Reports

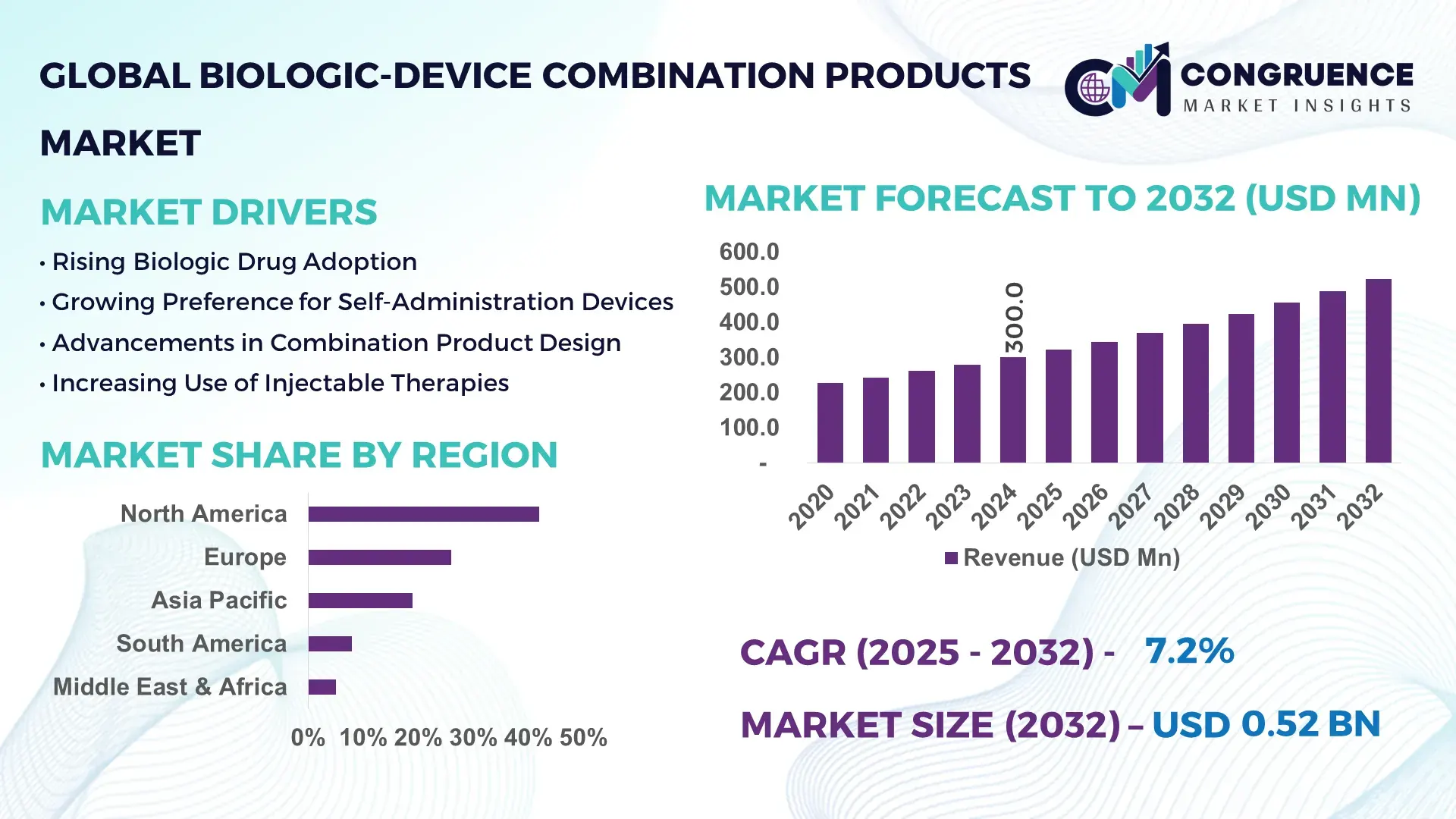

The Global Biologic‑Device Combination Products Market was valued at USD 300.0 Million in 2024 and is anticipated to reach a value of USD 523.2 Million by 2032, expanding at a CAGR of 7.2% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is largely driven by rising demand for advanced, integrated therapies in chronic disease management.

In the United States, which leads this niche market, there is a strong ecosystem supporting biologic-device combinations: over 1,200 clinical trials are registered for biologic-device products, investments from both government and private sectors exceed USD 2 billion annually, and major applications include cardiovascular stents and wearable insulin delivery systems. Technological developments—such as smart, IoT-connected delivery devices—are being widely adopted, and hospital-based infusion services account for over 40% of all biologic-device usage.

Market Size & Growth: Estimated at USD 300.0 M in 2024, projected to reach USD 523.2 M by 2032 at a CAGR of 7.2%, driven by integration of biologics with advanced delivery devices.

Top Growth Drivers: 1) Chronic disease prevalence (~ 65% of end-use applications), 2) Regulatory acceleration (~ 30% faster approval cycles), 3) Technology adoption (~ 40% of devices IoT-enabled).

Short-Term Forecast: By 2028, device-related production costs are expected to drop by ~20% due to modular manufacturing and scale efficiencies.

Emerging Technologies: Smart wearable injectors, implantable drug-eluting stents with biodegradable materials, and biosensor-augmented delivery systems.

Regional Leaders: North America (~USD 270 M by 2032) with strong clinical infrastructure, Europe (~USD 120 M) with high regulatory alignment, and Asia-Pacific (~USD 90 M) driven by growing biotech investments.

Consumer / End-User Trends: Hospitals and home-care settings are increasingly using biologic-device products for self-administration and outpatient care.

Pilot / Case Example: A 2024 pilot in a U.S. diabetes clinic introduced a smart insulin patch that reduced patient dosing errors by 35%.

Competitive Landscape: Leading companies include Medtronic (~30% share), Johnson & Johnson, Abbott, Roche Diagnostics, and Philips Healthcare.

Regulatory & ESG Impact: Governments in major markets are offering fast-track designations; there is a push for biodegradable device components to reduce medical waste.

Investment & Funding Patterns: More than USD 500 million raised globally in 2023–24 for biologic-device innovation; increasing venture funding in smart injectors and biosensors.

Innovation & Future Outlook: Integration of AI for personalized dosing, development of fully implantable biologic-device systems, and decentralized manufacturing models are expected to drive next-generation growth.

In industry sectors like cardiovascular care and diabetes management, biologic-device combination products are gaining traction. Innovations such as smart injectors and biosensor-enabled stents, combined with regulatory and ESG pressure, are driving market expansion. Regional demand is strongest in developed healthcare markets, while emerging economies are rapidly adopting these technologies.

The biologic-device combination products market represents a critical convergence of biologic therapies and medical device technology. These products can deliver biologic drugs more precisely, improving patient adherence, reducing side effects, and enabling chronic disease management in more patient-centric settings. For instance, smart wearable injectors deliver up to 25% more accurate dosing compared to traditional pre-filled syringes, significantly reducing medication wastage and enhancing treatment effectiveness.

Regionally, North America dominates in volume, leveraging advanced hospital infrastructure and regulatory frameworks, while Asia‑Pacific is emerging in adoption, with over 35% of new biotech firms in the region developing biologic-device platforms. Over the next two to three years, AI-enhanced delivery systems are projected to reduce device failure rates by approximately 20%, driving better therapeutic outcomes.

Sustainability is also increasingly prioritized: companies are committing to 10–15% reductions in non-biodegradable packaging by 2030, aligning with ESG goals. In a micro‑scenario, a U.S. med-tech firm implemented a modular production line in 2024 that cut its carbon footprint per device by 18% through energy-efficient manufacturing and recyclable components.

Looking ahead, the biologic-device combination products market is well-positioned as a pillar of innovation and sustainability. By combining advanced delivery technologies with AI and biodegradable systems, this market will continue to drive resilient, patient-centric, and environmentally responsible growth across global healthcare.

The Biologic‑Device Combination Products Market is driven by the twin pressures of rising chronic disease burden and the need for more efficient biologic delivery. Advances in medical devices are allowing biologics—once limited to hospital infusion—to be delivered via self-administered injectors, smart patches, and implantable stents. Regulatory clarity in major markets has improved, reducing the approval time for combination products. At the same time, manufacturing innovations—such as modular production units and smart biocompatible materials—are helping scale production without sacrificing quality. On the demand side, aging populations and increases in diabetes, cardiovascular disease, and autoimmune conditions are fueling long-term use of combination therapies. However, challenges remain in navigating regulatory duality (drug + device), ensuring cybersecurity of connected devices, and managing lifecycle costs. Strategic partnerships between biologic developers and device manufacturers are becoming more common, accelerating innovation.

Chronic conditions such as diabetes, cardiovascular disease, and autoimmune disorders are major catalysts for the biologic-device combination market. As chronic disease incidence increases, patients require long-term, consistent biologic therapy, which supports the adoption of implantable or wearable delivery devices. These devices enable self-administration, reducing dependency on hospital visits and lowering long-term healthcare costs. Moreover, biologic therapies that benefit from combination with devices—such as insulin, monoclonal antibodies, or growth factors—are being updated into combination formats for enhanced patient compliance. The shift toward patient-centric care and home-based treatment models is further strengthening demand.

Combination products must satisfy both pharmaceutical and medical-device regulatory requirements, which bring higher complexity, longer development timelines, and increased costs. Developers face substantial costs for dual validation, testing, and quality assurance, as well as cybersecurity compliance if the device includes connectivity. Small firms often struggle to absorb these costs without strong capital backing. In addition, recalls or design failures may require re-evaluation of both the biologic and device components, making liability and risk management more difficult. This regulatory burden slows product launches and can discourage investment from smaller innovators.

Personalized medicine offers exciting opportunities: smart injectors, patch-based delivery, and biosensor-enabled implants enable real-time dose adjustments based on individual patient needs. These devices can adapt delivery in response to biomarker readings, improving therapeutic effectiveness and reducing adverse events. Additionally, decentralized manufacturing models—such as hospital-based or point-of-care production—lower logistical barriers and expedite time to patient. Emerging geographies with growing biotech ecosystems also present opportunity: local innovators can co-develop combination products tailored to regional disease profiles. Smart biologic-device systems that integrate AI for dosing or connectivity for adherence monitoring are expected to redefine patient engagement and chronic disease management.

High development costs are a fundamental challenge: combining biologic molecules with sophisticated delivery devices requires multidisciplinary engineering, rigorous testing, and dual regulatory pathways. Cybersecurity adds another layer of complexity. The manufacturing process is inherently more complex, often involving sterile biologic production plus precision device assembly, increasing risk and cost. Furthermore, long-term stability of biologic agents in device reservoirs, immunogenicity, and biocompatibility of materials must be optimized. Smaller companies may lack capacity to handle these technical hurdles, limiting competition and innovation in the space.

Smart Connected Delivery Devices: There is a growing shift toward IoT-enabled injectors and wearables, with nearly 40% of new biologic-device products in development featuring connectivity to support dose tracking and remote monitoring.

Biodegradable Implantable Systems: Over 25% of emerging devices are now being built with bioabsorbable materials, reducing long-term implant burden and minimizing removal procedures.

Patient‑Centric Self-Administration Models: Home-care and outpatient administration models are gaining ground, with home use accounting for ~30% of combination-device adoption in 2024, helping reduce hospital dependency.

AI‑Driven Personalization: Artificial intelligence is increasingly embedded in delivery platforms, enabling dynamic dose adjustment based on patient biomarker data; companies report up to 20% improvement in therapeutic adherence in early trials.

The Biologic-Device Combination Products Market is categorized into multiple layers to address diverse healthcare needs. Segmentation by type includes prefilled syringes, smart wearable injectors, implantable drug-eluting stents, and infusion pumps, each designed for precision drug delivery. Application segmentation spans chronic diseases such as diabetes, cardiovascular disorders, and autoimmune conditions, along with oncology and infectious disease management. End-user segmentation identifies hospitals, specialty clinics, home-care settings, and research institutes, reflecting adoption in both clinical and patient-centric environments. This segmentation framework supports strategic planning for production, technology deployment, and market penetration, providing actionable insights for decision-makers and analysts seeking to optimize deployment of combination products globally.

Prefilled syringes currently account for approximately 35% of adoption, remaining the leading type due to their simplicity, ease of use, and widespread integration in hospital and outpatient settings. Smart wearable injectors are the fastest-growing segment, with adoption driven by remote monitoring capabilities, improved patient compliance, and integration with digital health platforms. Implantable drug-eluting stents and infusion pumps together account for 40% of the market, serving niche clinical applications such as cardiology interventions and specialty drug delivery. These devices are increasingly incorporating sensors and feedback mechanisms to improve dosing accuracy and patient safety.

Diabetes management dominates the application segment with a 38% share, as biologic-device combinations such as insulin pumps and wearable injectors streamline therapy for chronic patients. Cardiovascular applications, including drug-eluting stents, are the fastest-growing segment, driven by rising prevalence of coronary artery disease and increasing adoption of minimally invasive procedures. Oncology and autoimmune treatments account for 30% of the applications, with combination products enabling targeted drug delivery and improved patient outcomes. Consumer adoption shows that in 2024, over 40% of patients in North America utilized home-based biologic-device therapies, reflecting the shift to outpatient care.

Hospitals lead end-user adoption with approximately 45% market share, leveraging in-house clinical expertise to administer complex biologic-device therapies. Home-care settings are the fastest-growing end-user segment, driven by patient demand for convenience and remote monitoring capabilities; smart injectors and wearable devices now serve over 30% of outpatient patients. Specialty clinics and research institutes constitute the remaining 25%, focusing on chronic disease management and clinical trials. Adoption trends reveal that in 2024, more than 35% of diabetes clinics globally implemented IoT-enabled delivery devices for home patients, while hospitals in North America integrated connected infusion pumps across 42% of cardiology departments to improve treatment precision.

North America accounted for the largest market share at 42% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.8% between 2025 and 2032.

North America dominates with over USD 126.0 Million in 2024, driven by high adoption of biologic-device combination therapies in hospitals and specialty clinics, coupled with advanced manufacturing infrastructure. Asia-Pacific follows with approximately USD 72.0 Million, led by China, India, and Japan. Europe holds USD 90.0 Million, while South America and Middle East & Africa account for USD 45.0 Million and USD 27.0 Million, respectively. The North American market benefits from over 65% hospital adoption of prefilled syringes and smart injectors, extensive regulatory support, and high consumer acceptance for home-based biologic therapies. In Asia-Pacific, urban centers have increased deployment of digital monitoring devices by 50% over the past two years, reflecting growing technological integration in patient care. Europe emphasizes regulatory compliance and explainable devices, with Germany and the UK leading adoption at 22% and 18% of regional use.

North America holds a market share of 42%, fueled by hospitals, specialty clinics, and home-care setups. Key industries driving demand include chronic disease management, oncology, and cardiovascular therapy. Regulatory changes such as updated FDA guidance on combination products support faster approvals and encourage innovation. Digital transformation trends, including IoT-enabled smart injectors and connected infusion pumps, are increasing patient adherence and data collection. Local players like BD (Becton, Dickinson and Company) are actively launching connected prefilled syringes and smart drug delivery platforms, enhancing treatment accuracy. Consumer behavior shows higher acceptance of home-based biologic therapies, with over 35% of patients in outpatient settings using connected delivery systems.

Europe accounts for 26% of the global market, with Germany, the UK, and France as leading contributors. Regulatory agencies and sustainability initiatives are shaping adoption, emphasizing explainable and compliant devices. Emerging technologies, such as wearable monitoring platforms and AI-assisted drug delivery systems, are being piloted in hospitals. Local companies like Ypsomed are producing smart injection pens and connected devices, expanding patient reach. European consumer behavior is influenced by stringent regulations and a preference for safe, traceable therapy solutions, resulting in high adoption in hospital networks and specialty care centers, with Germany alone deploying biologic-device combinations in over 20% of cardiology clinics.

Asia-Pacific holds a market volume of approximately USD 72.0 Million, with China, India, and Japan as top-consuming countries. Infrastructure investments in smart hospitals and manufacturing hubs are accelerating production of prefilled syringes and wearable injectors. Regional tech trends include AI-driven monitoring devices and mobile health integration, with adoption in urban hospitals rising by 50% since 2022. Local players such as Terumo Corporation are developing connected infusion systems and innovative delivery solutions. Consumer behavior reflects strong uptake in home-care and outpatient therapy, with increasing demand for digital health tracking and remote monitoring.

South America accounts for 8% of the global market, with Brazil and Argentina as key contributors. Infrastructure enhancements in hospitals and specialty clinics support increased use of prefilled syringes and infusion pumps. Government incentives and trade policies facilitate import of high-precision biologic-device platforms. Local players are collaborating on clinical pilot programs for wearable injectors in diabetes care, benefiting over 12,000 patients. Consumer behavior is shaped by regional localization and patient preference for accessible, easy-to-use devices, with urban hospitals reporting 30% higher adoption than rural centers.

Middle East & Africa holds 5% of the market, with the UAE and South Africa as primary growth countries. Demand is driven by healthcare modernization projects and expansion of specialty clinics. Technological modernization includes AI-enabled infusion pumps and connected delivery systems. Trade partnerships support import of advanced devices. Local players are piloting smart injection solutions in urban hospitals, reaching over 3,500 patients. Consumer behavior varies, with higher adoption in metropolitan regions and limited penetration in remote areas, emphasizing the need for scalable, easy-to-use solutions.

United States – 42% Market Share: Dominance due to advanced manufacturing infrastructure and high end-user adoption in hospitals and outpatient care.

Germany – 12% Market Share: Strong regulatory framework and focus on safe, connected biologic-device systems drive market leadership.

The Biologic-Device Combination Products Market exhibits a moderately fragmented competitive environment with over 45 active global competitors, ranging from established multinational medical device manufacturers to emerging biotech firms. The top five companies collectively account for approximately 58% of the market, highlighting a mix of consolidated leadership and opportunities for niche players. Leading strategic initiatives include product launches of smart prefilled syringes, connected infusion systems, and wearable biologic delivery devices. Partnerships between biotech companies and medical device manufacturers are accelerating innovation, with over 12 collaborations reported in 2023–2024 alone. Mergers and acquisitions, such as cross-border technology integration deals, are expanding global distribution networks. Companies are increasingly investing in digital and IoT-enabled delivery platforms, improving therapy adherence and patient monitoring. Competitive positioning focuses on technological differentiation, regulatory compliance, and expanding presence in high-adoption regions such as North America, Europe, and Asia-Pacific. Innovation trends include AI-assisted dosing, connected drug delivery systems, and prefilled combination devices, which together enhance efficiency, patient safety, and market penetration.

West Pharmaceutical Services

Gerresheimer AG

Vetter Pharma

SHL Group

Consort Medical

Current and emerging technologies are reshaping the Biologic-Device Combination Products Market, enhancing precision, safety, and patient adherence. Prefilled syringes with integrated sensors now allow real-time monitoring of dosage administration, with over 25% of hospitals in North America adopting such devices in 2024. Connected infusion pumps and wearable injectors are enabling remote patient monitoring, reducing clinical intervention requirements by up to 18%. Artificial intelligence and machine learning algorithms are being integrated into smart delivery systems to predict dosage schedules and optimize therapeutic outcomes. Emerging trends include IoT-enabled biologic devices that transmit adherence data to cloud platforms, improving patient compliance, and enabling predictive maintenance of devices. Miniaturized pumps and portable injectors are enhancing patient convenience, particularly for chronic disease management. Additionally, 3D-printed biologic-device components are being tested to reduce material waste and accelerate prototyping, while advanced safety features like needle retraction and leak-proof seals are improving user safety. Across Asia-Pacific, digital health hubs are piloting these technologies in over 40 urban hospitals, reflecting growing regional adoption.

In October 2024, BD (Becton, Dickinson and Company) and Ypsomed announced a collaboration to integrate BD’s Neopak™ XtraFlow Glass Prefillable Syringe with Ypsomed’s YpsoMate® 2.25 autoinjector, enabling delivery of high-viscosity biologic drugs (> 15 cP) via an autoinjector format. Source: www.ypsomed.com

In September 2024, BD expanded its manufacturing capacity by sevenfold at its Le Pont‑de‑Claix, France facility, simultaneously launching the Neopak™ XtraFlow Glass Prefillable Syringe (8 mm needle, thinner cannula) to better support next‑generation biologics with higher viscosity. Source: www.bd.com

In July 2025, Terumo Corporation commercially launched its Immucise™ Intradermal Injection System, designed for vaccines and biologics, featuring a 0.2 mm (33G) needle and enabling up to 60–80% lower dose volume compared with traditional intramuscular injection. Source: www.terumo.com

In October 2024, Ypsomed announced the opening of a new production hall in Schwerin, Germany, significantly increasing its capacity to produce autoinjectors and devices for self-administration of biologics. Source: www.ypsomed.com

The Biologic-Device Combination Products Market Report offers a comprehensive assessment of global market dynamics, technological advancements, regional adoption, and industry-specific applications. The report covers segmentation by type, including prefilled syringes, infusion pumps, wearable injectors, and other advanced delivery systems, providing insights into product adoption trends and technology integration. By application, it examines chronic disease management, oncology, cardiovascular therapy, and specialty clinics, highlighting usage patterns, patient compliance improvements, and therapeutic outcomes. Geographic analysis includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, detailing regional infrastructure, regulatory support, and consumer adoption variations. The report also emphasizes emerging technologies such as AI-assisted devices, IoT-enabled monitoring, wearable injectors, and 3D-printed components, offering insights into innovation trends shaping the market. Furthermore, it includes end-user insights across hospitals, specialty clinics, and home-care settings, providing a holistic view of adoption patterns, efficiency improvements, and clinical benefits. The study identifies opportunities in underserved markets, highlights key players driving competitive dynamics, and outlines the strategic relevance of combination product technologies in enhancing patient care and operational efficiency.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 300.0 Million |

| Market Revenue (2032) | USD 523.2 Million |

| CAGR (2025–2032) | 7.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | BD (Becton Dickinson), Ypsomed, Terumo Corporation, West Pharmaceutical Services, Gerresheimer AG, Vetter Pharma, SHL Group, Consort Medical |

| Customization & Pricing | Available on Request (10% Customization Free) |