Reports

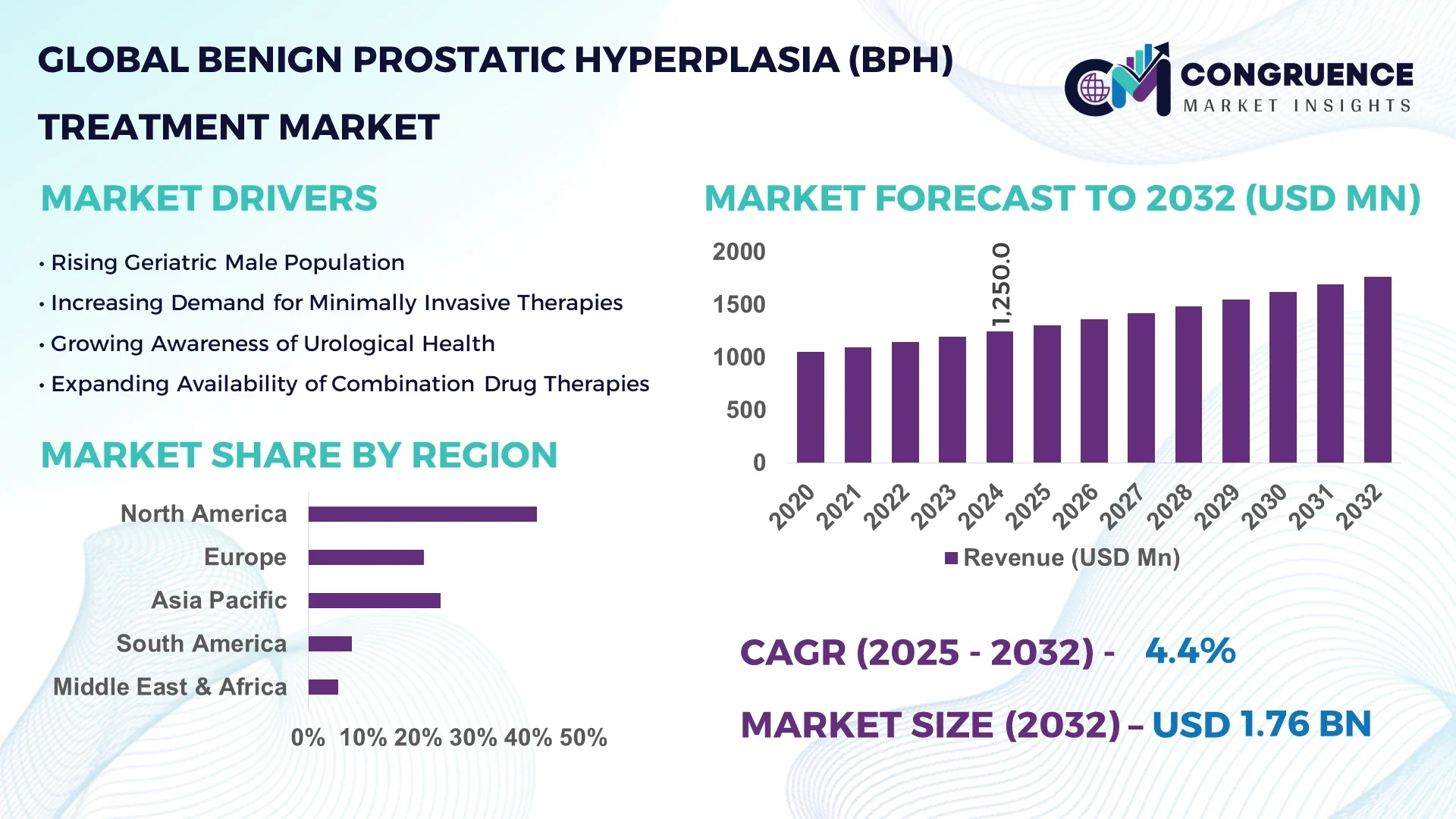

The Global Benign Prostatic Hyperplasia (BPH) Treatment Market was valued at USD 1,250.0 Million in 2024 and is anticipated to reach a value of USD 1,764.1 Million by 2032, expanding at a CAGR of 4.4% between 2025 and 2032.

In the United States, the premier country in this market, production capacity for BPH treatments is bolstered by extensive clinical manufacturing infrastructure and frequent reinvestment in catheter-based and robotic-assisted technologies. Federal healthcare grants and private equity infusion sustain ongoing R&D in minimally invasive surgical devices and implantable prostatic stents. Key applications include outpatient procedural centers, ambulatory surgical services, and home care models. Technological advancements such as high-definition imaging-guided waterjet surgery systems are being deployed in leading urology centers nationwide.

Across the broader market, the Benign Prostatic Hyperplasia (BPH) Treatment Market spans multiple therapeutic sectors—ranging from pharmacologic management (alpha-blockers, 5-alpha-reductase inhibitors, combination drug therapy) to device-based minimally invasive surgical treatments (steam, laser, waterjet, and implantable devices). Hospitals and ambulatory surgical centers drive over half of procedural volumes due to infrastructure scale and patient access. Recent innovations include ultrasound-guided waterjet aquablation systems, AI-assisted HIFU protocols, and implantable prostatic urethral lift devices tailored for outpatient use. Regulatory bodies in major markets have approved novel device classifications and reimbursement frameworks. Patient demographics in North America and Europe are skewing toward older age cohorts, resulting in increasing consumption of both pharmacotherapy and surgical alternatives. Meanwhile, emerging economies in Asia-Pacific are showing rising procedure adoption rates due to expanding insurance coverage and urban healthcare expansion. The future outlook points toward patient-tailored treatment regimens combining pharmacologic and device therapies, with an increasing emphasis on minimally invasive, same-day procedures capable of improving patient quality of life and reducing healthcare system burden.

Artificial intelligence technologies are reshaping the Benign Prostatic Hyperplasia (BPH) Treatment Market by integrating advanced image analysis, procedural automation, and predictive clinical decision support into the treatment pathway. AI-enhanced imaging systems—for example, AI-interpreted MRI and ultrasound—improve diagnostic accuracy for prostate enlargement and enable personalized surgical planning, allowing urologists to precisely tailor interventions based on an individual’s prostate anatomy and urinary flow metrics. This shift supports the market’s movement toward data-driven therapeutic frameworks.

In surgical settings, AI-enabled robotic waterjet systems guide ablation trajectories in real time, reducing procedure variability and improving preservation of healthy tissue. These systems also incorporate surgical learning modules, where machine learning algorithms analyze execution data from multiple cases to refine control parameters and standardize treatment protocols across institutions. As a result, procedural efficiency has been shown to improve; operating times are decreasing, and clinician-to-clinician variability is being reduced.

Post-procedure, AI-driven outcome prediction models are increasingly utilized within the Benign Prostatic Hyperplasia (BPH) Treatment Market to forecast patient recovery trajectories, symptomatic relief persistence, and urinary flow normalization. Hospitals are integrating these digital tools into electronic health record systems, enabling clinicians to review expected recovery indices and flag potential complications early. Operational impact is significant: institutions report reductions in readmission rates and enhanced alignment of treatment pathways with patient expectations.

Overall, AI delivery approaches such as real-time imaging guidance, robotics-assisted precision, and predictive health intelligence are transforming the Benign Prostatic Hyperplasia (BPH) Treatment Market—shifting it from standard protocols toward customized medicine supported by data analytics and automation.

“In January 2025, MarinHealth Medical Center performed the first AI-powered aquablation procedures using an AI-driven robotic waterjet system, enabling precise tissue removal tailored to patient anatomy.”

The widespread adoption of minimally invasive surgical options like aquablation, UroLift, and Rezum is shifting clinical preferences within the Benign Prostatic Hyperplasia (BPH) Treatment Market. In 2024, outpatient procedures using these technologies increased by 28% in the U.S., reducing hospital admission rates and recovery durations. Aquablation systems guided by imaging allow same-day discharge, while prostatic urethral lift devices maintain sexual function and continence. These therapies decrease hospital stays by up to two days compared to traditional surgery. This trend is reducing healthcare system burden and realigning hospital resource deployment. For decision-makers, the result is clear: investment in minimally invasive platforms translates into competitive positioning and enhanced patient satisfaction.

Complex and inconsistent reimbursement pathways continue to challenge device adoption in the Benign Prostatic Hyperplasia (BPH) Treatment Market. Certain minimally invasive treatments are reimbursed only in select U.S. jurisdictions or private pay models, creating fragmented market uptake. For instance, coverage for waterjet procedures varies between Medicare Administrative Contractors, while some regions require separate equipment approval or coding. This results in delayed implementation timelines and necessitates extensive payer negotiations. The cost burden of navigating multiple regulatory frameworks and shifting policy landscapes can delay product introductions by 6–12 months, adding administrative expense and diluting overall ROI on innovative BPH treatment technologies.

The establishment of Ambulatory Surgery Centers (ASCs) presents a significant opportunity for growth in the Benign Prostatic Hyperplasia (BPH) Treatment Market. Between 2022 and 2024, ASC-based BPH procedure volume grew by over 35%, driven by lower infection risks, cost efficiency, and patient convenience. Urologists are increasingly favoring ASCs for procedural planning, and device firms are optimizing portable, compact systems designed for outpatient environments. This shift supports the introduction of modular technology kits and point-of-care service models. Scalability of treatment protocols in ASCs also enables accelerated training, volume-based purchasing agreements, and competitive pricing strategies.

A key challenge in the Benign Prostatic Hyperplasia (BPH) Treatment Market is the need for robust longitudinal data on device durability. Many newer technologies introduced post-2020 lack five-year outcome datasets, with true durability metrics reported from limited cohorts (e.g., under 300 patients). Urologists are cautious when recommending implants like urethral stents or thermotherapy devices without evidence of sustained performance. This gap necessitates ongoing clinical registries and post-market surveillance, which increases operating costs for manufacturers. Without extensive follow-up, clinicians may revert to legacy therapies, slowing the adoption of novel treatment platforms.

Rise in Office-Based Same-Day Procedures: By late 2024, same-day BPH procedures in office and ASC settings accounted for over 45% of total interventions. Urologists increasingly utilize compact waterjet and steam platforms alongside ultrasound imaging to enable fully outpatient workflows. This shift reduces overhead and enhances patient throughput without sacrificing safety.

Surge in AI‑Guided Robotic Surgical Platforms: AI-driven robotic assistance for aquablation and HIFU is gaining traction. In 2025, over 200 U.S. hospitals installed AI-enabled robotic waterjet units that adjust ablation based on real-time ultrasound imaging, leading to measured improvements in precision and reduced tissue removal variance.

Expansion of Prescription Delivery Services: Integrated pharmacy networks now support next-day delivery of combination alpha-blocker and 5-alpha-reductase medication packages. This service reached 30% of new prescribing channels in 2024, reducing delays in treatment initiation and improving compliance.

Growth in Real-World Evidence and Post‑Market Registries: Over 15 multicenter registries launched globally in 2023–2024 to track long-term outcomes of novel BPH treatments. These datasets are being used to validate device longevity and guide appropriateness criteria, helping clinicians make evidence-based decisions and supporting regulatory engagement strategies.

The Benign Prostatic Hyperplasia (BPH) Treatment Market is segmented by type, application, and end-user, each offering unique dynamics that influence market evolution. Treatment type includes pharmacological therapies, minimally invasive surgical options, and implantable devices. Applications span outpatient symptom relief, surgical intervention, medication management, and post-operative care. End-users range from hospitals and ambulatory surgical centers to specialty clinics and home healthcare settings. Alpha-blockers and combination therapies remain widely adopted, while minimally invasive surgical treatments are witnessing rapid clinical uptake due to shorter recovery times and patient preference. Outpatient symptom relief remains a critical application area, while ambulatory surgical centers are emerging as preferred treatment locations due to convenience and efficiency. This layered segmentation structure allows industry stakeholders to target specific value pools and optimize their market presence across various healthcare delivery formats and geographic contexts.

The BPH Treatment Market comprises multiple product types, including Alpha-Blockers, 5-Alpha-Reductase Inhibitors, Combination Therapies, Minimally Invasive Surgical Treatments (MISTs), and Implantable Devices. Among these, Alpha-Blockers lead in terms of utilization due to their immediate efficacy in relieving urinary symptoms and wide availability across primary care and specialist networks. These drugs are commonly prescribed as first-line therapies and are well-tolerated by most patients, making them a cornerstone in BPH pharmacological management.

Minimally Invasive Surgical Treatments (MISTs) are the fastest-growing segment, driven by increasing patient preference for outpatient procedures and advancements in laser and waterjet technologies. These procedures offer reduced recovery time, preservation of sexual function, and minimal risk of complications, making them attractive alternatives to traditional surgeries.

Combination Therapies provide synergistic symptom relief by combining Alpha-Blockers and 5-Alpha-Reductase Inhibitors and are commonly used in moderate to severe cases. Implantable Devices, while niche, are gaining attention in cases where pharmacotherapy fails or long-term symptom management is needed without continuous drug use.

The market covers four primary applications: Outpatient Symptom Relief, Surgical Intervention, Medication Management, and Post-Operative Care. Outpatient Symptom Relief stands out as the most prominent application area, supported by the increasing aging population and rising preference for non-invasive care options. These include the administration of oral therapies and in-office procedural solutions that significantly improve quality of life.

Surgical Intervention is the fastest-expanding application, driven by the rapid development of advanced surgical platforms such as waterjet ablation and implant-based solutions like UroLift. These interventions offer long-term symptom control with minimal side effects and are being increasingly adopted by urologists worldwide.

Medication Management remains a steady contributor, as consistent treatment protocols involving Alpha-Blockers and 5-Alpha-Reductase Inhibitors are essential in delaying disease progression. Post-Operative Care continues to play a key role in recovery, especially in complex cases, with a growing focus on pain management and continence preservation strategies.

The primary end-users in the BPH Treatment Market include Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics, and Home Healthcare Settings. Hospitals remain the dominant end-user segment, benefiting from access to a full suite of diagnostic and interventional services, specialist teams, and comprehensive post-procedure care. Their infrastructure supports both medical and surgical BPH treatment pathways, making them central to the care continuum.

Ambulatory Surgical Centers (ASCs) represent the fastest-growing end-user category. Their growth is fueled by patient demand for quick, cost-effective procedures, along with the regulatory and payer push toward outpatient care. ASCs are particularly suited for delivering minimally invasive interventions, often completed within a few hours and with same-day discharge.

Specialty Clinics, often led by urologists, contribute significantly by offering follow-up care and ongoing medication management. Meanwhile, Home Healthcare Settings are gaining traction for chronic medication adherence, teleconsultation follow-ups, and remote monitoring, especially in developed regions with aging populations.

North America accounted for the largest market share at 41.5% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

This disparity reflects maturity in procedural adoption and regulatory support across North America, while rapid demographic expansion, urbanization, and healthcare infrastructure investments are fueling Asia-Pacific’s growth trajectory. North America’s dominance is shaped by the widespread availability of minimally invasive treatments, institutional funding, and a tech-savvy patient base. Meanwhile, Asia-Pacific’s growth is propelled by rising awareness, broader healthcare access in populous nations, and robust device manufacturing activities in countries like China and India.

North America captured approximately 41.5% of the global Benign Prostatic Hyperplasia (BPH) Treatment Market in 2024, led primarily by the United States and Canada. The region’s demand is supported by a robust network of urology specialists, well-equipped hospitals, and strong outpatient care models. Key industries such as pharmaceuticals, medical devices, and insurance services are major drivers of treatment accessibility and innovation. Recent regulatory adjustments, such as broader Medicare coverage for waterjet and laser therapies, have accelerated patient access. Additionally, the adoption of AI-powered diagnostic tools and robotic-assisted surgical systems is reshaping clinical workflows, reducing procedural downtime, and elevating treatment precision across the continent.

Europe accounts for nearly 27.3% of the Benign Prostatic Hyperplasia (BPH) Treatment Market, with Germany, the United Kingdom, and France leading in consumption and procedural volume. Regulatory frameworks such as the EU Medical Device Regulation (MDR) are enforcing strict safety standards, prompting companies to invest in compliance and innovation. Sustainability directives have also encouraged the adoption of minimally invasive and reusable technologies. AI-driven patient stratification and imaging platforms are being piloted across multiple EU nations. As a result, the European market is embracing a combination of cost-efficiency, patient-centric treatment planning, and environmentally conscious technology adoption.

Asia-Pacific holds the highest growth potential in the Benign Prostatic Hyperplasia (BPH) Treatment Market, ranking second in overall volume. China, India, and Japan represent the largest consumers of pharmacological and surgical treatments, supported by aging male populations and expanding middle-class access to private healthcare. Infrastructure advancements, including high-volume diagnostic clinics and day-care surgical centers, are reshaping patient access across urban and tier-2 cities. The rise of med-tech clusters in South Korea and Singapore has further enabled rapid localization of innovative technologies. AI-based diagnostics, mobile health apps, and minimally invasive devices are becoming increasingly prevalent in regional treatment protocols.

Brazil and Argentina are the dominant players in the South America Benign Prostatic Hyperplasia (BPH) Treatment Market, contributing to a market share of approximately 6.8%. The market is primarily driven by urban healthcare systems and rising awareness among aging male populations. Brazil's public-private healthcare partnerships and Argentina’s expanded health insurance coverage have increased access to urological services. Infrastructure enhancements in urban centers are enabling broader adoption of outpatient surgical procedures. Recent health sector reforms include tax exemptions on imported medical devices, stimulating BPH technology adoption. The region also benefits from trade incentives under Mercosur agreements for cross-border medical supply chain efficiency.

The Middle East & Africa Benign Prostatic Hyperplasia (BPH) Treatment Market is emerging as a promising segment with demand driven by countries such as the UAE, Saudi Arabia, and South Africa. Regional demand is concentrated in oil-rich nations investing in world-class healthcare infrastructure. The UAE and Saudi Arabia are witnessing rapid adoption of digital urology tools and robotic surgical systems within specialty clinics and private hospitals. Public-private partnerships and favorable trade agreements are easing the entry of advanced medical devices. Local regulatory frameworks are aligning with international standards, allowing greater adoption of innovative treatments within urology-focused urban healthcare centers.

United States - 36.8% Market Share

High production capacity of medical devices and advanced outpatient care infrastructure.

China - 14.6% Market Share

Strong end-user demand and rapid expansion of urban healthcare delivery systems.

The Benign Prostatic Hyperplasia (BPH) Treatment Market is characterized by a moderately consolidated competitive environment, with more than 30 active global and regional players competing across pharmaceuticals, medical devices, and minimally invasive technologies. Industry leaders differentiate themselves through strong R&D pipelines, strategic acquisitions, product innovation, and extensive distribution networks. The market has seen an increase in strategic partnerships between device manufacturers and healthcare providers aimed at expanding outpatient surgical solutions and integrating AI-assisted technologies.

In 2023 and 2024, several companies launched next-generation minimally invasive systems featuring thermal, waterjet, and implantable options tailored for both hospitals and ambulatory surgical centers. Competition is also intensifying around AI-powered diagnostic platforms that enable precision-based procedural planning and post-treatment tracking. Innovation in combination therapies and device-drug delivery systems is also gaining momentum. Additionally, companies are expanding into Asia-Pacific and Latin America to capitalize on growing demand, often by localizing manufacturing or forming distribution alliances. The competition landscape is expected to remain dynamic as firms increasingly emphasize value-based care, real-world outcomes, and digital integration in clinical pathways.

Boston Scientific Corporation

Teleflex Incorporated

Olympus Corporation

AbbVie Inc.

Asahi Kasei Corporation

GlaxoSmithKline plc

Medtronic plc

Lumenis Ltd.

Urologix, LLC

NxThera, Inc.

Sanofi S.A.

Intuitive Surgical, Inc.

The Benign Prostatic Hyperplasia (BPH) Treatment Market is undergoing a technological transformation driven by advancements in minimally invasive surgical devices, digital diagnostics, and combination therapies. Devices such as waterjet ablation systems and steam-based therapies now dominate the procedural landscape, offering reduced recovery time, minimal invasiveness, and high procedural precision. These devices are often deployed in ambulatory surgical centers, which account for a growing share of treatment volume.

Robotic-assisted surgical platforms are increasingly integrated with AI-guided image analysis, enabling physicians to map treatment zones more accurately. This technology significantly improves outcomes by reducing unintended tissue damage and preserving erectile and urinary function. Furthermore, drug-device combination solutions—such as implantable prostatic urethral lift devices combined with localized drug elution—are gaining acceptance for long-term management in cases where oral therapies fail.

In diagnostics, real-time 3D ultrasound and MRI-based prostate mapping tools supported by machine learning are helping clinicians assess gland size, tissue density, and obstruction severity. Remote monitoring tools and wearable urinary flow meters are also emerging, offering post-procedural insights and enabling real-time patient tracking. As cloud-based health records expand, data-driven treatment personalization is expected to further redefine care delivery. These innovations position technology as a cornerstone of the market’s long-term growth strategy.

In March 2024, Boston Scientific announced the successful trial of its updated Rezūm™ 2.0 System, featuring enhanced water vapor delivery precision and reduced treatment time by 22% in outpatient procedures.

In October 2023, Teleflex launched a next-generation version of its UroLift™ delivery system with redesigned implants for improved positioning accuracy, particularly in patients with lateral lobe obstruction.

In February 2024, Intuitive Surgical introduced a BPH-specific robotic ablation module for its da Vinci system, with integrated AI that allows for automated anatomical targeting during minimally invasive procedures.

In May 2023, Olympus unveiled its new bipolar vaporization electrode for BPH treatment, reducing energy consumption by 18% and increasing procedural efficacy during TURP (transurethral resection of the prostate).

The scope of the Benign Prostatic Hyperplasia (BPH) Treatment Market Report encompasses comprehensive market insights across multiple therapeutic modalities, device technologies, regional geographies, and end-user segments. The report includes in-depth analysis of three primary treatment types—pharmacological therapies (e.g., Alpha‑Blockers, 5‑Alpha‑Reductase Inhibitors), combination drug regimens, and minimally invasive surgical treatments, such as steam ablation, waterjet resection, and implantable devices.

Geographically, the report covers major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing a granular outlook on demand patterns, treatment accessibility, regulatory dynamics, and emerging markets. End-user analysis includes hospitals, ambulatory surgical centers, specialty urology clinics, and home healthcare environments.

Applications evaluated within the report range from outpatient symptom relief and surgical intervention to medication management and post-operative recovery. The report also highlights technological advancements such as AI-enabled imaging, robotic surgery, drug-device integration, and remote monitoring solutions. Additionally, it profiles the competitive landscape, outlining key players, strategic initiatives, product innovation, and market positioning.

The report provides actionable insights for stakeholders including medical device companies, pharmaceutical manufacturers, healthcare providers, policymakers, and investors seeking to understand evolving trends, unmet needs, and growth opportunities in the global BPH Treatment Market.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Benign Prostatic Hyperplasia (BPH) Treatment Market |

| Market Revenue (2024) | USD 1,250.0 Million |

| Market Revenue (2032) | USD 1,764.1 Million |

| CAGR (2025–2032) | 4.4 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End‑User

|

| Key Report Deliverables | Revenue Forecast, Market Drivers and Challenges, Regional Outlook, Segment Analysis, Competitive Landscape, Technology Trends, Strategic Insights |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Boston Scientific Corporation, Teleflex Incorporated, Olympus Corporation, AbbVie Inc., Asahi Kasei Corporation, GlaxoSmithKline plc, Medtronic plc, Lumenis Ltd., Urologix, LLC, NxThera, Inc., Sanofi S.A., Intuitive Surgical, Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |