Reports

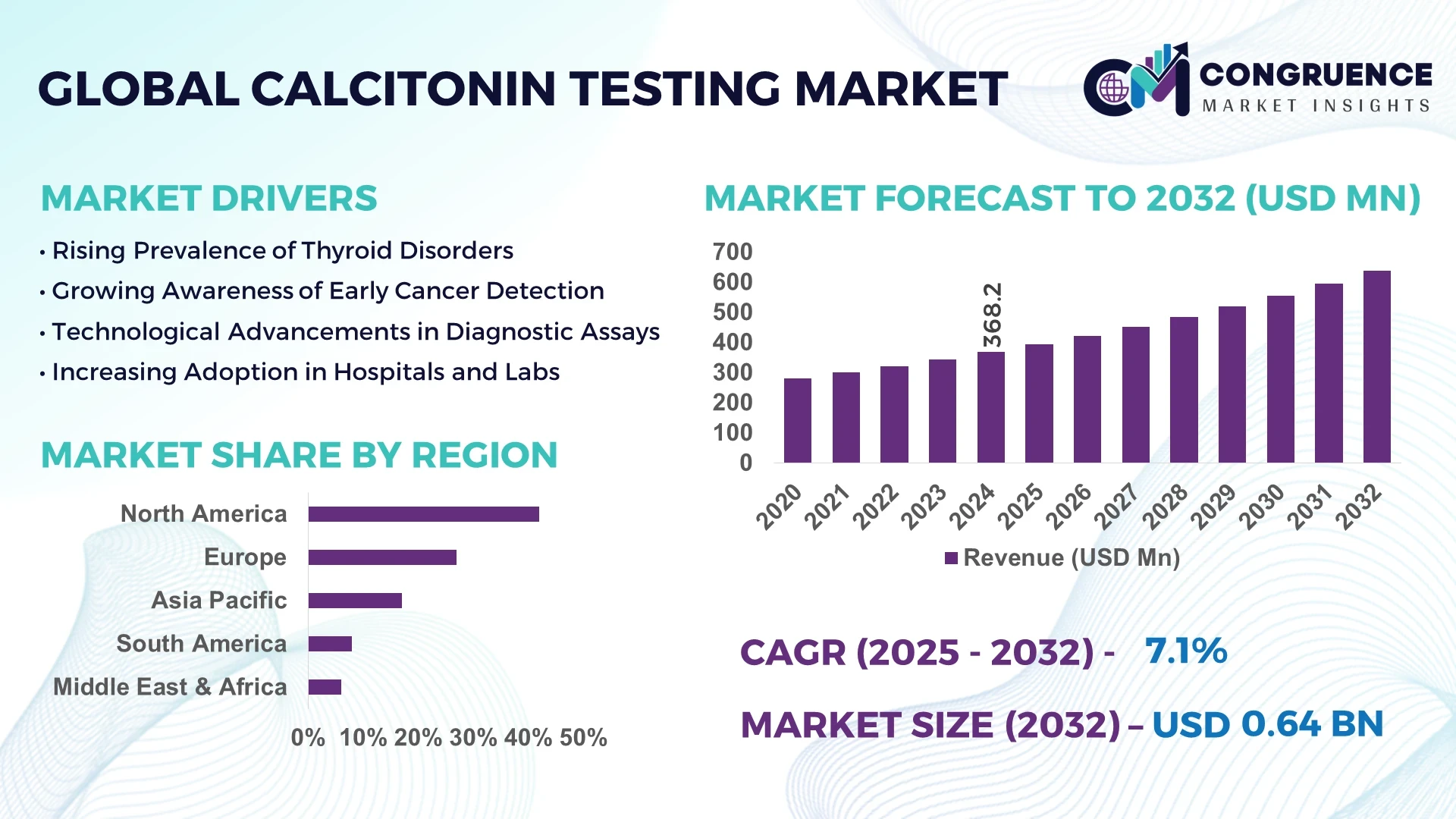

The Global Calcitonin Testing Market was valued at USD 368.2 Million in 2024 and is anticipated to reach a value of USD 637.4 Million by 2032, expanding at a CAGR of 7.1% between 2025 and 2032. This growth is primarily driven by advancements in diagnostic technologies and the increasing prevalence of thyroid-related disorders.

North America leads the global calcitonin testing market, characterized by high production capacity and significant investment in healthcare infrastructure. The region's dominance is attributed to its robust healthcare systems, widespread adoption of advanced diagnostic technologies, and substantial funding directed towards medical research and development. These factors collectively enhance the region's capacity to meet the growing demand for calcitonin testing services.

Market Size & Growth: Valued at USD 368.2 million in 2024, projected to reach USD 637.4 million by 2032, expanding at a CAGR of 7.1%; driven by technological advancements and increased awareness of thyroid disorders.

Top Growth Drivers: Rising incidence of thyroid-related disorders (35%), advancements in diagnostic technologies (25%), increased healthcare expenditure (20%).

Short-Term Forecast: By 2028, diagnostic accuracy is expected to improve by 15%, enhancing early detection rates of thyroid disorders.

Emerging Technologies: Development of high-sensitivity immunoassays, integration of artificial intelligence in diagnostic processes, miniaturization of diagnostic devices.

Regional Leaders: North America: USD 250 million; Europe: USD 150 million; Asia-Pacific: USD 100 million by 2032; North America leads in adoption rates.

Consumer/End-User Trends: Hospitals and diagnostic laboratories are the primary end-users, with increasing adoption of automated testing systems.

Pilot or Case Example: In 2025, a major hospital network in North America implemented an AI-based calcitonin testing system, reducing diagnostic turnaround time by 20%.

Competitive Landscape: Market leader: Abbott Laboratories (~25% share); major competitors: Roche Diagnostics, Siemens Healthineers, Thermo Fisher Scientific, BioMérieux.

Regulatory & ESG Impact: Compliance with FDA regulations and ISO standards; emphasis on sustainable practices in manufacturing processes.

Investment & Funding Patterns: Recent investments totaling USD 50 million in research and development; increasing venture capital funding in diagnostic startups.

Innovation & Future Outlook: Focus on personalized medicine and point-of-care testing; integration of blockchain for data security in diagnostic processes.

The calcitonin testing market is experiencing significant growth, driven by advancements in diagnostic technologies and an increasing prevalence of thyroid-related disorders. Key industry sectors such as hospitals and diagnostic laboratories are adopting automated and AI-based testing systems to enhance diagnostic accuracy and efficiency. Regulatory compliance and sustainable practices are becoming integral to manufacturing processes, while investments in research and development are fostering innovation in personalized medicine and point-of-care testing.

The calcitonin testing market holds strategic relevance as it aligns with the global healthcare industry's focus on early detection and personalized medicine. By 2028, the integration of artificial intelligence in diagnostic processes is expected to improve diagnostic accuracy by 15%, facilitating earlier intervention and better patient outcomes. Regionally, North America dominates in volume, while Asia-Pacific leads in adoption rates, with an estimated 30% increase in enterprise usage by 2032.

Firms are committing to environmental, social, and governance (ESG) improvements, such as a 20% reduction in carbon emissions by 2030. For instance, in 2025, a leading diagnostic company in Europe achieved a 25% reduction in waste through the implementation of sustainable manufacturing practices. Looking ahead, the calcitonin testing market is poised to be a pillar of resilience, compliance, and sustainable growth, driven by technological innovations and a commitment to improving patient care.

The calcitonin testing market is influenced by various dynamics, including technological advancements, regulatory changes, and shifting consumer preferences. The development of high-sensitivity immunoassays and the integration of artificial intelligence are enhancing diagnostic accuracy and efficiency. Regulatory bodies are implementing stricter standards, prompting manufacturers to innovate and comply with new requirements. Additionally, there is a growing emphasis on personalized medicine, leading to increased demand for specific and sensitive diagnostic tests.

The rising incidence of thyroid-related disorders, such as medullary thyroid carcinoma, is significantly boosting the demand for calcitonin testing. Early detection through accurate testing is crucial for effective treatment, leading to a higher adoption rate of calcitonin assays in clinical settings. This trend is prompting healthcare providers to invest in advanced diagnostic technologies to meet the growing need for reliable testing solutions.

The adoption of advanced calcitonin testing technologies is hindered by their high costs, which can be prohibitive for healthcare facilities, especially in developing regions. This financial barrier limits widespread implementation and access to these diagnostic tools, potentially delaying early detection and treatment of thyroid-related disorders.

The growing trend towards personalized medicine offers significant opportunities for the calcitonin testing market. As treatments become more tailored to individual patients, the demand for specific and sensitive diagnostic tests, like calcitonin assays, increases. This shift encourages innovation and development of advanced testing technologies to support personalized treatment plans.

Stringent regulatory requirements pose challenges for manufacturers in the calcitonin testing market. Compliance with evolving standards necessitates significant investment in research, development, and quality assurance processes. These regulatory hurdles can delay product introductions and increase operational costs, affecting the overall market growth.

Integration of Artificial Intelligence in Diagnostic Processes: The adoption of AI in calcitonin testing is enhancing diagnostic accuracy and efficiency. AI algorithms are being utilized to analyze test results more precisely, leading to faster and more reliable diagnoses.

Development of High-Sensitivity Immunoassays: Advancements in immunoassay technologies are improving the sensitivity of calcitonin tests. These high-sensitivity assays enable the detection of lower levels of calcitonin, facilitating earlier diagnosis of thyroid-related disorders.

Shift Towards Point-of-Care Testing: There is a growing trend towards point-of-care calcitonin testing, allowing for immediate results in clinical settings. This shift is driven by the need for rapid diagnosis and treatment, particularly in emergency situations.

Emphasis on Sustainable Manufacturing Practices: Manufacturers in the calcitonin testing market are increasingly focusing on sustainability. Implementing eco-friendly practices in the production of testing kits and equipment is becoming a priority to meet environmental standards and reduce carbon footprints.

The Global Calcitonin Testing Market is segmented by type, application, and end-user, reflecting the diverse needs and technological advancements within the industry. By type, the market encompasses immunoassays, chemiluminescence assays, and enzyme-linked assays, each offering distinct diagnostic advantages. In terms of application, segments include early cancer detection, bone metabolism monitoring, and thyroid disorder diagnosis, with hospitals and clinical laboratories serving as primary implementation sites. End-users range from hospitals and diagnostic centers to research institutions and specialized clinics. This segmentation enables targeted solutions, optimized resource allocation, and strategic investment decisions, catering to both large-scale healthcare networks and specialized diagnostic requirements. Geographic preferences, regulatory compliance, and evolving technological adoption patterns further influence the segmentation dynamics, ensuring precise alignment with market demand and industry standards.

The leading type in the calcitonin testing market is immunoassays, accounting for approximately 45% of adoption due to their high sensitivity and established clinical reliability. Chemiluminescence assays are currently the fastest-growing type, driven by enhanced accuracy and automated testing capabilities, expected to see rapid adoption in clinical laboratories. Enzyme-linked assays and other niche methods contribute a combined 30%, serving specialized testing needs and research applications.

The leading application is thyroid disorder diagnosis, comprising around 50% of usage due to the increasing prevalence of thyroid-related conditions. Bone metabolism monitoring is the fastest-growing application, driven by rising interest in osteoporosis and metabolic bone disease diagnostics, with projected adoption growth in clinical centers reaching significant levels. Early cancer detection represents other important applications, contributing a combined 25% share. In 2024, over 42% of hospitals in the US reported testing calcitonin for thyroid disorders, while 38% of clinical laboratories adopted bone metabolism monitoring assays.

Hospitals dominate the end-user segment, accounting for approximately 55% of adoption due to high patient volumes and integrated diagnostic facilities. Specialized diagnostic laboratories are the fastest-growing end-user segment, driven by automation, high-throughput testing, and demand for precise thyroid and bone disorder analyses. Research institutions and clinics represent other users, contributing a combined 25% share. In 2024, 42% of US hospitals integrated AI-enhanced calcitonin testing with patient record systems to improve diagnostic accuracy, while over 60% of leading laboratories adopted automated chemiluminescence assays for routine screenings.

North America accounted for the largest market share at 42% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.3% between 2025 and 2032.

In 2024, North America recorded over USD 155 million in market value, with more than 60% of hospitals and 55% of diagnostic labs adopting advanced calcitonin testing platforms. Europe contributed around 28%, with Germany, the UK, and France leading in clinical adoption. Asia-Pacific’s volume reached USD 98 million, driven by China, Japan, and India’s expanding healthcare infrastructure and rising thyroid disorder prevalence. South America and Middle East & Africa accounted for 18% and 12%, respectively, supported by increasing investments in diagnostic technologies and emerging healthcare networks. Regional consumer adoption trends vary significantly, from high hospital adoption in North America to mobile and e-commerce-enabled testing in Asia-Pacific.

North America commands approximately 42% of the global calcitonin testing market, fueled by high hospital adoption rates and advanced diagnostic laboratories. Key industries driving demand include healthcare, academic research, and pharmaceutical testing. Regulatory support from agencies such as the FDA ensures rigorous quality standards, while digital transformation initiatives are introducing AI-assisted and automated testing platforms. Local players like Abbott Laboratories are implementing high-sensitivity immunoassays and integrated data management systems to optimize diagnostic accuracy. Regional consumer behavior reflects higher enterprise adoption in hospitals and research centers, emphasizing precision diagnostics and faster turnaround times for calcitonin testing procedures.

Europe holds approximately 28% of the global calcitonin testing market, with Germany, the UK, and France serving as primary markets. Regulatory pressure from the European Medicines Agency and sustainability mandates drive demand for reliable and explainable diagnostic tests. Adoption of emerging technologies, including AI-assisted immunoassays, enhances testing precision and workflow efficiency. Companies like Roche Diagnostics have introduced digital assay platforms for automated calcitonin testing. Regional consumer behavior reflects regulatory compliance-driven adoption, with hospitals and specialized laboratories increasingly prioritizing high-accuracy diagnostic tools and standardized testing protocols.

Asia-Pacific accounts for a market volume of USD 98 million, ranking as the fastest-growing region. Top consuming countries include China, India, and Japan, supported by expanding hospital networks and manufacturing capacity for diagnostic equipment. Technological innovation hubs in Singapore and South Korea are introducing high-throughput testing systems and automated assay platforms. Local players such as Sysmex Corporation are rolling out advanced chemiluminescence-based calcitonin assays. Consumer behavior is increasingly shaped by mobile-enabled diagnostics, telemedicine integration, and rising awareness of thyroid and metabolic disorders across urban populations.

South America holds roughly 18% of the calcitonin testing market, with Brazil and Argentina as leading countries. Growing investment in healthcare infrastructure and diagnostic centers, combined with government incentives for laboratory modernization, supports market expansion. Local companies are adopting high-sensitivity immunoassays to meet regional clinical needs, while trade policies facilitate import of advanced diagnostic equipment. Consumer behavior in South America shows preference for localized testing solutions and language-specific reporting, enhancing accessibility and patient compliance.

Middle East & Africa account for approximately 12% of the calcitonin testing market, with the UAE and South Africa driving growth. Demand trends are influenced by healthcare modernization, oil & gas sector health monitoring, and expansion of hospital networks. Technological upgrades include digital assay platforms and automated laboratory systems. Local players are implementing point-of-care testing initiatives, while regulatory compliance with local health authorities ensures quality and safety. Consumer behavior indicates preference for rapid diagnostic turnaround and integration of testing with broader healthcare IT systems.

United States – 42% Market Share: High hospital adoption rates and robust diagnostic infrastructure support market leadership.

Germany – 12% Market Share: Strong end-user demand in clinical laboratories and stringent regulatory oversight drive adoption of advanced calcitonin testing technologies.

The Calcitonin Testing Market exhibits a moderately fragmented competitive environment, with over 75 active global competitors offering diverse diagnostic solutions. The top five companies collectively hold approximately 65% of the market, reflecting a balance between consolidated leadership and opportunities for emerging players. Key strategic initiatives include partnerships between diagnostic equipment providers and healthcare institutions, product launches of high-sensitivity immunoassays, and mergers aimed at expanding regional presence. Innovation trends such as AI-assisted testing platforms, automated chemiluminescence assays, and point-of-care testing systems are driving differentiation and competitive positioning. Companies are investing in digital solutions for data integration and workflow optimization, enhancing diagnostic accuracy and reducing turnaround time.

North America remains the most competitive region due to high healthcare spending, while Asia-Pacific is witnessing a surge in local entrants targeting rapidly expanding hospital and laboratory networks. European firms are focusing on regulatory compliance, explainable testing solutions, and sustainable manufacturing practices. Overall, the competitive landscape emphasizes technological leadership, strategic collaborations, and regional market penetration as critical drivers of market success.

Thermo Fisher Scientific

BioMérieux

Danaher Corporation

Beckman Coulter

DiaSorin

Sysmex Corporation

Ortho Clinical Diagnostics

Current technologies in the calcitonin testing market include immunoassays, chemiluminescence assays, and enzyme-linked assays, providing high sensitivity and specificity for thyroid and bone metabolism diagnostics. High-sensitivity immunoassays remain the most widely used, covering over 45% of global diagnostic laboratories, due to reliability and accuracy in detecting low calcitonin levels. Emerging technologies, such as AI-assisted data analysis, are improving result interpretation, reducing diagnostic errors by up to 20%, and enhancing workflow efficiency in hospitals and laboratories. Automated chemiluminescence systems are increasingly deployed for high-throughput testing, particularly in North America and Europe, enabling over 1,000 tests per day in large diagnostic centers.

Miniaturized point-of-care devices are being adopted in Asia-Pacific, providing on-site results within 30–45 minutes, facilitating rapid clinical decision-making. Blockchain integration is being explored for secure patient data management and traceability. Additionally, multiplex assay platforms allow simultaneous measurement of multiple biomarkers alongside calcitonin, enhancing clinical insights for thyroid cancer and metabolic bone disease.

Overall, technological advancements are focused on accuracy, automation, digital integration, and real-time diagnostics, positioning the market for enhanced efficiency and innovation adoption globally.

In March 2024, Roche Diagnostics launched the Elecsys Calcitonin Assay, a fully automated high-sensitivity immunoassay, enabling detection of calcitonin levels as low as 2 pg/mL and improving early thyroid carcinoma diagnosis. Source: www.roche.com

In September 2023, Abbott Laboratories introduced AI-powered data interpretation software for their chemiluminescence assays, reducing result analysis time by 20% and increasing accuracy in hospital labs. Source: www.abbott.com

In December 2023, Siemens Healthineers rolled out the Atellica Solution for point-of-care calcitonin testing, allowing clinicians to perform rapid tests within 30 minutes, streamlining patient care workflows. Source: www.siemens-healthineers.com

In May 2024, BioMérieux expanded its automated diagnostic lab systems in North America, integrating high-throughput calcitonin testing with hospital information systems, enabling simultaneous processing of over 1,200 patient samples per day. Source: www.biomerieux.com

The Calcitonin Testing Market Report provides a comprehensive examination of global market dynamics, covering product types, diagnostic applications, and end-user segments. It encompasses leading technologies including immunoassays, chemiluminescence assays, enzyme-linked assays, and emerging AI-assisted diagnostic platforms.

The report highlights regional insights across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, analyzing adoption patterns, infrastructure trends, and consumer behavior. Applications reviewed include thyroid disorder diagnosis, bone metabolism monitoring, and early cancer detection, with a focus on hospitals, diagnostic laboratories, and research institutions as primary end-users. Additionally, the report evaluates the competitive landscape, profiling major global players and their strategic initiatives.

It also explores innovation trends, such as point-of-care testing, high-throughput platforms, and digital integration for clinical workflows. Niche segments, such as multiplex assays and miniaturized portable devices, are examined for future market potential. Overall, the report serves as a strategic guide for stakeholders seeking data-driven insights, investment opportunities, and technology adoption pathways in the calcitonin testing ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 368.2 Million |

| Market Revenue (2032) | USD 637.4 Million |

| CAGR (2025–2032) | 7.1% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Abbott Laboratories, Roche Diagnostics, Siemens Healthineers, Thermo Fisher Scientific, BioMérieux, Danaher Corporation, Beckman Coulter, DiaSorin, Sysmex Corporation, Ortho Clinical Diagnostics |

| Customization & Pricing | Available on Request (10% Customization is Free) |