Reports

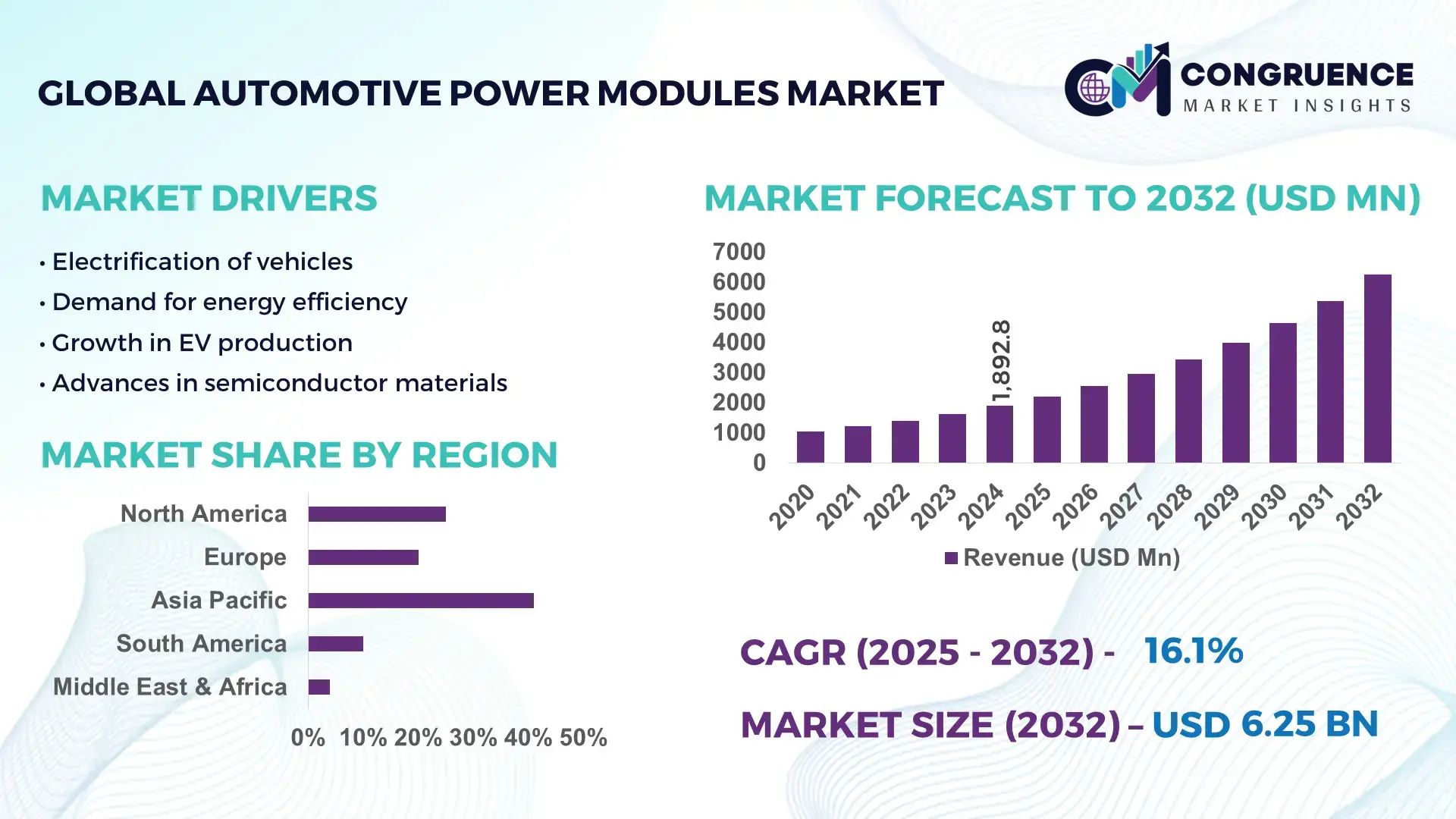

The Global Automotive Power Modules Market was valued at USD 1892.77 Million in 2024 and is anticipated to reach a value of USD 6248.23 Million by 2032 expanding at a CAGR of 16.1% between 2025 and 2032. Growth is supported by the rapid shift toward vehicle electrification and the increasing integration of high-efficiency power electronics across passenger and commercial vehicle platforms.

China functions as the largest global hub for automotive power module manufacturing and deployment. The country produces over 9 million electric vehicles annually and has established more than 15 dedicated automotive semiconductor fabrication and packaging facilities. Public and private investment in EV and power electronics infrastructure has surpassed USD 60 billion. Over 70% of domestically produced EV platforms integrate silicon carbide-based traction inverters, enabling efficiency improvements of approximately 5–7% and extending driving range by 8–10%. Power modules are primarily deployed in traction inverters, onboard chargers, and DC-DC converters, forming the core electrical architecture of next-generation electric mobility systems.

Market Size & Growth: USD 1.89 Billion in 2024, projected USD 6.25 Billion by 2032, CAGR 16.1%, driven by accelerating EV production and electrified drivetrain penetration

Top Growth Drivers: EV adoption growth 38%, power conversion efficiency improvement 12%, power density enhancement 18%

Short-Term Forecast: By 2028, inverter system cost reduction 15% and vehicle energy efficiency improvement 6%

Emerging Technologies: Silicon carbide MOSFETs, gallium nitride transistors, integrated intelligent power modules

Regional Leaders: Asia-Pacific USD 3.1 Billion, Europe USD 1.9 Billion, North America USD 1.2 Billion by 2032 with strong regulatory and infrastructure-driven adoption

Consumer/End-User Trends: OEMs prioritize high-voltage, high-efficiency modules to extend EV range and enable fast charging

Pilot or Case Example: 2024 silicon carbide inverter deployment achieved 7% range improvement and 10% thermal loss reduction

Competitive Landscape: Infineon approximately 22% share, followed by Mitsubishi Electric, Wolfspeed, ON Semiconductor, STMicroelectronics

Regulatory & ESG Impact: Emission standards, EV incentives, and carbon neutrality targets accelerate module integration

Investment & Funding Patterns: More than USD 8 Billion invested globally in power semiconductor fabs and R&D since 2022

Innovation & Future Outlook: High-voltage 800V architectures, AI-driven power management, and solid-state module development

The Automotive Power Modules Market is shaped primarily by demand from battery electric and plug-in hybrid vehicles, with traction inverters contributing roughly 45% of module demand, onboard chargers 25%, and DC-DC converters around 18%. Wide-bandgap semiconductors enable higher switching frequencies, lower losses, and compact system designs. Regional growth is strongest in Asia-Pacific, followed by Europe and North America, supported by charging infrastructure expansion, emission regulations, and government incentives. Emerging trends include ultra-fast charging systems, integrated vehicle power electronics, and modular scalable architectures for next-generation electric mobility platforms.

The Automotive Power Modules Market holds strategic relevance as a core enabler of vehicle electrification, energy efficiency, and compliance with tightening emission standards. Power modules now sit at the center of traction inverters, onboard chargers, and high-voltage DC-DC converters, directly influencing vehicle range, charging speed, thermal performance, and system reliability. Silicon carbide power modules deliver around 5–8% efficiency improvement compared to conventional silicon IGBT modules, while also enabling operation at higher temperatures and voltages, supporting 800V vehicle architectures and ultra-fast charging. Asia-Pacific dominates in volume, while Europe leads in adoption with over 65% of new electric vehicle platforms integrating advanced wide-bandgap power modules as standard components.

From a strategic standpoint, manufacturers are prioritizing vertical integration of power electronics, long-term semiconductor supply contracts, and in-house module packaging to reduce supply chain risk and protect intellectual property. By 2027, AI-based predictive thermal and load management is expected to improve power module lifespan by approximately 12% and reduce failure-related downtime by about 10%. Firms are committing to ESG improvements such as 30% reduction in production-related carbon emissions and 25% recycling of semiconductor materials by 2030, driven by regulatory pressure and corporate sustainability targets.

In 2024, China achieved a 7% vehicle range improvement through large-scale deployment of silicon carbide-based traction inverters across mass-market EV platforms. Looking forward, the Automotive Power Modules Market is positioned as a pillar of resilience, compliance, and sustainable growth by enabling cleaner mobility, supporting regulatory alignment, and strengthening the technological foundation of next-generation transportation systems.

Electric vehicle production has exceeded 14 million units globally, and each vehicle integrates multiple power modules across traction, charging, and auxiliary systems. As governments mandate lower fleet emissions and consumers shift toward zero-emission mobility, OEMs are increasing deployment of high-efficiency power electronics to extend range and reduce energy losses. The transition to higher voltage platforms further increases demand for advanced power modules capable of operating above 800V with minimal thermal degradation. This expanding functional reliance on power modules directly drives higher unit demand, wider application scope, and increased technical sophistication across the Automotive Power Modules Market.

Wide-bandgap semiconductors require specialized fabrication, advanced packaging, and strict quality controls, raising production costs by 20–30% compared to traditional silicon devices. Limited global foundry capacity and long equipment lead times restrict supply scalability. Automotive-grade certification processes also extend development cycles, delaying commercialization and increasing upfront investment. These financial and operational barriers limit adoption among cost-sensitive vehicle segments and smaller manufacturers, restraining broader market penetration despite strong long-term demand fundamentals.

Global deployment of high-power charging stations is accelerating, with tens of thousands of ultra-fast chargers already operational worldwide. These systems require advanced power modules capable of handling high voltages, fast switching, and minimal thermal losses. This creates opportunities for suppliers offering integrated, high-reliability, and compact power modules tailored for next-generation charging and grid-interactive vehicle platforms. OEM partnerships, co-development programs, and localized production facilities further expand opportunities for market participants to capture emerging demand.

Production of advanced semiconductors remains geographically concentrated, exposing the market to geopolitical risk, export controls, and logistics disruptions. At the same time, divergent safety, quality, and environmental regulations across regions increase compliance costs and complexity. Manufacturers must simultaneously meet automotive reliability standards, semiconductor process requirements, and environmental reporting obligations, raising operational burden and slowing time-to-market for new products in the Automotive Power Modules Market.

Shift toward modular and integrated power electronics architectures with 30% component reduction

OEMs are increasingly replacing discrete inverter, charger, and DC-DC designs with integrated and modular power electronics platforms. Around 48% of newly launched EV platforms in 2024 used modular power module assemblies that reduced component count by roughly 30% and wiring complexity by about 25%. This integration improves assembly efficiency, lowers vehicle weight by approximately 8–10 kg per platform, and enhances reliability by reducing interconnect failure points. Modular platforms also enable faster platform reuse across multiple vehicle models, shortening development cycles by nearly 20% and supporting scalable production strategies.

Rapid transition from silicon to wide-bandgap semiconductors reaching 42% of new designs

Silicon carbide and gallium nitride devices are increasingly replacing silicon IGBTs in high-voltage automotive systems. Approximately 42% of new EV powertrain designs now incorporate silicon carbide modules, enabling switching losses to drop by about 35% and thermal dissipation requirements to fall by nearly 20%. This transition supports higher operating voltages, faster charging, and extended vehicle range of around 5–8%, while also allowing smaller cooling systems and more compact inverter designs.

Expansion of 800V vehicle platforms with 60% faster charging capability

High-voltage architectures are becoming standard in premium and mid-range EV segments. About 38% of new EV models introduced in 2024 support 800V systems, enabling up to 60% faster charging compared to 400V platforms and reducing charging time from 40 minutes to approximately 25 minutes for comparable battery capacities. This shift directly increases demand for high-voltage-rated power modules with enhanced insulation, thermal stability, and reliability performance.

Growing focus on lifecycle efficiency and sustainability with 25% material recovery targets

Manufacturers are embedding sustainability into power module design and production. Over 40% of suppliers have adopted eco-design standards targeting 25% recovery or recycling of critical materials such as silicon, copper, and aluminum by 2030. Process optimization has already reduced manufacturing energy consumption by about 18% per module, while packaging innovations have cut material waste by approximately 15%, aligning the Automotive Power Modules Market with corporate ESG objectives and regulatory expectations.

The Automotive Power Modules Market is segmented by type, application, and end-user, reflecting how technology choices, functional deployment, and buyer profiles shape demand patterns. Type segmentation highlights the ongoing shift from traditional silicon-based modules to wide-bandgap technologies driven by efficiency, thermal, and voltage performance requirements. Application segmentation shows concentration around propulsion and charging systems, while emerging uses in energy management and safety electronics expand the addressable scope. End-user segmentation is led by automotive OEMs, but growing participation from tier-1 suppliers and charging infrastructure operators is changing procurement dynamics. Together, these segments reveal a market moving from component-centric purchasing toward system-level integration, platform standardization, and long-term technology partnerships.

Silicon-based IGBT power modules currently account for about 46% of installations, while silicon carbide modules represent around 38% and gallium nitride modules about 8%. However, adoption in silicon carbide modules is rising fastest, expected to surpass 45% by 2032, driven by their ability to reduce switching losses by around 35% and improve power density by more than 40%. The fastest-growing type is silicon carbide power modules with an estimated growth rate of about 28%, supported by expansion of 800V vehicle architectures and fast-charging infrastructure. Gallium nitride modules are gaining traction in low- to mid-power applications such as onboard chargers and auxiliary systems due to their high switching speed and compact form factor. The remaining niche types, including hybrid and advanced packaged modules, together account for roughly 8% of adoption and are used mainly in specialty or high-reliability platforms.

Traction inverters dominate applications with approximately 44% of deployment, followed by onboard chargers at 27% and DC-DC converters at 19%. However, adoption in ultra-fast charging and high-voltage conversion systems is rising fastest, expected to surpass 25% of application demand by 2032 as 800V platforms proliferate. The fastest-growing application is high-voltage onboard charging with an estimated growth rate of about 24%, supported by expansion of public fast-charging networks and consumer demand for shorter charging times. Other applications such as battery management, auxiliary power units, and thermal control electronics collectively account for around 10% and are becoming more relevant as vehicles integrate more electronic subsystems.

Automotive OEMs represent the largest end-user group with about 52% of procurement, followed by tier-1 suppliers at 31% and charging infrastructure operators at 9%. However, adoption among charging network operators is rising fastest, expected to surpass 15% by 2032 as public and private charging deployment accelerates. The fastest-growing end-user segment is charging infrastructure providers with an estimated growth rate of about 26%, driven by urban electrification programs and fleet electrification commitments. Other end-users such as public transport authorities, logistics fleet operators, and energy utilities together account for roughly 8% of demand and contribute mainly through large-volume procurement contracts.

Asia-Pacific accounted for the largest market share at 48% in 2024 however, Europe is expected to register the fastest growth, expanding at a CAGR of 18.2% between 2025 and 2032.

Asia-Pacific shipped more than 9.2 million EVs in 2024, with over 6.1 million units produced in China alone, driving high demand for traction inverters and onboard chargers. Europe accounted for 27% of installations, supported by over 3.4 million new electric vehicle registrations and mandatory fleet emission thresholds. North America represented 18%, led by strong pickup truck and SUV electrification programs. South America and the Middle East & Africa together contributed about 7%, reflecting early-stage adoption supported by government electrification initiatives and charging infrastructure programs. Regional variation is driven by differences in EV penetration, charging infrastructure density, regulatory intensity, and semiconductor manufacturing localization.

This region accounts for approximately 18% of global Automotive Power Modules demand. Key industries driving growth include passenger EV manufacturing, electric commercial fleets, and public charging infrastructure. Federal clean mobility incentives and zero-emission vehicle mandates are accelerating deployment of high-efficiency power electronics. Around 42% of newly launched EV models integrate 800V architectures, increasing demand for high-voltage modules. Local suppliers are expanding silicon carbide packaging and testing capabilities to improve thermal performance and reliability. Consumer behavior shows higher adoption in electric SUVs, fleet vehicles, and premium EV models, with over 35% of new EV buyers prioritizing fast-charging and extended range.

This region represents about 27% of the Automotive Power Modules Market, with Germany, the UK, and France accounting for over 60% of regional demand. Stringent fleet emission standards and electrification mandates drive OEM investments in efficient power electronics. Over 65% of new EV platforms integrate silicon carbide modules to meet energy efficiency and range targets. Regional sustainability frameworks require lower lifecycle emissions and material recovery targets above 25%. Consumer behavior reflects regulatory-driven purchasing, with strong preference for certified low-emission vehicles and transparent sustainability reporting.

This region ranks first by volume with approximately 48% of global installations. China, Japan, and South Korea dominate consumption and production, supported by high EV output, vertically integrated semiconductor manufacturing, and strong domestic supply chains. China alone produces more than 9 million EVs annually, driving large-scale demand for power modules. Regional innovation hubs focus on silicon carbide wafer processing, high-voltage packaging, and thermal interface materials. Consumer behavior is shaped by urban mobility, price sensitivity, and high EV penetration in metropolitan areas.

This region contributes around 4% of global demand, led by Brazil and Argentina. Public transit electrification, tax incentives on electric imports, and local assembly programs are expanding adoption. Over 12 major cities have introduced electric bus fleets, increasing demand for high-reliability traction inverters. Regional consumers focus on affordability and total cost of ownership, with fleet and municipal buyers representing a large share of early demand.

This region accounts for roughly 3% of global demand, led by the UAE, Saudi Arabia, and South Africa. Government diversification strategies emphasize clean mobility, smart cities, and advanced manufacturing. Charging infrastructure projects and electric public transport pilots are expanding module adoption. Consumers prioritize durability and high-temperature performance, reflecting climatic and infrastructure conditions.

China Automotive Power Modules Market – 34% share – dominance driven by high EV production volume and localized semiconductor manufacturing capacity

Germany Automotive Power Modules Market – 16% share – leadership supported by strong automotive OEM base and regulatory-driven electrification programs

The Automotive Power Modules Market is moderately consolidated, with approximately 35–40 active global and regional suppliers competing across silicon, silicon carbide, and gallium nitride technologies. The top five players together account for around 58% of total installations, reflecting strong concentration at the technology and scale level, while the remaining share is distributed among niche suppliers, regional manufacturers, and specialized packaging firms. Market leaders compete primarily on power efficiency, thermal performance, reliability certification, and ability to support high-volume automotive production.

Strategic initiatives are centered on expanding wide-bandgap manufacturing capacity, strengthening long-term supply agreements with automotive OEMs, and accelerating innovation in advanced packaging and thermal management. Over 60% of major suppliers have announced capacity expansions or technology upgrades since 2023, with a strong focus on 200 mm silicon carbide wafer processing, double-sided cooling, and integrated intelligent power modules. Partnerships between semiconductor manufacturers and automotive OEMs are increasing, with more than 20 formal co-development or supply agreements signed globally to secure next-generation power electronics for electric platforms.

Product differentiation increasingly depends on integration level, system-level efficiency gains, and compliance with automotive reliability standards. Around 45% of new product launches now target 800V and above architectures, while more than 30% focus on reducing module size and weight by over 20% to support compact vehicle designs. Innovation is also moving toward AI-enabled power management, digital twins for reliability testing, and lifecycle sustainability improvements, intensifying competition around both technology leadership and environmental performance.

Infineon Technologies AG

Mitsubishi Electric Corporation

STMicroelectronics

ON Semiconductor

Wolfspeed

Fuji Electric

Rohm Semiconductor

Toshiba Electronic Devices & Storage

Semikron Danfoss

Hitachi Energy

The Automotive Power Modules Market is being reshaped by rapid advances in semiconductor materials, packaging, thermal management, and system integration. The transition from silicon IGBT devices to wide-bandgap materials is the most significant technology shift, with silicon carbide now used in approximately 40% of new high-voltage electric vehicle platforms. Silicon carbide modules enable switching losses to drop by about 35%, operating temperatures to rise by 50–70°C, and system efficiency to improve by 5–8%, directly supporting 800V and higher vehicle architectures and ultra-fast charging capability. Gallium nitride is gaining adoption in onboard chargers and auxiliary power units due to its high-frequency switching and compact form factor, reducing charger size by roughly 30% and improving power density by over 40%.

Advanced packaging technologies are another critical area of innovation. Double-sided cooling, sintered silver die attach, and advanced ceramic substrates such as silicon nitride are increasingly used to improve thermal conductivity by more than 20% and extend module lifespan under high load cycles. Integration of multiple power functions into single intelligent power modules reduces wiring complexity by approximately 25% and vehicle weight by around 8–10 kg per platform. Digital twins and simulation-driven design are now applied across more than 50% of new product development programs, cutting physical prototyping time by about 20% and improving first-pass design accuracy.

Power modules are also becoming software-aware, with embedded sensors and connectivity enabling predictive maintenance, real-time thermal optimization, and remote diagnostics. Around 30% of newly released modules now include integrated temperature, voltage, and current monitoring to support AI-driven energy management and reliability forecasting. Together, these technologies are transforming power modules from passive components into intelligent, high-value systems central to the performance, efficiency, and sustainability of next-generation electric mobility platforms.

• In July 2024, onsemi signed a multi-year agreement with Volkswagen Group to supply an integrated silicon carbide-based power box solution for Volkswagen’s next-generation traction inverters, scalable across all vehicle categories and enhancing efficiency and performance for the OEM’s electric vehicles. (onsemi)

• In January 2024, Mitsubishi Electric Corporation announced the upcoming release of six new J3-Series automotive power semiconductor modules featuring silicon carbide (SiC-MOSFET) and RC-IGBT technologies, designed for more compact and efficient inverters in electric and plug-in hybrid vehicles. (Mitsubishi Electric)

• In March 2024, STMicroelectronics inaugurated a new 8-inch silicon carbide wafer fabrication facility in Catania, Italy, supported by a €730 million investment to strengthen local SiC device supply for automotive power modules and support European OEMs’ semiconductor needs.

• In 2024, ON Semiconductor completed the acquisition of SWIR Vision Systems for $295 million, enhancing its automotive sensing and integrated power module capabilities, particularly for advanced driver assistance and EV applications.

The scope of the Automotive Power Modules Market Report covers a comprehensive analysis of product types, application areas, end-user segments, geographic distribution, and emerging technologies influencing the industry. Type segmentation includes silicon IGBT, silicon carbide (SiC), and gallium nitride (GaN) modules, as well as integrated intelligent power modules tailored for traction inverters, onboard chargers, and DC-DC converters, offering decision-makers clear insights into material choices and performance trade-offs. Application segmentation assesses module usage across battery electric vehicles (BEVs), plug-in hybrids (PHEVs), commercial vehicles, and emerging electric mobility services, highlighting how functional requirements such as thermal performance, voltage ratings, and integration complexity differ by use case.

Geographic analysis spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, focusing on production hubs, consumer adoption patterns, regulatory environments, and regional manufacturing capacities. The report also examines the role of advanced semiconductor technologies — including wide-bandgap SiC and GaN — and packaging innovations such as double-sided cooling and embedded sensors, showing their impact on efficiency, reliability, and form factor. End-user insights differentiate automotive OEMs, tier-1 suppliers, and infrastructure operators, outlining procurement strategies and demand patterns.

Emerging niches such as high-voltage 800V platform adoption, wireless power transfer integration, and AI-enabled power management systems are included to provide forward-looking context. The report further evaluates industry focus areas such as sustainability targets, supply chain localization, and strategic partnerships, offering business professionals a detailed framework for understanding competitive positioning, investment priorities, and technological trajectories shaping the Automotive Power Modules landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1892.77 Million |

|

Market Revenue in 2032 |

USD 6248.23 Million |

|

CAGR (2025 - 2032) |

16.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Infineon Technologies AG , Mitsubishi Electric Corporation, STMicroelectronics , ON Semiconductor, Wolfspeed, Fuji Electric, Rohm Semiconductor , Toshiba Electronic Devices & Storage, Semikron Danfoss, Hitachi Energy |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |