Reports

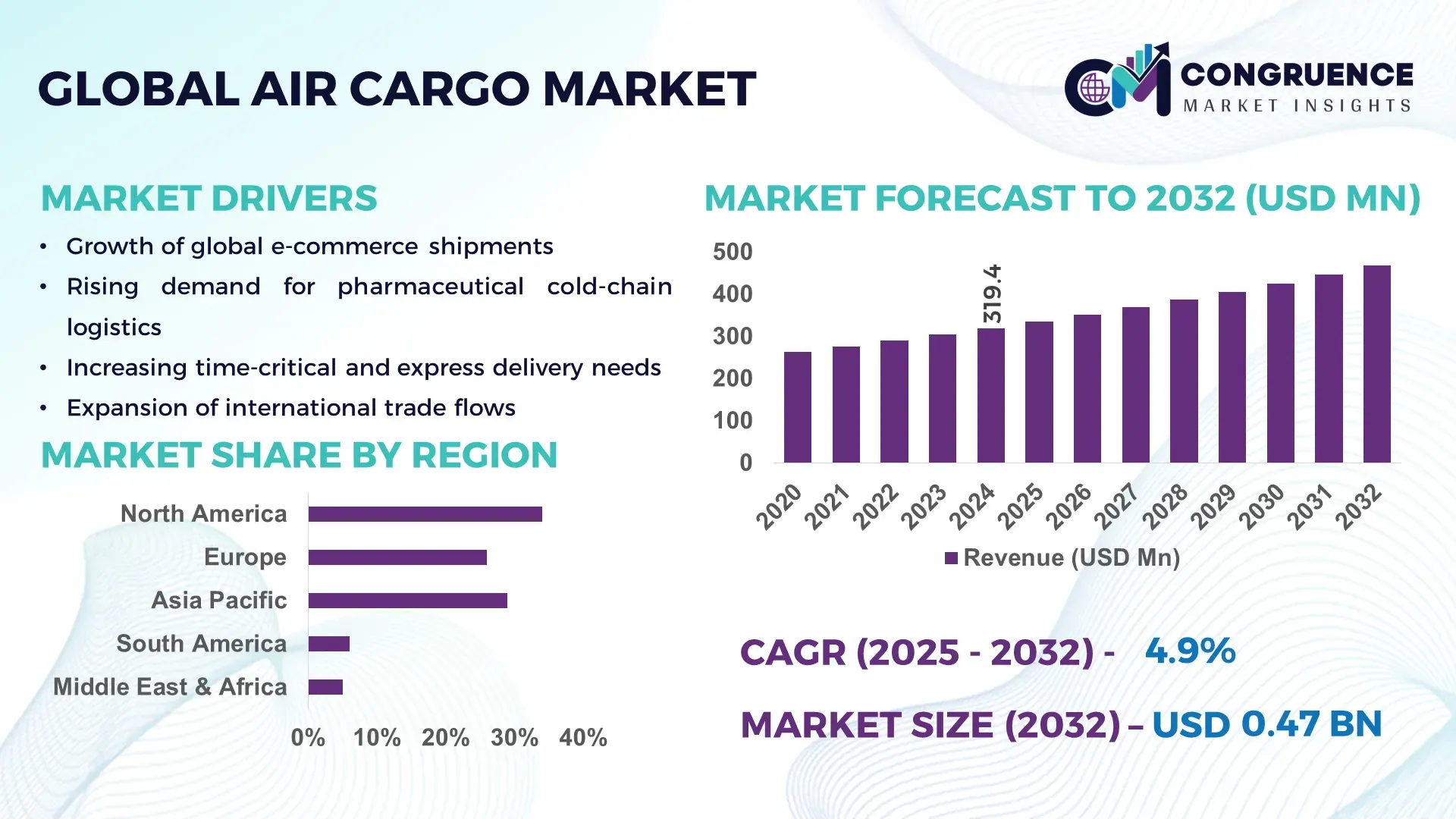

The Global Air Cargo Market was valued at USD 319.4 Million in 2024 and is anticipated to reach USD 468.3 Million by 2032, expanding at a CAGR of 4.9% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is strengthened by rising cross-border e-commerce volumes and accelerated demand for time-critical logistics.

The United States maintains a dominant position in the global Air Cargo Market due to its extensive hub-and-spoke air logistics network, advanced freight handling systems, and significant investment in temperature-controlled cargo infrastructure. The country handles over 44 million metric tons of air cargo annually, supported by highly automated sorting technologies, over 9,500 dedicated cargo aircraft movements per day, and robust cold-chain capabilities serving pharmaceuticals, electronics, aerospace, and perishables. Strategic airport modernization programs and digital cargo operations further strengthen its operational advantage.

Market Size & Growth: Market valued at USD 319.4 million in 2024, projected to reach USD 468.3 million by 2032, expanding at 4.9% CAGR; driven by increased demand for time-critical international shipments.

Top Growth Drivers: 38% rise in cross-border e-commerce adoption; 22% improvement in air-freight handling efficiency; 31% adoption surge in cold-chain cargo solutions.

Short-Term Forecast: By 2028, automated cargo handling systems expected to boost throughput efficiency by 27%.

Emerging Technologies: AI-enabled cargo routing, digital air-freight marketplaces, and autonomous ground-handling vehicles entering operational deployment.

Regional Leaders: By 2032, North America expected to reach USD 128 million, Asia-Pacific USD 142 million, and Europe USD 97 million, each showing strong digital logistics adoption trends.

Consumer/End-User Trends: High adoption from pharmaceuticals, electronics, and fast-fashion sectors driven by speed-sensitive delivery needs.

Pilot or Case Example: In 2024, a cargo-automation pilot at a major Asian hub achieved a 34% reduction in handling downtime.

Competitive Landscape: Market leader holds approx. 18% share; key competitors include FedEx, UPS, DHL Aviation, Qatar Airways Cargo, and Emirates SkyCargo.

Regulatory & ESG Impact: Global regulations promoting carbon-efficient aircraft and sustainable fuel use are accelerating green cargo operations.

Investment & Funding Patterns: Over USD 6.4 billion invested recently in air-cargo infrastructure, automation, and digital freight technologies.

Innovation & Future Outlook: Advancements in predictive analytics, smart cargo containers, and AI-integrated logistics expected to define next-generation air-freight systems.

The Air Cargo Market is increasingly shaped by high-tech industries such as pharmaceuticals, semiconductors, and precision engineering, contributing over 42% of specialized cargo volume. Recent innovations like temperature-adaptive containers, AI-enabled freight monitoring, and ultra-efficient wide-body aircraft are accelerating operational performance. Sustainability regulations, evolving customs standards, and expanding trade corridors continue to reshape global cargo flows, supporting resilient long-term growth.

The Air Cargo Market plays a central role in global trade, enabling rapid international transport of high-value and time-sensitive goods. Its strategic relevance is growing as industries increasingly demand fast, reliable, and digitally optimized logistics. Modern cargo operations are integrating AI-driven route optimization, predictive maintenance, and autonomous ground-handling to enhance operational efficiency, ensuring measurable performance improvements across the supply chain. For example, next-generation cargo management systems deliver up to 29% improvement compared to legacy manual processing frameworks, reducing delays and improving load accuracy.

Regional dynamics demonstrate further complexity. Asia-Pacific dominates in volume, supported by its vast manufacturing ecosystem, while Europe leads in digital adoption with nearly 61% of enterprises utilizing advanced cargo-automation systems. These trends highlight the shift toward region-specific strengths that shape global cargo flows.

Short-term outlooks reflect accelerated technology penetration. By 2027, AI-driven logistics orchestration is expected to cut ground-handling delays by 24%, significantly improving shipment turnaround. At the same time, supply-chain sustainability is becoming an operational requirement. Firms are committing to 30% CO₂-efficiency improvements by 2030, supported by sustainable aviation fuel (SAF) adoption and energy-efficient aircraft technologies.

Real-world scenarios further validate this trend. In 2024, a major European carrier achieved a 32% reduction in cargo processing time through an AI-enabled load sequencing initiative, demonstrating tangible efficiency gains. These advancements reinforce the position of the Air Cargo Market as a cornerstone of global resilience, compliance, and sustainable economic growth, driving forward the next decade of logistics transformation.

The Air Cargo Market is shaped by evolving global trade patterns, rising e-commerce activity, and increasing demand for quick, reliable, and temperature-controlled logistics. Industry dynamics are driven by modernization of cargo terminals, the introduction of digital freight platforms, and a growing focus on operational automation. Additionally, the expansion of high-value sectors like pharmaceuticals, electronics, and automotive components continues to influence air-freight preferences. Changes in global supply chains, trade regulations, and multi-modal transport integration further define market behavior, creating opportunities for higher efficiency, reduced turnaround times, and strengthened cargo visibility across transport nodes.

The surge in pharmaceutical, biotech, and temperature-sensitive product movement is significantly influencing the Air Cargo Market. Growing volumes of vaccines, biologics, and precision-medicine shipments require stringent temperature maintenance—between 2°C and 8°C for nearly 70% of medical cargo. Air logistics ensures compliance through specialized containers, cold rooms, and advanced tracking. With more than 2.5 million temperature-controlled tonnes transported annually, carriers are expanding refrigerated storage capacity and investing in active cooling technologies. Enhanced shipment reliability, reduced spoilage incidents, and improved real-time monitoring capabilities further accelerate adoption of air-based transport among pharmaceutical manufacturers, reinforcing the sector’s structural role in air-freight demand.

Air cargo capacity constraints—particularly at major global hubs—pose significant operational challenges. Airports in high-density regions experience congestion, with peak-hour slot limitations affecting aircraft movements and cargo throughput. Ground-handling delays exceed 18% during high-volume seasons, causing shipment backlogs. Limited cold-storage availability restricts pharmaceutical and perishable cargo handling, while labor shortages in ramp operations and cargo-terminal workforces further reduce operational efficiency. Additionally, regulatory compliance checks, security screening requirements, and customs clearance delays extend total processing times. These challenges slow cargo turnaround, increase operational costs, and hinder market responsiveness, creating supply-chain friction for time-sensitive goods.

Digitalization offers substantial opportunity for efficiency gains across the Air Cargo Market. Adoption of digital airway bills (e-AWB) has expanded to over 80% globally, reducing document-processing times by up to 45%. AI-enabled cargo-planning tools improve load optimization accuracy by 20–30%, while smart containers equipped with IoT sensors enhance real-time temperature and vibration monitoring. Integration of blockchain for secure documentation tracking provides additional transparency for high-value shipments. As airports modernize operations, investments in automated ground-handling equipment and robotic pallet movers are rising, offering airlines and freight forwarders improved reliability, reduced errors, and faster cargo flow across terminals.

Escalating operational costs—from aircraft maintenance to airport storage fees—continue to challenge air-cargo profitability. Fuel expenses represent a major cost driver, with fluctuations exceeding 30% year-to-year, affecting airline planning and cargo pricing. Compliance with global security standards requires investment in advanced screening technologies, increasing processing expenditures. Environmental regulations mandate the adoption of cleaner aircraft engines and sustainable aviation fuel, adding further cost layers. Moreover, geopolitical disruptions, trade-policy shifts, and fluctuating international freight rates create uncertainty for long-term planning. These challenges necessitate continuous modernization investment and strategic cost-optimization measures across carriers and cargo operators.

AI-Driven Cargo Optimization: AI-enabled routing and load-planning platforms are transforming operational efficiency, enabling up to 28% improvement in cargo load accuracy and 19% faster turnaround scheduling. Predictive analytics solutions are monitoring over 50,000 daily freight movements, ensuring tighter capacity planning and reducing unutilized space across major hubs.

Expansion of Temperature-Controlled Logistics: Advanced cold-chain solutions are expanding rapidly, with over 3.2 million tonnes of sensitive cargo requiring temperature regulation annually. New temperature-adaptive containers demonstrate 18% lower spoilage rates, while airport cold-room capacity has increased by 22% in key pharmaceutical export corridors.

Automation in Ground Handling: Automated cargo handling systems and robotic pallet movers are gaining adoption, delivering 25% reduction in manual labor hours and 31% improvement in cargo-sorting speed. More than 110 airports are deploying autonomous tugs to streamline apron operations, reducing operational delays significantly.

Digital Freight Platforms & Real-Time Visibility: Digital marketplaces now handle over 40% of spot air-freight bookings, improving price transparency and reducing booking times by 60%. IoT-equipped smart containers provide continuous monitoring, capturing more than 200 data points per shipment, improving operational control and cargo security.

The segmentation of the Air Cargo Market is shaped by product type, application, and end-user characteristics that together determine operational focus, infrastructure investment, and service design. Types range from belly-hold freight on passenger aircraft to dedicated freighters, integrator/express services, charter operations, and specialized temperature-controlled solutions; each type demands different handling, ground equipment, and regulatory compliance. Applications span express e-commerce shipments, pharmaceuticals and cold-chain logistics, electronics and high-value components, perishables, and industrial machinery, driving distinct routing and storage needs. End-users include e-commerce retailers, manufacturers, healthcare providers, integrators, and government/defense logistics; these users differ in frequency, payload composition, and service-level expectations. Segmentation influences capacity planning (aircraft mix and terminal design), investment priorities (cold rooms, automation), and service packaging (guaranteed time-windows, insurance, visibility). Decision-makers should align fleet and terminal strategy to the dominant segment mixes in their target lanes, prioritizing digital visibility and specialized handling capabilities where temperature control and high-value goods are concentrated.

The primary product types in the air-cargo ecosystem are: Belly-hold cargo (on passenger aircraft), Dedicated freighter services, Integrator/express carrier services, Temperature-controlled (cold-chain) solutions, Charter services, and Mail/parcel consolidated offerings. Belly-hold cargo remains the leading type, accounting for approximately 45% of total volume due to large passenger flight networks that provide consistent belly capacity on established trade lanes. Dedicated freighters follow, essential for outsized or heavy consignments and long-haul routes. The fastest-growing type is temperature-controlled (cold-chain) logistics, driven by rising pharma and perishable shipments; it is expanding at an estimated CAGR of 7.2%, reflecting investments in active container systems and cold-room capacity. Other types—integrator services, charter operations, and mail/parcel consolidation—collectively represent the remaining 30% and serve niche needs such as guaranteed time-definite delivery, ad-hoc capacity, and small-parcel aggregation.

Applications in the Air Cargo Market include express e-commerce and parcel delivery, pharmaceuticals and life-sciences logistics, high-value electronics and semiconductors, perishables (fresh food and flowers), industrial and aerospace components, and emergency/relief shipments. Express e-commerce is the leading application, representing roughly 40% of shipment count because of the high frequency and parcelized nature of online retail flows; its prominence is reinforced by dense point-to-point networks and integrator hub models. The fastest-growing application is pharmaceutical and temperature-sensitive shipments, supported by cold-chain innovation, unique packaging, and compliance requirements; this segment is expanding with an estimated CAGR of 8.1% as healthcare supply chains globalize. Other applications—electronics, perishables, industrial parts, and emergency logistics—make up the remaining 32%, each contributing to lane-specific capacity and handling profiles. Consumer and enterprise adoption statistics reflect accelerating digital and specialized adoption: in 2024, over 38% of enterprises globally reported piloting advanced air-cargo tracking and monitoring systems for customer experience platforms; and more than 60% of major distributors now prefer certified active-container solutions for temperature-sensitive loads.

End-users of air cargo services include e-commerce platforms and retailers, pharmaceutical and biotech companies, electronics manufacturers, automotive and aerospace OEMs, fresh-food exporters, integrators/forwarders, and government agencies. E-commerce retailers are the leading end-user segment, accounting for about 36% of air-cargo shipments by piece-count, driven by consumer demand for fast fulfillment and frequent small-parcel movements. The fastest-growing end-user group is pharmaceutical and biotech firms, with an estimated CAGR of 9.4% for their demand profile as biologics, cold-chain clinical supplies, and temperature-sensitive consignments proliferate. Other end-users—electronics, automotive parts, perishables exporters, and government relief operations—collectively contribute the remaining 34%, each shaping lane characteristics (e.g., night-flight preferences for perishables, priority slots for aerospace parts). Adoption statistics reinforce these patterns: in 2024, more than 38% of enterprises reported piloting advanced cargo-visibility and exception-management platforms; and a survey of logistics buyers showed 42% of large hospitals in one economy testing dedicated air-freight pharma supply corridors for time-critical deliveries.

North America accounted for the largest market share at 34% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

North America handled more than 21 million tonnes of air freight in 2024, supported by high-value trade lanes and extensive airport automation. Asia-Pacific followed closely with 31 million tonnes of throughput driven by e-commerce acceleration. Europe maintained 26% share, anchored by major hubs processing over 18 million tonnes annually. South America and the Middle East & Africa jointly contributed around 9%, supported by rising cross-border trade, perishables transport, and infrastructure expansion. Regional disparities reflect variations in manufacturing density, digital adoption, regulatory frameworks, temperature-controlled capabilities, and investment cycles—all of which shape freight flows and demand patterns.

North America represents one of the most advanced air-cargo regions globally, holding approximately 34% of total volume in 2024. Demand is primarily driven by pharmaceuticals, aerospace components, electronics, and fast-growing e-commerce shipments. Regulatory support, including enhanced customs automation and security screening modernization, continues to streamline freight flows. Digital transformation is prominent, with AI-enabled cargo routing, automated sortation systems, and autonomous ramp vehicles becoming standard in major hubs. Leading players such as FedEx have expanded their express cargo sorting capacity, processing over 19 million packages per day in peak periods. Enterprises in healthcare and finance show higher adoption of advanced tracking and monitoring systems, reflecting a preference for transparency and real-time visibility. Consumer behavior also favors fast, guaranteed delivery, resulting in strong demand for premium air-freight services.

Europe accounted for roughly 26% of global air-cargo volume in 2024, with leading markets including Germany, the United Kingdom, and France, together handling more than 12 million tonnes of freight. Strong regulatory oversight, including emissions-reduction targets and sustainable aviation fuel (SAF) adoption frameworks, is influencing fleet renewal and ground operations. Technology adoption remains high, with increased deployment of automated cargo-handling machinery and digital air-freight booking platforms. Major carriers and logistics operators in the region continue to invest in temperature-controlled facilities to support pharmaceuticals and perishable goods. A notable regional player expanded its Frankfurt hub capacity by 15% to meet growing demand for high-value cargo. European consumers demonstrate strong preference for transparent, compliant, and environmentally conscious logistics solutions, reinforcing demand for traceable and explainable operational workflows.

Asia-Pacific is the largest air-cargo processing region by volume, handling more than 31 million tonnes in 2024. Top consuming countries—China, India, Japan, and South Korea—contribute the bulk of regional throughput due to strong manufacturing ecosystems, export-heavy industries, and rapidly expanding e-commerce sectors. Growing investments in mega-airport cargo complexes, automation, and AI-driven freight-management systems support rising demand. Innovation hubs in Singapore, Shenzhen, and Tokyo are accelerating the digitalization of freight operations, with increasing deployment of robotics and IoT-enabled tracking. A key regional airline recently expanded its widebody freighter fleet by 20%, boosting lane capacity for electronics and pharmaceuticals. Consumer behavior reflects high mobile-commerce adoption, with more than 70% of online buyers prioritizing fast delivery options that rely heavily on air-freight networks.

South America’s air-cargo market is anchored by Brazil, Argentina, and Chile, collectively accounting for around 6% of global volume in 2024. Brazil remains the primary hub due to its large industrial base, agricultural exports, and growing demand for temperature-controlled logistics. Regional cargo flows are shaped by trade policies promoting export diversification and improved customs procedures. Energy, mining, and agribusiness sectors generate significant outbound freight, while infrastructure investments continue to upgrade airport cargo handling by 12–18% in key hubs. A major Brazilian airline expanded its cargo network to 110+ destinations, supporting rapid parcel and perishables delivery. Consumer preferences in the region show strong reliance on localized digital commerce platforms and increasing demand for language-adapted logistics solutions across cross-border markets.

The Middle East & Africa region represented approximately 5% of global air-cargo throughput in 2024, supported by strong demand from oil & gas, construction materials, automotive components, and perishables. Key growth countries include the UAE, Saudi Arabia, Kenya, and South Africa, each investing heavily in logistics corridors, free-trade zones, and multimodal connectivity. Technological modernization—such as AI-led cargo tracking, smart warehousing, and automated documentation—is expanding across major hubs. A leading carrier in the Gulf region enhanced its cargo-terminal handling capacity by 25%, improving regional transit flows. Regulatory partnerships promoting faster customs clearance and integrated trade systems also support cross-border freight. Consumer behavior trends show increasing adoption of digital shopping, especially in urban centers, boosting express parcel movement.

United States – 18% Market Share: Dominance attributed to advanced cargo infrastructure, high-tech manufacturing shipments, and extensive express-delivery networks.

China – 15% Market Share: Driven by strong export capacity, large-scale manufacturing output, and rapidly expanding e-commerce-driven freight volumes.

The Air Cargo Market is intensely competitive, comprising over 150 active participants including major cargo airlines, global integrators, freight forwarders, and regional carriers. Market structure is moderately consolidated at the top—with the largest integrators and national flag carriers commanding significant lane control—but remains fragmented across regional and niche operators serving specialized lanes (perishables, pharma, outsized cargo). Top strategic moves in 2023–2024 included fleet renewals and freighter orders, network expansions, major digitalization alliances, and capacity reconfigurations: for example, global integrators announced fleet modernizations and hub investments, while traditional carriers pursued freighter buys and lease extensions to secure long-haul capacity. Recent consolidation and restructuring initiatives reflect this dynamic (e.g., major operational consolidations announced by a leading US carrier in 2024). Innovation trends—AI route optimization, automated sortation, active cold-chain containers, and digital freight marketplaces—are reshaping competitive positioning; several carriers reported double-digit improvements in handling throughput following automation pilots.

The marketplace exhibits a hybrid nature: a few large players exercise strong global reach, while hundreds of regional specialists capture lane-specific demand. The combined share of the top 5 companies is estimated in the mid-40s percent range, reflecting significant but not overwhelming concentration and leaving space for regional specialists and integrators to compete on service niches, time-definite operations, and value-added handling. Strategic initiatives include partnerships with robotics/AI firms, deployment of electric/alternative-fuel ground fleets, new freighter orders, and targeted investments in temperature-sensitive infrastructure—moves that materially affect capacity, turnaround times, and service reliability.

DHL

UPS

DHL Aviation

Cathay Pacific Cargo

Cargolux

Lufthansa Cargo

Korean Air Cargo

Technological advancements are fundamentally reshaping the Air Cargo Market, with operators prioritizing systems that improve efficiency, reliability, and visibility across the logistics chain. AI and predictive analytics now support dynamic routing, demand forecasting, and predictive maintenance, enabling carriers to reduce idle time and improve load factor accuracy—several AI-driven load sequencing pilots have reported double-digit improvements in handling precision and reductions in misloads. Automation and robotics are increasingly integrated into cargo terminals, where automated sortation lines, robotic pallet movers, and autonomous apron vehicles are delivering 20–30% gains in throughput. Parallel advancements in active cold-chain technologies—including smart, temperature-controlled containers and IoT sensor networks—help reduce thermal excursions and strengthen compliance for pharmaceutical and perishable shipments. Digital freight platforms and electronic airway bills (e-AWB) continue to streamline booking and documentation, leading to measurable reductions in processing delays, while blockchain-based document security pilots enhance traceability for high-value consignments. Sustainability-focused technologies are also accelerating, particularly AI-based fuel-efficiency optimization tools, fleet modernization strategies, and systems supporting the handling and planning of Sustainable Aviation Fuel (SAF). For decision-makers, the convergence of automation hardware with AI-driven orchestration software creates multiplicative operational gains, improving capacity utilization and enabling premium, service-differentiated cargo products such as guaranteed cold-chain lanes and high-precision express services.

In mid-2024 FedEx announced a major consolidation of operating companies to streamline operations and cut redundancies, with plans to combine key operating units into a single global organization to enhance efficiency and cost structure. Source: www.fedex.com

In June 2024 UPS placed over 100 new electric vehicles in Paris, part of a broader rollout of 600+ EVs slated for deployment across European urban centers by year-end to reduce tailpipe emissions and operate in zero-emission zones. Source: about.ups.com

In fiscal 2023–24 Qatar Airways Cargo reported increased lift with a chargeable weight tonnage figure exceeding 1.56 billion kg, marking operational scale gains and continued digitalization of its cargo services. Source: www.gulf-times.com

In 2024 Emirates announced firm orders and lease extensions for Boeing 777 freighters (including a recent confirmation to buy five 777Fs) and is pursuing fleet expansion and conversions to bolster long-haul cargo capacity. Source: www.reuters.com

This Air Cargo Market Report covers the operational, technological, commercial, and regulatory dimensions of global air freight and cargo services. The scope includes: detailed segmentation by service type (belly-hold, dedicated freighters, integrator/express services, charters, temperature-controlled/cold-chain solutions, mail/parcel consolidation); application areas (e-commerce/express parcel, pharmaceuticals and life sciences, electronics and semiconductors, perishables, industrial/aerospace parts, emergency logistics); and end-user categories (e-retailers, manufacturers, healthcare providers, integrators/forwarders, governments). Geographically, the report analyses regional dynamics across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with country-level profiles for leading markets and an assessment of hub capacities, throughput volumes, and infrastructure investments.

The report examines technology vectors—automation, AI/predictive analytics, digital freight marketplaces, active cold-chain systems, e-AWB adoption, blockchain pilots, and sustainability enablers (SAF logistics and fleet modernization)—and maps these to operational KPIs such as handling throughput, dwell time, temperature-excursion rates, and on-time delivery performance. Competitive coverage includes a profiling of major global integrators, cargo airlines, and freight forwarders, analysis of market concentration (top-player share ranges), and strategic initiatives (fleet orders, partnerships, digital alliances). The work also contains actionable chapters for decision-makers: investment opportunities (terminal automation, cold-chain expansion), regulatory & ESG compliance frameworks, risk scenarios (capacity constraints, geopolitical shocks), and go-to-market strategies for carriers and logistics providers seeking lane expansion or premium service verticals. Niche and emerging segments—such as pharma-clinical trials logistics, oversized/outsized cargo corridors, and same-day express air lanes—are also covered, giving stakeholders an operationally focused blueprint for capacity planning, technology investment, and commercial positioning.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 319.4 Million |

| Market Revenue (2032) | USD 468.3 Million |

| CAGR (2025–2032) | 4.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers, Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Regulatory Overview |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | FedEx, Emirates SkyCargo, Qatar Airways Cargo, DHL, UPS, DHL Aviation, Cathay Pacific Cargo, Cargolux, Lufthansa Cargo, Korean Air Cargo |

| Customization & Pricing | Available on Request (10% Customization Free) |