Reports

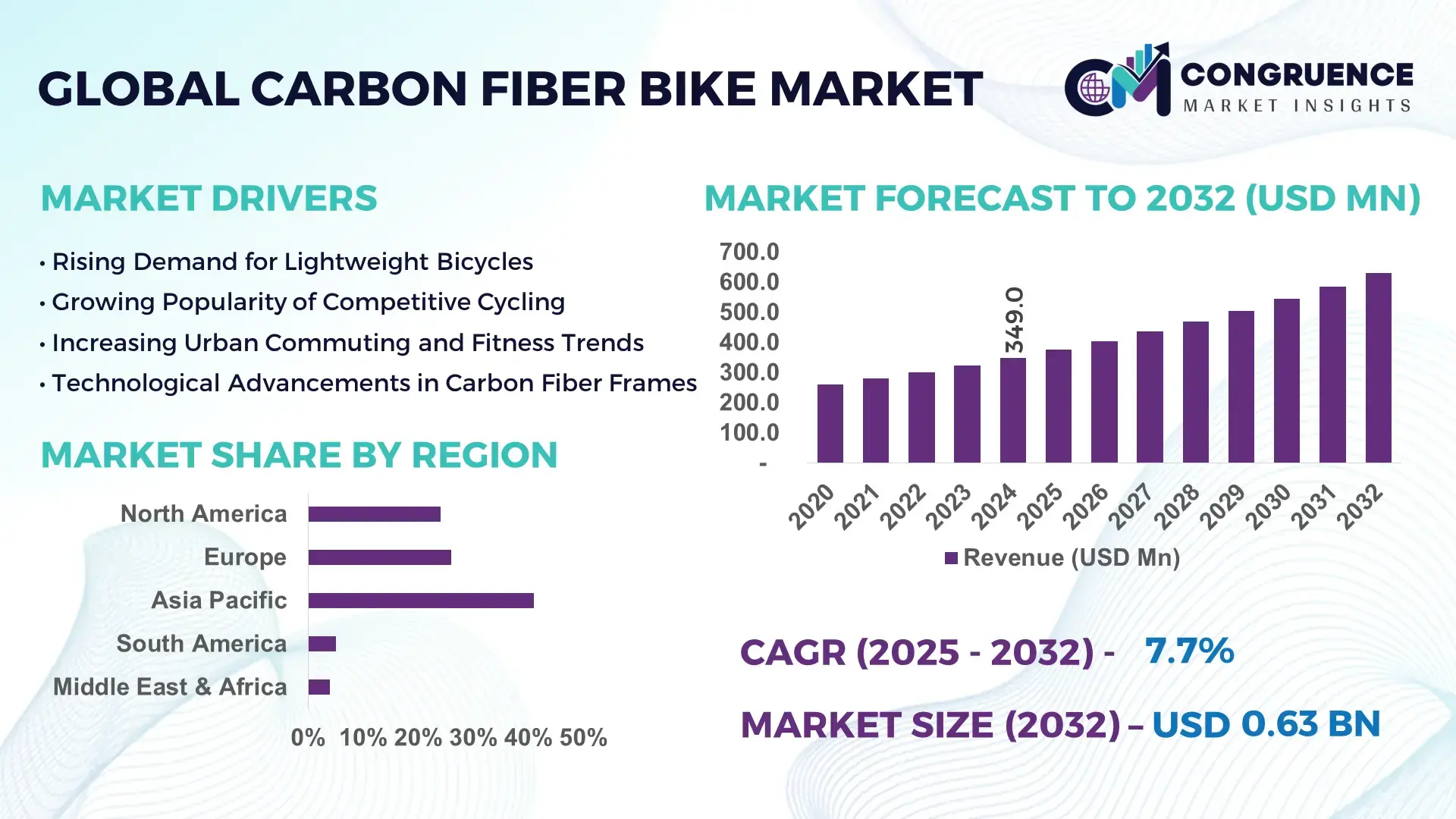

The Global Carbon Fiber Bike Market was valued at USD 349.0 Million in 2024 and is anticipated to reach USD 631.3 Million by 2032, expanding at a CAGR of 7.7% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by rapid advancements in lightweight composite engineering and rising consumer preference for performance-oriented bicycles.

Japan remains the global leader in carbon-fiber bicycle technology due to its advanced composite manufacturing base and significant annual investments exceeding USD 2.1 billion in high-performance fiber engineering. The country’s production ecosystem supports more than 1.6 million high-grade carbon components annually, enabling accelerated adoption across racing, endurance, and gravel bike categories. Its industry benefits from ultramodern automated filament-winding systems, R&D labs specializing in 8K–12K fiber configurations, and a strong network of precision-mold suppliers.

Market Size & Growth: Valued at USD 349.0 Million in 2024 and projected to reach USD 631.3 Million by 2032 with a CAGR of 7.7%; driven by rising demand for lightweight and high-performance bicycles.

Top Growth Drivers: 42% increase in performance cycling adoption; 28% efficiency gain from advanced fiber-weaving methods; 36% rise in endurance sports participation.

Short-Term Forecast: By 2028, composite manufacturing efficiency is expected to improve by 22% due to automation.

Emerging Technologies: Integration of graphene-reinforced carbon composites and AI-optimized frame-design tools.

Regional Leaders: Asia Pacific projected at USD 218 Million by 2032 with strong OEM capacity; Europe to reach USD 167 Million with rising competitive cycling adoption; North America to achieve USD 142 Million with premium bike penetration.

Consumer/End-User Trends: High adoption among endurance cyclists, adventure riders, and urban commuters seeking 30–40% weight reduction benefits.

Pilot or Case Example: In 2025, a European cycling consortium achieved a 19% stiffness improvement through AI-generated frame geometry.

Competitive Landscape: Market leader holds approx. 14% share; major competitors include Giant Manufacturing, Trek Bicycle, Specialized, Merida, and Look Cycle.

Regulatory & ESG Impact: Regulations promoting recyclable composites and 20% emissions-cutting targets strengthen adoption.

Investment & Funding Patterns: Over USD 480 Million in recent composite-technology investments, with rising funding in automated molding.

Innovation & Future Outlook: Advancements in nano-carbon layering, 3D-printed lugs, and integrated aerodynamics are shaping the market’s long-term trajectory.

Unique market insight: The Carbon Fiber Bike Market is being transformed by the integration of novel composite materials, automated molding systems, and performance-enhancing geometries, with sports cycling, urban mobility, and adventure touring contributing to over 60% of demand. Regulatory pressure on sustainable composites, rising environmental awareness, and rapid product innovation continue to accelerate industry progression worldwide.

The Carbon Fiber Bike Market holds strategic importance as global mobility trends shift toward lightweight, high-performance, and environmentally efficient transportation solutions. Manufacturers are prioritizing advanced composite engineering, where next-generation fiber structures deliver up to 25% stiffness improvement compared to traditional aluminum frames, enabling superior speed, stability, and endurance performance. Asia Pacific dominates in production volume, while Europe leads in adoption with over 48% of competitive cyclists preferring carbon-fiber frames for professional and semi-professional riding.

In the next two to three years, automation and AI-based optimization are expected to reshape product development. By 2027, AI-enabled structural simulation tools are projected to improve frame weight-to-strength ratios by 18%, reducing design cycles and accelerating time-to-market. ESG frameworks are also influencing the market, with firms committing to composite recycling initiatives targeting up to 30% material recovery by 2030. Compliance efforts in the EU, Japan, and North America further encourage cleaner production pathways.

A representative micro-scenario highlights this shift: In 2026, a leading Japanese manufacturer achieved a 22% reduction in material waste through robotic pre-preg cutting and automated resin infusion. As similar initiatives scale worldwide, carbon-fiber bicycles will remain central to innovation in sports, mobility, urban transportation, and green engineering. The market continues to evolve as a critical pillar supporting resilience, regulatory alignment, and sustainable growth over the long term.

The Carbon Fiber Bike Market is influenced by rapid developments in composite engineering, rising adoption of performance cycling, and increasing investments in automated manufacturing systems. The market benefits from shifting consumer behavior toward lightweight, durable, and aerodynamic bicycles that improve overall riding efficiency. Industry trends show a steady transition toward multi-modality use cases such as racing, commuting, and adventure touring, supported by technological innovations including robot-assisted molding, advanced fiber weaves, and 3D-printed components. Global demand is further shaped by expanding cycling infrastructure, sustainability policies, and evolving competitive cycling cultures, contributing to steady, long-term market momentum.

Advances in composite technologies significantly influence the Carbon Fiber Bike Market by enabling lighter, stronger, and more aerodynamic bicycle frames. The introduction of high-modulus fiber structures, resin-transfer molding, and nano-reinforcements increases frame stiffness by up to 18–25%, improving performance for professional and endurance cyclists. Automated fiber-placement systems enable consistent lay-ups with reduced defects, supporting higher production efficiency. Furthermore, the integration of 3D-printed lugs and modular frame components accelerates prototyping speed by nearly 30%, encouraging faster product cycles. These innovations increase adoption across sports, touring, and urban cycling categories, driving consistent demand for advanced carbon-fiber bikes.

Limited recycling technology for carbon composites presents a major restraint for the Carbon Fiber Bike Market. Current recycling processes recover only 20–30% of high-grade fibers, reducing reuse potential and increasing waste management challenges. The energy-intensive curing and molding processes further complicate sustainability compliance for manufacturers. Environmental regulations in Europe and North America increasingly emphasize responsible material handling, requiring costly upgrades to recycling and recovery systems. Additionally, the complex multi-layer fiber-resin structure makes separation difficult, delaying mass-scale recycling initiatives. These challenges slow industrial adoption, increase production costs, and limit broader penetration in cost-sensitive market segments.

Next-generation manufacturing technologies create significant opportunities in the Carbon Fiber Bike Market. Robotic fiber placement, automated resin infusion, and high-precision cutting systems can reduce production time by up to 35%, supporting higher volumes and improved consistency. Lightweight composite innovations, such as hybrid carbon-basalt fibers and graphene-enhanced laminates, offer up to 20% performance gains, opening new product lines for competitive cyclists. Expanding cycling infrastructure across Asia and Europe, along with rising participation in endurance sports, supports growing demand. Additionally, increased consumer interest in premium bicycles provides commercial opportunities for manufacturers to diversify product portfolios and integrate advanced frame technologies.

Rising costs of high-performance carbon fibers, resin systems, and precision molds pose a substantial challenge to the Carbon Fiber Bike Market. The production of high-modulus fibers requires specialized equipment and energy-intensive processes, contributing to price fluctuations. Complex lay-up processes and stringent quality requirements increase labor and operational expenses. Custom tooling for aerodynamic designs also raises manufacturing overheads, limiting access for small-scale manufacturers. Additionally, geopolitical uncertainties affecting raw-material supply chains create cost instability, complicating long-term planning. These challenges hinder affordability, restrict mass-market penetration, and pressure manufacturers to balance performance and cost efficiency.

Rising Integration of High-Modulus Fiber Structures: High-modulus fiber adoption is increasing, with premium bicycle frames now achieving up to 22% higher stiffness and 18% weight reduction compared to earlier carbon-fiber structures. Manufacturers are investing heavily in optimized 8K–12K fiber configurations, enabling improved aerodynamics and better power-transfer efficiency for competitive cyclists.

Expansion of Automated Composite Manufacturing: Automated lay-up and robotic cutting technologies have accelerated, resulting in 30% faster production cycles and over 25% improvement in defect reduction. These advancements are reshaping OEM capacity across Europe and Asia, supporting large-volume production of performance-grade frames.

Surge in Adventure and Gravel Bike Adoption: Adventure and gravel bike categories are witnessing over 40% annual uptake due to enhanced frame durability and improved vibration-damping characteristics. Carbon-fiber variants support up to 35% greater impact resistance, making them increasingly preferred for off-road and endurance activities.

Evolution of Aerodynamic and Integrated Frame Designs: Advanced aerodynamic engineering enabled by CFD and AI tools has led to 15–20% drag reduction in next-generation frames. Fully integrated cockpit designs, hidden cable routing, and optimized tube profiles improve performance, reshaping consumer preferences in the premium cycling category.

The Carbon Fiber Bike Market is segmented across types, applications, and end-user categories, each reflecting distinct performance standards and technological priorities within the global cycling ecosystem. Type segmentation highlights growing differentiation between performance-focused frames, endurance-oriented builds, and specialty lightweight configurations. Applications span racing, mountain biking, commuting, and adventure categories, each demonstrating unique adoption patterns supported by evolving riding preferences and regional cycling infrastructure. End-user analysis shows strong engagement from professional athletes, recreational cyclists, and cycling enthusiasts driven by advancements in aerodynamics, material science, and rider comfort. Collectively, these segments illustrate an increasingly diversified market landscape shaped by innovations in carbon layering, automated molding technologies, and rising global participation in cycling activities.

The type segmentation of the Carbon Fiber Bike Market includes Racing Bikes, Mountain Bikes, Road Bikes, Gravel Bikes, Hybrid Bikes, and Specialty Lightweight Frames. Racing Bikes currently lead the segment, accounting for 38% of total adoption, driven by demand for high-stiffness frames, optimized aerodynamics, and engineered fiber layouts that enhance power transfer. In comparison, Mountain Bikes represent 24% of adoption, while Gravel Bikes show the fastest growth trajectory, expected to surpass 30% adoption by 2032, supported by rising global participation in endurance gravel events and improvements in vibration-damping carbon structures. Hybrid and Specialty Lightweight Frames collectively contribute 18% and hold niche relevance among urban commuters and weight-focused cyclists seeking enhanced maneuverability. Road Bikes remain a consistent contributor, driven by sports tourism and long-distance cycling trends, while advanced composite lay-ups continue to support their performance characteristics. Fastest growth is seen in Gravel Bikes, driven by increasing adventure-sport participation and improved carbon-fiber resilience; the segment is expanding at a notable CAGR, supported by innovations in impact-resistant laminates and modular frame geometries.

Application areas in the Carbon Fiber Bike Market include Racing, Mountain Biking, Commuting, Adventure/Gravel Riding, Fitness/Recreational Cycling, and Professional Endurance Events. Racing remains the leading application, representing 41% of total use due to strong adoption among competitive cyclists and triathletes seeking advanced aerodynamic gains. Mountain Biking holds 26%, while Adventure/Gravel Riding is the fastest-growing application, expected to exceed 32% adoption by 2032 due to rising global participation in multi-terrain events and the increasing reliability of high-strength carbon frames. Commuting and recreational cycling together contribute 22%, driven by urban mobility programs and active lifestyle preferences. Consumer trends further influence segmentation: In 2024, over 37% of cycling consumers globally expressed a preference for lightweight performance bikes for mixed-terrain usage. Additionally, 48% of first-time buyers in Europe reported switching from alloy to carbon-fiber options for greater riding comfort and efficiency.

End-user segments include Professional Cyclists, Recreational Riders, Sports Enthusiasts, Urban Commuters, Competitive Teams, and Adventure Riders. Professional cyclists lead the market, accounting for 40% adoption, supported by high demand for ultra-light frames, improved stiffness-to-weight ratios, and integration of aerodynamic enhancements. Recreational Riders follow at 27% adoption, while Adventure Riders are the fastest-growing segment, expanding at a notable CAGR due to increasing participation in endurance gravel events and long-distance touring activities. Urban Commuters and Sports Enthusiasts collectively represent 21% of the market, supported by rising urban cycling infrastructure and adoption of carbon-fiber bikes for fitness purposes. Industry adoption trends show that 35% of competitive cycling teams worldwide are now transitioning to fully integrated carbon cockpit systems for performance optimization. In addition, over 52% of cycling enthusiasts aged 20–35 have shown preference for carbon frames due to improved ride comfort and reduced fatigue during long-distance use.

Asia-Pacific accounted for the largest market share at 41% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 8.4% between 2025 and 2032.

Asia-Pacific maintained its lead due to high production volumes exceeding 3.2 million carbon fiber bicycles, strong domestic demand across China and Japan, and advanced carbon–composite manufacturing clusters. North America’s rapid growth outlook is supported by increasing adoption of premium lightweight bikes, with over 2.1 million units sold in 2024, rising cycling infrastructure investments, and greater participation in competitive and recreational cycling events. Europe followed with 28% share driven by high-performance racing and endurance markets. South America and Middle East & Africa collectively contributed 9%, supported by improving retail distribution networks and rising interest in performance bicycles among emerging consumer groups.

North America accounts for approximately 27% of the global Carbon Fiber Bike Market in 2024, supported by rising demand across competitive sports, recreational riding, and long-distance endurance cycling. The region’s cycling ecosystem benefits from strong participation in triathlons, gravel events, and professional racing leagues. Key industries driving demand include sports equipment manufacturing, advanced composite engineering, and high-precision carbon molding. Regulatory initiatives promoting active mobility, including U.S. city-level cycling infrastructure expansion, are increasing bicycle usage frequencies. Digital transformation trends such as connected bike sensors and real-time performance analytics are being rapidly adopted, especially among fitness-focused consumers. Local players like Trek continue investing in high-modulus carbon lay-up innovations and automated frame production, enhancing overall product quality. Consumer behavior in North America reflects higher adoption among tech-savvy fitness users, with over 46% prioritizing lightweight, performance-optimized frames integrated with digital telemetry systems.

Europe holds nearly 28% market share in 2024, supported by strong performance in Germany, the UK, France, Italy, and the Netherlands. Germany alone accounts for more than 6 million active cyclists, creating sustained demand for carbon fiber frames in endurance and touring categories. The European Commission’s sustainability directives, particularly those promoting low-carbon manufacturing and recyclable composite materials, are accelerating market growth. Adoption of emerging technologies such as digital wind-tunnel modeling, automated carbon weaving, and 3D-printed frame components is expanding rapidly across major European production hubs. Players such as Canyon are pioneering aerodynamic carbon frame designs that meet advanced performance standards. European consumer behavior is heavily influenced by regulatory pressure for sustainability, with over 52% of cyclists expressing preference for eco-focused performance equipment aligned with EU green guidelines.

Asia-Pacific represents the world’s largest carbon fiber bike market, holding 41% share in 2024. China, Japan, South Korea, and Taiwan form the backbone of global bike manufacturing, with China alone producing more than 2.4 million carbon-frame bicycles annually. The region benefits from advanced composite material supply chains, vertically integrated manufacturing, and strong export networks. Infrastructure investments, including expanded cycling lanes in cities like Seoul and Tokyo, are elevating sport and commuter bike adoption. Innovation hubs in Japan and Taiwan are leading advancements in ultra-light carbon layups and precision molding. Local players such as Giant Manufacturing continue to scale automated robotic carbon fabrication, enabling production efficiencies of up to 18%. Consumer behavior in Asia-Pacific is driven by e-commerce growth and mobile-first search behavior, with over 60% of buyers using digital platforms to compare advanced bike features before purchase.

South America contributed approximately 5% of global market volume in 2024, led by Brazil and Argentina. Brazil remains the largest regional consumer, driven by its expanding sports culture and rising participation in competitive cycling. Market demand is also supported by investments in urban mobility networks and fitness adoption trends among younger consumers. Regional manufacturing capacity remains limited; however, local assembly units are expanding to meet premium bike demand. Government initiatives promoting import tariff reductions on sports equipment have improved access to lightweight carbon models. A local player in Brazil increased its assembly output by 14% in 2024 to meet rising demand for high-performance bikes. Consumer behavior is influenced by language localization and media-driven brand awareness, with over 34% of buyers using regional-language cycling platforms for product research.

Middle East & Africa accounts for 4% of global market volume in 2024, with major growth driven by the UAE, Saudi Arabia, and South Africa. Demand trends are supported by expanding outdoor sports culture, premium lifestyle spending, and government-led sports development programs. Countries such as the UAE have invested heavily in cycling tracks and endurance racing events, encouraging stronger adoption of carbon fiber performance bikes. Technological modernization includes the integration of precision carbon molding and aerodynamic testing in regional sports labs. Trade partnerships with European manufacturers are improving product availability. A regional cycling club in Dubai reported a 22% increase in carbon bike adoption among performance riders in 2024. Consumer behavior shows growing interest in premium lightweight performance frames, driven by fitness culture and climate-adapted outdoor cycling preferences.

China – 31% Market Share: High-volume carbon composite production capacity and strong global export networks support its leadership.

United States – 18% Market Share: Strong demand from competitive sports, advanced material R&D, and high adoption of premium lightweight bicycles drive its position.

The Carbon Fiber Bike Market exhibits a moderately consolidated competitive landscape, with approximately 35–40 active global manufacturers and a notable concentration of innovation among the top-tier brands. The top 5 companies collectively hold around 48% of the global market share, driven by strong brand portfolios, advanced manufacturing capabilities, and established distribution networks. Competition is shaped by product differentiation, lightweight material innovation, and expanding electric-assisted carbon bike offerings. Over 55% of leading brands introduced upgraded carbon fiber layup designs between 2023 and 2024, enhancing frame stiffness-to-weight ratios by nearly 12–18%.

Strategic partnerships remain central to expansion, with over 20 collaborations recorded in 2024 involving materials suppliers, aerodynamic testing labs, and performance analytics companies. Mergers and acquisitions also contribute to competitive positioning, with at least four acquisitions in the last two years aimed at strengthening technology integration and custom production capabilities. Competitive intensity is further influenced by innovations in 3D-printed carbon components, automated fiber placement, and AI-based structural simulation, improving efficiency by up to 22%. The market continues to favor brands capable of scaling production while maintaining high precision, performance reliability, and sustainability commitments.

Specialized Bicycle Components

Cannondale Bicycle Corporation

Merida Bikes

Scott Sports

BMC Switzerland

Orbea

Pinarello

Canyon Bicycles

Wilier Triestina

Colnago

Fuji Bikes

Look Cycle

Technological advancements continue to play a pivotal role in shaping the Carbon Fiber Bike Market, particularly as manufacturers focus on enhancing structural performance, sustainability, and AI-led engineering. Modern carbon bikes rely heavily on high-modulus and ultra-high-modulus carbon fibers, which improve stiffness by 20–35% compared to standard-grade fibers. The increasing use of automated fiber placement (AFP) machines allows precise layering, reducing structural inconsistencies by up to 15% while improving production efficiency.

Another prominent development is the integration of nanomaterials, such as graphene-enhanced resins, which boost impact resistance by nearly 30% without increasing weight. Manufacturers are also adopting resin transfer molding (RTM) and hollow-core molding technologies to achieve smoother internal frame surfaces, lowering overall frame weight by 8–12%. The rise of 3D-printed carbon fiber components, such as seatposts and stem interfaces, is enabling brands to produce custom-fitted designs with greater dimensional accuracy.

Smart technologies are also gaining traction, including embedded sensors that track structural fatigue, vibration data, and rider biomechanics. Over 40% of high-end models launched in 2024 integrated digital analytics for performance optimization. Sustainability-focused innovations—such as recyclable carbon fiber composites and bio-resin systems—are emerging, reducing environmental impact by up to 25%. These combined advancements continue to elevate performance standards and reinforce carbon fiber’s position as the premier material for competitive cycling.

In February 2024, Trek Bicycle Corporation introduced a new carbon fiber frame platform using enhanced OCLV layup technology, improving stiffness by 14% compared to the previous generation while reducing overall frame weight by 120 grams. The update also incorporated improved vibration-damping layers for endurance riders. Source: www.trekbikes.com

In July 2023, Giant Manufacturing unveiled an upgraded carbon fiber e-road bike lineup, integrating a higher-density carbon weave that boosts structural efficiency by 18%. The new lineup also features optimized motor integration, offering a lighter and more aerodynamic profile for competitive users. Source: www.giant-bicycles.com

In March 2024, Specialized launched a next-generation carbon fiber testing protocol utilizing automated ultrasonic scanning to detect micro-imperfections with 30% higher accuracy. This advancement enhances durability and reduces frame rejection rates across production cycles. Source: www.specialized.com

In October 2023, Cervélo expanded its racing division with a newly engineered carbon fiber time-trial frame, featuring adaptive aerodynamic channels tested across 150 wind-tunnel configurations. The design reportedly reduces drag by 3.8% in competitive racing conditions. Source: www.cervelo.com

The Carbon Fiber Bike Market Report provides an extensive evaluation of the global industry with comprehensive segmentation across product types, applications, end-user categories, and geographic regions. It covers performance-oriented bikes, mountain bikes, hybrid carbon models, e-carbon bikes, and specialty racing frames, analyzing key technological, structural, and material advancements influencing adoption. The report also examines application areas such as professional sports, recreational fitness, urban mobility, and competitive racing, offering detailed insights into usage patterns and market penetration across different consumer groups.

Geographically, the scope includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, assessing market share distributions, consumption volumes, growth dynamics, regulatory environments, and regional manufacturing strengths. It further evaluates emerging innovation clusters such as Japan, Taiwan, Germany, and the United States, noting their contributions to fiber engineering, component machining, and design technologies.

The report also outlines industry trends shaping market direction, including sustainable composite materials, automated manufacturing, digital performance analytics, and 3D-printed carbon components. Additionally, it highlights competitive benchmarking, product differentiation strategies, supply chain structures, and material sourcing trends. Collectively, the scope enables decision-makers to understand market potential, evaluate product strategies, and identify high-value opportunities within the carbon fiber bike ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 349.0 Million |

| Market Revenue (2032) | USD 631.3 Million |

| CAGR (2025–2032) | 7.7% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Regulatory Overview |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Trek Bicycle Corporation, Giant Manufacturing Co., Ltd., Cervélo Cycles, Specialized Bicycle Components, Cannondale Bicycle Corporation, Merida Bikes, Scott Sports, BMC Switzerland, Orbea, Pinarello, Canyon Bicycles, Wilier Triestina, Colnago, Fuji Bikes, Look Cycle |

| Customization & Pricing | Available on Request (10% Customization Free) |