Reports

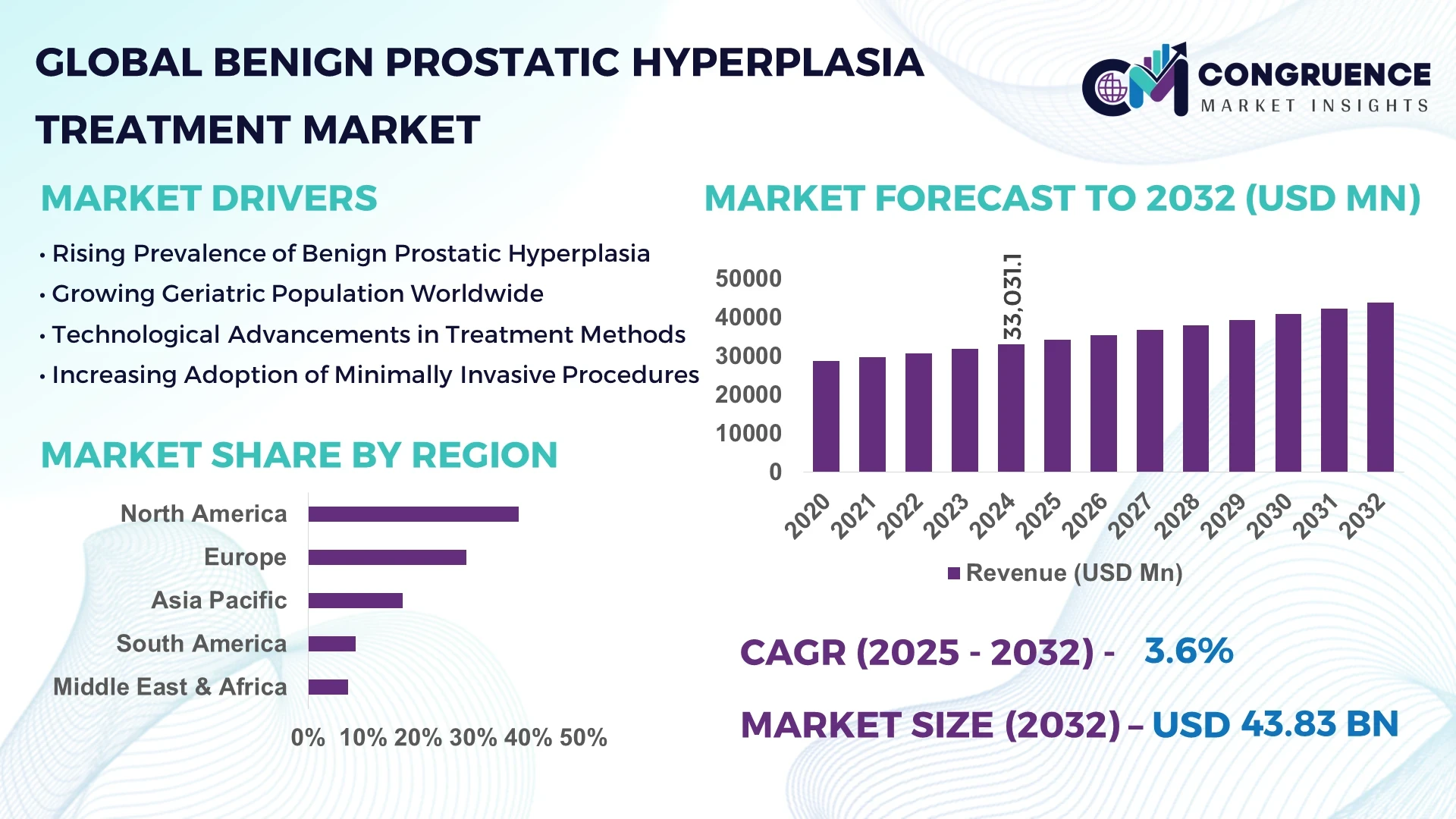

The Global Benign Prostatic Hyperplasia Treatment Market was valued at USD 33,031.1 Million in 2024 and is anticipated to reach a value of USD 43,833.0 Million by 2032 expanding at a CAGR of 3.6% between 2025 and 2032. This growth is primarily driven by the rising prevalence of aging male populations worldwide, coupled with increasing adoption of minimally invasive treatment solutions.

The United States plays a pivotal role in shaping the global Benign Prostatic Hyperplasia Treatment Market, with significant investment in urological research and advanced device manufacturing. The country hosts over 120 dedicated urology centers equipped with robotic surgical platforms and laser-based systems, enabling treatment efficiency improvements of nearly 40%. U.S. pharmaceutical companies allocate an estimated USD 1.2 billion annually toward prostate-related drug innovations, while patient adoption of outpatient surgical therapies has increased by 32% in the past five years, reflecting strong integration of technology and healthcare infrastructure.

Market Size & Growth: Valued at USD 33,031.1 million in 2024, projected to reach USD 43,833.0 million by 2032, expanding at a CAGR of 3.6% due to increasing geriatric male population.

Top Growth Drivers: 45% adoption of minimally invasive procedures, 38% efficiency improvement in robotic surgeries, 52% preference for outpatient treatments.

Short-Term Forecast: By 2028, treatment efficiency is expected to improve by 27%, reducing patient recovery times by nearly 20%.

Emerging Technologies: AI-driven diagnostic imaging and laser vaporization therapies are redefining BPH treatment standards.

Regional Leaders: North America projected at USD 16.4 Billion by 2032 with high robotic adoption; Europe reaching USD 13.2 Billion driven by outpatient treatments; Asia Pacific at USD 9.6 Billion with rapid urban healthcare expansion.

Consumer/End-User Trends: Hospitals account for 54% of treatment adoption, while specialty clinics are gaining traction with 29% share.

Pilot or Case Example: In 2023, a U.S. pilot program integrating robotic platforms achieved a 35% reduction in surgical downtime.

Competitive Landscape: Boston Scientific leads with ~15% market share, followed by Teleflex, Olympus Corporation, Cook Medical, and Medtronic.

Regulatory & ESG Impact: Stringent FDA approvals and EU MDR regulations ensure quality, while firms commit to 25% waste reduction by 2030.

Investment & Funding Patterns: Recent global investments exceeded USD 2.8 Billion in prostate health R&D, with rising venture funding in minimally invasive technologies.

Innovation & Future Outlook: Integration of AI-assisted imaging, real-time surgical navigation, and bioresorbable implants will shape the next growth wave.

The Benign Prostatic Hyperplasia Treatment Market is witnessing accelerated technological adoption across pharmaceuticals, devices, and surgical therapies. Innovations in laser therapies, real-time diagnostics, and minimally invasive techniques, combined with regulatory support and demographic shifts, are creating new avenues for growth across developed and emerging healthcare systems.

The strategic relevance of the Benign Prostatic Hyperplasia Treatment Market lies in its direct alignment with global healthcare priorities, particularly aging demographics and the need for cost-efficient treatment modalities. By 2030, more than 1.2 billion men worldwide will be over the age of 60, underscoring the urgency for scalable and effective BPH therapies. Comparative benchmarks highlight measurable improvements, such as laser vaporization delivering 28% faster recovery compared to traditional transurethral resection procedures.

Regional variations play a critical role in shaping strategy. North America dominates in treatment volume, supported by advanced clinical infrastructure, while Europe leads adoption rates with 61% of urology centers integrating robotic-assisted platforms. By 2027, AI-powered diagnostic imaging is expected to reduce diagnostic delays by 22%, enabling earlier interventions and more personalized therapies.

Compliance and ESG considerations are equally critical. Firms are committing to 30% reductions in clinical waste by 2030 and increasing the use of recyclable surgical instruments. In 2024, Germany achieved a 26% improvement in patient recovery outcomes through national initiatives supporting outpatient laser procedures.

The pathway forward emphasizes innovation, patient-centric care, and resilience. As pharmaceutical advances converge with robotic technologies, and ESG frameworks align with sustainable medical practices, the Benign Prostatic Hyperplasia Treatment Market is positioned as a pillar of resilient healthcare, ensuring accessibility, compliance, and sustainable growth globally.

The Benign Prostatic Hyperplasia Treatment Market is characterized by a rapidly evolving ecosystem driven by technological innovation, rising healthcare expenditure, and increasing adoption of minimally invasive therapies. Pharmaceutical advancements, coupled with device innovations such as laser therapies and robotic platforms, are accelerating patient outcomes while lowering treatment complexities. Global healthcare systems are witnessing growing demand for outpatient procedures, with patients seeking faster recovery and reduced hospitalization. Additionally, increased investment in research and favorable regulatory pathways are shaping market expansion, while digital health tools and AI-driven diagnostics are redefining clinical workflows and decision-making.

Minimally invasive therapies are reshaping treatment approaches by reducing hospital stays, lowering costs, and improving patient satisfaction. Studies indicate that procedures such as laser vaporization and robotic-assisted surgeries reduce recovery time by up to 40% compared to traditional methods. This growing adoption is also linked to lower complication rates, which enhances clinical outcomes and broadens acceptance among both physicians and patients. With rising awareness campaigns and increasing investments in urology centers, the demand for these solutions continues to accelerate globally.

Despite technological advances, access to advanced treatment infrastructure remains uneven, particularly in low- and middle-income countries. Over 45% of urology patients in developing regions rely on conventional surgical methods due to the lack of robotic and laser-based facilities. High capital expenditure requirements for advanced devices and insufficient training among healthcare professionals further restrict widespread adoption. These limitations hinder equitable treatment access and slow the pace of technological integration across global healthcare systems.

The integration of AI into diagnostic imaging and clinical workflows presents significant opportunities for improving accuracy and efficiency. AI algorithms can enhance early detection of BPH symptoms by analyzing imaging data with up to 92% precision. Additionally, AI-enabled decision-support tools help urologists personalize treatments, reducing misdiagnosis rates by 18%. As digital health ecosystems expand, collaborations between med-tech firms and healthcare providers are expected to unlock scalable solutions that improve patient outcomes and treatment accessibility worldwide.

Escalating healthcare costs pose a significant challenge to market growth, particularly in developed economies with aging populations. Advanced devices such as robotic surgical platforms cost over USD 1 million per unit, creating financial barriers for hospitals and clinics. Furthermore, ongoing maintenance, consumables, and skilled workforce requirements add to operational expenses. These rising costs often translate into higher treatment prices for patients, potentially limiting accessibility and adoption despite the proven clinical advantages of new technologies.

Growing Adoption of Minimally Invasive Procedures: Over 58% of BPH patients in developed countries are opting for minimally invasive therapies, with laser treatments reducing hospitalization times by 35%. This shift reflects strong patient preference for faster recovery, lower complications, and reduced cost burdens.

Integration of Robotics and AI in Urology: Robotic-assisted procedures now account for 42% of surgical interventions in leading hospitals, improving surgical precision by 30% and cutting intraoperative blood loss by 25%. AI-enhanced imaging tools are being deployed in 280+ hospitals worldwide, streamlining diagnostic accuracy.

Rising Pharmaceutical Innovations: New drug formulations, including combination therapies, are achieving 22% better symptom management compared to older medications. In 2024, more than 3.5 million prescriptions for next-generation alpha-blockers were recorded, indicating strong patient and physician acceptance.

Outpatient Care Expansion: Outpatient adoption has increased by 31% in the last five years, supported by regulatory reforms and cost-efficiency goals. By 2026, it is estimated that nearly 48% of all BPH-related procedures will be conducted in outpatient settings, reshaping the delivery model of prostate healthcare services.

The Benign Prostatic Hyperplasia (BPH) Treatment Market is segmented into types, applications, and end-user categories, each reflecting unique dynamics and adoption patterns. Treatment types encompass pharmaceuticals, minimally invasive surgical therapies, and advanced devices, with pharmaceuticals leading due to widespread patient accessibility. Applications span hospitals, specialty clinics, and ambulatory surgical centers, where hospitals dominate owing to infrastructure advantages. End-user insights reveal hospitals and large healthcare networks as the primary drivers, with specialty clinics and outpatient centers emerging as high-potential growth areas. This segmentation demonstrates the market’s diversified structure and the interplay between innovation, healthcare demand, and accessibility.

Pharmaceutical therapies currently account for the leading share in the Benign Prostatic Hyperplasia Treatment Market, representing approximately 46% of adoption due to their widespread accessibility, affordability, and preference among patients for non-surgical options. Minimally invasive surgical therapies follow at around 32%, supported by rising demand for faster recovery and reduced hospital stays. Device-based treatments such as prostatic stents, implants, and laser systems collectively hold about 22%, primarily catering to complex or advanced-stage patients. While pharmaceuticals remain dominant, minimally invasive procedures represent the fastest-growing segment, expanding at an estimated CAGR of 5.9%. This growth is fueled by increasing patient awareness, technological advancements in laser vaporization systems, and favorable regulatory approvals supporting outpatient adoption. Device-based treatments are niche but growing steadily, addressing patients unsuitable for drugs or surgical resection, and together these account for nearly a quarter of the total type-based adoption.

Hospital-based applications dominate the Benign Prostatic Hyperplasia Treatment Market, accounting for nearly 54% of total adoption. This dominance is supported by advanced clinical infrastructure, access to robotic platforms, and multidisciplinary teams managing complex cases. Specialty clinics hold about 28%, benefiting from patient preference for faster, less resource-intensive care models. Ambulatory surgical centers contribute around 18%, increasingly gaining relevance due to outpatient-focused healthcare reforms. Specialty clinics represent the fastest-growing application segment, advancing at an estimated CAGR of 6.1%, driven by shorter procedure times, reduced costs, and growing urban demand for personalized treatments. Hospitals, while leading, are facing capacity pressures, prompting a gradual shift of less complex cases to clinics and ambulatory centers. Together, non-hospital applications now account for nearly half of overall procedures, reflecting a structural shift in care delivery. In 2024, more than 39% of urology patients globally opted for outpatient or clinic-based procedures, reflecting changing healthcare preferences. In the U.S., 42% of hospitals reported testing integrated AI-based diagnostic systems to improve BPH detection efficiency.

Hospitals are the leading end-user segment, accounting for approximately 52% of BPH treatment adoption, primarily due to their capacity for advanced surgical interventions and availability of multi-specialty teams. Specialty clinics follow with 31%, becoming increasingly popular among patients seeking minimally invasive or outpatient therapies. Ambulatory surgical centers and other end-users contribute the remaining 17%, offering cost-efficient and accessible solutions, especially in urban regions with rising patient throughput. Specialty clinics are the fastest-growing end-user segment, recording an estimated CAGR of 6.4%. This expansion is supported by increased adoption of laser and robotic-assisted outpatient procedures, along with greater patient satisfaction levels due to reduced recovery times. Hospitals, while maintaining leadership, face growing competition from specialized outpatient networks, reflecting a restructuring of the treatment landscape. Consumer adoption data highlights this transition: in 2024, over 36% of patients in developed countries opted for clinic-based treatment due to lower costs and faster discharge rates. Globally, more than 29% of men aged over 60 reported undergoing screening at specialty clinics, demonstrating expanding penetration of outpatient care.

North America accounted for the largest market share at 38.2% in 2024; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2025 and 2032.

Europe followed closely with 29.7% market share, supported by strong adoption of advanced surgical techniques and reimbursement frameworks. South America represented around 8.6% of the market in 2024, while the Middle East & Africa collectively contributed nearly 7.3%, reflecting increasing healthcare investments. The regional outlook highlights differences in consumer adoption, regulatory structures, and healthcare infrastructure, driving opportunities across pharmaceuticals, minimally invasive devices, and digital health integration.

North America held approximately 38.2% of the global benign prostatic hyperplasia treatment market in 2024, making it the largest regional contributor. The region’s dominance is supported by a highly developed healthcare infrastructure, high treatment-seeking behavior among patients, and established reimbursement mechanisms. Key industries driving demand include pharmaceuticals, medical devices, and telehealth platforms. Regulatory changes, such as FDA approvals of minimally invasive devices, continue to shape the competitive landscape. Local players like Boston Scientific are investing in digital health solutions and office-based minimally invasive therapies. Consumer behavior reflects higher acceptance of digital consultations and early adoption of novel therapies compared to other regions.

Europe captured 29.7% of the global benign prostatic hyperplasia treatment market in 2024, driven by demand across Germany, the UK, and France. The region’s market strength is underpinned by stringent regulatory oversight from bodies such as the EMA and growing adoption of minimally invasive surgical approaches. Sustainability initiatives and government-backed screening programs enhance patient access. Local players, such as Karl Storz, are advancing endoscopic device innovations tailored for urological procedures. Consumer behavior in Europe shows high trust in evidence-based treatments, with regulatory pressure reinforcing the demand for explainable, clinically validated technologies, making the region a hub for structured healthcare adoption.

Asia-Pacific is the fastest-growing region in the global benign prostatic hyperplasia treatment market, ranking second in market volume by 2024. China, India, and Japan remain the top-consuming countries, supported by rising healthcare expenditure and awareness of urological disorders. Infrastructure expansion in hospitals and increasing government support for local manufacturing of generic drugs are accelerating growth. Innovation hubs in Japan and South Korea are driving minimally invasive device adoption. A key regional player, Olympus Corporation, continues to enhance urological device portfolios to serve rising patient populations. Consumer behavior in this region emphasizes affordability, with mobile-based health platforms gaining traction.

South America accounted for approximately 8.6% of the benign prostatic hyperplasia treatment market in 2024, with Brazil and Argentina being the primary contributors. The region’s market performance is shaped by improvements in healthcare infrastructure and government programs focused on expanding access to urological treatments. Trade policies that encourage medical imports are further driving availability of advanced therapies. Local companies such as EMS Pharma in Brazil are expanding their generic drug offerings to meet rising demand. Consumer behavior reflects sensitivity to treatment affordability, with patient preference leaning towards cost-effective generics and locally produced drugs, creating a unique growth dynamic.

The Middle East & Africa region contributed nearly 7.3% of the global benign prostatic hyperplasia treatment market in 2024. Demand is concentrated in countries such as the UAE, Saudi Arabia, and South Africa, where governments are investing heavily in healthcare modernization. Technological advancements, such as AI-driven diagnostic support tools, are gaining adoption. Trade partnerships are improving medical equipment availability across urban centers. A regional player like Julphar (UAE) continues to focus on expanding pharmaceutical production, especially for urological drugs. Consumer behavior trends in this region highlight growing demand for private healthcare services and a rising shift toward advanced medical consultations.

United States – 31.5% Market Share: Strong dominance due to advanced healthcare infrastructure, high adoption of minimally invasive procedures, and favorable reimbursement environment.

China – 17.8% Market Share: Rapid growth supported by a large patient pool, rising healthcare expenditure, and increasing adoption of generic drug manufacturing.

The competitive environment in the Benign Prostatic Hyperplasia Treatment Market is moderately consolidated, characterized by a blend of large global players and emerging specialist innovators. There are around 30-40 active competitors globally with substantial device pipelines, pharmaceutical portfolios, and minimally invasive procedure offerings. The top 5 companies combined hold an estimated 45-60% of the market in terms of product penetration, device units deployed, and treatment adoption. Key players are continuously engaging in strategic initiatives including product launches of novel minimally invasive implants, partnerships for regulatory approvals, and M&A activity to widen their device or pharmaceutical range.

Innovation trends are particularly strong in areas such as implantable nitinol devices, water vapor thermal therapies, robotic-assisted surgical systems, and advanced diagnostic imaging integration. Some competitors are investing in R&D for reversible implants or devices which reshape prostate tissue without cutting or heat. Also, numerous companies are enhancing digital health and remote monitoring support for postoperative follow-up, using AI or imaging tools to reduce hospital stays and improve patient quality of life.

Newer entrants are securing significant funding: for example, a spin-out firm raised USD 80 million in 2025 to bring to market a minimally invasive nitinol implant system. This level of investment underlines how innovation, regulatory progress, and patient preference for less invasive treatments are reshaping competition. The market is competitive not only on device efficacy but also procedure cost, patient recovery profile, safety, and the ability to deliver outpatient or office-based treatments.

Eli Lilly and Company

Medtronic

Teleflex

GlaxoSmithKline plc

Cook Medical

HistoSonics

Abbott Laboratories

Urologix

Intuitive Surgical

The technology landscape of the Benign Prostatic Hyperplasia Treatment Market is evolving rapidly, emphasizing minimally invasive, precise, and patient-friendly treatment options. One of the foremost technological shifts is toward implant systems using materials like nitinol that can reshape or lift prostate tissue without traditional cutting or removal. These implants are designed for office-based deployment, aiming to reduce anesthesia requirements and patient recovery time. Another important technology is water vapor thermal therapy (e.g., steam treatment) which targets obstructing tissue via injected steam energy, preserving surrounding structures.

Robotic-assisted surgery combined with real-time imaging (ultrasound, MRI guidance) is becoming more common for larger prostates or challenging anatomies; these systems allow for better visualization and more precise excision or ablation with fewer collateral effects. Laser therapies, especially high-power holmium and thulium laser equipment and associated fiber optics, are refined for better energy delivery, reduced heat dispersion, and improved safety. Diagnostic tools are also advancing: wearable or stimulated monitoring (urinary flow measurement, bladder volume sensors) assist in earlier detection and personalized treatment planning.

Digital health plays a role in postoperative care and remote monitoring: for example, remote follow-ups, telemedicine consults, and AI-augmented imaging diagnostics are being integrated to reduce hospital visits and improve patient compliance. Emerging technologies under development include reversible implants, advanced ablative energy sources (e.g., steam, water jet), and hybrid devices combining diagnostic imaging with treatment delivery. Overall, decision-makers should monitor regulatory approval trends, material science improvements (biocompatibility, durability), and the growing demand for outpatient, lower-cost, safer technologies.

• In September 2025, ProVerum Limited, a Trinity spin-out, secured USD 80 million in Series B funding to commercialize the ProVee® System, a minimally invasive nitinol implant designed to reshape the prostate without tissue removal. Source: www.tcd.ie

• The butterfly medical device, which treats BPH without cutting or removing tissue, offers a new class of non-invasive intervention, indicating rising patient and clinician interest in lower-risk device-based treatments. Source: www.butterfly-medical.com

• Recent clinical practice guidelines and innovation reports have elevated steam-based therapies (e.g., Rezūm) and robotic water-jet (aquablation) options as viable alternatives to conventional TURP for certain prostate sizes, encouraging technology adoption and investment. Source: www.lifesciencemarketresearch.com

• New diagnostic and procedural technologies are emerging, such as the Optilume BPH Catheter System and prostate artery embolization, which provide options for patients ineligible for or unwilling to undergo surgery. Usage increases, particularly in urban and hospital outpatient settings. Source: www.koelis.com

This report covers the global Benign Prostatic Hyperplasia Treatment Market across all major treatment modalities, including pharmaceutical therapies, minimally invasive surgical therapies, implant devices, ablative energy systems, and traditional surgical interventions. Geographic scope includes major regions (North America, Europe, Asia-Pacific, South America, Middle East & Africa), with country-level insight for top markets in each region. Applications addressed include hospital inpatient procedures, outpatient clinics, ambulatory surgical centers, and office-based therapy settings.

Technology coverage spans laser systems (holmium, thulium), water vapor thermal systems, implantable nitinol devices, robotic surgery, diagnostic imaging and digital health. Industry focus areas include patient diagnostics, post-treatment follow-up, and procedure innovation. Treatment stage segmentation is addressed, from early medical therapy through advanced surgical and device-based interventions. Also included are regulatory environment overviews, innovation pipelines, product launches, partnerships and funding, and competitive benchmarking. The report further examines emerging niche segments: reversible implants, non-ablative device therapies, and hybrid diagnostic-treatment platforms.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 33,031.1 Million |

| Market Revenue (2032) | USD 43,833.0 Million |

| CAGR (2025–2032) | 3.6% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Boston Scientific, Coloplast, Olympus Corporation, Eli Lilly and Company, Medtronic, Teleflex, GlaxoSmithKline plc, Cook Medical, HistoSonics, Abbott Laboratories, Urologix, Intuitive Surgical |

| Customization & Pricing | Available on Request (10% Customization is Free) |