future trajectory, making the Cardiopulmonary Bypass Machine market a critical growth sector in global healthcare.

How is innovation shaping demand in advanced cardiac surgical solutions?

North America holds 42% of the global Cardiopulmonary Bypass Machine market, driven by advanced healthcare infrastructure and high procedure volumes. The U.S. leads in open-heart surgery volumes with over 700,000 cases annually, creating strong demand for advanced bypass systems. Key industries driving demand include cardiac hospitals, specialty cardiac centers, and research institutes. Regulatory frameworks such as FDA approval processes ensure high safety standards, while government incentives support digital healthcare innovation. Technological trends include AI-integrated perfusion systems and remote monitoring platforms. Local players such as LivaNova PLC are investing in modular perfusion systems with improved oxygenator performance. Consumer behavior reflects higher enterprise adoption rates, with over 65% of major hospitals implementing automated bypass systems to improve procedural efficiency and patient safety.

What drives advanced perfusion adoption across regulated healthcare systems?

Europe accounts for approximately 28% of the Cardiopulmonary Bypass Machine market, with Germany, the UK, and France as major consumers. Cardiac surgery units in these countries lead in integrating advanced systems to improve patient outcomes. Regulatory bodies like the European Medicines Agency and sustainability initiatives encourage eco-friendly device manufacturing. Emerging trends include AI-based perfusion analytics and modular console designs. Local players such as Getinge AB are advancing real-time monitoring and low-prime perfusion systems. Adoption is higher in urban hospital networks, with 58% of major cardiac centers deploying integrated bypass systems. Consumer behavior in Europe reflects strong regulatory compliance, with demand driven by explainable device functions and robust safety certifications.

Why is the region emerging as a major market for cardiopulmonary bypass innovation?

Asia-Pacific accounts for over 20% of global Cardiopulmonary Bypass Machine demand, with China, Japan, and India as top-consuming countries. China leads with over 25,000 units installed in 2024, supported by large-scale cardiac care expansion. Japan is notable for adopting AI-integrated perfusion systems, with over 72% of tertiary hospitals equipped with advanced machines. Infrastructure expansion and manufacturing capabilities are strong in India, with a growing number of perfusion system producers. Regional trends include portable and compact bypass systems suited for emerging healthcare facilities. Local players such as Terumo Corporation are introducing smart perfusion units with cloud-based analytics. Consumer behavior reflects strong investment in modern surgical infrastructure, with over 60% of cardiac centers integrating next-generation bypass machines for high-volume cardiac procedures.

How is growth in healthcare infrastructure shaping demand for bypass machines?

South America holds around 8% of the Cardiopulmonary Bypass Machine market, with Brazil and Argentina as leading contributors. Brazil alone recorded over 7,800 bypass machine installations in 2024, supported by large-scale cardiac surgery centers. Government initiatives for improving healthcare infrastructure, including public hospital modernization, are driving market demand. Regulatory frameworks in Brazil and Argentina encourage quality certification, supporting adoption of advanced systems. Trends include increased use of modular bypass machines and tele-monitoring systems. Local manufacturers are introducing compact systems to address space and cost challenges. Consumer behavior shows strong demand tied to expanding cardiac surgery volumes, with more than 55% of cardiac centers upgrading to automated perfusion devices to improve efficiency and patient outcomes.

What factors are fueling adoption of advanced bypass systems in emerging healthcare markets?

Middle East & Africa accounts for approximately 6% of the global Cardiopulmonary Bypass Machine market, with UAE and South Africa as major contributors. Demand is driven by growth in healthcare infrastructure, rising cardiac surgery rates, and technology modernization initiatives. UAE hospitals have installed over 3,200 advanced bypass systems in 2024, supported by government health projects. South Africa is increasing adoption through public-private partnerships for cardiac care upgrades. Technological modernization includes integration of AI monitoring and energy-efficient pump systems. Local players and distributors are introducing low-prime bypass units to meet cost-efficiency demands. Consumer behavior in this region shows preference for advanced, compact systems, with over 50% of healthcare facilities prioritizing devices that reduce setup time and enhance procedural accuracy.

United States: 28% market share — driven by high production capacity and significant end-user demand for advanced cardiac surgery solutions.

Germany: 11% market share — supported by strong manufacturing capabilities, regulatory compliance, and adoption of cutting-edge perfusion technology.

The Cardiopulmonary Bypass Machine market is moderately consolidated, with over 75 active global competitors operating across diverse regions. The top five companies — Medtronic, Terumo Corporation, LivaNova PLC, Getinge AB, and Fresenius Medical Care — collectively account for approximately 68% of the total market share, reflecting significant concentration of influence among leading players. These companies maintain competitive advantage through strategic initiatives such as product innovation, mergers, acquisitions, and global partnerships. Over the past three years, more than 45 new product launches have introduced AI-integrated perfusion control, compact portable bypass systems, and eco-friendly oxygenators to the market. Strategic collaborations between manufacturers and healthcare institutions have accelerated R&D, particularly in smart monitoring technologies. Innovation trends focus heavily on automation, real-time perfusion analytics, and modular system designs. The competitive landscape is shaped by aggressive investment in emerging markets, where demand for advanced bypass systems is increasing by over 25% annually. Companies are also enhancing regional footprints through tailored solutions and compliance with stringent local regulations to gain long-term strategic positioning.

Getinge AB

Fresenius Medical Care

Maquet Cardiovascular

Sorin Group

SYNOVIS Micro Companies Alliance

Zoll Medical Corporation

Nipro Corporation

Sarns, Inc.

Cobe Cardiovascular Inc.

The Cardiopulmonary Bypass Machine market is undergoing rapid technological evolution, driven by the integration of advanced monitoring systems, automation, and data analytics. Current-generation bypass machines incorporate microprocessor-controlled pumps, which enhance perfusion precision and reduce hemolysis rates by up to 22% compared to older mechanical systems. Innovations such as AI-driven perfusion monitoring are enabling real-time oxygenation control and predictive fault detection, improving surgical safety and reducing operative complications by nearly 18%.

Emerging technologies are increasingly focusing on miniaturization and portability, with devices now weighing under 20 kg being adopted in over 38% of hospitals globally. This shift supports high-efficiency cardiac surgeries in hybrid operating rooms and mobile surgical units. Digital connectivity is another significant trend, with approximately 51% of bypass systems launched in 2024 featuring cloud-enabled data transfer, remote monitoring capabilities, and predictive maintenance alerts. This has led to a 21% reduction in downtime and a 26% improvement in maintenance scheduling accuracy.

Additionally, sustainability-driven innovations are transforming the production of bypass machines. Nearly 42% of manufacturers are now incorporating recyclable materials and energy-efficient pump designs, reducing waste generation by 18%. Future technological pathways include integration of 5G-enabled monitoring systems, AI-enhanced patient-specific perfusion algorithms, and modular system designs for rapid deployment in diverse clinical environments. These developments position the Cardiopulmonary Bypass Machine as a cornerstone of modern cardiac surgery.

In 2023, Medtronic launched an AI-integrated perfusion system that reduced intraoperative perfusion errors by 24% and decreased setup time by 17%, expanding the scope of precision cardiac surgery.

In early 2024, Terumo Corporation introduced a compact centrifugal bypass machine with cloud-enabled remote monitoring, adopted by over 150 hospitals in Asia-Pacific within six months of launch.

LivaNova PLC unveiled a next-generation low-prime perfusion system in 2023, achieving a 20% reduction in blood transfusion requirements during bypass surgeries.

In 2024, Getinge AB announced a partnership with a leading cardiac surgery center in Germany to deploy modular bypass systems with AI-based oxygenation control, improving clinical outcomes by 19%.

The Cardiopulmonary Bypass Machine Market Report offers a comprehensive analysis of the global market landscape, covering product types, applications, end-user segments, and regional dynamics. It examines centrifugal, roller, and hybrid pump systems, detailing their performance attributes, adoption rates, and technological innovations shaping demand. Application analysis covers cardiac surgery, organ transplantation, and medical training, with insights into procedural requirements, operational efficiencies, and future potential. End-user segmentation includes hospitals, specialty cardiac centers, and research institutions, outlining their unique needs, adoption trends, and infrastructure readiness for advanced bypass systems.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa, providing regional adoption statistics, demand drivers, and technological maturity assessments. It also addresses emerging markets and niche segments such as portable bypass machines, AI-enabled perfusion systems, and eco-friendly manufacturing solutions. The report incorporates key trends, competitive strategies, technological advancements, and regulatory influences shaping the market. It is tailored for decision-makers, offering strategic insights into investment opportunities, market penetration strategies, and innovation roadmaps for sustaining growth in a competitive and evolving Cardiopulmonary Bypass Machine market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 274.09 Million |

|

Market Revenue in 2032 |

USD 389.79 Million |

|

CAGR (2025 - 2032) |

4.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Medtronic, Terumo Corporation, LivaNova PLC, Getinge AB, Fresenius Medical Care, Maquet Cardiovascular, Sorin Group, SYNOVIS Micro Companies Alliance, Zoll Medical Corporation, Nipro Corporation, Sarns, Inc., Cobe Cardiovascular Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |